|

Christopher

Hayward

Finance

Director

4

World Financial Center

North

Tower

New

York, New York 10080

(212)

449-0778

|

|

|

Christopher

Hayward

Finance

Director

4

World Financial Center

North

Tower

New

York, New York 10080

(212)

449-0778

|

|

Re:

|

Merrill

Lynch & Co., Inc.

|

|

Form

10-K for the Fiscal Year ended December 29, 2006

|

|

|

Forms

10-Q for the Fiscal Quarters ended March 30, 2007 and June 29,

2007

|

|

|

File

No. 1-7182

|

|

1.

|

Where

a comment below requests additional disclosures or other revision to be

made, please show us in your response what the revisions will look like in

your future filings.

|

|

2.

|

You

disclosed that you have less liquid financial instrument assets of

approximately $22 billion and financial instrument liabilities of $9

billion that you valued using management’s best estimate of fair value and

using a model where either the inputs to the model and/or the models

themselves require significant judgment by management. You also

disclosed that in applying these models you consider such factors as

projected cash flows, market comparables, volatility, and various market

inputs. Given the apparent subjectivity involved in determining

the valuation of these less liquid financial instruments, please consider

disclosing in greater detail the types of models used as well as the key

inputs and estimates used in each of these models. Please

consider disclosing whether or not there have been any changes in the

models or methods used in the valuations. Please also consider

providing a sensitivity analysis which shows the potential impact of

adverse changes in the key inputs and estimates used in each of these

models.

|

|

|

a)

|

Quoted

prices for similar assets or liabilities in active markets (for example,

restricted stock);

|

|

|

b)

|

Quoted

prices for identical or similar assets or liabilities in non-active

markets (examples include corporate and municipal bonds, which trade

infrequently);

|

|

|

c)

|

Pricing

models whose inputs are observable for substantially the full term of the

asset or liability (examples include most over-the-counter derivatives

including interest rate and currency swaps);

and

|

|

|

d)

|

Pricing

models whose inputs are derived principally from or corroborated by

observable market data through correlation or other means for

substantially the full term of the asset or liability (examples include

certain residential and commercial mortgage related assets, including

loans, securities and derivatives).

|

|

3.

|

We

have reviewed your responses to prior comments 3 and 13. We

note the additional disclosures you intend to provide solely related to

exposure from credit default swaps on U.S. super senior ABS

CDOs. We continue to believe that you should provide additional

disclosures regarding the remaining areas of exposure related to credit

default swaps. Please consider addressing the

following:

|

|

|

·

|

Disclosing the types of credit

exposures that you hedge;

|

|

|

·

|

Disclosing the credit ratings

of the counter-parties involved in the credit default swaps and the

related dollar amounts

hedged;

|

|

|

·

|

Disclosing the likelihood of a

potential downgrade to the sellers of the credit default swaps and the

impact that such a downgrade could have on your valuation of credit

default swaps;

|

|

|

·

|

Disclosing the average duration

of your credit default swap assets and liabilities by type of credit

rating;

|

|

|

·

|

Disclosing whether you hold any

collateral on your credit default swaps;

and

|

|

|

·

|

Disclosing concentrations of

credit risks as required by paragraph 15A of SFAS 107. In this

regard, please tell us the metric that you used to define a material

concentration of credit

risk.

|

|

|

·

|

To economically hedge certain

of our ABS CDO and U.S. sub-prime mortgage exposures, we entered into

credit default swaps with various counterparties, including financial

guarantors. At December 28, 2007, our short exposure from credit

default swaps with financial guarantors to economically hedge certain

U.S. super senior ABS CDOs was $13.8 billion, which represented

credit default swaps with a notional amount of $19.9 billion that

have been adjusted for mark-to-market gains of

|

|

·

|

Concentration

of Risk to the U.S. Sub-Prime Residential Mortgage

Market

|

|

|

·

|

Net exposure of

$2.7 billion in U.S. sub-prime residential mortgage-related

positions, excluding Merrill Lynch’s U.S. banks investment security

portfolio;

|

|

|

·

|

Net exposure of

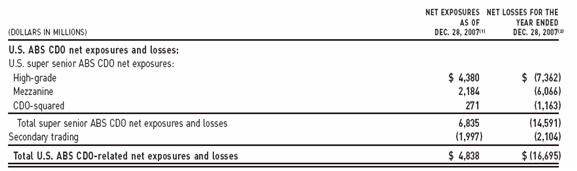

$4.8 billion in super senior U.S. ABS CDOs and secondary trading

exposures related to the ABS CDO business;

and

|

|

|

·

|

Net exposure of

$4.2 billion in sub-prime residential mortgage-backed securities and

U.S. ABS CDOs held in Merrill Lynch’s U.S. banks’ investment

portfolio.

|

|

4.

|

On

a weekly basis, your CODM receives the Global Markets and Investment

Banking Weekly Highlights Report which includes revenue, compensation

expense, non-compensation expense, pre-tax earnings, and after-tax

earnings for each of the businesses included in your Global Markets and

Investment Banking segment. These businesses are as

follows:

|

|

|

·

|

Fixed income, currency and

commodities;

|

|

|

·

|

Equity markets;

and

|

|

|

·

|

Investment

Banking

|

|

5.

|

Please

provide us with the following reports based off Appendix II of

your response:

|

|

|

·

|

Merrill Lynch’s 2008 Operating

Plan

|

|

|

·

|

All of the Merrill Lynch &

Co’s Daily earnings Summaries provided to the CODM during the month of

December 2007 and December

2006

|

|

|

·

|

Presentations to the Executive

Committee provided during or related the three months ended December 28,

2007 and December 29, 2006;

|

|

|

·

|

Presentations to the Board of

Directors provided during or related to the three months ended December

28, 2007 and December 29,

2006;

|

|

|

·

|

GMI Weekly Highlight Report

provided to the CODM during the month of December 2007 as well as during

the months of December 2005 and December 2006;

and

|

|

|

·

|

Financial Summary to the Board

of Directors provided related to December 2007 and December

2006.

|

|

6.

|

Please

address the comments above in your interim filings as

well.

|

|

7.

|

We

have reviewed your response to prior comment 10. Please

consider expanding your disclosures related to the interests you retain

from sub-prime residential mortgage securitizations to discuss the key

assumptions used to value your retained interests as well as to provide a

sensitivity analysis specifically related to these retained interests

similar to the analysis included on page 37 of your Form

10-Q.

|

|

8.

|

We

are still evaluating your response to prior Comment

8.

|

|

9.

|

We

have reviewed your response to prior comments 11 and 12. Given

the significant write-downs taken in the third and fourth quarters of

2007, we continue to believe that you should quantify and disclose each

significant component of the $2.0 billion net decrease in other net

changes in net exposures as well as quantify and reconcile the difference

between the gross and net exposure to U.S. sub-prime residential

mortgage-related exposures. Please also consider disclosing

what led to the decrease of approximately $500 million in hedges (short

positions) which resulted in an increase in the net exposure related to

residential mortgage-backed

securities.

|

|

10.

|

We

have reviewed your response to prior comment 14. It does not

appear that your press release dated January 17, 2008 includes a

presentation of your gross exposures to CDO positions. Please

tell us what consideration you gave to presenting your gross exposures to

CDO positions in addition to your current presentation of net

exposures. For example, an additional table could reconcile

from your gross exposures to your net CDO exposures, with corresponding

explanations for the significant reconciling

items.

|

|

11.

|

We

have reviewed your response to prior comment 15. It does not

appear that your press release dated January 17. 2008 specifically

addresses risks and exposures to non-U.S. sub-prime residential

mortgage-related and ABS CDO positions in a similar manner to your

discussion of the U.S. market beginning on page 73 of your Form

10-QSB. Please tell us what consideration you gave to providing

these disclosures.

|

|

|

·

|

U.S.

Alt A mortgages

|

|

|

·

|

U.S.

Prime mortgages

|

|

|

·

|

Non-U.S.

mortgages and

|

|

|

·

|

Mortgage

servicing rights

|

|

|

·

|

U.S. Alt-A: We had net exposures of

$2.7 billion at the end of 2007, which consisted primarily of

residential mortgage-backed securities collateralized by Alt-A residential

mortgages. These net exposures resulted from secondary market trading

activity or were retained from our securitizations of Alt-A residential

mortgages, which were purchased from third-party mortgage originators. We

do not originate Alt-A mortgages.

We

view Alt-A mortgages as single-family residential mortgages that are

generally higher credit quality than sub-prime loans but have

characteristics that would disqualify the borrower from a traditional

prime loan. Alt-A lending characteristics may include one or more of the

following: (i) limited documentation; (ii) high

combined-loan-to-value (‘‘CLTV”) ratio (CLTV greater than 80%);

(iii) loans secured by non-owner occupied properties; or

(iv) debt-to-income ratio above normal

limits.

|

|

|

·

|

U.S. Prime: We had net exposures of

$28.2 billion at the end of 2007, which consisted primarily of prime

mortgage whole loans, including approximately $12 billion of prime

loans originated with GWM clients and $9.7 billion of prime loans

originated by First Republic, an operating division of Merrill Lynch Bank

& Trust Co., FSB (“MLBT-FSB”). We also purchase prime whole loans from

third-party originators for securitization and for the investment

portfolios of Merrill Lynch Bank USA (“MLBUSA”) and

MLBT-FSB.

|

|

|

·

|

Non-U.S.: We had net exposures of

$9.6 billion at the end of 2007 which consisted primarily of

residential mortgage whole loans originated in the United Kingdom, as well

as through mortgage originators in the Pacific

Rim.

|

|

|

·

|

Mortgage

Servicing Rights:

We own approximately $400 million of mortgage servicing rights which

represent the right to current and future cash flows based on contractual

servicing fees for mortgage loans. In connection with our residential

mortgage businesses, we may retain or acquire mortgage servicing rights.

See Note 6 to the Consolidated Financial Statements for further

information.

|

|

12.

|

In

your January 17, 2008 press release you disclosed that you had a net

exposure to Alt-A residential mortgages of $2.7 billion and Alt-A

residential mortgage-backed securities in the amount of $7.1 billion at

December 31, 2007. Please consider expanding your disclosures

to address the risks and exposures to Alt-A residential mortgage assets

and investment securities to include the

following:

|

|

|

·

|

Your definition and a

description of what you consider to be Alt-A

loans;

|

|

|

·

|

Your underwriting policies for

Alt-A loans;

|

|

|

·

|

Your risk management policies

with respect to Alt-A loans

|

|

|

·

|

Your gross and net exposure to

Alt-A residential mortgages and mortgage-backed securities with a

corresponding reconciliation between the gross and net amounts and an

explanation of the significant reconciling items;

and

|

|

|

·

|

The models and methods used to

value amounts related to Alt-A loans as well as the key inputs and

estimates used in each of these models. Please disclose whether

or not there have been any changes in the models or methods used in the

valuations. Please also provide a sensitivity analysis which

shows the potential impact of adverse changes in the key inputs and

estimates used in these

models.

|

|

13.

|

In

your January 17, 2008 press release you disclosed a net exposure to U.S.

prime real estate mortgage assets of $28.2 billion and prime residential

mortgage-backed securities of $4.2 billion as of December 28,

2007. In light of the weaker U.S. housing market, please

consider disclosing the risks and exposures to loss arising from your

prime mortgage related exposures. Please also consider

disclosing your gross as well as net exposures as well providing any

additional disclosures which will provide additional insight on your

exposures.

|

|

Sincerely,

/s/Christopher

Hayward

Christopher

Hayward

Finance

Director

Principal

Accounting Officer

|

|

cc:

|

Gus

Rodriguez, Staff Accountant

|

|

Nudrat

Salik, Staff Accountant

|

|

|

Nelson

Chai, Chief Financial Officer

|