UNITED

STATES

SECURITES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

NOTICE

OF EXEMPT SOLICITATION

|

|

1.

|

Name

of the Registrant:

|

BANK OF

AMERICA CORPORATION

|

|

2.

|

Name

of the person relying on exemption:

|

FINGER

INTERESTS NUMBER ONE, LTD.

|

|

3.

|

Address

of person relying on exemption:

|

520 Post

Oak Blvd., Suite 750, Houston, TX 77027

|

|

4.

|

Written

Materials. Attach written material required to be submitted pursuant to

Rule 14a-6(g)(1).

|

Dear

Shareholder:

We have

modified the Powerpoint Presentation on our website, www.bacProxyVote.com. The

updated Powerpoint Presentation is attached, and incorporates many of the slides

that were in different sections of our website. Also,

we believe the graphs at the end of the Powerpoint presentation are of

particular significance.

We continue to urge you to VOTE

AGAINST three directors that are standing for re-election at the Annual

Meeting of Bank of America on April 29, 2009:

Vote

AGAINST the election of KENNETH D. LEWIS to the board of directors

Vote

AGAINST the election of O. TEMPLE SLOAN, JR. to the board of

directors

Vote

AGAINST the election of JACKIE M. WARD to the board of directors

SLIDESHOW

PRESENTATION TO FELLOW

SHAREHOLDERS

SHAREHOLDERS

UPDATED

MARCH 25, 2009

www.BACPROXYVOTE.com

Table

of Contents

— Our Thesis / Our

Goals

Pages 3-4

— The Case For

Change Page

5

— Risky &

Overpriced Acquisitions Pages

6-11

— Credit Risk

Assumed through Acquisitions Pages

12-14

— Concealed

Information on Merrill Acqusition Pages

15-16

— Securities Law

Questions

Pages 17-19

— Our Goals Page

20

— Actions taken to

Date

Page 21

— Appendix - Graphs

(important)

÷ Permanent

Destruction of Shareholder Value Pages

22-25

www.BACPROXYVOTE.com

2

Our

Thesis

— Management has

embarked on a program of premium

priced and high risk acquisitions, with the consent and

support of the board of directors.

priced and high risk acquisitions, with the consent and

support of the board of directors.

— Misguided Emphasis

on size, market share and “footprint”

rather than Tangible Book Value, Return on Equity,

Earnings Per Share and Protecting Shareholder Value.

rather than Tangible Book Value, Return on Equity,

Earnings Per Share and Protecting Shareholder Value.

— These actions by

management and the board have caused

shareholder dilution that will result in the Permanent

Destruction of Shareholder Value.

shareholder dilution that will result in the Permanent

Destruction of Shareholder Value.

— Thus, the Board

has failed in its primary duty to

shareholders to protect and preserve shareholder value.

shareholders to protect and preserve shareholder value.

www.BACPROXYVOTE.com

3

Our

Goals

— We are long-term

holders of 1.1 MM shares of BAC stock since 1996.

We want to improve the Company and its governance.

We want to improve the Company and its governance.

— We are focused on

Accountability to shareholders. This

board

collectively failed to function properly as a decision making body that

was responsible for protecting the interests of shareholders, first and

foremost.

collectively failed to function properly as a decision making body that

was responsible for protecting the interests of shareholders, first and

foremost.

— We are seeking to

change the culture of corporate governance at the

Company, so that the board of directors oversees management more

firmly and fulfills its duty to shareholders.

Company, so that the board of directors oversees management more

firmly and fulfills its duty to shareholders.

— For the April 29

Annual Meeting, we recommend shareholders:

¡ Vote “Against” 3

directors - Ken Lewis, Temple Sloan, Jackie Ward

(Item 1)

¡ Vote to Separate

Chairman & CEO position (Item 8)

¡ Vote to Limit

Executive Compensation (Items 3, 5, 11)

www.BACPROXYVOTE.com

4

The

Case for Change

• Risky and

Overpriced Acquisitions

• Assumption of

Massive Credit risk Through Acquisitions

• We believe

Management & Board Concealed Information

from Shareholders About Losses at Merrill Lynch prior to

December 5th merger vote

from Shareholders About Losses at Merrill Lynch prior to

December 5th merger vote

• Possible

Violations of Securities Laws regarding disclosure

of Material Information related to new TARP Funds and

Merrill Q4 losses

of Material Information related to new TARP Funds and

Merrill Q4 losses

• Prior knowledge

regarding significant bonus payments to

Merrill executives

Merrill executives

• The above actions

have resulted in Permanent Destruction

of Shareholder Value

of Shareholder Value

www.BACPROXYVOTE.com

5

Risky

and Overpriced Acquistions

— LaSalle

Acquistion

— Countrywide Acquisition

— Merrill Lynch

Acquisition

www.BACPROXYVOTE.com

6

LaSalle

Acquisition

— Full Price

Paid

¡ 20.3x LTM

Earnings

¡ Cash Acquisition -

no common equity issued in transaction

¡ Over $11 BN of

Goodwill created by Transaction

¡ Tangible Book

Value Dropped by $3.5BN due to goodwill

created + lack of common equity issued

created + lack of common equity issued

¡ Tangible Common

Equity / Assets fell from 3.5% at 9/30/07 to

2.99% at 12/31/07

2.99% at 12/31/07

¡ Poorly Executed

Transaction

÷ Assumption of

Large Commercial Loan Book

÷ Multiple

Management Defections / Lost Clients

¡ Thus, Dilutive to

Shareholders

www.BACPROXYVOTE.com

7

Countrywide

Acquisition

— Unknown Litigation

Risk / Costs Prior to Close

¡ 5 States Attorney

General Suits Prior to Closing

¡ At least 6

Subsequent AG Suits

¡ October 2008

Agreement with 11 Attorneys General to modify

$8.4Billion in Loans, 400,000 borrowers

$8.4Billion in Loans, 400,000 borrowers

¡ $220Million

Reserved for Settlements to Date

— Very Negative

Impact to Tangible Capital Ratios

¡ Tangible Common

Equity drops from $46.6BN at 6/30/08 to

$24.8BN at 9/30/08 due to $4.1 BN increase in goodwill and

$16 BN increase in “other intangibles” (including mtg. serv. rights)

$24.8BN at 9/30/08 due to $4.1 BN increase in goodwill and

$16 BN increase in “other intangibles” (including mtg. serv. rights)

¡ Tangible Common

Equity ratio drops from 4.62% of total

assets at 6/30/08 to 2.6% of total assets at 9/30/08

assets at 6/30/08 to 2.6% of total assets at 9/30/08

www.BACPROXYVOTE.com

8

Merrill Lynch

Acquisition #1

— Inability to do

Due Diligence

¡ Less than 48 hours

of negotiations and Due Diligence

¡ If due diligence

was attempted, it was inadequate and faulty

¡ Offer price per

share = 60% premium to prior closing share

price in unstable and declining stock markets

price in unstable and declining stock markets

÷ Pending failure of

Lehman

÷ Frozen Credit

Markets

÷ Funding

Uncertainty for Broker Dealer Firms

¡ Significant Credit

Risk Assets Acquired, and yet:

÷ Did they have time

& expertise to evaluate assets and risks?

÷ Did they properly

assess their ability to hedge risks assumed?

www.BACPROXYVOTE.com

9

Merrill Lynch

Acquisition#2

— Before factoring

in unexpected Q4 writedowns, our calculations

show this acquisition to be permanently dilutive to shareholders

show this acquisition to be permanently dilutive to shareholders

¡ 1.4 Billion new

shares issued to MER shareholders

¡ Required Pretax

Earnings of $9.7 BN to be non-dilutive to Earnings

Per Share for Bank of America stockholders

Per Share for Bank of America stockholders

¡ MER pretax

earnings at “artificial peak” in 2006 = $9.8 BN,

including $7.2 BN of non-recurring “Trading Revenues” related to

Asset Backed Securities Operations, all of which (and more) has been

subsequently written off as losses

including $7.2 BN of non-recurring “Trading Revenues” related to

Asset Backed Securities Operations, all of which (and more) has been

subsequently written off as losses

¡ MER Profits appear

highly dependent upon capital markets activity

requiring capital at risk, i.e. proprietary trading, securitizations, etc.

(volatile, low multiple stream of earnings)

requiring capital at risk, i.e. proprietary trading, securitizations, etc.

(volatile, low multiple stream of earnings)

¡ Planned $7 +

billion of cost savings often result in declining revenues

¡ Added cost of

retaining best producers

www.BACPROXYVOTE.com

10

Merrill Lynch

Acquisition#3

— True Cost of MER

Deal (our calculation):

¡ BAC Stock issued

to Merrill shareholders

$19.4 BN

¡ Merrill Preferred

Stock Assumed

$ 9.7 BN

¡ Drop in BAC Stock

($33=>$22 x 5 bn shrs)

$55 BN

÷ (1 day after

announcement of deal)

¡ Cost of Retention

Bonuses Paid to MER Brokers

$ 3.7 BN

¡ Cost of New Gov’t

TARP Money (new pfd stock @ 8%)

$20 BN

¡ After tax cost of

MER 4th Qtr Asset Write

Downs / Loss

$15.5 BN

¡ Disputed Merrill

Bonuses - Thain / Cuomo

$ 3.6 BN

¡ Purchase of Gov’t

Asset Protection (TARP)

$4 BN

¡ TARP insured

future MER Losses (75% x deductible)

$15 BN

÷ Total Cost

$146 BN

¡ True Cost per MER

share $104 /

share

— Drop in BAC Market

Capitalization Since Deal

$145 BN

www.BACPROXYVOTE.com

11

Credit Risk

Assumed Through Acquisitions

— Countrywide

Acquisition

— Merrill Lynch

Acquisition

www.BACPROXYVOTE.com

Countrywide -

Credit Risk Assumed

— Acquired Unknown

Credit Risks to Balance Sheet

¡ Pay Option Arm

Loans (negative amortization)

$26.4 BN

¡ Sub Prime

Loans

$2.4 BN

¡ Home Equity +

2nd Lien Loans

$33.4 BN

¡ Level 3 Derivative

Assets Acquired - Excluding

Mortgage Servicing

Rights

$15 BN

¡ Total of $77.2 BN

in assets listed above EXCEED 1.6x Tangible

Book Value ($46.6BN at 6/30/08) before acquisition

Book Value ($46.6BN at 6/30/08) before acquisition

— Worsening Credit

Trends at Acquisition Date

¡ Charge offs rose

by over 700% for six months ended 6/30/08 as

compared to prior year

compared to prior year

¡ $750 MM Additional

Charges in Q4 2008 for asset quality

deterioration (after purchase accounting adjustments)

deterioration (after purchase accounting adjustments)

www.BACPROXYVOTE.com

Merrill Lynch

Credit Risk Assumed

— (dollars in

BN)

— Transitory

Leveraged Lending

$5.65

— Commercial Real

Estate

$9.7

— First Republic -

Real Estate

$3.1

— Unhedged Super

Senior ABS CDO

$0.8

— Hedged Super

Senior ABS CDO

$1.0

— CDS with Monoline

Guarantors On US & non

US ABS CDO’s

$9.2

— Investment

Portfolio

$10.4

¡ Sum of Credit Risk

Assumed

$39.9

¡ Equal to 85% of

tangible capital at 9/30/08

Source:

BAC investor presentations

www.BACPROXYVOTE.com

Concealed

Information on Merrill Lynch Losses #1

— WSJ reports on

Merrill losses in 2/5/09 article:

¡ In

Merrill Deal, U.S. Played Hardball, By Dan

Fitzpatrick

¡ http://online.wsj.com/article/SB123379687205650255.html

— Financial Times

reports that Bank of America

involved in determining Merrill Q4 Losses

involved in determining Merrill Q4 Losses

¡ Bank

of America directly linked to Merrill's final

writedown, By Greg Farrell in New York, Published: March 20 2009

writedown, By Greg Farrell in New York, Published: March 20 2009

¡ http://www.ft.com/cms/s/0/ca0e8f8c-14ee-11de-8cd1-0000779fd2ac.html

www.BACPROXYVOTE.com

15

Concealed

Information on Merrill Lynch Losses #2

— Failure to

Disclose Material Information to Shareholders

¡ October &

November 2008 were two of the worst months in fixed income

and credit market history

and credit market history

¡ On November 12,

Henry Paulson announces TARP will not buy assets, asset

prices go into freefall

prices go into freefall

¡ Losses in Merrill

portfolio would have been evident well before December

5th, 2008 shareholder vote to approve merger

5th, 2008 shareholder vote to approve merger

¡ Wall Street

Journal article dated 2/5/09 details timing of losses in Merrill

Portfolio (see article)

Portfolio (see article)

¡ Bank of America

had a full team of accountants at Merrill’s offices reviewing

the portfolio marks daily starting in September

the portfolio marks daily starting in September

¡ Ken Lewis claims

losses not evident until Dec. 15th. Credit

and fixed income

markets improved during December

markets improved during December

¡ BAC & Board do

not disclose losses until 1/16/09. 47% of

shares trade in the

period 12/15/08 to 1/16/09. Creates significant legal exposure to BAC.

period 12/15/08 to 1/16/09. Creates significant legal exposure to BAC.

www.BACPROXYVOTE.com

16

Securities Law

Questions

— Failure to Amend

Proxy Statement prior to 12/5 vote

— Use of TARP Funds

to Complete Acquisition is a

material change in transaction terms. Should have

been resubmitted to shareholders for approval

material change in transaction terms. Should have

been resubmitted to shareholders for approval

— 47% of shares

trade during period between 12/17 and

1/16/09 without disclosure of Merrill losses and

accepting more TARP funds

1/16/09 without disclosure of Merrill losses and

accepting more TARP funds

www.BACPROXYVOTE.com

17

Securities Law

Questions

Failure to Disclose Material Information

Failure to Disclose Material Information

— Finger Interests

has alleged in a class action lawsuit

that certain officers and directors failed to disclose

material information to shareholders.

that certain officers and directors failed to disclose

material information to shareholders.

¡ Management and the

board of directors withheld material

information that would have affected stockholders’ decisions

to buy, hold or sell their shares of Bank of America common

stock.

information that would have affected stockholders’ decisions

to buy, hold or sell their shares of Bank of America common

stock.

¡ Management and the

board of directors filed an inaccurate

proxy statement dated October 31, 2008, and failed, either by

omission or affirmative act, to amend the proxy statement to

reflect material changes in the financial condition of Merrill

Lynch.

proxy statement dated October 31, 2008, and failed, either by

omission or affirmative act, to amend the proxy statement to

reflect material changes in the financial condition of Merrill

Lynch.

¡ A copy of the

lawsuit is under the “Our Lawsuit” tab.

www.BACPROXYVOTE.com

Securities Law

Questions #2

Failure to Disclose Material Information

Failure to Disclose Material Information

— We have been

advised by counsel that such omissions by certain

officers and directors may be a violation of the disclosure

requirements under section 14 (a) of the Exchange Act and SEC rule

14(a)-9(a).

officers and directors may be a violation of the disclosure

requirements under section 14 (a) of the Exchange Act and SEC rule

14(a)-9(a).

— We believe the

decision by the board to not amend the merger proxy

statement dated October 31, 2008 was also a failure of board to fulfill

its fiduciary duty to protect the interests of shareholders.

statement dated October 31, 2008 was also a failure of board to fulfill

its fiduciary duty to protect the interests of shareholders.

— We further believe

this failure by the board is generally reflective of

the board’s willingness to acquiesce to management’s wishes with

respect to acquisitions and other matters of great significance to the

interests of shareholders.

the board’s willingness to acquiesce to management’s wishes with

respect to acquisitions and other matters of great significance to the

interests of shareholders.

— As such, we urge

shareholders to vote for change.

www.BACPROXYVOTE.com

Our

Goals

— Change in

Governance

¡ Vote “Against”

election of Three Directors (Item 1)

÷ Ken Lewis -

Current Chairman / CEO, architect of Countrywide

and Merrill Deals

and Merrill Deals

÷ Temple Sloan -

Lead Director

÷ Jackie Ward -

Chair, Asset Quality Committee

¡ Separate Chairman

and CEO - New Chairman/Lead Director

willing to Protect Shareholders and Challenge Management (item 8)

willing to Protect Shareholders and Challenge Management (item 8)

¡ Tie Compensation

to Long Term Share Performance (Items

3,5,11)

— Change

Culture

¡ Greater Focus on

Building Shareholder Value

¡ Greater Focus on

Risk - Reward Analysis in use of Capital

¡ Promote Greater

Transparency and Disclosure

www.BACPROXYVOTE.com

20

Actions to

Date

— Legal

Action

¡ Filed Class Action

Lawsuit regarding Securities Law issues

¡ Initial Contacts

with Regulatory Agencies

— Launched Campaign

to Communicate with

Shareholders

Shareholders

¡ Web site - www.bacProxyVote.com

¡ Exempt

Solicitation Filing with Securities Exchange Commission

÷ http://idea.sec.gov/Archives/edgar/data/70858/000095013409005879/d66927px14a6g.htm

¡ Public Relations

Firm

¡ Initial Contact

with Regulatory Bodies

¡ Targeting Proxy

Voting Services

¡ Communications

with Significant Shareholders

www.BACPROXYVOTE.com

21

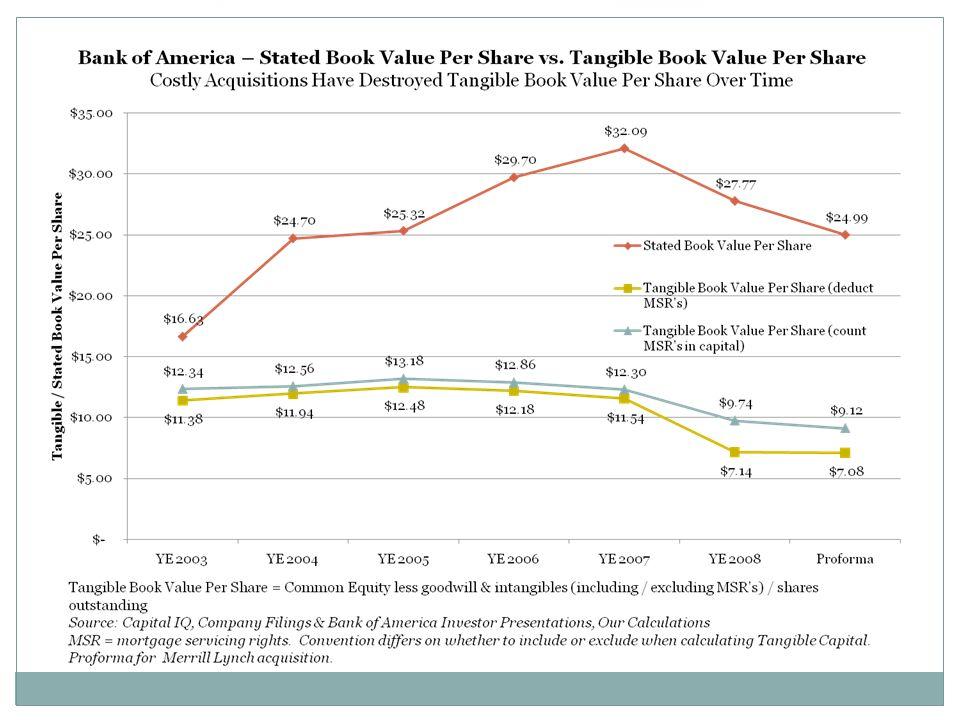

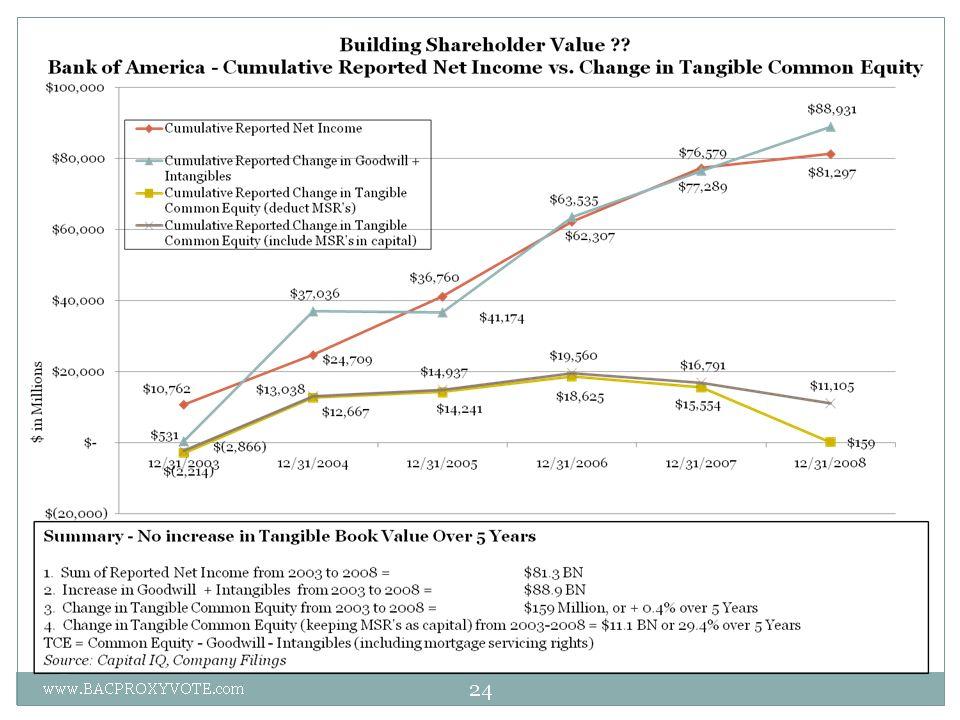

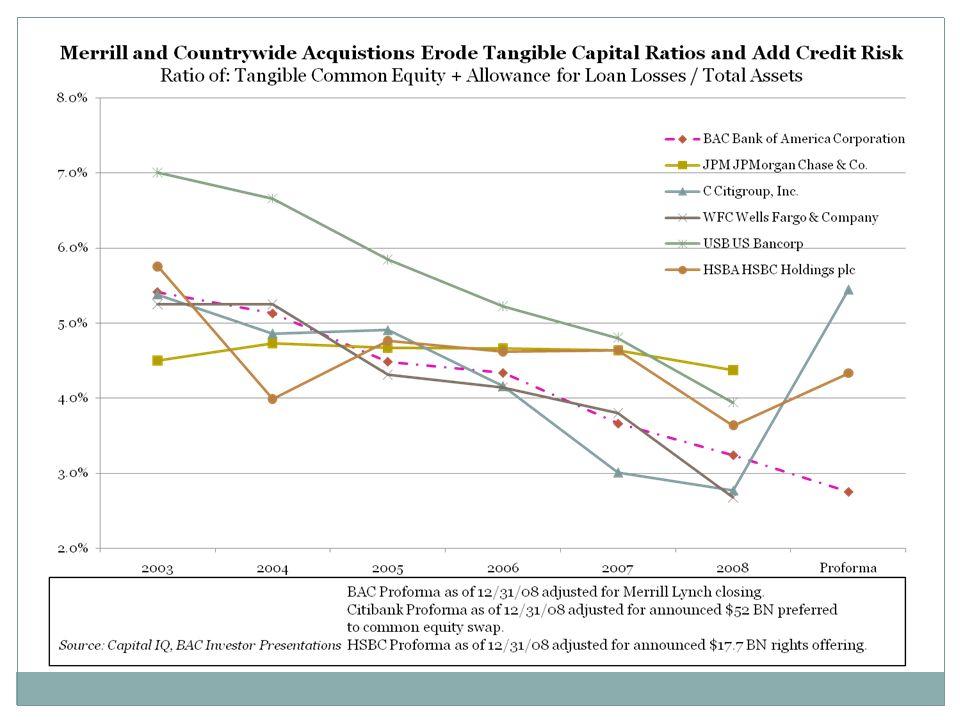

Appendix -

Graphs

Permanent

Destruction of Shareholder

Value

Value

÷ Graph of Tangible

Book Value Per Share

÷ Graph Reported Net

Income vs Change in Goodwill

vs Change in Tangible Common Equity

vs Change in Tangible Common Equity

÷ Graph Ratio of

Tangible Common Equity +

Allowance for Loan Loss / Total Assets

Allowance for Loan Loss / Total Assets

www.BACPROXYVOTE.com

22

www.BACPROXYVOTE.com

23

www.BACPROXYVOTE.com

25