|

|

FINGER

INTERESTS, LTD.

|

520 POST

OAK BLVD.; SUITE 750, HOUSTON, TX, 77027

Tele:

713-621-7525 Fax: 713-621-7552

Email:

fingerint@aol.com

|

|

FINGER

INTERESTS, LTD.

|

|

Vote AGAINST re-election

of

|

Kenneth D. Lewis -

Chairman and CEO

|

|

Vote AGAINST re-election

of

|

O. Temple Sloan, Jr. –

Lead director, Chair Compensation Committee, Chair Executive Committee,

Corporate Governance Committee

Member

|

|

Vote AGAINST re-election

of

|

Jackie M. Ward – Chair

Asset Quality Committee

|

|

/s/

Jerry E. Finger

|

/s/

Jonathon S. Finger

|

|

|

Jerry

E. Finger

|

Jonathan

S. Finger

|

|

1)

|

Management and Board Pursued

Risky and Overpriced Acquisitions – Management and the Board are

focused on size, footprint and market share, regardless of the impact on

shareholder value. They have pursued acquisitions that are

overpriced and assumed credit and other risks that are not consistent with

maintaining and building shareholder

value.

|

|

a)

|

Merrill

Lynch Offer price per share = 60% premium to prior closing share price in

unstable and declining stock markets, in the face

of:

|

|

|

i)

|

Pending

failure of Lehman; (ii) Frozen Credit Markets; (iii) Funding Uncertainty

for Broker Dealer Firms

|

|

2)

|

Management

and the Board Assumed Massive Credit Risk Through

Acquisitions

|

|

a)

|

Countrywide

Risk - Acquired $26.4 BN pay option ARMs, $2.4 BN Sub Prime Loans, $33.4

BN Home Equity / 2nd

lien loans, $15 BN level 3 assets for a total of $77.2BN or 1.6x tangible

common equity at 6/30/08. The worsening of credit trends at

acquisition date, plus huge litigation risk of 5 lawsuits filed by state

attorneys general regarding CFC lending

practices.

|

|

b)

|

Merrill

Lynch – Acquired $39.9BN of risk assets, including Leveraged Loans,

commercial real estate, CDO’s, Credit default swaps with monocline

exposure and other investments totaling 85% of tangible common equity at

9/30/08.

|

|

3)

|

Management

and the Board Failed to Disclose Information to Shareholders Regarding

Losses at Merrill Lynch, resulting in Possible Securities Law

Violations

|

|

a)

|

Despite

having knowledge of $13.3BN of losses at Merrill by end of November,

management and board elected not to inform shareholders of losses before

shareholder vote on December 5th. See

WSJ article 2/5/09.

|

|

b)

|

BAC’s

chief accounting officer, Neil Cotty was directly involved in Merrill’s Q4

2008 write-downs, and had full access to Merrill’s financial information

and books. BAC disclosed nothing regarding Merrill loses until

1/16/09. See Financial Times article,

3/20/09.

|

|

c)

|

Failed

to amend proxy statement prior to shareholder vote. Failed to

disclose to shareholders the additional TARP funds requested from

government on December 15th to facilitate acquisition of

Merrill. This was a material change in deal terms that was not

disclosed to shareholders.

|

|

d)

|

47%

of weighted average shares trade from 12/15/08 to 1/16/09 when TARP and

Merrill losses are disclosed, creating potential liability for

directors.

|

|

4)

|

Management

and Board had Prior Knowledge of Merrill bonus payments through merger

agreement side letter, credibility

weakened

|

|

a)

|

Ken

Lewis and the board initially disavowed any knowledge of size and timing

of Merrill bonuses. Irrespective of the merit of awarding such

bonuses, testimony in NY AG Cuomo’s investigation casts serious doubt

regarding management’s account of events. Management integrity

is a key factor to maintain the confidence of investors and securities

analysts.

|

|

5)

|

Management

and Board have Caused Permanent Destruction of Shareholder

Value

|

|

a)

|

The

Merrill Lynch transaction, even prior to the disclosure of 4th

quarter losses, was, by our calculation, dilutive from an earnings per

share basis as a result of the 1.4bn BAC shares issued to acquire Merrill

Lynch. Based on the number of shares issued, Merrill would need

to earn $9.7BN pretax to not be dilutive to E.P.S. In 2006,

Merrill earned $9.8BN pretax, including $7.2 BN in trading revenues, all

of which has subsequently been charged-off as

losses.

|

|

b)

|

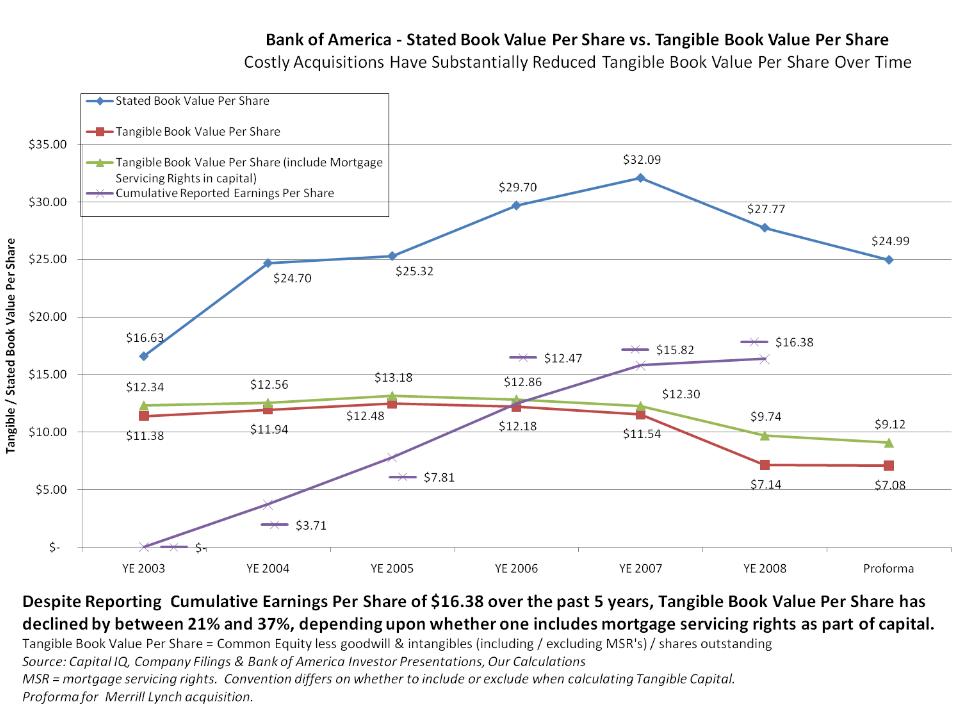

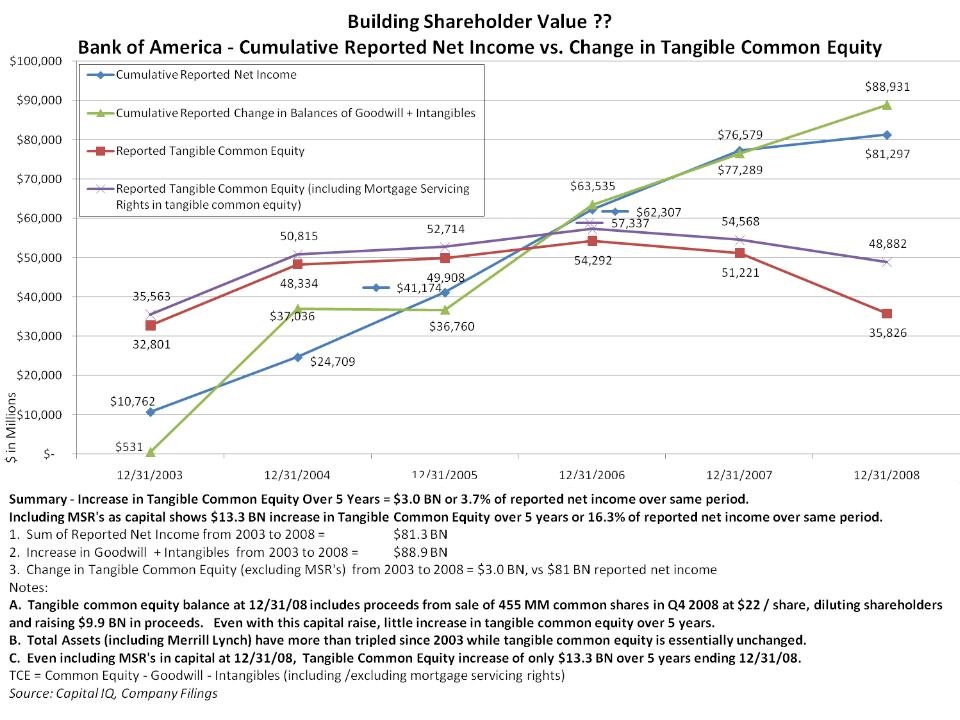

Tangible

Book Value per share has fallen as a result of goodwill created by

overpriced acquisitions and poor capital management. Tangible

Book Value, excluding mortgage servicing rights fell from $11.38 per share

at 12/31/03 to $7.08 per share at 12/31/08, pro forma for the acquisition

of Merrill.

|