Capped Return Notes

Linked to MSCI EAFE Index® due August 27, 2009

The Index

All

disclosure contained in this term sheet regarding the MSCI Indices including,

without limitation, their make-up, method of calculation and changes in

components, is derived from the MSCI Global Investable Market Indices Methodology

Book published by MSCI, Inc. (“MSCI”, the successor to Morgan Stanley Capital

International, Inc.) in June 2008 and other publicly available information.

This information reflects the policies of MSCI, as stated in this publicly

available information, and is subject to change by MSCI at its discretion. MSCI

has no obligation to continue to publish, and may discontinue publication of,

the MSCI Indices. ML&Co. and MLPF&S have not independently verified and

make no representation as to the accuracy or completeness of such information.

None of ML&Co., the calculation agent and MLPF&S accepts any

responsibility for the calculation, maintenance or publication of the MSCI

Indices or any successor indices.

General – MSCI Indices

The MSCI

Indices were founded in 1969 by Capital International S.A. as the first

international performance benchmarks constructed to facilitate accurate

comparison of world markets. Morgan Stanley acquired the rights to the indices

and data from Capital International in 1986. In November 1998, Morgan Stanley

transferred all rights to the MSCI indices to Morgan Stanley Capital

International Inc., which was later succeeded by MSCI. The MSCI Indices have

covered the world’s developed markets since 1969 and, in 1988, MSCI commenced

coverage of the emerging markets. MSCI applies the same criteria and

calculation methodology across all markets for all equity indices, developed

and emerging.

In March

2006, MSCI announced enhancements to the methodology of its Global Investable

Market Indices methodology, by moving from a sampled multi-cap approach to an

approach targeting exhaustive coverage with non-overlapping size and style

segments. The MSCI Standard and MSCI Small Cap Indices, along with the other

MSCI equity indices based on them, transitioned to the Global Investable Market

Indices methodology described below. The indices transitioned in two phases.

The first phase was completed on November 30, 2007 and the second was completed

on May 30, 2008. The transition was synchronized for all market and composite

indices with the exception of the MSCI Euro and Pan-Euro Indices, which

transitioned in one phase as of the close of November 30, 2007.

The MSCI

Standard Indices are now composed of the MSCI Large Cap and Mid Cap Indices.

The previous MSCI Small Cap Index transitioned to the MSCI Small Cap Index

resulting from the Global Investable Market Indices methodology, and contains

no overlap with constituents of the transitioned MSCI Standard Indices. In

addition, under the MSCI Global Investable Market Indices methodology, there

are new Small Cap Indices covering Emerging Markets countries. There are also

new MSCI Value and Growth Indices constructed from the Small Cap Index Series

for both Emerging and Developed Markets. Together, the relevant MSCI Large Cap,

Mid Cap and Small Cap Indices now make up the MSCI Investable Market Index for

each country, composite, sector, and style index that MSCI offers.

Constructing the MSCI

Global Investable Market Indices

MSCI

undertakes an index construction process, which involves: (i) defining the

Equity Universe; (ii) determining the Market Investable Equity Universe for

each market; (iii) determining market capitalization size segments for each

market; (iv) applying Index Continuity Rules for the Standard Index; (v)

creating style segments within each size segment within each market; and (vi)

classifying securities under the Global Industry Classification Standard (the

“GICS®”).

Defining the Equity Universe

(i)

Identifying Eligible Equity Securities: The Equity Universe initially looks at

securities listed in any of the countries in the MSCI Global Index Series,

which will be classified as either Developed Markets (DM) or Emerging Markets

(EM). All listed equity securities, or listed securities that exhibit

characteristics of equity securities, except mutual funds, ETFs, equity

derivatives, limited partnerships, and most investment trusts are eligible for

inclusion in the Equity Universe. Real Estate Investment Trusts (REITs) in some

countries and certain income trusts in Canada are also eligible for inclusion.

(ii)

Country Classification of Eligible Securities: Each company and its securities

(i.e., share classes) is classified in one and only one country, which allows

for a distinctive sorting of each company by its respective country.

Determining the Market Investable Equity

Universes

A Market

Investable Equity Universe for a market is derived by applying investability

screens to individual companies and securities in the Equity Universe that are

classified in that market. A market is equivalent to a single country, except

in DM Europe, where all DM countries in Europe are aggregated into a single

market for index construction purposes. Subsequently, individual DM Europe country

indices within the MSCI Europe Index are derived from the constituents of the

MSCI Europe Index under the Global Investable Market Indices methodology.

The

investability screens used to determine the Investable Equity Universe in each

market are as follows:

(i) Equity Universe Minimum Size Requirement:

This investability screen is applied at the company level. In order to be

included in a Market Investable Equity Universe, a company must have the

required minimum full market capitalization.

(ii) Equity Universe Minimum Float-Adjusted Market

Capitalization Requirement: This investability screen is applied at

the individual security level. To be eligible for inclusion in a Market

Investable Equity Universe, a security must have a free float-adjusted market

capitalization equal to or higher than 50% of the Equity Universe Minimum Size

Requirement.

(iii) DM and EM Minimum Liquidity Requirement:

This investability screen is applied at the individual security level. To be

eligible for inclusion in a Market Investable Equity Universe, a security must

have adequate liquidity. The Annualized Traded Value Ratio (ATVR), a measure

which offers the advantage of screening out extreme daily trading volumes and

taking into account the free float-adjusted market capitalization size of

securities, is used to measure liquidity. In the calculation of the ATVR, the

trading volumes in depository receipts associated with that security, such as

ADRs or GDRs, are also considered. A minimum liquidity level of 20% ATVR is

required for inclusion of a security in a Market Investable Equity Universe of

a Developed Market and a minimum liquidity level of 15% ATVR is required for

inclusion of a security in a Market Investable Equity Universe of an Emerging

Market.

(iv) Global Minimum Foreign Inclusion Factor Requirement:

This investability screen is applied at the individual security level. To be

eligible for inclusion in a Market Investable Equity Universe, a security’s

Foreign Inclusion Factor (FIF) must reach a certain threshold. The FIF of a

security is defined as the proportion of shares outstanding that is available

for purchase in the public equity markets by international investors. This

proportion accounts for the available free float of and/or the foreign

ownership limits applicable to a specific security (or company). In general, a

security must have an FIF equal to or larger than 0.15 to be eligible for

inclusion in a Market Investable Equity Universe.

TS-6

Capped Return Notes

Linked to MSCI EAFE Index® due August 27, 2009

(v) Minimum Length of Trading Requirement: This

investability screen is applied at the individual security level. For an IPO to

be eligible for inclusion in a Market Investable Equity Universe, the new issue

must have started trading at least four months before the implementation of the

initial construction of the index or at least three months before the

implementation of a Semi-Annual Index Review. This requirement is applicable to

small new issues in all markets. Large IPOs are not subject to the Minimum

Length of Trading Requirement and may be included in a Market Investable Equity

Universe and the Standard Index outside of a Quarterly or Semi-Annual Index

Review.

Defining Market Capitalization Size

Segments for Each

Market

Once a

Market Investable Equity Universe is defined, it is segmented into the

following size-based indices:

|

|

|

|

|

|

•

|

Investable Market Index (Large +

Mid + Small)

|

|

|

•

|

Standard Index (Large + Mid)

|

|

|

•

|

Large Cap Index

|

|

|

•

|

Mid Cap Index

|

|

|

•

|

Small Cap Index

|

Creating

the Size Segment Indices in each market involves the following steps: (i)

defining the Market Coverage Target Range for each size segment; (ii)

determining the Global Minimum Size Range for each size segment; (iii)

determining the Associated Market Size-Segment Cutoffs and Segment Number of

Companies; (iv) assigning companies to the size segments and (v) applying final

size-segment investability requirements.

Applying Index Continuity Rules for the

Standard

Indices

In order to

achieve index continuity, as well as provide some basic level of

diversification within a market index, notwithstanding the effect of other

index construction rules contained herein, a minimum number of five

constituents will be maintained for a DM Standard Index and a minimum number of

three constituents will be maintained for an EM Standard Index.

Creating Style Indices within Each Size

Segment

All

securities in the investable equity universe are classified into Value or

Growth segments using the MSCI Global Value and Growth methodology, which uses

multiple factors to identify value and growth characteristics. The value

investment style characteristics use the following three variables for index

construction: book value to price ratio, 12-month forward earnings to price

ratio, and dividend yield. The growth investment style characteristics use the

following five variables for index construction: long-term forward earnings per

share (“EPS”) growth rate, short-term EPS growth rate, current internal growth

rate, long-term historical EPS growth trend and long-term historical sales per

share growth trend.

Classifying Securities under the Global

Industry

Classification Standard

All

securities in the Global Investable Equity Universe are assigned to the

industry that best describes their business activities. To this end, MSCI has

designed, in conjunction with Standard & Poor’s, the Global Industry

Classification Standard (GICS). Under the GICS, each company is assigned

uniquely to one sub-industry according to its principal business activity.

Therefore, a company can only belong to one industry grouping at each of the

four levels of the GICS.

Maintaining the MSCI Global

Investable Market Indices

The MSCI

Global Investable Market Indices are maintained with the objective of

reflecting the evolution of the underlying equity markets and segments on a

timely basis, while seeking to achieve index continuity, continuous

investability of constituents and replicability of the indices, and index

stability and low index turnover.

In

particular, index maintenance involves:

(i)

Semi-Annual Index Reviews (SAIRs) in May and November of the Size Segment and

Global Value and Growth Indices which include:

|

|

|

|

|

|

•

|

Updating the indices on the basis

of a fully refreshed Equity Universe.

|

|

|

•

|

Taking buffer rules into

consideration for migration of securities across size and style segments.

|

|

|

•

|

Updating Foreign Inclusion

Factors (FIFs) and Number of Shares (NOS).

|

(ii)

Quarterly Index Reviews (QIRs) in February and August of the Size Segment

Indices aimed at:

|

|

|

|

|

|

•

|

Including significant new

eligible securities (such as IPOs which were not eligible for earlier

inclusion) in the index.

|

|

|

•

|

Allowing for significant moves of

companies within the Size Segment Indices, using wider buffers than in the

SAIR.

|

|

|

•

|

Reflecting the impact of

significant market events on FIFs and updating NOS.

|

(iii)

Ongoing event-related changes are generally implemented in the indices as they

occur. Significantly large IPOs are included in the indices after the close of

the company’s tenth day of trading.

TS-7

Capped Return Notes

Linked to MSCI EAFE Index® due August 27, 2009

The MSCI EAFE Index

The Index

is a free float-adjusted market capitalization index that is designed to

measure the equity market performance of developed markets, excluding the

United States and Canada. As of the Pricing Date, the Index consisted of the

following 21 developed market country indices: Australia, Austria, Belgium,

Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Italy, Japan,

the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden,

Switzerland, and the United Kingdom. As of the Pricing Date, the five largest

country weights were: Japan (21.48%), the United Kingdom (21.31%), France

(10.73%), Germany (9.18%) and Switzerland (7.05%) and the five largest sector

weights were: Financials (25.64%), Industrials (12.17%), Materials (11.79%),

Consumer Discretionary (9.99%) and Energy (8.78%).

The Index

is published by MSCI and is intended to measure the performance of certain

developed equity markets. The Index is a free float-adjusted market

capitalization index with a base date of December 31, 1969 and an initial value

of 100. The Index is calculated daily in U.S. dollars and published in real

time every 60 seconds during market trading hours. The Index is published by

Bloomberg under the index symbol “MXEA”.

The Index

is part of the MSCI Equity Indices series. For more detail on how the MSCI

Equity Indices are calculated and how the securities comprising such indices

are selected, please see the section entitled “The MSCI Indices” in the index

supplement I-1.

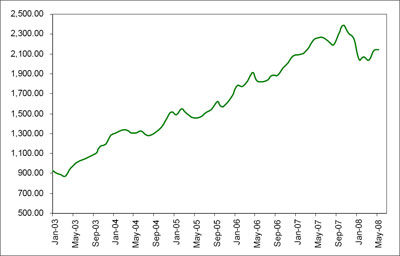

The following graph sets forth the historical

performance of the Index in the period from January 2003 through May 2008. This

historical data on the Index is not necessarily indicative of the future

performance of the Index or what the value of the Notes may be. Any historical

upward or downward trend in the level of the Index during any period set forth

below is not an indication that the Index is more or less likely to increase or

decrease at any time over the term of the Notes. On the Pricing Date, the

closing level of the Index was 1,991.94.

|

|

|

The information on the MSCI EAFE Index provided in this document should

be read together with the discussion under the heading “The MSCI Indices”

beginning on page IS-40 of the index supplement I-1.

|

TS-8

Capped Return Notes

Linked to MSCI EAFE Index® due August 27, 2009

Certain

U.S. Federal Income Taxation Considerations

Set forth

below is a summary of certain U.S. federal income tax considerations relating

to an investment in the Notes. The following summary is not complete and is

qualified in its entirety by the discussions under the sections entitled

“United States Federal Income Taxation” in the accompanying product supplement

CRN-1 and MTN prospectus supplement, which you should carefully review prior to

investing in the Notes.

General. There are no statutory provisions, regulations,

published rulings or judicial decisions addressing or involving the

characterization and treatment, for United States federal income tax purposes,

of the Notes or securities with terms substantially the same as the Notes.

Accordingly, the proper United States federal income tax characterization and

treatment of the Notes is uncertain. Pursuant to the terms of the Notes,

ML&Co. and every holder of a Note agree (in the absence of an

administrative determination, judicial ruling or other authoritative guidance

to the contrary) to characterize and treat a Note for all tax purposes as a

pre-paid cash-settled forward contract linked to the level of the Index. Due to

the absence of authorities that directly address instruments that are similar

to the Notes, significant aspects of the United States federal income tax

consequences of an investment in the Notes are not certain, and no assurance

can be given that the Internal Revenue Service (the “IRS”) or the courts will

agree with the characterization and tax treatment described above. Accordingly,

prospective purchasers are urged to consult their own tax advisors regarding the

United States federal income tax consequences of an investment in the Notes

(including alternative characterizations and tax treatments of the Notes) and

with respect to any tax consequences arising under the laws of any state, local

or foreign taxing jurisdiction.

Payment on the Maturity Date. Assuming that the Notes are

properly characterized and treated as pre-paid cash-settled forward contracts

linked to the level of the Index, upon the receipt of cash on the maturity date

of the Notes, a U.S. Holder (as defined in the accompanying product supplement

CRN-1) will recognize gain or loss. The amount of such gain or loss will be the

extent to which the amount of the cash received differs from the U.S. Holder’s

tax basis in the Note. A U.S. Holder’s tax basis in a Note generally will equal

the amount paid by the U.S. Holder to purchase the Note. It is uncertain

whether any such gain or loss would be treated as ordinary income or loss or

capital gain or loss. Absent a future clarification in current law (by an

administrative determination, judicial ruling or otherwise), where required,

ML&Co. intends to report any such gain or loss to the IRS in a manner

consistent with the treatment of such gain or loss as capital gain or loss. If

such gain or loss is treated as capital gain or loss, then any such gain or

loss will be long-term capital gain or loss if the U.S. Holder has held the

Note for more than one year as of the maturity date.

Sale or Exchange of the Notes. Assuming that the Notes

are properly characterized and treated as pre-paid cash-settled forward

contracts linked to the level of the Index, upon a sale or exchange of a Note

prior to the maturity date of the Notes, a U.S. Holder will generally recognize

capital gain or loss in an amount equal to the difference between the amount

realized on such sale or exchange and such U.S. Holder’s tax basis in the Note

so sold or exchanged. Any such capital gain or loss will be long-term capital

gain or loss if the U.S. Holder has held the Note for more than one year as of

the date of such sale or exchange.

Possible Future Tax Law Changes. On December 7, 2007, the

IRS released a notice that could possibly affect the taxation of holders of the

Notes. According to the notice, the IRS and the U.S. Department of the Treasury

(the “Treasury Department”) are actively considering, among other things,

whether the holder of an instrument having terms similar to the Notes should be

required to accrue either ordinary income or capital gain on a current basis,

and they are seeking comments on the subject. It is not possible to determine

what guidance they will ultimately issue, if any. It is possible, however, that

under such guidance, holders of instruments having terms similar to the Notes

will ultimately be required to accrue income currently and this could be

applied on a retroactive basis. The IRS and the Treasury Department are also

considering other relevant issues, including whether additional gain or loss

from such instruments should be treated as ordinary or capital, whether foreign

holders of such instruments should be subject to withholding tax on any deemed

income accruals, whether the tax treatment of such instruments should vary

depending upon whether or not such instruments are traded on a securities

exchange, whether such instruments should be treated as indebtedness, whether

the tax treatment of such instruments should vary depending upon the nature of

the underlying asset, and whether the special “constructive ownership rules”

contained in Section 1260 of the Internal Revenue Code of 1986, as amended

might be applied to such instruments. Holders are urged to consult their tax

advisors concerning the significance, and the potential impact, if any, of the

above considerations to their investment in the Notes. ML&Co. intends to

continue to treat the Notes for U.S. federal income tax purposes in accordance

with the treatment described herein unless and until such time as the Treasury

Department and IRS determine that some other treatment is more appropriate.

Prospective purchasers of the Notes should consult their own tax advisors

concerning the tax consequences, in light of their particular circumstances,

under the laws of the United States and any other taxing jurisdiction, of the

purchase, ownership and disposition of the Notes. See the discussion under the

section entitled “United States Federal Income Taxation” in the accompanying

product supplement CRN-1.

TS-9

Capped Return Notes

Linked to MSCI EAFE Index® due August 27, 2009

Experts

The

consolidated financial statements incorporated by reference in this term sheet

from Merrill Lynch & Co., Inc.’s Annual Report on Form 10-K for the year

ended December 28, 2007 and the effectiveness of Merrill Lynch & Co., Inc.

and subsidiaries’ internal control over financial reporting have been audited

by Deloitte & Touche LLP, an independent registered public accounting firm,

as stated in their reports, incorporated herein by reference (which reports (1)

expressed an unqualified opinion on the consolidated financial statements and

included an explanatory paragraph regarding the changes in accounting methods

in 2007 relating to the adoption of Statement of Financial Accounting Standards

No. 157, “Fair Value Measurement,”

Statement of Financial Accounting Standards No. 159, “The Fair Value Option for Financial Assets and

Financial Liabilities—Including an amendment of FASB Statement No. 115,” and

FASB Interpretation No. 48, “Accounting for

Uncertainty in Income Taxes, an Interpretation of FASB Statement No. 109,”

and in 2006 for share-based payments to conform to Statement of Financial

Accounting Standards No. 123 (revised 2004), “Share-Based

Payment,” and included an explanatory paragraph relating to the

restatement discussed in Note 20 to the consolidated financial statements and

(2) expressed an unqualified opinion on the effectiveness of internal control

over financial reporting). Such consolidated financial statements have been so

incorporated in reliance upon the reports of such firm given upon their authority

as experts in accounting and auditing.

With

respect to the unaudited condensed consolidated interim financial information

as of March 28, 2008 and for the three-month periods ended March 28, 2008 and

March 30, 2007, which is incorporated herein by reference, Deloitte &

Touche LLP, an independent registered public accounting firm, have applied

limited procedures in accordance with the standards of the Public Company

Accounting Oversight Board (United States) for a review of such information. However,

as stated in their report included in Merrill Lynch & Co., Inc.’s Quarterly

Report on Form 10-Q for the quarter ended March 28, 2008 and incorporated by

reference herein (which report included an explanatory paragraph relating to

the restatement discussed in Note 16 to the condensed consolidated interim

financial statements), they did not audit and they do not express an opinion on

that interim financial information. Accordingly, the degree of reliance on

their reports on such information should be restricted in light of the limited

nature of the review procedures applied. Deloitte & Touche LLP are not

subject to the liability provisions of Section 11 of the Securities Act of 1933

for their reports on the unaudited interim financial information because those

reports are not “reports” or a “part” of the Registration Statement prepared or

certified by an accountant within the meaning of Sections 7 and 11 of the Act.

TS-10

Capped Return Notes

Linked to MSCI EAFE Index® due August 27, 2009

Additional

Note Terms

You should

read this term sheet, together with the documents listed below (collectively,

the “Note Prospectus”), which together contain the terms of the Notes and

supersede all prior or contemporaneous oral statements as well as any other

written materials. You should carefully consider, among other things, the

matters set forth under “Risk Factors” in the sections indicated on the cover

of this term sheet. The Notes involve risks not associated with conventional

debt securities. We urge you to consult your investment, legal, tax, accounting

and other advisers before you invest in the Notes.

You may

access the following documents on the SEC Website at www.sec.gov

as

follows (or if such address has changed, by reviewing our filings for the

relevant date on the SEC Website):

|

|

|

|

|

|

§

|

Product supplement CRN-1 dated

June 3, 2008:

|

|

|

|

http://www.sec.gov/Archives/edgar/data/65100/000116923208002245/d74383_424b2.htm

|

|

|

|

|

|

|

§

|

Index supplement I-1 dated June

6, 2007:

|

|

|

|

http://www.sec.gov/Archives/edgar/data/65100/000119312507130785/d424b2.htm

|

|

|

|

|

|

|

§

|

MTN prospectus supplement dated

March 31, 2006:

|

|

|

|

http://www.sec.gov/Archives/edgar/data/65100/000119312506070946/d424b5.htm

|

|

|

|

|

|

|

§

|

General prospectus supplement

dated March 31, 2006:

|

|

|

|

http://www.sec.gov/Archives/edgar/data/65100/000119312506070973/d424b5.htm

|

|

|

|

|

|

|

§

|

Prospectus dated March 31, 2006:

|

|

|

|

http://www.sec.gov/Archives/edgar/data/65100/000119312506070817/ds3asr.htm

|

Our Central Index Key, or CIK, on the SEC Website is 65100. References

in this term sheet to “ML&Co.”, “we”, “us” and “our” are to Merrill Lynch

& Co., Inc., and references to “MLPF&S” are to Merrill Lynch, Pierce,

Fenner & Smith Incorporated.

ML&Co. has filed a registration statement (including a prospectus)

with the Securities and Exchange Commission (the “SEC”) for the offering to

which this term sheet relates. Before you invest, you should read the

prospectus in that registration statement, and the other documents relating to

this offering that ML&Co. has filed with the SEC for more complete

information about ML&Co. and this offering. You may get these documents

without cost by visiting EDGAR on the SEC Website at www.sec.gov.

Alternatively, ML&Co., any agent or any dealer participating in this

offering, will arrange to send you the Note Prospectus if you so request by

calling toll-free 1-866-500-5408.

Structured

Investments Classification

ML&Co.

classifies certain of its structured investments (the “Structured

Investments”), including the Notes, into four categories, each with different

investment characteristics. The description below is intended to briefly

describe the four categories of Structured Investments offered: Principal

Protection, Enhanced Income Market Participation and Enhanced Participation. A

Structured Investment may, however, combine characteristics that are relevant

to one or more of the other categories. As such, a category should not be

relied upon as a description of any particular Structured Investment.

Principal Protection: Principal Protected Structured Investments offer full

or partial principal protection at maturity, while offering market exposure and

the opportunity for a better return than may be available from comparable fixed

income securities. Principal protection may not be achieved if the investment

is sold prior to maturity.

Enhanced Income: Structured

Investments offering enhanced income may offer an enhanced income stream

through interim fixed or variable coupon payments. However, in exchange for

receiving current income, investors may forfeit upside potential on the

underlying asset. These investments generally do not include the principal

protection feature.

Market Participation: Market

Participation Structured Investments can offer investors exposure to specific

market sectors, asset classes and/or strategies that may not be readily

available through traditional investment alternatives. Returns obtained from

these investments are tied to the performance of the underlying asset. As such,

subject to certain fees, the returns will generally reflect any increases or

decreases in the value of such assets. These investments are not structured to

include the principal protection feature.

Enhanced Participation: Enhanced

Participation Structured Investments may offer investors the potential to

receive better than market returns on the performance of the underlying asset.

Some structures may offer leverage in exchange for a capped or limited upside

potential and also in exchange for downside risk. These investments are not

structured to include the principal protection feature.

The classification of

Structured Investments is meant solely for informational purposes and is not

intended to fully describe any particular Structured Investment nor guarantee

any particular performance.

TS-11