| PROSPECTUS SUPPLEMENT (To prospectus dated November 26, 2003) |

Filed Pursuant to Rule 424(b)(5) Registration No. 333-109802 |

2,000,000 Units

Merrill Lynch & Co., Inc.

Long Short NotesSM

Linked to the Long Short Index — Series III due January 30, 2006

(the “Notes”)

$10 original public offering price per Unit

| The Notes: Ÿ Senior unsecured debt securities of Merrill Lynch & Co., Inc.

Ÿ We will pay interest on the principal amount of the Notes semiannually, at the rate of 2.5% per year, beginning July 30, 2004.

Ÿ Linked to the value of the Long Short Index — Series III (the “Composite Index”) (index symbol “JKC”), which is designed to provide exposure to the performance of ten stocks and two equity sector indices, as described herein.

Ÿ The Composite Index reflects a leveraged long position equal to 150% of the Starting Value of the Composite Index (which equals 100), distributed initially on an equally weighted basis (i.e., 15% per stock) over a basket of ten stocks described below (collectively, the “Stock Basket”), and a short position equal to 50% of the Starting Value of the Composite Index, distributed initially on an equally weighted basis (i.e., 25% per index) over a basket of two sector indices listed below (together, the “Select Sector Basket”). The Composite Index does not take into account the dividends paid, if any, on any of the stocks included in either the Stock Basket or the Select Sector Basket.

Ÿ The Stock Basket is composed of the top ten dividend yielding stocks, reconstituted annually, in the Dow Jones Industrial Average. The Select Sector Basket will be composed of the Consumer Discretionary Select Sector Index and the Financial Select Sector Index.

Ÿ Increasesin the value of the Stock Basket will increase the level |

Basket will decrease the level of the Composite Index. Conversely, increases in the value of the Select Sector Basket will decrease the level of the Composite Index while decreases in the value of the Select Sector Basket will increase the level of the Composite Index.

Ÿ The Notes will not be listed on any securities exchange.

Ÿ Expected closing date: June 29, 2004.

Payment at maturity:

Ÿ The Notes do not provide for the repayment of a fixed principal amount.

Ÿ At maturity, you will receive a cash amount, in addition to accrued and unpaid interest, based upon the percentage change in the level of the Composite Index, which reflects the percentage change in the value of the long positions in the Stock Basket and the short position in the Select Sector Basket. If the level of the Composite Index declines over the term of the Notes, you will receive less, and possibly significantly less, than the original public offering price of $10 per Note.

Early redemption:

Ÿ If the closing level of the Composite Index falls below a specified level, the Notes will be redeemed prior to their stated maturity date. If redeemed, we will pay you a cash amount based on the percentage decrease in the level of the Composite Index as described in this prospectus supplement. |

Investing in the Notes involves risks that are described in the “ Risk Factors” section beginning on page S-8 of this prospectus supplement.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus supplement or the accompanying prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Unit |

Total | |||

| Public offering price (1) |

$10.00 | $20,000,000 | ||

| Underwriting fee |

$.20 | $400,000 | ||

| Proceeds, before expenses, to Merrill Lynch & Co., Inc. |

$9.80 | $19,600,000 | ||

| (1) Plus accrued interest from June 29, 2004, if settlement occurs after that date | ||||

Merrill Lynch & Co.

The date of this prospectus supplement is June 23, 2004.

“Long Short Notes” is a service mark of Merrill Lynch & Co., Inc.

Prospectus Supplement

| Page | ||

| S-3 | ||

| S-8 | ||

| S-11 | ||

| S-17 | ||

| S-24 | ||

| S-27 | ||

| S-28 | ||

| S-28 | ||

| S-30 | ||

| S-31 | ||

| S-31 | ||

| S-32 | ||

| A-1 |

Prospectus

| Page | ||

| MERRILL LYNCH & CO., INC |

2 | |

| USE OF PROCEEDS |

2 | |

| RATIO OF EARNINGS TO FIXED CHARGES AND RATIO OF EARNINGS TO COMBINED FIXED CHARGES AND PREFERRED STOCK DIVIDENDS |

3 | |

| THE SECURITIES |

3 | |

| DESCRIPTION OF DEBT SECURITIES |

4 | |

| DESCRIPTION OF DEBT WARRANTS |

13 | |

| DESCRIPTION OF CURRENCY WARRANTS |

15 | |

| DESCRIPTION OF INDEX WARRANTS |

16 | |

| DESCRIPTION OF PREFERRED STOCK |

22 | |

| DESCRIPTION OF DEPOSITARY SHARES |

27 | |

| DESCRIPTION OF PREFERRED STOCK WARRANTS |

31 | |

| DESCRIPTION OF COMMON STOCK |

33 | |

| DESCRIPTION OF COMMON STOCK WARRANTS |

36 | |

| PLAN OF DISTRIBUTION |

39 | |

| WHERE YOU CAN FIND MORE INFORMATION |

39 | |

| INCORPORATION OF INFORMATION WE FILE WITH THE SEC |

40 | |

| EXPERTS |

41 |

S-2

This summary includes questions and answers that highlight selected information from this prospectus supplement and the accompanying prospectus to help you understand the Long Short NotesSM Linked to the Long Short Index—Series III due January 30, 2006 (the “Notes”). You should carefully read this prospectus supplement and the accompanying prospectus to fully understand the terms of the Notes, the Long Short Index—Series III (the “Composite Index”) and the tax and other considerations that are important to you in making a decision about whether to invest in the Notes. You should carefully review the “Risk Factors” section, which highlights certain risks associated with an investment in the Notes, to determine whether an investment in the Notes is appropriate for you.

References in this prospectus supplement to “ML&Co.”, “we”, “us” and “our” are to Merrill Lynch & Co., Inc., and references to “MLPF&S” are to Merrill Lynch, Pierce, Fenner & Smith Incorporated.

What are the Notes?

The Notes will be a series of senior debt securities issued by ML&Co. and will not be secured by collateral. The Notes will rank equally with all of our other unsecured and unsubordinated debt. Unless redeemed prior to the stated maturity date under the circumstances described herein, the Notes will mature on January 30, 2006. The Notes will be linked to the change in the level of the Composite Index.

Are there any risks associated with my investment?

Yes, an investment in the Notes is subject to risks. Please refer to the section entitled “Risk Factors” in this prospectus supplement.

When will I receive interest?

Interest on the Notes will accrue at a rate of 2.5% per year on the $10 principal amount of each Unit from and including June 29, 2004 to but excluding the maturity date or redemption date. You will receive semiannual interest payments on January 30 and July 30 of each year, beginning July 30, 2004. If any interest payment date is not a business day, you will receive payment on the following business day.

What is the Composite Index?

The Composite Index is designed to provide exposure to the performance of ten stocks and two equity sector indices (each, an “Index Component”), as described herein. The Composite Index reflects a leveraged long position equal to 150% of the Starting Value, distributed initially on an equally weighted basis (i.e., 15% per stock) over a basket of ten stocks described below (collectively, the “Stock Basket”) and a short position equal to 50% of the Starting Value, distributed initially on an equally weighted basis (i.e., 25% per index) over a basket of two equity sector indices listed below (each, a “Select Sector Index” and together, the “Select Sector Basket”). The Composite Index does not take into account the dividends paid, if any, on any of the stocks included in either the Stock Basket or the Select Sector Basket.

The Stock Basket will be composed of the top ten dividend yielding stocks, reconstituted annually, in the Dow Jones Industrial Average. Standard & Poor’s publishes the two equity sector indices comprising the Select Sector Basket, which are the Consumer Discretionary Select Sector Index and the Financial Select Sector Index. The Index Components are described in the sections entitled “The Composite Index—Stock Basket” and “—Select Sector Basket” in this prospectus supplement.

Each Index Component has been assigned a weighting and such weighting will reflect the relative contribution that Index Component makes to the level of the Composite Index. A positive weighting indicates that the Composite Index is long a particular Index Component. A negative weighting indicates that the Composite Index is short a particular Index Component. The weightings are disclosed in the section entitled “The Composite Index” in this prospectus supplement.

The level of the Composite Index was set to 100.00 on June 23, 2004, the date the Notes were priced for initial sale to the public (the “Pricing Date”).

S-3

A fixed factor (the “Multiplier”) was determined for each Index Component on the Pricing Date. The Multipliers can be used to calculate the level of the Composite Index on any given day by summing the products of the value of each Index Component and its designated Multiplier, as described in this prospectus supplement. The Multipliers for each Index Component are listed in the section entitled “The Composite Index” in this prospectus supplement.

The Notes are debt obligations of ML&Co. and an investment in the Notes does not entitle you to any ownership interest in the stocks included in the Stock Basket and underlying each Index Component contained in the Select Sector Basket (collectively, the “Component Stocks”).

How has the Composite Index performed historically?

The Composite Index did not exist until the Pricing Date. We have, however, included a table showing hypothetical monthly historical levels of the Composite Index for each month from January 1999 to May 2004 based upon the Multipliers for each Index Component and historical values of each Index Component. In addition, we have included tables showing the historical monthly values of each of the Index Components for each month from January 1999 to May 2004. The tables for the Index Components in the Stock Basket are included in Annex A to this prospectus supplement. The tables for the Index Components in the Select Sector Basket are included in the section entitled “The Composite Index” in this prospectus supplement.

We have provided this hypothetical historical and historical information to help you evaluate the behavior of the Composite Index in various economic environments; however, this past performance is not indicative of how the Composite Index will perform in the future.

Any prospective purchaser of the Notes should undertake an independent investigation of the Index Components as in its judgment is appropriate to make an informed decision regarding an investment in the Notes. The composition of the Composite Index does not reflect any investment or sell recommendations of ML&Co. or its affiliates.

Who determines the level of the Composite Index?

The American Stock Exchange will calculate the level of the Composite Index as described in the section entitled “The Composite Index” in this prospectus supplement and disseminate the value of the composite Index under the symbol (JKC).

What form will the Notes take?

A Unit will represent a single Note with an original public offering price of $10.00 (a “Unit”). You may transfer the Notes only in whole Units. You will not have the right to receive physical certificates evidencing your ownership except under limited circumstances. Instead, we will issue the Notes in the form of a global certificate, which will be held by The Depository Trust Company, also known as DTC, or its nominee. Direct and indirect participants in DTC will record your ownership of the Notes. You should refer to the section entitled “Description of the Debt Securities—Depositary” in the accompanying prospectus.

What will I receive upon maturity of the Notes?

At maturity, you will receive a cash payment, in addition to accrued and unpaid interest, on the Notes equal to the “Redemption Amount”.

The “Redemption Amount” per Unit will equal:

| $10.00 × | ( | Ending Value |

) | |||||

| Starting Value |

The “Starting Value” equals 100.00, the value of the Composite Index as set on the Pricing Date.

For purposes of determining the Redemption Amount, the “Ending Value” means the average, arithmetic mean, of the levels of the Composite Index at the close of the market on five business days shortly before the maturity of the Notes. We may calculate the Ending Value by reference to fewer than five or even a single day’s closing value if, during the period shortly before the maturity date of the Notes, there is a disruption in the publication of one or more of the Index Components, as described herein.

For more specific information about the Redemption Amount, please see the section entitled “Description of the Notes” in this prospectus supplement.

S-4

How does the early redemption feature work?

If on any date the closing level of the Composite Index is equal to or less than 50.00, the Notes will be redeemed on the fifth Business Day following such date (the “Early Redemption Date”). If this redemption event is triggered, we will pay you on the Early Redemption Date a cash payment per Note equal to the Redemption Amount, as described above; provided, however, for purposes of calculating the Redemption Amount, the Ending Value will equal the average of the closing levels of the Composite Index on the two business days immediately succeeding the date the closing level of the Composite Index was less than or equal to 50.00.

Examples

Here are six examples of Redemption Amount calculations, assuming:

| Ÿ | The Starting Value of the Composite Index is 100.00 and the starting values of the Index Components are the closing values of each Index Component as observed on the Pricing Date and set forth in the table below. The Multipliers were determined based upon these values and used for the calculation of the hypothetical Ending Value in each example, as described in the section entitled “The Composite Index” in this prospectus supplement. |

| Ÿ | Any change in the value of the Stock Basket is attributable to an equal change in each of the ten Index Components comprising the Stock Basket. You should be aware, however, that there may be no correlation among the values of the ten Index Components comprising the Stock Basket and that an increase in any particular Index Component comprising the Stock Basket does not assure there will be an increase in any other Index Component comprising the Stock Basket, and, conversely, a decrease in any particular Index Component comprising the Stock Basket does not assure there will be a decrease in any other Index Component comprising the Stock Basket. |

| Ÿ | Any change in the value of the Select Sector Basket is attributable to an equal change in each of the two Index Components comprising the Select Sector Basket. You should be aware, however, that there may be no correlation among the values of the two Index Components comprising the Select Sector Basket and that an increase in one Index Component comprising the Select Sector Basket does not assure there will be an increase in the other Index Component comprising the Select Sector Basket, and, conversely, a decrease in one Index Component comprising the Select Sector Basket does not assure there will be a decrease in the other Index Component comprising the Select Sector Basket. |

| Ÿ | The composition and weighting of the Index Components comprising the Stock Basket remain the same over the term of the Notes. The composition and weighting of those Index Components will be reconstituted on the anniversary of the Pricing Date as described in the section entitled “The Composite Index—Stock Basket—Annual Stock Basket Portfolio Reconstitution” in this prospectus supplement. |

| Ÿ | The closing level of the Composite Index is not equal to or less than 50.00 on any date during the term of the Notes. If on any date the closing level of the Composite Index is equal to or less than 50.00, the Notes will be redeemed early as described in the section entitled “Description of the Notes—Redemption Event” in this prospectus supplement. In such an event, your investment in the Notes should be expected to result in a significant loss to you. See “Risk Factors—Your investment may result in a loss” in this prospectus supplement. |

S-5

For each of the Index Components, the following table sets forth the starting value, the Multiplier and the hypothetical closing value used to calculate the level of the Composite Index and the Redemption Amount in each of the examples below.

| Hypothetical Closing Values | ||||||||||||||||||||||

| Long | +5% | +5% | +5% | -5% | -5% | -5% | ||||||||||||||||

| Short |

+5% |

+17% |

-5% |

+5% |

-5% |

-17% | ||||||||||||||||

| Index Components |

Starting Value |

Multiplier |

Example 1 |

Example 2 |

Example 3 |

Example 4 |

Example 5 |

Example 6 | ||||||||||||||

| Altria Group, Inc. |

48.47 | 0.30946978 | 50.89 | 50.89 | 50.89 | 46.05 | 46.05 | 46.05 | ||||||||||||||

| Citigroup Inc. |

47.24 | 0.31752752 | 49.60 | 49.60 | 49.60 | 44.88 | 44.88 | 44.88 | ||||||||||||||

| E.I. du Pont de Nemours and Company |

44.40 | 0.33783784 | 46.62 | 46.62 | 46.62 | 42.18 | 42.18 | 42.18 | ||||||||||||||

| Exxon Mobil Corporation |

45.46 | 0.3299604 | 47.73 | 47.73 | 47.73 | 43.19 | 43.19 | 43.19 | ||||||||||||||

| General Electric Company |

33.42 | 0.44883303 | 35.09 | 35.09 | 35.09 | 31.75 | 31.75 | 31.75 | ||||||||||||||

| General Motors Corporation |

48.26 | 0.31081641 | 50.67 | 50.67 | 50.67 | 45.85 | 45.85 | 45.85 | ||||||||||||||

| J.P. Morgan Chase & Co. |

37.62 | 0.39872408 | 39.50 | 39.50 | 39.50 | 35.74 | 35.74 | 35.74 | ||||||||||||||

| Merck & Co., Inc. |

47.81 | 0.3137419 | 50.20 | 50.20 | 50.20 | 45.42 | 45.42 | 45.42 | ||||||||||||||

| SBC Communications Inc. |

24.25 | 0.6185567 | 25.46 | 25.46 | 25.46 | 23.04 | 23.04 | 23.04 | ||||||||||||||

| Verizon Communications Inc. |

35.45 | 0.42313117 | 37.22 | 37.22 | 37.22 | 33.68 | 33.68 | 33.68 | ||||||||||||||

| Financial Select Sector Index |

285.86 | -0.0874554 | 300.15 | 334.46 | 271.57 | 300.15 | 271.57 | 237.26 | ||||||||||||||

| Consumer Discretionary Select Sector Index |

319.42 | -0.07826686 | 335.39 | 373.72 | 303.45 | 335.39 | 303.45 | 265.12 | ||||||||||||||

| Composite Index |

100.00 | — | 105.00 | 99.00 | 110.00 | 90.00 | 95.00 | 101.00 | ||||||||||||||

| Redemption Amount |

$ | 10.50 | $ | 9.90 | $ | 11.00 | $ | 9.00 | $ | 9.50 | $ | 10.10 | ||||||||||

Example 1—At maturity, the value of the Stock Basket has increased by 5%, the value of the Select Sector Basket has increased by 5% and the level of the Composite Index is above the Starting Value:

| Redemption Amount (per Unit) |

= | $ | 10 | × | ( | 105.00 |

) | = | $ | 10.50 | ||||||||

| 100.00 |

Total payment at maturity (per Unit) = $10.50

Example 2—At maturity, the value of the Stock Basket has increased by 5%, the value of the Select Sector Basket has increased by 17% and the level of the Composite Index is below the Starting Value:

| Redemption Amount (per Unit) |

= | $ | 10 | × | ( | 99.00 |

) | = | $ | 9.90 | ||||||||

| 100.00 |

Total payment at maturity (per Unit) = $9.90

Example 3—At maturity, the value of the Stock Basket has increased by 5%, the value of the Select Sector Basket has decreased by 5% and the level of the Composite Index is above the Starting Value:

| Redemption Amount (per Unit) |

= | $ | 10 | × | ( | 110.00 |

) | = | $ | 11.00 | ||||||||

| 100.00 |

Total payment at maturity (per Unit) = $11.00

Example 4—At maturity, the value of the Stock Basket has decreased by 5%, the value of the Select Sector Basket has increased by 5% and the level of the Composite Index is below the Starting Value:

| Redemption Amount (per Unit) |

= | $ | 10 | × | ( | 90.00 |

) | = | $ | 9.00 | ||||||||

| 100.00 |

Total payment at maturity (per Unit) = $9.00

S-6

Example 5—At maturity, the value of the Stock Basket has decreased by 5%, the value of the Select Sector Basket has decreased by 5% and the level of the Composite Index is below the Starting Value:

| Redemption Amount (per Unit) |

= | $ | 10 | × | ( | 95.00 |

) | = | $ | 9.50 | ||||||||

| 100.00 |

Total payment at maturity (per Unit) = $9.50

Example 6—At maturity, the value of the Stock Basket has decreased by 5%, the value of the Select Sector Basket has decreased by 17% and the level of the Composite Index is above the Starting Value:

| Redemption Amount (per Unit) |

= | $ | 10 | × | ( | 101.00 |

) | = | $ | 10.10 | ||||||||

| 100.00 |

Total payment at maturity (per Unit) = $10.10

What about taxes?

The U.S. federal income tax consequences of an investment in the Notes are complex and uncertain. Pursuant to the terms of the Notes, ML&Co. and you agree, in the absence of an administrative or judicial ruling to the contrary, to characterize a Note for all tax purposes as an investment unit consisting of a debt instrument of ML&Co. and a forward contract to receive a payment of the Redemption Amount at maturity. Under this characterization of the Notes, for U.S. federal income tax purposes, you will generally include payments of interest on the Notes in income in accordance with your regular method of tax accounting. You should review the discussion under the section entitled “United States Federal Income Taxation” in this prospectus supplement.

Will the Notes be listed on a stock exchange?

The Notes will not be listed on any securities exchange and we do not expect a trading market for the Notes to develop, which may affect the price you receive for your Notes upon any sale prior to maturity or redemption. You should review the section entitled “Risk Factors—A trading market for the Notes is not expected to develop” in this prospectus supplement.

What is the role of MLPF&S?

Our subsidiary, MLPF&S, is the underwriter for the offering and sale of the Notes. After the initial offering, MLPF&S intends to buy and sell Notes to create a secondary market for holders of the Notes, and may stabilize or maintain the market price of the Notes during their initial distribution. However, MLPF&S will not be obligated to engage in any of these market activities or continue them once it has started.

MLPF&S, as calculation agent (the “calculation agent”), will also be our agent for purposes of calculating, among other things, the Ending Value and Redemption Amount. Under certain circumstances, these duties could result in a conflict of interest between the status of MLPF&S as our subsidiary and its responsibilities as calculation agent.

What is ML&Co.?

Merrill Lynch & Co., Inc. is a holding company with various subsidiaries and affiliated companies that provide investment, financing, insurance and related services on a global basis.

For information about ML&Co., see the section entitled “Merrill Lynch & Co., Inc.” in the accompanying prospectus. You should also read other documents we have filed with the SEC, which you can find by referring to the section entitled “Where You Can Find More Information” in this prospectus supplement.

S-7

Your investment in the Notes will involve risks. An investment in the Notes involves credit risks which are identical to those related to investments in any other debt obligations of ML&Co., and additional risks which are similar to investing in or shorting, as applicable, each Component Stock. You should carefully consider the following discussion of risks before deciding whether an investment in the Notes is suitable for you.

Your investment may result in a loss

We will not repay you a fixed amount of principal on the Notes at maturity. The payment on the Notes will depend on the change in the level of the Composite Index. Because the level of the Composite Index is subject to market fluctuations, the Redemption Amount you receive may be more or less than the original public offering price of your Notes and may be zero. If the applicable Ending Value at maturity is less than the Starting Value, then the Redemption Amount you receive will be less than the original public offering price of each Note, in which case your investment in the Notes will result in a loss, and possibly a significant loss, to you.

In addition, if on any date the closing level of the Composite Index is equal to or less than 50.00, the Notes will be redeemed early and you will receive, for each Note then owned by you, a cash amount, in addition to accrued and unpaid interest, based on the percentage decrease in the level of the Composite Index. This amount will be less than the original public offering price of the Notes and, if you purchased your Notes in the initial distribution, will result in a loss of significant part, if not all, of your initial investment in the Notes.

Your yield may be lower than the yield on other debt securities of comparable maturity

The amount we pay you at maturity or upon early redemption, in addition to the interest payments you receive, may be less than the return you could earn on other investments. Your yield may be less than the yield you would earn if you bought other senior non-callable debt securities of ML&Co. with the same stated maturity date. Your investment may not reflect the full opportunity cost to you when you take into account factors that affect the time value of money.

Your return will not reflect the return of owning the Component Stocks

The return on your Notes will not reflect the return you would realize if you actually owned the stocks represented by the long positions of the Index Components and sold short the stocks represented by the short positions of the Index Component included in the Composite Index. The long positions of the Composite Index will not reflect dividends paid on those stocks because the level of the Composite Index is calculated by reference to the prices of the stocks included in the Index Components without taking into consideration the value of dividends paid on those stocks. The trading value of the Notes and final return on the Notes may also differ from the results of the Composite Index for the reasons discussed below under “Many factors affect the trading value of the Notes; these factors interrelate in complex ways and the effect of any one factor may offset or magnify the effect of another factor”.

S-8

The long and short positions of the Index Components will have a substantial effect on the level of the Composite Index, and in turn, the value of the Notes

The Composite Index will reflect a leveraged long position in the Stock Basket equal to 150% of the Starting Value and a short position in the Select Sector Basket equal to 50% of the Starting Value. The leveraged position offers the potential for significant increases in the level of the Composite Index due to increases in the value of Stock Basket, but also entails a high degree of risk, including the risk of substantial decreases in the level of the Composite Index if there is a decrease in the value of Stock Basket. In addition, as a result of the short position, any increases in the value of the Select Sector Basket will adversely affect the level of the Composite Index, and may offset any gains in the level of the Composite Index related to increases in the level of the Stock Basket.

A trading market for the Notes is not expected to develop

The Notes will not be listed on any securities exchange and we do not expect a trading market for the Notes to develop. Although our affiliate MLPF&S has indicated that it expects to bid for Notes offered for sale to it by Note holders, it is not required to do so and may cease making such bids at any time. The limited trading market for your Notes may affect the price that you receive for your Notes if you do not wish to hold your investment until maturity.

Many factors affect the trading value of the Notes; these factors interrelate in complex ways and the effect of any one factor may offset or magnify the effect of another factor

The trading value of the Notes will be affected by factors that interrelate in complex ways. It is important for you to understand that the effect of one factor may offset the increase in the trading value of the Notes caused by another factor and that the effect of one factor may exacerbate the decrease in the trading value of the Notes caused by another factor. The following paragraphs describe the expected impact on the market value of the Notes given a change in a specific factor, assuming all other conditions remain constant.

The level of the Composite Index is expected to affect the trading value of the Notes. The value of the Notes will depend substantially on the amount by which the Composite Index exceeds or does not exceed the Starting Value. The value of the Notes is related to the Composite Index, and consequently, a sale of the Notes may result in a loss. Additionally, because the trading value and perhaps final return on your Notes is dependent on factors in addition to the Composite Index, such as our credit rating, an increase in the level of the Composite Index will not reduce the other investment risks related to the Notes.

Changes in dividend yields of the Component Stocks are expected to affect the trading value of the Notes. In general, if dividend yields on the Component Stocks in which there is a long position increase, we expect that the value of the Notes will decrease and, conversely, if dividend yields on the Component Stocks in which there is a long position decrease, we expect that the value of the Notes will increase. In general, if dividend yields on the Component Stocks in which there is a short position decrease, we expect that the value of the Notes will decrease and, conversely, if dividend yields on the Component Stocks in which there is a short position increase, we expect that the value of the Notes will increase.

Changes in our credit ratings may affect the trading value of the Notes. Our credit ratings are an assessment of our ability to pay our obligations. Consequently, real or anticipated changes in our credit ratings may affect the trading value of the Notes. However, because your return on your Notes is dependent upon factors in addition to our ability to pay our obligations under the Notes, such as the percentage increase, if any, in the level of the Composite Index at maturity, an improvement in our credit ratings will not reduce the other investment risks related to the Notes.

S-9

Purchases and sales by us and our affiliates may affect your return

We and our affiliates may from time to time buy or sell the Component Stocks or futures or options contracts on the Component Stocks or the Select Sector Indices for our own accounts for business reasons and expect to enter into such transactions in connection with hedging our obligations under the Notes. These transactions could affect the price of the Component Stocks or the Select Sector Indices and, in turn, the value of the Composite Index, in a manner that would be adverse to your investment in the Notes. Any purchases or sales by us, our affiliates or others on our behalf on or before the Pricing Date may temporarily increase or decrease the prices of the Component Stocks or the Select Sector Indices. Temporary increases or decreases in the market prices of the Component Stocks or the Select Sector Indices may also occur as a result of the purchasing activities of other market participants. Consequently, the prices of the Component Stocks or the Select Sector Indices may change subsequent to the Pricing Date, affecting the level of the Composite Index and therefore the market value of the Notes.

Potential conflicts

Our subsidiary MLPF&S is our agent for the purposes of calculating the Ending Value and Redemption Amount. Under certain circumstances, MLPF&S’ role as our subsidiary and its responsibilities as calculation agent for the Notes could give rise to conflicts of interest. These conflicts could occur, for instance, in connection with its determination as to whether the level of the Composite Index can be calculated on a particular trading day, or in connection with judgments that it would be required to make in the event of a discontinuance of a Select Sector Index. See the sections entitled “Description of the Notes—Adjustments to the Index Components; Market Disruption Events” and “—Discontinuance of a Published Index” in this prospectus supplement. MLPF&S is required to carry out its duties as calculation agent in good faith and using its reasonable judgment. However, you should be aware that because we control MLPF&S, potential conflicts of interest could arise.

We have entered into an arrangement with one of our subsidiaries to hedge the market risks associated with our obligation to pay amounts due at maturity on the Notes. This subsidiary expects to make a profit in connection with this arrangement. We did not seek competitive bids for this arrangement from unaffiliated parties.

Amounts payable on the Notes may be limited by state law

New York State law governs the 1983 Indenture under which the Notes will be issued. New York has usury laws that limit the amount of interest that can be charged and paid on loans, which includes debt securities like the Notes. Under present New York law, the maximum rate of interest is 25% per annum on a simple interest basis. This limit may not apply to debt securities in which $2,500,000 or more has been invested.

While we believe that New York law would be given effect by a state or federal court sitting outside of New York, many other states also have laws that regulate the amount of interest that may be charged to and paid by a borrower. We will promise, for the benefit of the Note holders, to the extent permitted by law, not to voluntarily claim the benefits of any laws concerning usurious rates of interest.

Uncertain tax consequences

You should consider the tax consequences of investing in the Notes, aspects of which are uncertain. See the section entitled “United States Federal Income Taxation” in this prospectus supplement.

S-10

ML&Co. will issue the Notes as a series of senior debt securities under the 1983 Indenture, which is more fully described in the accompanying prospectus. The Notes will mature on January 30, 2006.

The Notes are not subject to redemption by ML&Co. at our option before the stated maturity date except as described below under the section entitled “Redemption Event”. If an Event of Default occurs with respect to the Notes, beneficial owners of the Notes may accelerate the maturity of the Notes, as described under “—Events of Default and Acceleration” in this prospectus supplement and “Description of Debt Securities—Events of Default” in the accompanying prospectus.

ML&Co. will issue the Notes in denominations of whole Units each with an original public offering price of $10 per Unit. You may transfer the Notes only in whole Units. You will not have the right to receive physical certificates evidencing your ownership except under limited circumstances. Instead, we will issue the Notes in the form of a global certificate, which will be held by The Depository Trust Company, also known as DTC, or its nominee. Direct and indirect participants in DTC will record your ownership of the Notes. You should refer to the section entitled “Description of the Debt Securities—Depositary” in the accompanying prospectus.

The Notes will not have the benefit of any sinking fund.

Interest

The Notes will bear interest at a rate of 2.5% per year on the $10 principal amount of each Unit from and including June 29, 2004 or from the most recent interest payment date for which interest has been paid or provided for, to but excluding the stated maturity date or redemption date, as applicable. We will pay interest on the Notes in cash semiannually in arrears on January 30 and July 30 of each year, beginning July 30, 2004, and on the maturity date or redemption date, as applicable. We will pay this interest to the persons in whose names the Notes are registered at the close of business on the immediately preceding January 15 and July 15, respectively, whether or not a Business Day. Notwithstanding the foregoing, upon redemption, the final payment of interest will be paid to the person to whom ML&Co. pays the Redemption Amount. Interest on the Notes will be computed on the basis of a 360-day year of twelve 30-day months. If an interest payment date falls on a day that is not a Business Day, that interest payment will be made on the next Business Day and no additional interest will accrue as a result of the delayed payment.

“Business Day” means each Monday, Tuesday, Wednesday, Thursday and Friday that is not a day on which banking institutions in The City of New York are authorized or obligated by law to close.

Payment at Maturity

For each Note, the holder will be entitled to receive the Redemption Amount, as provided below.

Determination of the Redemption Amount

The “Redemption Amount” per Unit will be determined by the calculation agent and will equal:

| $10.00 |

× | ( | Ending Value |

) |

||||||||

| Starting Value |

The “Starting Value” was set to 100.00 on the Pricing Date.

S-11

For the purpose of determining the Redemption Amount, the “Ending Value” will be determined by the calculation agent and will equal the average, arithmetic mean, of the closing levels of the Composite Index determined on each of the first five Calculation Days during the Calculation Period. If there are fewer than five Calculation Days during the Calculation Period, then the Ending Value will equal the average, arithmetic mean, of the closing levels of the Composite Index on those Calculation Days. If there is only one Calculation Day during the Calculation Period, then the Ending Value will equal the closing level of the Composite Index on that Calculation Day. If no Calculation Days occur during the Calculation Period, then the Ending Value will equal the closing level of the Composite Index determined on the last scheduled Index Business Day in the Calculation Period, regardless of the occurrence of a Market Disruption Event on that day.

The “Calculation Period” means the period from and including the seventh scheduled Index Business Day prior to the maturity date to and including the second scheduled Index Business Day prior to the maturity date.

A “Calculation Day” means any Index Business Day during the Calculation Period on which a Market Disruption Event has not occurred.

An “Index Business Day” means any day on which the New York Exchange (the “NYSE”), The Nasdaq National Market and the American Stock Exchange (the “AMEX”) are open for trading and which is also a Business Day.

All determinations made by the calculation agent shall be at the sole discretion of the calculation agent and, absent manifest error, shall be conclusive for all purposes and binding on ML&Co. and the holders and beneficial owners of the Notes.

S-12

Hypothetical Returns

The following table illustrates, for a range of hypothetical average closing levels of the Composite Index:

| Ÿ | the percentage change from the Starting Value to the hypothetical average closing level, |

| Ÿ | the total amount payable at maturity for each Unit of the Notes, including the payment of accrued and unpaid interest, |

| Ÿ | the total yield to beneficial owners of the Notes, |

| Ÿ | the pretax annualized yield to beneficial owners of the Notes, and |

| Ÿ | the pretax annualized yield of an investment in the applicable long and short positions in the Component Stocks, which includes an assumed aggregate dividend yield for the Component Stocks, as more fully described in the notes to the table below. |

| Hypothetical average closing level during the calculation period |

Percentage change from the Starting Value to the hypothetical average closing level |

Total amount payable at maturity per Unit of the Notes(1) |

Pretax annualized yield on the Notes (2)(3) |

Pretax yield of stocks | ||||

| 60.00 | –40% | $ 6.125 | –24.92% | –23.19% | ||||

| 70.00 | –30% | $ 7.125 | –17.56% | –15.87% | ||||

| 80.00 | –20% | $ 8.125 | –10.57% | –8.78% | ||||

| 90.00 | –10% | $ 9.125 | –3.90% | –1.88% | ||||

| 100.00(5) | 0% | $10.125 | 2.51% | 4.86% | ||||

| 110.00 | 10% | $11.125 | 8.69% | 11.48% | ||||

| 120.00 | 20% | $12.125 | 14.66% | 17.98% | ||||

| 130.00 | 30% | $13.125 | 20.46% | 24.38% | ||||

| 140.00 | 40% | $14.125 | 26.09% | 30.70% |

| (1) | The amounts specified in this column include payment of accrued and unpaid interest payable on the maturity date. |

| (2) | This yield: |

| (a) | assumes coupon payments are (i) made semiannually on the 30th of January and July of each year during the term of the Notes, beginning July 30, 2004, and (ii) reinvested for the remainder of the term of the Notes at the applicable yield listed in this column; |

| (b) | assumes an investment term from June 29, 2004 to January 30, 2006, a term equal to that of the Notes; and |

| (c) | is computed on the basis of a 360-day year of twelve 30-day months compounded annually. |

| (3) | The annualized rates of return are calculated on a semiannual bond equivalent basis. |

| (4) | This yield assumes: |

| (a) | a percentage change in the aggregate price of the long stock positions and the short stock positions which results in an aggregate percentage change that equals the percentage change in the Composite Index from the Starting Value to the relevant hypothetical average closing level; |

| (b) | a constant dividend yield of 3.73% per annum for the stocks included in the Stock Basket and 1.61% for the stocks included in the Select Sector Basket, paid quarterly from the date of initial delivery of the Notes, applied to their respective values (dividends paid on stocks included in the Select Sector Basket will decrease this yield while dividends paid on stocks included in the Stock Basket will increase this yield) at the end of each quarter assuming the aggregate dividends payable increases or decreases linearly from the value of such Index Component used to set the Starting Value to 100.00 to the percentage change required to arrive at the applicable hypothetical average closing level; |

| (c) | no transaction fees or expenses or margin charges; and |

| (d) | an investment term from June 29, 2004 to January 30, 2006, a term expected to be equal to that of the Notes. |

| (5) | This is the Starting Value. |

The above figures are for purposes of illustration only. The actual Redemption Amount, received by you, if any, and the resulting total and pretax annualized yield will depend on the actual Ending Value determined by the calculation agent as described in this prospectus supplement.

S-13

Redemption Event

If on any date the closing level of the Composite Index is equal to or less than 50.00, the Notes will be redeemed on the fifth Business Day following such date (the “Early Redemption Date”). If this redemption event is triggered, we will pay you on the Early Redemption Date a cash payment, in addition to accrued and unpaid interest, per Note equal to the Redemption Amount, as described above under “—Payment at Maturity”; provided, however, the Ending Value shall be equal to the average of the closing levels of the Composite Index on the two Index Business Days immediately succeeding the date the closing level of the Composite Index was less than or equal to 50.00, provided that if a Market Disruption Event occurs on either date and if there is only one Calculation Day, the Ending Value will be determined on that Calculation Day, and if a Market Disruption Event occurs on both dates, the Ending Value will be determined using the closing level of the Composite Index on the second Index Business Day following the date the closing level of the Composite Index was less than or equal to 50.00, regardless of the occurrence of a Market Disruption Event on such date.

The amount payable on an Early Redemption Date will be delivered and paid to the holder of a Note on the Early Redemption Date; provided, however, that in the event that the Early Redemption Date falls after a record date for the payment of interest on the Notes but prior to the next succeeding scheduled interest payment date, the portion of the amount payable on an Early Redemption Date equal to the accrued interest amount will be paid to the person who was the holder of the Note as of such record date.

Adjustments to the Index Components; Market Disruption Events

If at any time either the AMEX or Standard & Poor’s, a division of The McGraw-Hill Companies, Inc. or Standard & Poor’s (“S&P”) (each an “Index Publisher”), makes a material change in the formula for or the method of calculating the Composite Index or either Select Sector Index (collectively, the “Published Indices”), respectively, or in any other way materially modifies a Published Index so that the Published Index does not, in the opinion of the calculation agent, fairly represent the value of the Published Index had those changes or modifications not been made, then, from and after that time, the calculation agent will, at the close of business in New York, New York, on each date that the closing level of the Composite Index is to be calculated, make those adjustments as, in the good faith judgment of the calculation agent, may be necessary in order to arrive at a calculation of a value of a stock index comparable to each Published Index as if those changes or modifications had not been made, and calculate the closing value with reference to the Published Index , as so adjusted. Accordingly, if the method of calculating the Published Index is modified so that the value of the Published Index is a fraction or a multiple of what it would have been if it had not been modified, e.g., due to a split, then the calculation agent shall adjust the Published Index in order to arrive at a value of the Published Index as if it had not been modified, e.g., as if a split had not occurred.

“Market Disruption Event” means either of the following events as determined by the calculation agent:

| (A) | the suspension of or material limitation on trading for more than two hours of trading, or during the one-half hour period preceding the close of trading, on the applicable exchange, in 20% or more of the stocks which then comprise the Stock Basket (the “Basket Stocks”) or underlying each Index Component contained in the Select Sector Basket or any successor index; or |

| (B) | the suspension of or material limitation on trading, in each case, for more than two hours of trading, or during the one-half hour period preceding the close of trading, on the applicable exchange, whether by reason of movements in price otherwise exceeding levels permitted by the relevant exchange or otherwise, in option contracts or futures contracts related to a Select Sector Index, or any successor index, which are traded on any major U.S. exchange. |

For the purpose of the above definition:

| (1) | a limitation on the hours in a trading day and/or number of days of trading will not constitute a Market Disruption Event if it results from an announced change in the regular business hours of the relevant exchange, and |

S-14

| (2) | for the purpose of clause (A) above, any limitations on trading during significant market fluctuations under NYSE Rule 80A, or any applicable rule or regulation enacted or promulgated by the NYSE or any other self regulatory organization or the SEC of similar scope as determined by the calculation agent, will be considered “material”. |

As a result of terrorist attacks, the financial markets were closed from September 11, 2001 through September 14, 2001 and values of the Basket Stocks and the Select Sector Indices are not available for such dates. Such market closures would have constituted Market Disruption Events.

Discontinuance of a Published Index

If either Index Publisher discontinues publication of its respective Published Index and the Index Publisher or another entity publishes a successor or substitute index that the calculation agent determines, in its sole discretion, to be comparable to its respective Published Index (a “successor index”), then, upon the calculation agent’s notification of any determination to the indenture trustee and ML&Co., the calculation agent will substitute the successor index as calculated by the Index Publisher or any other entity for the Published Index and calculate the closing value as described above under “—Payment at Maturity”. Upon any selection by the calculation agent of a successor index, ML&Co. shall cause notice to be given to holders of the Notes.

In the event that an Index Publisher discontinues publication of a Published Index and:

| Ÿ | the calculation agent does not select a successor index, or |

| Ÿ | the successor index is no longer published on any of the Calculation Days, |

the calculation agent will compute a substitute value for the Published Index in accordance with the procedures last used to calculate the Published Index before any discontinuance. If a successor index is selected or the calculation agent calculates a value as a substitute for the Published Index as described below, the successor index or value will be used as a substitute for the Published Index for all purposes, including for purposes of determining whether a Market Disruption Event exists.

If an Index Publisher discontinues publication of a Published Index before the Calculation Period and the calculation agent determines that no successor index is available at that time, then on each Index Business Day until the earlier to occur of:

| Ÿ | the determination of the Ending Value, or |

| Ÿ | a determination by the calculation agent that a successor index is available, |

the calculation agent will determine the value that would be used in computing the Redemption Amount as described in the preceding paragraph as if that day were a Calculation Day. The calculation agent will cause notice of each value to be published not less often than once each month in The Wall Street Journal (the “WSJ”) or another newspaper of general circulation, and arrange for information with respect to these values to be made available by telephone.

Notwithstanding these alternative arrangements, discontinuance of the publication of a Published Index may adversely affect trading in the Notes.

S-15

Events of Default and Acceleration

In case an Event of Default with respect to any Notes has occurred and is continuing, the amount payable to a beneficial owner of a Note upon any acceleration permitted by the Notes, with respect to each Unit, will be equal to the Redemption Amount, if any, calculated as though the date of early repayment were the stated maturity date of the Notes. See the section entitled “—Payment at Maturity” in this prospectus supplement. If a bankruptcy proceeding is commenced in respect of ML&Co., the claim of the beneficial owner of a Note may be limited, under Section 502(b)(2) of Title 11 of the United States Code, to the original public offering price of the Note plus an additional amount of contingent interest calculated as though the date of the commencement of the proceeding was the maturity date of the Notes.

In case of default in payment of the Notes, whether at any interest payment date, the stated maturity date, the Early Redemption Date or upon acceleration, from and after that date the Notes will bear interest, payable upon demand of their beneficial owners, at the rate of 1.25% per year to the extent that payment of any interest is legally enforceable on the unpaid amount due and payable on that date in accordance with the terms of the Notes to the date payment of that amount has been made or duly provided for.

S-16

Composite Index

The Composite Index is designed to allow investors to participate in the percentage change in the value of leveraged long positions in ten stocks (collectively, the “Stock Basket”) and short positions in two equity sector indices (each, a “Select Sector Index” and together, the “Select Sector Basket”), the ten stocks and the two indices composing the Composite Index (each, an “Index Component”), over the term of the Notes. Each of the Index Components is described, respectively, in the sections entitled “—Stock Basket” and “—Select Sector Basket” below. Each Index Component has been assigned a weighting and such weighting reflects the relative contribution that Index Component will make to the level of the Composite Index. A positive weighting indicates that the Composite Index is long a particular Index Component. A negative weighting indicates that the Composite Index is short a particular Index Component. The weightings for each Index Component are disclosed below.

The Index Publishers have no obligations relating to the Notes or amounts to be paid to you, including any obligation to take the needs of ML&Co. or of beneficial owners of the Notes into consideration for any reason. The Index Publishers will not receive any of the proceeds of the offering of the Notes and are not responsible for, and have not participated in, the offering of the Notes and are not responsible for, and will not participate in, the determination or calculation of the amount receivable by beneficial owners of the Notes.

The Index Publishers are under no obligation to continue the calculation and dissemination of any of the Index Components. The Notes are not sponsored, endorsed, sold or promoted by the Index Publishers. No inference should be drawn from the information contained in this prospectus supplement that the Index Publishers make any representation or warranty, implied or express, to ML&Co., the holder of the Notes or any member of the public regarding the advisability of investing in securities generally or in the Notes in particular or the ability of the Index Components or the Composite Index to track general stock market performance.

Determination of the Multiplier for each Index Component

A fixed factor (the “Multiplier”) was determined for each Index Component based upon the weighting of each Index Component. The Multiplier for each Index Component was calculated on the Pricing Date and equals:

| Ÿ | the weighting for the Index Component multiplied by 100, divided by |

| Ÿ | the most recent available closing value of the Index Component. |

The Multipliers were calculated in this way so that the Composite Index equaled 100.00 on the Pricing Date. The Multipliers will be revised only in connection with the annual reconstitution of the Stock Basket, except that the calculation agent may in its good faith judgment adjust the Multiplier of any Index Component in the event such Index Component is changed or modified in a manner that does not, in the opinion of the calculation agent, fairly represent the value of such Index Component had those changes or modifications not been made.

The Multipliers for each Index Component are listed under “—Computation of the Composite Index” below.

Computation of the Composite Index

The AMEX calculates the closing level of the Composite Index by summing the products of the most recently available closing value of each Index Component on a Calculation Day and the Multiplier applicable to each Index Component. If a scheduled Calculation Day is not an Index Business Day or a Market

S-17

Disruption Event (as defined below) occurs or is continuing on such day, the next scheduled Index Business Day immediately following such day will be the Calculation Day, regardless of whether a Market Disruption Event occurs or is continuing on such day. The AMEX will disseminate the value of the Composite Index (under the symbol “JKC”) based on the most recently reported prices of each Index Component (as reported by the exchange or trading system on which each Index Component is listed or traded), at approximately 15-second intervals during the AMEX’s business hours and the end of each Index Business Day via the Consolidated Tape Association’s Network B.

The level of the Composite Index will vary based on the appreciation or depreciation of each Index Component and on whether there is a long or short position in that Index Component. For an Index Component in which there is a long position, any appreciation in that Index Component will result in an increase in the level of the Composite Index. Conversely, any depreciation in an Index Component in which there is a long position will result in a decrease in the level of the Composite Index. For an Index Component in which there is a short position, any depreciation in that Index Component will result in an increase in the level of the Composite Index. Conversely, any appreciation in an Index Component in which there is a short position will result in a decrease in the level of the Composite Index. On the Pricing Date, for each Index Component, the weight, initial closing value, Multiplier and initial Composite Index level for each Index Component were as follows:

| Index Components |

Symbol |

Weight |

Closing Value (1) |

Multiplier (2) |

Composite Points | |||||

| Altria Group, Inc. |

MO | 15% | 48.47 | 0.309470 | 15 | |||||

| Citigroup Inc. |

C | 15% | 47.24 | 0.317528 | 15 | |||||

| E.I. du Pont de Nemours and Company |

DD | 15% | 44.40 | 0.337838 | 15 | |||||

| Exxon Mobil Corporation |

XOM | 15% | 45.46 | 0.329960 | 15 | |||||

| General Electric Company |

GE | 15% | 33.42 | 0.448833 | 15 | |||||

| General Motors Corporation |

GM | 15% | 48.26 | 0.310816 | 15 | |||||

| J.P. Morgan Chase & Co. |

JPM | 15% | 37.62 | 0.398724 | 15 | |||||

| Merck & Co., Inc. |

MRK | 15% | 47.81 | 0.313742 | 15 | |||||

| SBC Communications Inc. |

SBC | 15% | 24.25 | 0.618557 | 15 | |||||

| Verizon Communications Inc. |

VZ | 15% | 35.45 | 0.423131 | 15 | |||||

| Consumer Discretionary Select Sector Index |

IXY | –25%(3) |

319.42 | -0.078267 | –25 | |||||

| Financial Select Sector Index |

IXM | –25%(3) |

285.86 | -0.087455 | –25 | |||||

| Starting Value: | 100 | |||||||||

| (1) | This was the closing value or, in the case of an Index Component that is contained in the Stock Basket, the closing market price, of the Index Component on the Pricing Date. |

| (2) | The Multiplier equals weight multiplied by 100, and then divided by the applicable closing value on the Pricing Date. |

| (3) | This figure represents a short position in the Index Component. |

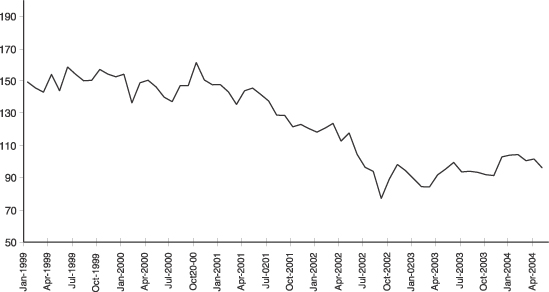

Hypothetical Historical Data on the Composite Index

The Composite Index did not exist until the Pricing Date. We have, however, included a table showing monthly hypothetical historical levels of the Composite Index for each month (the “Hypothetical Historical Month-End Closing Level”) from January 1999 to May 2004 based upon the applicable Multiplier for each Index Component. The historical values of each Basket Stock are included in Annex A to this pricing supplement and the historical values for each Select Sector Index can be found in the section“—The Select Sector Basket” below. All Hypothetical Historical Month-End Closing Levels presented in the following table were calculated by the calculation agent.

The Hypothetical Historical Month-End Closing Levels have been calculated hypothetically on the same basis that the Composite Index will be calculated. The value of the Composite Index was set to 100 on the

S-18

Pricing Date and the Multipliers are used to provide an illustration of past movements of the Hypothetical Historical Month-End Closing Levels only. You should understand we have provided this historical information to help you evaluate the behavior of the Composite Index in various economic environments. These Hypothetical Historical Month-End Closing Levels are not necessarily indicative of the future performance of the Composite Index or what the value of the Notes may be. Any historical upward or downward trend in the level of the Composite Index during any period set forth below is not any indication that the Composite Index is more or less likely to increase or decrease at any time during the term of the Notes.

| 1999 |

2000 |

2001 |

2002 |

2003 |

2004 | |||||||

| January |

149.44 | 154.19 | 147.70 | 118.08 | 89.03 | 103.73 | ||||||

| February |

145.66 | 136.29 | 143.15 | 120.51 | 84.01 | 104.03 | ||||||

| March |

143.00 | 148.86 | 135.33 | 123.52 | 83.85 | 100.22 | ||||||

| April |

154.06 | 150.44 | 143.87 | 112.46 | 91.38 | 101.29 | ||||||

| May |

143.85 | 146.29 | 145.54 | 117.56 | 95.01 | 95.81 | ||||||

| June |

158.71 | 139.87 | 141.66 | 104.17 | 99.14 | |||||||

| July |

154.18 | 137.08 | 137.49 | 96.06 | 93.21 | |||||||

| August |

150.12 | 147.08 | 128.68 | 93.59 | 93.63 | |||||||

| September |

150.39 | 147.09 | 128.45 | 76.64 | 92.96 | |||||||

| October |

157.20 | 161.50 | 121.38 | 88.71 | 91.50 | |||||||

| November |

154.31 | 150.62 | 122.87 | 97.85 | 90.95 | |||||||

| December |

152.58 | 147.64 | 120.26 | 94.12 | 102.60 |

The following graph sets forth the hypothetical historical performance of the Composite Index presented in the table above, based upon the Multipliers set on the Pricing Date. Past movements of the Composite Index are not necessarily indicative of the future Composite Index levels.

Stock Basket

On any Business Day the value of the Stock Basket will equal the sum of the products of the current market price for each of the Basket Stocks and the applicable Multiplier (the sum equals the “Stock Basket Portfolio Value”).

S-19

Determination of Stock Basket Portfolio

At any time the “Stock Basket Portfolio” will consist of the then current Basket Stocks. The stocks in the Stock Basket Portfolio are the ten common stocks in the Dow Jones Industrial Average (the “DJIA”) as determined by the AMEX as having the highest Dividend Yield as of the second Index Business Day prior the Pricing Date. We have included a brief description of each of the companies that are included in the Stock Basket (the “Stock Basket Companies”) and their corresponding Dividend Yield and historical stock price information in Annex A to this prospectus supplement. “Dividend Yield” for each common stock is determined by annualizing the last quarterly or semi-annual ordinary cash dividend for which the ex-dividend date has occurred, excluding any extraordinary dividend, and dividing the result by the last available sale price for each stock on its primary exchange on the date that Dividend Yield is to be determined.

The Multiplier applicable to each Basket Stock will be recalculated by the AMEX on the Anniversary Date of each year, or in certain circumstances on a day shortly thereafter as described below. The Multiplier applicable to each Basket Stock will be set to equal the number of shares of that stock, or portion thereof, based upon the closing market price of that stock on the Anniversary Date, so that each stock represents approximately an equal percentage of the Composite Index as of the Anniversary Date.

Dow Jones Industrial Average

The DJIA is comprised of 30 common stocks chosen by the editors of the WSJ as representative of the broad market of American industry generally. The companies are major factors in their industries and their stocks are typically widely held by individuals and institutional investors. Changes in the composition of the DJIA are made entirely by the editors of the WSJ without consultation with the companies, the stock exchange or any official agency or ML&Co. For the sake of continuity, changes are made infrequently. Most substitutions have been the result of mergers, but from time to time, changes may be made to achieve a better representation. The components of the DJIA may be changed at any time for any reason. Dow Jones & Company, Inc., publisher of the WSJ, is not affiliated with ML&Co., has not participated in any way in the creation of the Notes or in the selection of stocks to be included in the Stock Basket Portfolio and has not reviewed or approved any information included in this prospectus supplement.

The first DJIA, consisting of 12 stocks, was published in the WSJ in 1896. The list grew to 20 stocks in 1916 and to 30 stocks on October 1, 1928. For two periods of 17 consecutive years each, there were no changes to the list: March 15, 1939 through July 2, 1956 and June 2, 1959 through August 8, 1976.

Annual Stock Basket Portfolio Reconstitution

As of the close of business on each Anniversary Date, the Stock Basket Portfolio will be reconstituted to include the ten common stocks in the DJIA having the highest Dividend Yield (the “New Stocks”) on the second scheduled Index Business Day prior to the applicable Anniversary Date (the “Annual Determination Date”). “Anniversary Date” will mean the anniversary date of the Pricing Date of each year; provided, however, that if the date is not an Index Business Day or a Market Disruption Event occurs on that date, then the Anniversary Date for that year will mean the immediately succeeding Index Business Day on which a Market Disruption Event does not occur. The AMEX will only add a stock having characteristics as of the applicable Annual Determination Date that will permit the Stock Basket to remain within the criteria specified in the rules of the AMEX and within the applicable rules of the SEC. Except as provided below, the criteria and rules will apply only on an Annual Determination Date to exclude a proposed New Stock. If a proposed New Stock does not meet these criteria or rules, the AMEX will replace it with the common stock in the DJIA with the next highest Dividend Yield which meets the criteria and rules. These criteria currently provide, among other things, (1) that each Component Stock must have a minimum market value of at least $75 million, except that up to 10% of the Component Stocks in the Stock Basket may have a market value of $50 million; (2) that each Component Stock

S-20

must have an average monthly trading volume in the preceding six months of not less than 1,000,000 shares, except that up to 10% of the Component Stocks in the Stock Basket may have an average monthly trading volume of 500,000 shares or more in the last six months; (3) 90% of the Stock Basket’s numerical index value and at least 80% of the total number of Basket Stocks will meet the then current criteria for standardized option trading set forth in the rules of the AMEX; and (4) all Basket Stocks will either be listed on the AMEX, the NYSE or traded through the facilities of the National Association of Securities Dealers Automated Quotation System and reported as National Market System Securities. In addition, if as of any Annual Determination Date any Basket Stock or proposed New Stock is also included in any Index Component comprising the Select Sector Basket, the reconstituted Stock Basket Portfolio will not include that Basket Stock or proposed New Stock.

The Multiplier for each New Stock will be determined by the AMEX and will equal the number of shares of each New Stock, based upon the closing market price of that New Stock on the Anniversary Date, so that each New Stock represents approximately an equal percentage of the Composite Index on the applicable Anniversary Date. As an example, if the portion of the Composite Index represented by the Stock Basket in effect at the close of business on an Anniversary Date equaled 200, then each of the ten New Stocks would be allocated a portion of the value of the Composite Index equal to 20 and if, for example, the closing market price of a New Stock on the Anniversary Date was 40, the applicable Multiplier would be 0.5. If the portion of the Composite Index represented by the stock basket equaled 80, then each of the ten New Stocks would be allocated a portion of the value of the Composite Index equal to 8 and if the closing market price of a New Stock on the Anniversary Date was 40, the applicable Multiplier would be 0.2.

Adjustments to the Basket Stock Multipliers and Stock Basket Portfolio

The Multiplier applicable to any Stock Basket Stock and the Stock Basket Portfolio will be adjusted as follows:

1. If a Basket Stock is subject to a stock split or reverse stock split, then once the split has become effective, the Multiplier applicable to that Basket Stock will be adjusted to equal the product of the number of shares of that Basket Stock issued with respect to one share of that Basket Stock and the prior multiplier.

2. If a Basket Stock is subject to a stock dividend, issuance of additional shares of the Basket Stock, that is given equally to all holders of shares of the issuer of that Basket Stock, then once the dividend has become effective and that Basket Stock is trading ex-dividend, the Multiplier applicable to that Basket Stock will be adjusted so that the new Multiplier will equal the product of the number of shares of that Basket Stock issued with respect to one share of that Basket Stock and the prior multiplier.

3. If a Stock Basket Company is being liquidated or is subject to a proceeding under any applicable bankruptcy, insolvency or other similar law, that Basket Stock will continue to be included in the Stock Basket Portfolio so long as a market price for that Basket Stock is available. If a market price is no longer available for a Basket Stock for whatever reason, including the liquidation of the issuer of the Basket Stock or the subjection of the issuer of the Basket Stock to a proceeding under any applicable bankruptcy, insolvency or other similar law, then the value of that Basket Stock will equal zero in connection with calculating the Stock Basket Portfolio Value for so long as no market price is available, and no attempt will be made to immediately find a replacement stock or increase the value of the Stock Basket Portfolio to compensate for the deletion of that Basket Stock. If a market price is no longer available for a Basket Stock as described above, the Stock Basket Portfolio Value will be computed based on the remaining Basket Stocks for which market prices are available and no New Stock will be added to the Stock Basket Portfolio until the annual reconstitution of the Stock Basket Portfolio. As a result, there may be periods during which the Stock Basket Portfolio contains fewer than ten Basket Stocks.

4. If a Stock Basket Company has been subject to a merger or consolidation and is not the surviving entity or is nationalized, then a value for that Basket Stock will be determined at the time the issuer is merged or consolidated or nationalized and will equal the last available market price for that Basket Stock and that value will be constant until the Stock Basket Portfolio is reconstituted. At that time, no adjustment will be made to the Multiplier of the relevant Basket Stock.

S-21

5. If a Stock Basket Company issues to all of its shareholders equity securities that are publicly traded of an issuer other than the Stock Basket Company, or a tracking stock is issued by a Stock Basket Company to all of its shareholders, then the new equity securities will be added to the Stock Basket Portfolio as a new Basket Stock. The Multiplier applicable to the new Basket Stock will equal the product of the original Multiplier with respect to the Basket Stock for which the new Basket Stock is being issued (the “Original Basket Stock”) and the number of shares of the new Basket Stock issued with respect to one share of the Original Basket Stock.

No adjustments of any Multiplier applicable to a Basket Stock will be required unless the adjustment would require a change of at least 1% in the Multiplier then in effect. The Multiplier resulting from any of the adjustments specified above will be rounded to the nearest ten-thousandth with five hundred-thousandths being rounded upward.

The AMEX expects that no adjustments to the Multiplier applicable to any Basket Stock will be made other than those specified above; however, the AMEX may at its discretion make adjustments to maintain the value of the Composite Index if certain events would otherwise alter the value of the Composite Index despite no change in the market prices of the Basket Stocks.

Select Sector Basket

The Select Sector Basket is comprised of the Consumer Discretionary Select Sector Index (the “Consumer Index”) and the Financial Select Sector Index (the “Financial Index”). Each stock in the S&P 500 is allocated to only one Select Sector Index, and the combined companies of the nine Select Sector Indexes represent all of the companies in the S&P 500.

Description of Consumer Index. The Consumer Index (IXY) is a modified market capitalization-based index intended to track the movements of companies that are components of the S&P 500 and are involved in the development or production of consumer discretionary products. Consumer discretionary products include automobiles and automobile components, consumer durables, apparel, hotels, restaurants, leisure, media and retailing. The Consumer Index, which serves as the benchmark for the Consumer Discretionary Select Sector SPDR Fund (XLY), was established with a value of 250.00 on June 30, 1998.

Month-End Closing Values of the Consumer Index. The following table sets forth the closing value of the Consumer Index at the end of each month, in the period from January 1999 through May 2004. This historical data on the Consumer Index is not necessarily indicative of the future performance of the Consumer Index or what the value of the Notes may be. Any historical upward or downward trend in the closing value of the Consumer Index during any period set forth below is not any indication that the Consumer Index is more or less likely to decline at any time during the term of the Notes. The closing value of the Consumer Index on June 23, 2004 was 319.42.

| 1999 |

2000 |

2001 |

2002 |

2003 |

2004 | |||||||

| January |

275.09 | 271.67 | 285.35 | 295.67 | 224.04 | 312.70 | ||||||

| February |

272.11 | 255.93 | 266.41 | 296.56 | 222.04 | 319.02 | ||||||

| March |

285.33 | 291.27 | 261.04 | 300.20 | 227.98 | 318.53 | ||||||

| April |

293.58 | 287.15 | 273.43 | 292.02 | 254.33 | 313.45 | ||||||

| May |

281.34 | 268.94 | 277.66 | 289.72 | 267.06 | 315.52 | ||||||

| June |

296.97 | 257.56 | 275.63 | 275.35 | 270.92 | |||||||

| July |

274.32 | 260.92 | 290.80 | 242.95 | 276.73 | |||||||

| August |

262.94 | 248.02 | 263.32 | 249.19 | 290.43 | |||||||

| September |

261.57 | 249.28 | 231.10 | 227.61 | 276.49 | |||||||

| October |

283.45 | 245.48 | 241.26 | 242.28 | 301.08 | |||||||

| November |

284.60 | 239.16 | 275.38 | 253.96 | 303.63 | |||||||

| December |

308.96 | 255.95 | 287.84 | 231.68 | 315.28 |

S-22

Description of Financial Index. The Financial Index (IXM) is a modified market capitalization-based index intended to track the movements of companies that are components of the S&P 500 and are involved in the financial industry. Companies in the Financial Index include banks, diversified financial companies, insurance companies and real estate companies. The Financial Index, which serves as the benchmark for the Financial Select Sector SPDR Fund (XLF), was established with a value of 250.00 on June 30, 1998.

Month-End Closing Values of the Financial Index. The following table sets forth the closing value of the Financial Index at the end of each month, in the period from January 1999 through June 2004. This historical data on the Financial Index is not necessarily indicative of the future performance of the Financial Index or what the value of the Notes may be. Any historical upward or downward trend in the closing value of the Financial Index during any period set forth below is not any indication that the Financial Index is more or less likely to decline at any time during the term of the Notes. The closing value of the Financial Index on the Pricing Date was 285.86.

| 1999 |

2000 |

2001 |

2002 |

2003 |

2004 | |||||||

| January |

237.56 | 229.99 | 293.13 | 258.70 | 215.93 | 289.84 | ||||||

| February |

240.45 | 205.00 | 273.44 | 254.54 | 208.84 | 297.12 | ||||||

| March |

249.18 | 242.19 | 264.96 | 271.24 | 207.60 | 293.58 | ||||||

| April |

265.72 | 234.32 | 274.43 | 263.59 | 232.62 | 279.35 | ||||||

| May |

250.69 | 249.65 | 284.93 | 262.71 | 244.42 | 284.11 | ||||||

| June |

260.65 | 234.52 | 284.59 | 249.75 | 244.59 | |||||||

| July |

244.10 | 258.32 | 279.60 | 229.54 | 255.15 | |||||||

| August |

232.62 | 282.25 | 262.15 | 233.81 | 252.16 | |||||||

| September |

219.94 | 288.87 | 246.32 | 206.07 | 253.36 | |||||||

| October |

255.77 | 287.65 | 241.35 | 224.19 | 270.13 | |||||||

| November |

243.29 | 270.52 | 258.17 | 233.01 | 268.94 | |||||||

| December |

238.03 | 294.39 | 263.38 | 220.08 | 281.54 |

Publisher. Standard and Poor’s is the publisher of the two indices comprising the Select Sector Basket.