Exhibit 99.2

Supplemental Information

Fourth Quarter 2004

This information is preliminary and based on company data available at the time of the presentation. It speaks only as of the particular date or dates included in the accompanying pages. Bank of America does not undertake an obligation to, and disclaims any duty to, correct or update any of the information provided. Any forward-looking statements in this information are subject to the forward-looking language contained in Bank of America’s reports filed with the SEC pursuant to the Securities Exchange Act of 1934, which are available at the SEC’s website (www.sec.gov) or at Bank of America’s website (www.bankofamerica.com). Bank of America’s future financial performance is subject to risks and uncertainties as described in its SEC filings.

| Bank of America Corporation |

Results Overview

Full Year 2004

| • | Net income of $14.1 billion or $3.69 per diluted share compared to a reported $3.57 in 2003. |

Excluding merger and restructuring charges of $618 million, $411 million after tax, earnings were $3.80 per diluted share, 6% over 2003.

Merger and restructuring charges in 2004 include $343 million merger charge and $68 million for recently announced infrastructure initiative.

| • | Revenue of $48.9 billion increased 29% over 2003. |

| • | The primary driver of this reported growth is the addition of Fleet results in 2004 which closed April 1, 2004. |

Further comments will refer to proforma statements (as filed on a Form 8-K/A with the SEC on January 18, 2005) including Fleet results for both years for a more meaningful comparison. The unaudited pro forma condensed combined financial information is presented for illustrative purposes only and does not indicate the financial results of the combined companies had the companies actually been combined at the beginning of the period presented and had the impact of possible revenue enhancements, expense efficiencies, hedging activities, asset dispositions, and share repurchases, among other factors, been considered.

| • | Revenue of $52.2 billion increased 4% over 2003 with strong net interest income growth and steady noninterest income fees. |

| • | 8% net interest income growth was led by strength in consumer lending and deposit gathering as well as interest rate risk management activity. This growth was slightly offset by the impact of lower corporate loan balances and a lower contribution from trading related assets. |

| • | Higher equity investment gains, card income, trading profits and service fees were offset by lower mortgage banking and other income to hold noninterest fees flat year to year. |

| • | Securities gains for the year were $2,172 million as the company repositioned the securities portfolio for expected interest rate moves. Securities gains for 2003 were $1,069 million. |

| • | Noninterest expense, excluding merger and restructuring charges of $28.5 billion increased 4%. |

| • | $909 million in merger cost saves in 2004 were offset by higher litigation costs and mutual fund related matters. |

| • | Other expenses rose in connection with transacting higher business volumes and personnel costs associated with business growth in new branches and premier banking. |

| • | Provision expense of $2,769 million decreased 28% from 2003 driven by improvements in commercial asset quality. |

| • | Business highlights: |

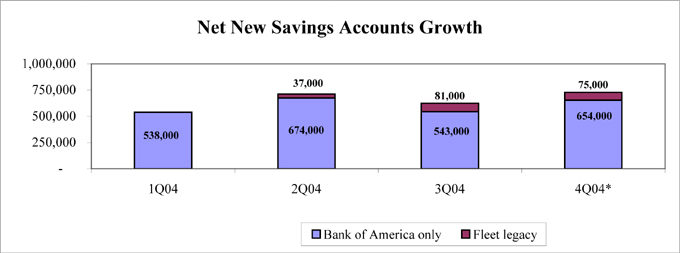

| • | Number of net new checking accounts grew by 2.1 million. |

| • | Number of net new savings accounts grew by 2.6 million. |

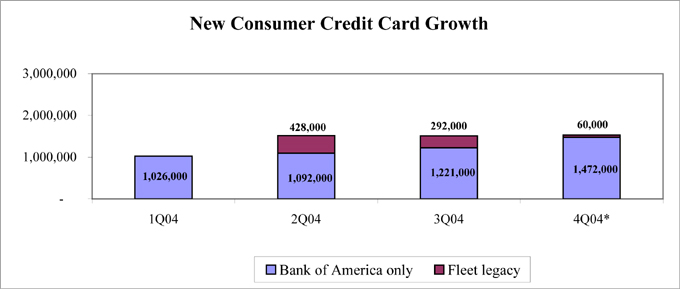

| • | Opened 5.6 million new credit card accounts. |

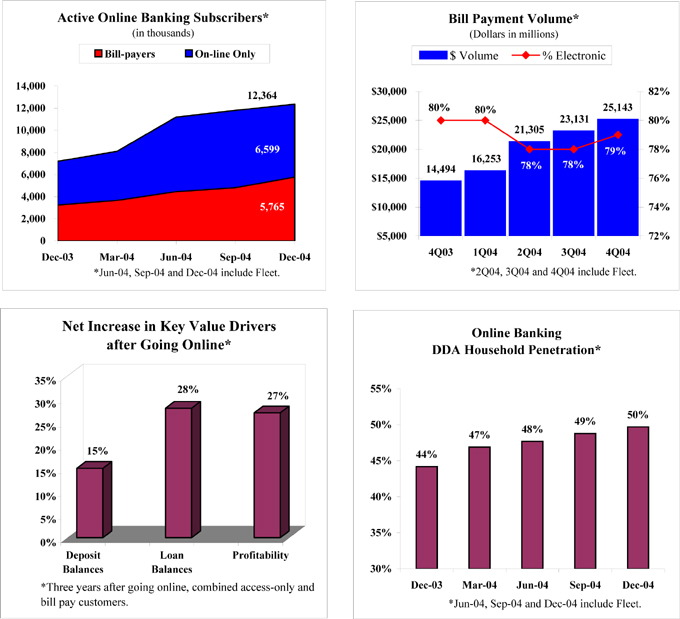

| • | Active online banking users increased to 12.4 million while bill payers reached 5.8 million and volume increased to more than $25 billion in 2004. |

| • | Product sales in 3Q04 increased 21% over same period in 2003 on a proforma basis. |

| • | Core deposits continue to grow climbing to $527 billion and have increased $44 billion or 9% over 2003 on a proforma basis as a result of improved customer delight, improved sales processes and new product offerings. |

| • | Loans grew 6% to $505 billion on a proforma average basis with strength in card and consumer real estate and moderate steady commercial growth offset somewhat by large corporate loans declining. |

| • | Assets under management ended the year at $451 billion and reflect a continued shift in mix of assets to more equities and less cash and fixed income. |

| • | Banc of America securities grew market share in several debt products in 2004 and maintained the #2 position in syndicated lending. |

| • | Returned more than $8.8 billion to shareholders in 2004 through dividends and net share repurchases. |

| • | Total return to shareholders including stock price improvement as well as dividends in 2004 was 21.4% beating the performance of all large cap banking competitors as well as twice the rate of the S & P 500. |

| • | Merger integration ahead of schedule. |

| • | Cost savings are on track. $909 million in 2004. |

| • | Banking center rebranding has been completed. |

| • | Customer delight continued to improve throughout the year reaching its highest point in December. |

| • | Added 174,000 net new checking accounts and 193,000 net new savings accounts in legacy Fleet franchise in 2004. |

| • | Sales per seller per day doubled in the Northeast from less than 2 at merger date to more than 4. |

| • | More than 100,000 Northeast customers have accepted offers to become Premier Banking customers. |

| • | “Cross-footprint” transaction volume is steadily increasing. More than 750,000 transactions completed in most recent quarter. |

1

Bank of America Corporation

Consolidated Financial Highlights

(Dollars in millions, except per share information; shares in thousands)

| Year-to- 2004 |

Year-to- 2003 |

Fourth Quarter 2004 |

Third Quarter 2004 |

Second Quarter 2004 |

First Quarter 2004 |

Fourth Quarter 2003 |

||||||||||||||||||||||

| Income statement |

||||||||||||||||||||||||||||

| Total revenue |

$ | 48,894 | $ | 37,914 | $ | 13,714 | $ | 12,587 | $ | 13,062 | $ | 9,531 | $ | 9,635 | ||||||||||||||

| Provision for credit losses |

2,769 | 2,839 | 706 | 650 | 789 | 624 | 583 | |||||||||||||||||||||

| Gains on sales of securities |

2,123 | 941 | 101 | 732 | 795 | 495 | 139 | |||||||||||||||||||||

| Noninterest expense |

27,027 | 20,155 | 7,334 | 7,021 | 7,242 | 5,430 | 5,288 | |||||||||||||||||||||

| Income tax expense |

7,078 | 5,051 | 1,926 | 1,884 | 1,977 | 1,291 | 1,177 | |||||||||||||||||||||

| Net income |

14,143 | 10,810 | 3,849 | 3,764 | 3,849 | 2,681 | 2,726 | |||||||||||||||||||||

| Diluted earnings per common share |

3.69 | 3.57 | 0.94 | 0.91 | 0.93 | 0.91 | 0.92 | |||||||||||||||||||||

| Average diluted common shares issued and outstanding |

3,823,943 | 3,030,356 | 4,106,040 | 4,121,375 | 4,131,290 | 2,933,402 | 2,978,962 | |||||||||||||||||||||

| Dividends paid per common share |

$ | 1.70 | $ | 1.44 | $ | 0.45 | $ | 0.45 | $ | 0.40 | $ | 0.40 | $ | 0.40 | ||||||||||||||

| Performance ratios |

||||||||||||||||||||||||||||

| Return on average assets |

1.35 | % | 1.44 | % | 1.33 | % | 1.37 | % | 1.41 | % | 1.29 | % | 1.42 | % | ||||||||||||||

| Return on average common shareholders’ equity |

16.83 | 21.99 | 15.63 | 15.56 | 16.63 | 22.16 | 22.42 | |||||||||||||||||||||

| Book value per share of common stock |

$ | 24.56 | $ | 16.63 | $ | 24.56 | $ | 24.14 | $ | 23.51 | $ | 16.85 | $ | 16.63 | ||||||||||||||

| Market price per share of common stock: |

||||||||||||||||||||||||||||

| Closing price |

$ | 46.99 | $ | 40.22 | $ | 46.99 | $ | 43.33 | $ | 42.31 | $ | 40.49 | $ | 40.22 | ||||||||||||||

| High closing price for the period |

47.44 | 41.77 | 47.44 | 44.98 | 42.72 | 41.38 | 41.25 | |||||||||||||||||||||

| Low closing price for the period |

38.96 | 32.82 | 43.62 | 41.81 | 38.96 | 39.15 | 36.43 | |||||||||||||||||||||

| Market capitalization |

190,147 | 115,911 | 190,147 | 175,446 | 171,891 | 117,056 | 115,911 | |||||||||||||||||||||

| Number of banking centers-domestic |

5,885 | 4,277 | 5,885 | 5,829 | 5,774 | 4,272 | 4,277 | |||||||||||||||||||||

| Number of ATMs-domestic |

16,771 | 13,241 | 16,771 | 16,728 | 16,672 | 13,168 | 13,241 | |||||||||||||||||||||

| Full-time equivalent employees |

175,742 | 133,549 | 175,742 | 175,523 | 177,986 | 134,374 | 133,549 | |||||||||||||||||||||

Certain prior period amounts have been reclassified to conform to current period presentation.

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

2

Bank of America Corporation

Supplemental Financial Data

(Dollars in millions)

Fully taxable-equivalent basis data

| Year-to- Date 2004 |

Year-to- Date 2003 |

Fourth Quarter 2004 |

Third Quarter 2004 |

Second Quarter 2004 |

First Quarter 2004 |

Fourth Quarter 2003 |

||||||||||||||||||||||

| Net interest income |

$ | 29,513 | $ | 22,107 | $ | 7,956 | $ | 7,836 | $ | 7,751 | $ | 5,970 | $ | 5,745 | ||||||||||||||

| Total revenue |

49,610 | 38,557 | 13,920 | 12,758 | 13,232 | 9,700 | 9,794 | |||||||||||||||||||||

| Net interest yield |

3.26 | % | 3.40 | % | 3.18 | % | 3.30 | % | 3.31 | % | 3.26 | % | 3.43 | % | ||||||||||||||

| Efficiency ratio |

54.48 | 52.27 | 52.69 | 55.03 | 54.73 | 55.98 | 53.98 | |||||||||||||||||||||

Reconciliation to GAAP financial measures

Supplemental financial data presented on an operating basis is a basis of presentation not defined by GAAP (generally accepted accounting principles) that excludes merger and restructuring charges. We believe that the exclusion of the merger and restructuring charges, which represent incremental costs to integrate Bank of America and FleetBoston’s operations and include costs related to an infrastructure initiative undertaken in the third quarter to simplify the Corporation’s business model, provides a meaningful period-to-period comparison and is more reflective of normalized operations.

Shareholder value added (SVA) is a key measure of performance not defined by GAAP that is used in managing our growth strategy orientation and strengthening our focus on generating long-term growth and shareholder value. SVA is used in measuring the performance of our different business units and is an integral component for allocating resources. Each business segment has a goal for growth in SVA reflecting the individual segment’s business and customer strategy.

Other companies may define or calculate supplemental financial data differently. See the Tables below for supplemental financial data and corresponding reconciliation to GAAP financial measures for the years ended December 31, 2004 and 2003, and the quarters ended December 31, 2004, September 30, 2004, June 30, 2004, March 31, 2004 and December 31, 2003.

Reconciliation of net income to operating earnings

| Year-to- Date 2004 |

Year-to- Date 2003 |

Fourth Quarter 2004 |

Third Quarter 2004 |

Second Quarter 2004 |

First Quarter 2004 |

Fourth Quarter 2003 |

||||||||||||||||||||||

| Net income |

$ | 14,143 | $ | 10,810 | $ | 3,849 | $ | 3,764 | $ | 3,849 | $ | 2,681 | $ | 2,726 | ||||||||||||||

| Merger and restructuring charges |

618 | — | 272 | 221 | 125 | — | — | |||||||||||||||||||||

| Related income tax benefit |

(207 | ) | — | (91 | ) | (74 | ) | (42 | ) | — | — | |||||||||||||||||

| Operating earnings |

$ | 14,554 | $ | 10,810 | $ | 4,030 | $ | 3,911 | $ | 3,932 | $ | 2,681 | $ | 2,726 | ||||||||||||||

| Operating basis | ||||||||||||||||||||||||||||

| Diluted earnings per common share |

$ | 3.80 | $ | 3.57 | $ | 0.98 | $ | 0.95 | $ | 0.95 | $ | 0.91 | $ | 0.92 | ||||||||||||||

| Return on average assets |

1.39 | % | 1.44 | % | 1.39 | % | 1.42 | % | 1.44 | % | 1.29 | % | 1.42 | % | ||||||||||||||

| Return on avg common shareholders’ equity |

17.32 | 21.99 | 16.37 | 16.17 | 16.99 | 22.16 | 22.42 | |||||||||||||||||||||

| Efficiency ratio |

53.23 | 52.27 | 50.73 | 53.30 | 53.79 | 55.98 | 53.98 | |||||||||||||||||||||

| Reconciliation of net income to shareholder value added |

||||||||||||||||||||||||||||

| Net income |

$ | 14,143 | $ | 10,810 | $ | 3,849 | $ | 3,764 | $ | 3,849 | $ | 2,681 | $ | 2,726 | ||||||||||||||

| Amortization of intangibles |

664 | 217 | 209 | 200 | 201 | 54 | 54 | |||||||||||||||||||||

| Merger and restructuring charges, net of tax benefit |

411 | — | 181 | 147 | 83 | — | — | |||||||||||||||||||||

| Capital charge |

(9,235 | ) | (5,406 | ) | (2,705 | ) | (2,658 | ) | (2,542 | ) | (1,330 | ) | (1,337 | ) | ||||||||||||||

| Shareholder value added |

$ | 5,983 | $ | 5,621 | $ | 1,534 | $ | 1,453 | $ | 1,591 | $ | 1,405 | $ | 1,443 | ||||||||||||||

Certain prior period amounts have been reclassified to conform to current period presentation.

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

3

Bank of America Corporation

Consolidated Statement of Income

(Dollars in millions, except per share information; shares in thousands)

| Year-to- Date 2004 |

Year-to- Date 2003 |

Fourth Quarter 2004 |

Third Quarter 2004 |

Second Quarter 2004 |

First Quarter 2004 |

Fourth Quarter 2003 | ||||||||||||||||

| Interest income |

||||||||||||||||||||||

| Interest and fees on loans and leases |

$ | 28,216 | $ | 21,668 | $ | 7,922 | $ | 7,508 | $ | 7,237 | $ | 5,549 | $ | 5,580 | ||||||||

| Interest and dividends on securities |

7,265 | 3,068 | 2,068 | 2,078 | 1,907 | 1,212 | 726 | |||||||||||||||

| Federal funds sold and securities purchased under agreements to resell |

2,043 | 1,373 | 712 | 484 | 413 | 434 | 506 | |||||||||||||||

| Trading account assets |

4,016 | 3,947 | 1,035 | 960 | 1,009 | 1,012 | 912 | |||||||||||||||

| Other interest income |

1,687 | 1,507 | 461 | 457 | 424 | 345 | 322 | |||||||||||||||

| Total interest income |

43,227 | 31,563 | 12,198 | 11,487 | 10,990 | 8,552 | 8,046 | |||||||||||||||

| Interest expense |

||||||||||||||||||||||

| Deposits |

6,275 | 4,908 | 1,829 | 1,711 | 1,529 | 1,206 | 1,178 | |||||||||||||||

| Short-term borrowings |

4,434 | 1,871 | 1,543 | 1,152 | 1,019 | 720 | 515 | |||||||||||||||

| Trading account liabilities |

1,317 | 1,286 | 352 | 333 | 298 | 334 | 317 | |||||||||||||||

| Long-term debt |

2,404 | 2,034 | 724 | 626 | 563 | 491 | 450 | |||||||||||||||

| Total interest expense |

14,430 | 10,099 | 4,448 | 3,822 | 3,409 | 2,751 | 2,460 | |||||||||||||||

| Net interest income |

28,797 | 21,464 | 7,750 | 7,665 | 7,581 | 5,801 | 5,586 | |||||||||||||||

| Noninterest income |

||||||||||||||||||||||

| Service charges |

6,989 | 5,618 | 1,891 | 1,899 | 1,783 | 1,416 | 1,436 | |||||||||||||||

| Investment and brokerage services |

3,627 | 2,371 | 1,007 | 972 | 1,013 | 635 | 619 | |||||||||||||||

| Mortgage banking income (loss) |

414 | 1,922 | 156 | (250 | ) | 299 | 209 | 292 | ||||||||||||||

| Investment banking income |

1,886 | 1,736 | 497 | 438 | 547 | 404 | 458 | |||||||||||||||

| Equity investment gains |

861 | 215 | 424 | 220 | 84 | 133 | 215 | |||||||||||||||

| Card income |

4,588 | 3,052 | 1,380 | 1,257 | 1,156 | 795 | 815 | |||||||||||||||

| Trading account profits |

869 | 409 | 269 | 184 | 413 | 3 | 27 | |||||||||||||||

| Other income |

863 | 1,127 | 340 | 202 | 186 | 135 | 187 | |||||||||||||||

| Total noninterest income |

20,097 | 16,450 | 5,964 | 4,922 | 5,481 | 3,730 | 4,049 | |||||||||||||||

| Total revenue |

48,894 | 37,914 | 13,714 | 12,587 | 13,062 | 9,531 | 9,635 | |||||||||||||||

| Provision for credit losses |

2,769 | 2,839 | 706 | 650 | 789 | 624 | 583 | |||||||||||||||

| Gains on sales of securities |

2,123 | 941 | 101 | 732 | 795 | 495 | 139 | |||||||||||||||

| Noninterest expense |

||||||||||||||||||||||

| Personnel |

13,473 | 10,446 | 3,532 | 3,540 | 3,639 | 2,762 | 2,697 | |||||||||||||||

| Occupancy |

2,379 | 2,006 | 648 | 622 | 621 | 488 | 514 | |||||||||||||||

| Equipment |

1,214 | 1,052 | 326 | 309 | 318 | 261 | 263 | |||||||||||||||

| Marketing |

1,349 | 985 | 337 | 364 | 367 | 281 | 268 | |||||||||||||||

| Professional fees |

836 | 844 | 275 | 207 | 194 | 160 | 224 | |||||||||||||||

| Amortization of intangibles |

664 | 217 | 209 | 200 | 201 | 54 | 54 | |||||||||||||||

| Data processing |

1,325 | 1,104 | 371 | 340 | 330 | 284 | 301 | |||||||||||||||

| Telecommunications |

730 | 571 | 216 | 180 | 183 | 151 | 158 | |||||||||||||||

| Other general operating |

4,439 | 2,930 | 1,148 | 1,038 | 1,264 | 989 | 809 | |||||||||||||||

| Merger and restructuring charges |

618 | — | 272 | 221 | 125 | — | — | |||||||||||||||

| Total noninterest expense |

27,027 | 20,155 | 7,334 | 7,021 | 7,242 | 5,430 | 5,288 | |||||||||||||||

| Income before income taxes |

21,221 | 15,861 | 5,775 | 5,648 | 5,826 | 3,972 | 3,903 | |||||||||||||||

| Income tax expense |

7,078 | 5,051 | 1,926 | 1,884 | 1,977 | 1,291 | 1,177 | |||||||||||||||

| Net income |

$ | 14,143 | $ | 10,810 | $ | 3,849 | $ | 3,764 | $ | 3,849 | $ | 2,681 | $ | 2,726 | ||||||||

| Net income available to common shareholders |

$ | 14,127 | $ | 10,806 | $ | 3,844 | $ | 3,759 | $ | 3,844 | $ | 2,680 | $ | 2,725 | ||||||||

| Per common share information |

||||||||||||||||||||||

| Earnings |

$ | 3.76 | $ | 3.63 | $ | 0.95 | $ | 0.93 | $ | 0.95 | $ | 0.93 | $ | 0.93 | ||||||||

| Diluted earnings |

$ | 3.69 | $ | 3.57 | $ | 0.94 | $ | 0.91 | $ | 0.93 | $ | 0.91 | $ | 0.92 | ||||||||

| Dividends paid |

$ | 1.70 | $ | 1.44 | $ | 0.45 | $ | 0.45 | $ | 0.40 | $ | 0.40 | $ | 0.40 | ||||||||

| Average common shares issued and outstanding |

3,758,507 | 2,973,407 | 4,032,979 | 4,052,304 | 4,062,384 | 2,880,306 | 2,926,494 | |||||||||||||||

| Average diluted common shares issued and outstanding |

3,823,943 | 3,030,356 | 4,106,040 | 4,121,375 | 4,131,290 | 2,933,402 | 2,978,962 | |||||||||||||||

Certain prior period amounts have been reclassified to conform to current period presentation.

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

4

Bank of America Corporation

Consolidated Balance Sheet

| (Dollars in millions) |

December 31, 2004 |

September 30, 2004 |

December 31, 2003 |

|||||||||

| Assets |

||||||||||||

| Cash and cash equivalents |

$ | 28,936 | $ | 29,252 | $ | 27,084 | ||||||

| Time deposits placed and other short-term investments |

12,361 | 11,021 | 8,051 | |||||||||

| Federal funds sold and securities purchased under agreements to resell |

91,360 | 104,570 | 76,492 | |||||||||

| Trading account assets |

93,587 | 102,925 | 68,547 | |||||||||

| Derivative assets |

30,235 | 25,398 | 29,009 | |||||||||

| Securities: |

||||||||||||

| Available-for-sale |

194,743 | 163,438 | 66,382 | |||||||||

| Held-to-maturity, at cost |

330 | 420 | 247 | |||||||||

| Total securities |

195,073 | 163,858 | 66,629 | |||||||||

| Loans and leases |

521,837 | 511,639 | 371,463 | |||||||||

| Allowance for loan and lease losses |

(8,626 | ) | (8,723 | ) | (6,163 | ) | ||||||

| Loans and leases, net of allowance |

513,211 | 502,916 | 365,300 | |||||||||

| Premises and equipment, net |

7,517 | 7,884 | 6,036 | |||||||||

| Mortgage servicing rights |

2,482 | 2,453 | 2,762 | |||||||||

| Goodwill |

45,262 | 44,709 | 11,455 | |||||||||

| Core deposit intangibles and other intangibles |

3,887 | 3,726 | 908 | |||||||||

| Other assets |

86,546 | 74,117 | 57,210 | |||||||||

| Total assets |

$ | 1,110,457 | $ | 1,072,829 | $ | 719,483 | ||||||

| Liabilities |

||||||||||||

| Deposits in domestic offices: |

||||||||||||

| Noninterest-bearing |

$ | 163,833 | $ | 155,406 | $ | 118,495 | ||||||

| Interest-bearing |

396,645 | 380,956 | 262,032 | |||||||||

| Deposits in foreign offices: |

||||||||||||

| Noninterest-bearing |

6,066 | 5,632 | 3,035 | |||||||||

| Interest-bearing |

52,026 | 49,264 | 30,551 | |||||||||

| Total deposits |

618,570 | 591,258 | 414,113 | |||||||||

| Federal funds purchased and securities sold under agreements to repurchase |

119,741 | 142,992 | 78,046 | |||||||||

| Trading account liabilities |

36,654 | 36,825 | 26,844 | |||||||||

| Derivative liabilities |

17,928 | 12,721 | 15,062 | |||||||||

| Commercial paper and other short-term borrowings |

75,921 | 61,585 | 34,980 | |||||||||

| Accrued expenses and other liabilities (includes $402, $446 and $416 of Reserve for unfunded lending commitments) |

41,243 | 28,851 | 27,115 | |||||||||

| Long-term debt |

100,755 | 100,586 | 75,343 | |||||||||

| Total liabilities |

1,010,812 | 974,818 | 671,503 | |||||||||

| Shareholders’ equity |

||||||||||||

| Preferred stock, $0.01 par value; authorized - 100,000,000 shares; issued and outstanding - 1,090,189; 1,090,189 and 2,539,200 shares |

271 | 271 | 54 | |||||||||

| Common stock and additional paid-in capital, $0.01 par value; authorized - 7,500,000,000; 7,500,000,000 and 5,000,000,000 shares; issued and outstanding - 4,046,546,212; 4,049,062,685 and 2,882,287,572 shares |

44,236 | 44,756 | 29 | |||||||||

| Retained earnings |

58,006 | 55,979 | 50,198 | |||||||||

| Accumulated other comprehensive loss |

(2,587 | ) | (2,669 | ) | (2,148 | ) | ||||||

| Other |

(281 | ) | (326 | ) | (153 | ) | ||||||

| Total shareholders’ equity |

99,645 | 98,011 | 47,980 | |||||||||

| Total liabilities and shareholders’ equity |

$ | 1,110,457 | $ | 1,072,829 | $ | 719,483 | ||||||

Certain prior period amounts have been reclassified to conform to current period presentation.

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior period has not been restated.

5

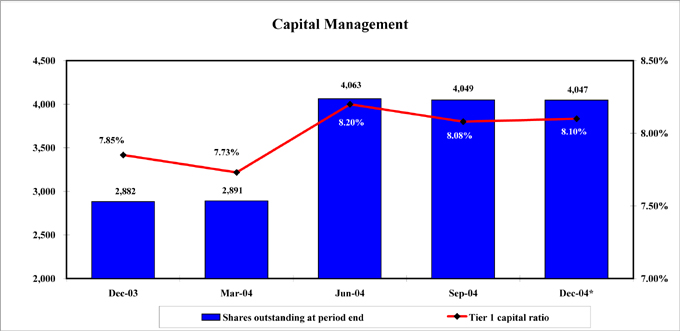

Bank of America Corporation

Capital Management

(Dollars in millions)

| 4Q04* |

3Q04 |

2Q04 |

1Q04 |

4Q03 |

||||||||||||||||

| Tier 1 capital |

$ | 64,281 | $ | 62,981 | $ | 61,883 | $ | 45,515 | $ | 44,050 | ||||||||||

| Total capital |

92,266 | 91,326 | 90,267 | 67,484 | 66,651 | |||||||||||||||

| Risk-weighted assets |

793,523 | 779,858 | 754,386 | 588,770 | 561,294 | |||||||||||||||

| Tier 1 capital ratio |

8.10 | % | 8.08 | % | 8.20 | % | 7.73 | % | 7.85 | % | ||||||||||

| Total capital ratio |

11.63 | 11.71 | 11.97 | 11.46 | 11.87 | |||||||||||||||

| Ending equity / ending assets |

8.97 | 9.14 | 9.35 | 6.10 | 6.67 | |||||||||||||||

| Ending capital / ending assets |

9.85 | 10.00 | 10.25 | 6.86 | 7.51 | |||||||||||||||

| Average equity / average assets |

8.51 | 8.79 | 8.52 | 5.84 | 6.32 | |||||||||||||||

| Leverage ratio |

5.82 | 5.92 | 5.83 | 5.43 | 5.73 | |||||||||||||||

*Preliminary data on risk-based capital

Share Repurchase Program

34.1 million common shares were repurchased in the fourth quarter of 2004 as a part of ongoing share repurchase programs.

80.6 million shares remain outstanding under the 2004 authorized program.

31.5 million shares were issued in the fourth quarter of 2004.

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

6

Bank of America Corporation

Quarterly Average Balances and Interest Rates - Fully Taxable-equivalent Basis

(Dollars in millions)

| Fourth Quarter 2004 |

Third Quarter 2004 |

Fourth Quarter 2003 |

|||||||||||||||||||||||||

| Average Balance |

Interest Income/ Expense |

Yield/ Rate |

Average Balance |

Interest Income/ Expense |

Yield/ Rate |

Average Balance |

Interest Income/ Expense |

Yield/ Rate |

|||||||||||||||||||

| Earning assets |

|||||||||||||||||||||||||||

| Time deposits placed and other short-term investments |

$ | 15,620 | $ | 128 | 3.24 | % | $ | 14,726 | $ | 127 | 3.45 | % | $ | 11,231 | $ | 49 | 1.71 | % | |||||||||

| Federal funds sold and securities purchased under agreements to resell |

149,226 | 712 | 1.90 | 128,339 | 484 | 1.50 | 96,713 | 506 | 2.08 | ||||||||||||||||||

| Trading account assets |

110,585 | 1,067 | 3.85 | 98,459 | 975 | 3.96 | 94,630 | 926 | 3.91 | ||||||||||||||||||

| Securities |

171,173 | 2,083 | 4.87 | 169,515 | 2,095 | 4.94 | 59,197 | 742 | 5.01 | ||||||||||||||||||

| Loans and leases(1): |

|||||||||||||||||||||||||||

| Residential mortgage |

178,879 | 2,459 | 5.49 | 175,046 | 2,371 | 5.41 | 142,482 | 1,931 | 5.41 | ||||||||||||||||||

| Home equity lines |

48,336 | 609 | 5.01 | 44,309 | 514 | 4.62 | 23,206 | 255 | 4.36 | ||||||||||||||||||

| Direct/Indirect consumer |

39,526 | 551 | 5.55 | 38,951 | 538 | 5.49 | 33,422 | 478 | 5.67 | ||||||||||||||||||

| Credit card |

49,366 | 1,351 | 10.88 | 45,818 | 1,265 | 10.98 | 32,734 | 810 | 9.83 | ||||||||||||||||||

| Other consumer(2) |

7,557 | 153 | 8.07 | 7,693 | 152 | 7.91 | 7,737 | 124 | 6.37 | ||||||||||||||||||

| Total consumer |

323,664 | 5,123 | 6.31 | 311,817 | 4,840 | 6.19 | 239,581 | 3,598 | 5.98 | ||||||||||||||||||

| Commercial - domestic |

121,412 | 1,917 | 6.28 | 122,093 | 1,855 | 6.04 | 90,309 | 1,612 | 7.08 | ||||||||||||||||||

| Commercial - foreign |

18,828 | 272 | 5.76 | 18,251 | 245 | 5.34 | 11,594 | 101 | 3.45 | ||||||||||||||||||

| Commercial real estate |

31,355 | 392 | 4.98 | 30,792 | 344 | 4.44 | 19,616 | 211 | 4.27 | ||||||||||||||||||

| Commercial lease financing |

20,204 | 254 | 5.01 | 20,125 | 233 | 4.64 | 9,971 | 93 | 3.71 | ||||||||||||||||||

| Total commercial |

191,799 | 2,835 | 5.88 | 191,261 | 2,677 | 5.57 | 131,490 | 2,017 | 6.09 | ||||||||||||||||||

| Total loans and leases |

515,463 | 7,958 | 6.15 | 503,078 | 7,517 | 5.95 | 371,071 | 5,615 | 6.02 | ||||||||||||||||||

| Other earning assets |

35,937 | 456 | 5.08 | 34,266 | 460 | 5.33 | 33,938 | 369 | 4.32 | ||||||||||||||||||

| Total earning |

998,004 | 12,404 | 4.96 | 948,383 | 11,658 | 4.90 | 666,780 | 8,207 | 4.90 | ||||||||||||||||||

| Cash and cash equivalents |

31,028 | 29,469 | 22,975 | ||||||||||||||||||||||||

| Other assets, less allowance for loan and lease losses |

123,519 | 118,831 | 74,431 | ||||||||||||||||||||||||

| Total assets |

$ | 1,152,551 | $ | 1,096,683 | $ | 764,186 | |||||||||||||||||||||

| Interest-bearing liabilities |

|||||||||||||||||||||||||||

| Domestic interest-bearing deposits: |

|||||||||||||||||||||||||||

| Savings |

$ | 36,927 | $ | 36 | 0.39 | % | $ | 36,823 | $ | 35 | 0.38 | % | $ | 25,494 | $ | 19 | 0.30 | % | |||||||||

| NOW and money market deposit accounts |

234,596 | 589 | 1.00 | 233,602 | 523 | 0.89 | 155,369 | 400 | 1.02 | ||||||||||||||||||

| Consumer CDs and IRAs |

109,243 | 711 | 2.59 | 101,250 | 668 | 2.63 | 73,246 | 476 | 2.58 | ||||||||||||||||||

| Negotiable CDs, public funds and other time deposits |

7,563 | 81 | 4.27 | 5,654 | 69 | 4.85 | 6,195 | 44 | 2.81 | ||||||||||||||||||

| Total domestic interest-bearing deposits |

388,329 | 1,417 | 1.45 | 377,329 | 1,295 | 1.37 | 260,304 | 939 | 1.43 | ||||||||||||||||||

| Foreign interest-bearing deposits(4): |

|||||||||||||||||||||||||||

| Banks located in foreign countries |

17,953 | 275 | 6.11 | 17,864 | 307 | 6.83 | 13,225 | 177 | 5.34 | ||||||||||||||||||

| Governments and official institutions |

5,843 | 33 | 2.21 | 5,021 | 22 | 1.80 | 2,654 | 11 | 1.58 | ||||||||||||||||||

| Time, savings and other |

30,459 | 104 | 1.36 | 29,513 | 87 | 1.17 | 20,019 | 51 | 1.02 | ||||||||||||||||||

| Total foreign interest-bearing deposits |

54,255 | 412 | 3.02 | 52,398 | 416 | 3.16 | 35,898 | 239 | 2.65 | ||||||||||||||||||

| Total interest-bearing deposits |

442,584 | 1,829 | 1.64 | 429,727 | 1,711 | 1.58 | 296,202 | 1,178 | 1.58 | ||||||||||||||||||

| Federal funds purchased, securities sold under agreements to repurchase and other short-term borrowings |

252,384 | 1,543 | 2.43 | 226,025 | 1,152 | 2.03 | 144,082 | 517 | 1.42 | ||||||||||||||||||

| Trading account liabilities |

37,387 | 352 | 3.74 | 37,706 | 333 | 3.51 | 38,298 | 317 | 3.28 | ||||||||||||||||||

| Long-term debt |

99,588 | 724 | 2.91 | 98,361 | 626 | 2.54 | 70,596 | 450 | 2.55 | ||||||||||||||||||

| Total interest-bearing liabilities(3) |

831,943 | 4,448 | 2.13 | 791,819 | 3,822 | 1.92 | 549,178 | 2,462 | 1.78 | ||||||||||||||||||

| Noninterest-bearing sources: |

|||||||||||||||||||||||||||

| Noninterest-bearing deposits |

167,352 | 158,151 | 122,638 | ||||||||||||||||||||||||

| Other liabilities |

55,156 | 50,321 | 44,077 | ||||||||||||||||||||||||

| Shareholders’ equity |

98,100 | 96,392 | 48,293 | ||||||||||||||||||||||||

| Total liabilities and shareholders’ equity |

$ | 1,152,551 | $ | 1,096,683 | $ | 764,186 | |||||||||||||||||||||

| Net interest spread |

2.83 | 2.98 | 3.12 | ||||||||||||||||||||||||

| Impact of noninterest-bearing sources |

0.35 | 0.32 | 0.31 | ||||||||||||||||||||||||

| Net interest income/yield on earning assets |

$ | 7,956 | 3.18 | % | $ | 7,836 | 3.30 | % | $ | 5,745 | 3.43 | % | |||||||||||||||

| (1) | Nonperforming loans are included in the respective average loan balances. Income on such nonperforming loans is recognized on a cash basis. |

| (2) | Includes consumer finance of $3,473 and $3,644 in the fourth and third quarters of 2004, and $3,938 in the fourth quarter of 2003, respectively; foreign consumer of $3,523 and $3,304 in the fourth and third quarters of 2004, and $1,939 in the fourth quarter of 2003, respectively; and consumer lease financing of $561 and $745 in the fourth and third quarters of 2004, and $1,860 in the fourth quarter of 2003, respectively. |

| (3) | Interest income includes the impact of interest rate risk management contracts, which increased interest income on the underlying assets $496 and $531 in the fourth and third quarters of 2004, respectively, and $884 in the fourth quarter of 2003. These amounts were substantially offset by corresponding decreases in the income earned on the underlying assets. Interest expense includes the impact of interest rate risk management contracts, which increased interest expense on the underlying liabilities $156 and $217 in the fourth and third quarters of 2004, respectively, and $90 in the fourth quarter of 2003. These amounts were substantially offset by corresponding decreases in the interest paid on the underlying liabilities. |

| (4) | Primarily consists of time deposits in denominations of $100,000 or more. |

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

7

Bank of America Corporation

Year-to-Date Average Balances and Interest Rates - Fully Taxable-equivalent Basis

(Dollars in millions)

| Year Ended December 31 |

||||||||||||||||||

| 2004 |

2003 |

|||||||||||||||||

| Average Balance |

Interest Income/ Expense |

Yield/ Rate |

Average Balance |

Interest Income/ Expense |

Yield/ Rate |

|||||||||||||

| Earning assets |

||||||||||||||||||

| Time deposits placed and other short-term investments |

$ | 14,254 | $ | 362 | 2.54 | % | $ | 9,056 | $ | 172 | 1.90 | % | ||||||

| Federal funds sold and securities purchased under agreements to resell |

128,981 | 2,043 | 1.58 | 78,857 | 1,373 | 1.74 | ||||||||||||

| Trading account assets |

104,616 | 4,092 | 3.91 | 97,222 | 4,005 | 4.12 | ||||||||||||

| Securities |

150,171 | 7,326 | 4.88 | 70,666 | 3,131 | 4.43 | ||||||||||||

| Loans and leases(1): |

||||||||||||||||||

| Residential mortgage |

167,298 | 9,074 | 5.42 | 127,059 | 6,872 | 5.41 | ||||||||||||

| Home equity lines |

39,400 | 1,835 | 4.66 | 22,890 | 1,040 | 4.55 | ||||||||||||

| Direct/Indirect consumer |

38,078 | 2,093 | 5.50 | 32,593 | 1,964 | 6.03 | ||||||||||||

| Credit card |

43,435 | 4,653 | 10.71 | 28,210 | 2,886 | 10.23 | ||||||||||||

| Other consumer(2) |

7,717 | 594 | 7.70 | 8,865 | 588 | 6.63 | ||||||||||||

| Total consumer |

295,928 | 18,249 | 6.17 | 219,617 | 13,350 | 6.08 | ||||||||||||

| Commercial - domestic |

114,644 | 7,126 | 6.22 | 93,458 | 6,729 | 7.20 | ||||||||||||

| Commercial - foreign |

16,505 | 849 | 5.15 | 12,970 | 460 | 3.54 | ||||||||||||

| Commercial real estate |

28,085 | 1,263 | 4.50 | 20,042 | 862 | 4.30 | ||||||||||||

| Commercial lease financing |

17,483 | 819 | 4.68 | 10,061 | 395 | 3.92 | ||||||||||||

| Total commercial |

176,717 | 10,057 | 5.69 | 136,531 | 8,446 | 6.19 | ||||||||||||

| Total loans and leases |

472,645 | 28,306 | 5.99 | 356,148 | 21,796 | 6.12 | ||||||||||||

| Other earning assets |

34,635 | 1,814 | 5.24 | 37,599 | 1,729 | 4.60 | ||||||||||||

| Total earning assets(3) |

905,302 | 43,943 | 4.85 | 649,548 | 32,206 | 4.96 | ||||||||||||

| Cash and cash equivalents |

28,511 | 22,637 | ||||||||||||||||

| Other assets, less allowance for loan and lease losses |

110,847 | 76,871 | ||||||||||||||||

| Total assets |

$ | 1,044,660 | $ | 749,056 | ||||||||||||||

| Interest-bearing liabilities |

||||||||||||||||||

| Domestic interest-bearing deposits: |

||||||||||||||||||

| Savings |

$ | 33,959 | $ | 119 | 0.35 | % | $ | 24,538 | $ | 108 | 0.44 | % | ||||||

| NOW and money market deposit accounts |

214,542 | 1,921 | 0.90 | 148,896 | 1,236 | 0.83 | ||||||||||||

| Consumer CDs and IRAs |

94,770 | 2,533 | 2.67 | 70,246 | 2,784 | 3.96 | ||||||||||||

| Negotiable CDs, public funds and other time deposits |

5,977 | 290 | 4.85 | 7,627 | 130 | 1.70 | ||||||||||||

| Total domestic interest-bearing deposits |

349,248 | 4,863 | 1.39 | 251,307 | 4,258 | 1.69 | ||||||||||||

| Foreign interest-bearing deposits(4): |

||||||||||||||||||

| Banks located in foreign countries |

18,426 | 1,040 | 5.64 | 13,959 | 403 | 2.89 | ||||||||||||

| Governments and official institutions |

5,327 | 97 | 1.82 | 2,218 | 31 | 1.40 | ||||||||||||

| Time, savings and other |

27,739 | 275 | 0.99 | 19,027 | 216 | 1.14 | ||||||||||||

| Total foreign interest-bearing deposits |

51,492 | 1,412 | 2.74 | 35,204 | 650 | 1.85 | ||||||||||||

| Total interest-bearing deposits |

400,740 | 6,275 | 1.57 | 286,511 | 4,908 | 1.71 | ||||||||||||

| Federal funds purchased, securities sold under agreements to repurchase and other short-term borrowings |

227,558 | 4,434 | 1.95 | 140,458 | 1,871 | 1.33 | ||||||||||||

| Trading account liabilities |

35,326 | 1,317 | 3.73 | 37,176 | 1,286 | 3.46 | ||||||||||||

| Long-term debt |

93,330 | 2,404 | 2.58 | 68,432 | 2,034 | 2.97 | ||||||||||||

| Total interest-bearing liabilities(3) |

756,954 | 14,430 | 1.91 | 532,577 | 10,099 | 1.90 | ||||||||||||

| Noninterest-bearing sources: |

||||||||||||||||||

| Noninterest-bearing deposits |

150,819 | 119,722 | ||||||||||||||||

| Other liabilities |

52,704 | 47,553 | ||||||||||||||||

| Shareholders’ equity |

84,183 | 49,204 | ||||||||||||||||

| Total liabilities and shareholders’ equity |

$ | 1,044,660 | $ | 749,056 | ||||||||||||||

| Net interest spread |

2.94 | 3.06 | ||||||||||||||||

| Impact of noninterest-bearing sources |

0.32 | 0.34 | ||||||||||||||||

| Net interest income/yield on earning assets |

$ | 29,513 | 3.26 | % | $ | 22,107 | 3.40 | % | ||||||||||

| (1) | Nonperforming loans are included in the respective average loan balances. Income on such nonperforming loans is recognized on a cash basis. |

| (2) | Includes consumer finance, foreign consumer and consumer lease financing of $3,735, $3,020 and $962 for the year ended December 31, 2004, respectively, and $4,137, $1,977 and $2,751 for the year ended December 31, 2003, respectively. |

| (3) | Interest income includes the impact of interest rate risk management contracts, which increased interest income on the underlying assets $2,400 and $2,972 in the years ended December 31, 2004 and 2003, respectively. These amounts were substantially offset by corresponding decreases in the income earned on the underlying assets. Interest expense includes the impact of interest rate risk management contracts, which increased interest expense on the underlying liabilities $888 and $305 in the years ended December 31, 2004 and 2003, respectively. These amounts were substantially offset by corresponding decreases in the interest paid on the underlying liabilities. |

| (4) | Primarily consists of time deposits in denominations of $100,000 or more. |

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

8

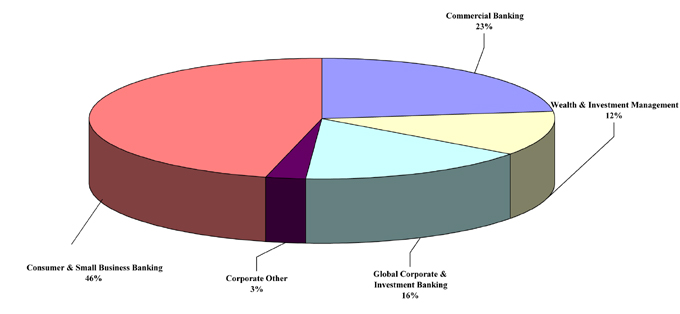

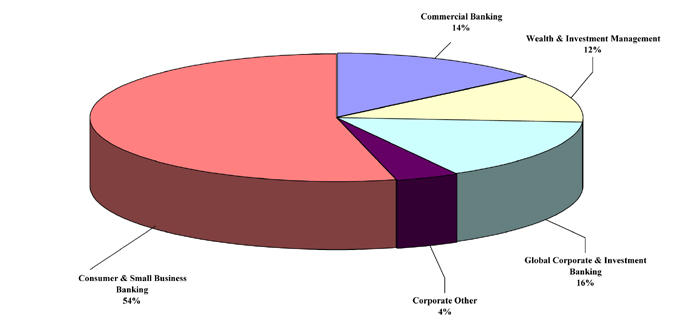

Bank of America Corporation

Business Segment View

Net Income

Fourth Quarter 2004

Revenue

Fourth Quarter 2004

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

9

Bank of America Corporation

Consumer and Small Business Banking Segment Results(1)

(Dollars in millions)

| Year-to-Date |

Quarterly |

|||||||||||||||||||||||||||

| 2004 |

2003 |

4 Qtr 04 |

3 Qtr 04 |

2 Qtr 04 |

1 Qtr 04 |

4 Qtr 03 |

||||||||||||||||||||||

| Key Measures |

||||||||||||||||||||||||||||

| Total revenue(2) |

$ | 26,857 | $ | 20,930 | $ | 7,589 | $ | 7,025 | $ | 7,153 | $ | 5,090 | $ | 5,344 | ||||||||||||||

| Provision for credit losses |

3,341 | 1,678 | 1,243 | 1,000 | 662 | 436 | 448 | |||||||||||||||||||||

| Net income |

6,548 | 5,706 | 1,763 | 1,683 | 1,889 | 1,213 | 1,431 | |||||||||||||||||||||

| Shareholder value added |

3,390 | 4,367 | 802 | 753 | 1,016 | 819 | 1,048 | |||||||||||||||||||||

| Return on average equity |

19.89 | % | 42.25 | % | 17.46 | % | 17.34 | % | 20.52 | % | 30.98 | % | 37.49 | % | ||||||||||||||

| Efficiency ratio(2) |

49.64 | 49.37 | 47.37 | 49.85 | 49.03 | 53.62 | 50.55 | |||||||||||||||||||||

| Selected Average Balance Sheet Components |

||||||||||||||||||||||||||||

| Total loans and leases |

$ | 137,357 | $ | 92,776 | $ | 154,506 | $ | 150,334 | $ | 145,862 | $ | 98,395 | $ | 95,408 | ||||||||||||||

| Total deposits |

314,652 | 240,371 | 336,593 | 339,565 | 339,575 | 242,359 | 248,156 | |||||||||||||||||||||

| Total earning assets |

323,426 | 243,175 | 347,986 | 349,708 | 347,677 | 247,776 | 253,135 | |||||||||||||||||||||

| Period End (in billions) |

||||||||||||||||||||||||||||

| Mortgage servicing portfolio |

$ | 259.1 | $ | 246.5 | $ | 259.1 | $ | 254.2 | $ | 253.3 | $ | 247.6 | $ | 246.5 | ||||||||||||||

| Mortgage originations: |

||||||||||||||||||||||||||||

| Retail |

57.6 | 91.8 | 12.7 | 11.7 | 19.2 | 14.0 | 11.7 | |||||||||||||||||||||

| Wholesale |

30.0 | 39.3 | 5.7 | 5.2 | 9.3 | 9.8 | 6.7 | |||||||||||||||||||||

| (1) | Consumer and Small Business major subsegments are Consumer Banking, Consumer Products and Small Business Banking. |

| (2) | Fully taxable-equivalent basis |

Certain prior period amounts have been reclassified among the segments to conform to the current period presentation.

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

10

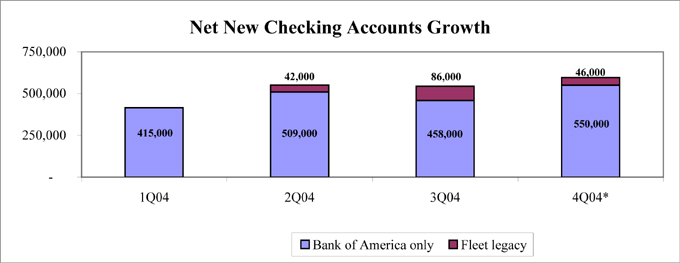

Bank of America Corporation

Consumer Channel

| * | preliminary data |

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

11

Bank of America Corporation

E-Commerce & BankofAmerica.com

Bank of America has the largest active online banking customer base with 12.4 million subscribers. This represents an active customer penetration rate of 49.7%.

Bank of America uses a strict Active User standard - customers must have used our online services within the last 90 days.

5.8 million active bill pay users paid $25.1 billion worth of bills this quarter. The number of customers who sign up and use Bank of America’s Bill Pay Service continues to far surpass that of any other financial institution.

Currently, approximately 300 companies are presenting 12.6 million e-bills per quarter.

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

12

Bank of America Corporation

Card Services Results(1)

(Dollars in millions)

| Year-to-Date |

Quarterly |

|||||||||||||||||||||||||||

| 2004 |

2003 |

4 Qtr 04 |

3 Qtr 04 |

2 Qtr 04 |

1 Qtr 04 |

4 Qtr 03 |

||||||||||||||||||||||

| Key Measures |

||||||||||||||||||||||||||||

| Consumer Credit Card Outstandings: |

||||||||||||||||||||||||||||

| On-balance sheet (Period end) |

$ | 51,726 | $ | 34,814 | $ | 51,726 | $ | 47,521 | $ | 42,195 | $ | 36,087 | $ | 34,814 | ||||||||||||||

| Managed (Period end) |

58,629 | 36,596 | 58,629 | 55,399 | 51,990 | 37,296 | 36,596 | |||||||||||||||||||||

| On-balance sheet (Average) |

43,435 | 28,210 | 49,366 | 45,589 | 43,177 | 35,303 | 32,734 | |||||||||||||||||||||

| Managed (Average) |

50,295 | 31,552 | 56,444 | 54,419 | 53,136 | 36,855 | 34,783 | |||||||||||||||||||||

| Managed Income Statement: |

||||||||||||||||||||||||||||

| Total revenue |

$ | 8,140 | $ | 4,786 | $ | 2,354 | $ | 2,267 | $ | 2,173 | $ | 1,346 | $ | 1,342 | ||||||||||||||

| Provision for credit losses |

3,555 | 1,977 | 1,335 | 994 | 760 | 466 | 555 | |||||||||||||||||||||

| Noninterest expense |

2,172 | 1,369 | 700 | 544 | 546 | 382 | 379 | |||||||||||||||||||||

| Income before income taxes |

$ | 2,413 | $ | 1,440 | $ | 319 | $ | 729 | $ | 867 | $ | 498 | $ | 408 | ||||||||||||||

| Shareholder Value Added |

$ | 1,137 | $ | 660 | $ | 89 | $ | 403 | $ | 407 | $ | 238 | $ | 192 | ||||||||||||||

| Merchant Acquiring Business: |

||||||||||||||||||||||||||||

| Processing volume (millions) |

145,093 | 79,686 | 75,383 | 24,898 | 23,239 | 21,573 | 21,150 | |||||||||||||||||||||

| Total transactions (millions) |

2,781 | 1,183 | 1,756 | 374 | 342 | 309 | 312 | |||||||||||||||||||||

| Consumer Credit Card Credit Quality: |

||||||||||||||||||||||||||||

| On-balance sheet: |

||||||||||||||||||||||||||||

| Charge-offs $ |

$ | 2,305 | $ | 1,514 | $ | 691 | $ | 586 | $ | 585 | $ | 443 | $ | 423 | ||||||||||||||

| Charge-offs % |

5.31 | % | 5.37 | % | 5.57 | % | 5.09 | % | 5.45 | % | 5.05 | % | 5.12 | % | ||||||||||||||

| Managed: |

||||||||||||||||||||||||||||

| Losses $ |

$ | 2,829 | $ | 1,691 | $ | 837 | $ | 753 | $ | 776 | $ | 463 | $ | 451 | ||||||||||||||

| Losses % |

5.63 | % | 5.36 | % | 5.90 | % | 5.48 | % | 5.88 | % | 5.05 | % | 5.14 | % | ||||||||||||||

| Managed delinquency %: (2) |

||||||||||||||||||||||||||||

| 30+ |

n/a | n/a | 4.37 | % | 4.30 | % | 3.86 | % | 3.75 | % | 3.93 | % | ||||||||||||||||

| 90+ |

n/a | n/a | 2.13 | 1.98 | 1.76 | 1.81 | 1.77 | |||||||||||||||||||||

n/a = not applicable

| (1) | Card Services includes Consumer and Small Business Credit Card and Merchant Services. |

| (2) | 3Q04 has been adjusted for an understatement related to an available-for-sale portfolio acquired with the Fleet acquisition. |

Represents financial statement presentation with certain reclassifications to reflect securitization activity.

Certain prior period amounts have been reclassified among the segments to conform to the current period classification.

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

13

Bank of America Corporation

Commercial Banking Segment Results(1)

(Dollars in millions)

| Year-to-Date |

Quarterly |

|||||||||||||||||||||||||||

| 2004 |

2003 |

4 Qtr 04 |

3 Qtr 04 |

2 Qtr 04 |

1 Qtr 04 |

4 Qtr 03 |

||||||||||||||||||||||

| Key Measures |

||||||||||||||||||||||||||||

| Total revenue(2) |

$ | 6,722 | $ | 4,517 | $ | 1,946 | $ | 1,824 | $ | 1,748 | $ | 1,204 | $ | 1,201 | ||||||||||||||

| Provision for credit losses |

(241 | ) | 458 | (188 | ) | (60 | ) | (20 | ) | 27 | 98 | |||||||||||||||||

| Net income |

2,833 | 1,471 | 887 | 824 | 657 | 465 | 410 | |||||||||||||||||||||

| Shareholder value added |

884 | 846 | 282 | 221 | 74 | 307 | 252 | |||||||||||||||||||||

| Return on average equity |

15.34 | % | 25.01 | % | 15.47 | % | 14.40 | % | 11.86 | % | 31.41 | % | 27.68 | % | ||||||||||||||

| Efficiency ratio(2) |

36.84 | 39.75 | 34.47 | 34.20 | 41.39 | 38.05 | 40.09 | |||||||||||||||||||||

| Selected Average Balance Sheet Components |

||||||||||||||||||||||||||||

| Total loans and leases |

$ | 129,671 | $ | 93,378 | $ | 142,610 | $ | 140,083 | $ | 139,156 | $ | 96,577 | $ | 94,996 | ||||||||||||||

| Total deposits |

53,088 | 31,461 | 59,549 | 58,175 | 59,866 | 34,636 | 34,053 | |||||||||||||||||||||

| Total earning assets |

135,098 | 97,888 | 148,904 | 145,806 | 144,706 | 100,709 | 99,734 | |||||||||||||||||||||

| (1) | Commercial Banking major subsegments are Middle Market Banking, Commercial Real Estate Banking, Dealer Financial Services, Business Capital and Leasing. |

| (2) | Fully taxable-equivalent basis |

Certain prior period amounts have been reclassified among the segments to conform to the current period presentation.

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

14

Bank of America Corporation

Global Corporate and Investment Banking Segment Results(1)

(Dollars in millions)

| Year-to-Date |

Quarterly |

|||||||||||||||||||||||||||

| 2004 |

2003 |

4 Qtr 04 |

3 Qtr 04 |

2 Qtr 04 |

1 Qtr 04 |

4 Qtr 03 |

||||||||||||||||||||||

| Key Measures |

||||||||||||||||||||||||||||

| Total revenue(2) |

$ | 9,049 | $ | 8,334 | $ | 2,203 | $ | 2,062 | $ | 2,621 | $ | 2,163 | $ | 1,935 | ||||||||||||||

| Provision for credit losses |

(459 | ) | 303 | (207 | ) | (158 | ) | 5 | (99 | ) | (83 | ) | ||||||||||||||||

| Net income |

1,950 | 1,794 | 596 | 475 | 415 | 464 | 512 | |||||||||||||||||||||

| Shareholder value added |

891 | 893 | 308 | 186 | 132 | 265 | 305 | |||||||||||||||||||||

| Return on average equity |

19.46 | % | 21.35 | % | 21.81 | % | 17.34 | % | 15.43 | % | 24.91 | % | 26.38 | % | ||||||||||||||

| Efficiency ratio(2) |

72.45 | 63.91 | 69.43 | 72.95 | 75.87 | 70.92 | 65.62 | |||||||||||||||||||||

| Selected Average Balance Sheet Components |

||||||||||||||||||||||||||||

| Total loans and leases |

$ | 34,237 | $ | 36,640 | $ | 34,246 | $ | 35,781 | $ | 37,985 | $ | 28,917 | $ | 31,034 | ||||||||||||||

| Total deposits |

76,884 | 66,095 | 83,354 | 74,345 | 80,692 | 69,101 | 62,997 | |||||||||||||||||||||

| Total earning assets |

276,768 | 230,773 | 307,147 | 271,279 | 275,531 | 261,711 | 242,062 | |||||||||||||||||||||

| (1) | Global Corporate and Investment Banking offers clients a comprehensive range of global capabilities through three subsegments: Global Investment Banking, Global Credit Products and Global Treasury Services. |

| (2) | Fully taxable-equivalent basis |

Certain prior period amounts have been reclassified among the segments to conform to the current period presentation.

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

15

Bank of America Corporation

Global Corporate and Investment Banking

(Dollars in millions)

| Year-to-Date |

Quarterly |

|||||||||||||||||||||||||||

| 2004 |

2003 |

4 Qtr 04 |

3 Qtr 04 |

2 Qtr 04 |

1 Qtr 04 |

4 Qtr 03 |

||||||||||||||||||||||

| Trading-related Revenue |

||||||||||||||||||||||||||||

| Net interest income(1) |

$ | 2,039 | $ | 2,239 | $ | 417 | $ | 448 | $ | 597 | $ | 577 | $ | 523 | ||||||||||||||

| Trading account profits |

1,028 | 587 | 233 | 137 | 390 | 268 | 27 | |||||||||||||||||||||

| Total trading-related revenue |

$ | 3,067 | $ | 2,826 | $ | 650 | $ | 585 | $ | 987 | $ | 845 | $ | 550 | ||||||||||||||

| Trading-related revenue by product |

||||||||||||||||||||||||||||

| Fixed income |

$ | 1,547 | $ | 1,352 | $ | 283 | $ | 299 | $ | 456 | $ | 509 | $ | 228 | ||||||||||||||

| Interest rate(1) |

667 | 954 | 93 | 118 | 289 | 167 | 166 | |||||||||||||||||||||

| Foreign exchange |

757 | 551 | 233 | 164 | 171 | 189 | 155 | |||||||||||||||||||||

| Equities(2) |

195 | 344 | 75 | 40 | 83 | (3 | ) | 61 | ||||||||||||||||||||

| Commodities |

45 | (45 | ) | 33 | 18 | (4 | ) | (2 | ) | 2 | ||||||||||||||||||

| Market-based trading-related revenue |

3,211 | 3,156 | 717 | 639 | 995 | 860 | 612 | |||||||||||||||||||||

| Credit portfolio hedges(3) |

(144 | ) | (330 | ) | (67 | ) | (54 | ) | (8 | ) | (15 | ) | (62 | ) | ||||||||||||||

| Total trading-related revenue |

$ | 3,067 | $ | 2,826 | $ | 650 | $ | 585 | $ | 987 | $ | 845 | $ | 550 | ||||||||||||||

| Year-to-Date |

Quarterly |

|||||||||||||||||||||||||||

| 2004 |

2003 |

4 Qtr 04 |

3 Qtr 04 |

2 Qtr 04 |

1 Qtr 04 |

4 Qtr 03 |

||||||||||||||||||||||

| Investment Banking Income |

||||||||||||||||||||||||||||

| Securities underwriting |

$ | 920 | $ | 962 | $ | 209 | $ | 219 | $ | 275 | $ | 217 | $ | 232 | ||||||||||||||

| Syndications |

521 | 407 | 140 | 128 | 174 | 79 | 106 | |||||||||||||||||||||

| Advisory services |

310 | 229 | 94 | 66 | 73 | 77 | 76 | |||||||||||||||||||||

| Other |

32 | 38 | 7 | 7 | 10 | 8 | 12 | |||||||||||||||||||||

| Total investment banking income |

$ | 1,783 | $ | 1,636 | $ | 450 | $ | 420 | $ | 532 | $ | 381 | $ | 426 | ||||||||||||||

| (1) | Fully taxable-equivalent basis |

| (2) | Does not include commissions from equity transactions which where were $666 and $648 for the year ended December 31, 2004 and 2003, respectively and $173, $153, $168, $172 and $167 for the three months ended December 31, 2004, September 30, 2004, June 30, 2004, March 31, 2004 and December 31, 2003. |

| (3) | Includes credit default swaps used for credit risk management. |

Certain prior period amounts have been reclassified among the segments to conform to the current period presentation.

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

16

Bank of America Corporation

Global Corporate & Investment Banking Strategic Progress Continues

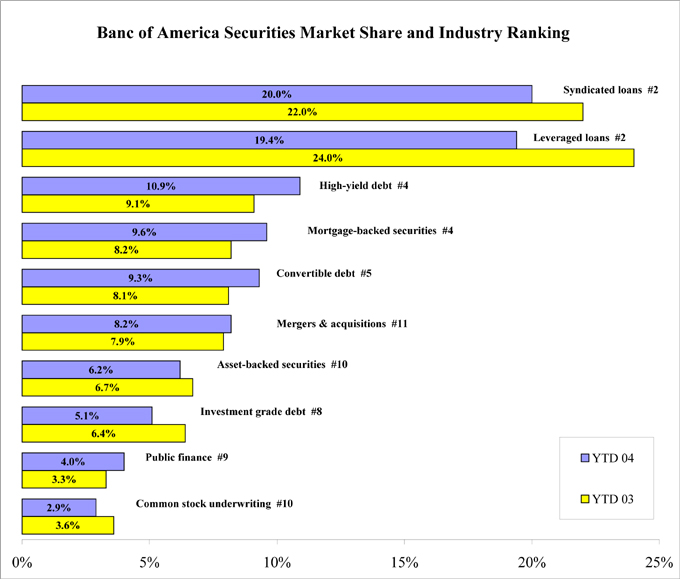

Source: Thomson Financial except Syndicated Loans from Loan Pricing Corporation.

Significant US market share gains

Banc of America Securities increased market share in high yield, mortgage-backed securities, convertible debt and public finance.

| • | #2 in leveraged loans, ranked by dollar volume, with 19.4% market share |

| • | #1 in leveraged loans, ranked by number of deals |

| • | #2 syndicated lender, ranked by dollar volume, with 20.0% market share |

| • | #1 syndicated lender, ranked by number of deals |

| • | High yield debt market share increased over YTD03, from 9.1% to 10.9% |

17

Bank of America Corporation

Wealth and Investment Management Segment Results(1)

(Dollars in millions)

| Year-to-Date |

Quarterly |

|||||||||||||||||||||||||||

| 2004 |

2003 |

4 Qtr 04 |

3 Qtr 04 |

2 Qtr 04 |

1 Qtr 04 |

4 Qtr 03 |

||||||||||||||||||||||

| Key Measures |

||||||||||||||||||||||||||||

| Total revenue(2) |

$ | 5,918 | $ | 4,030 | $ | 1,676 | $ | 1,601 | $ | 1,540 | $ | 1,101 | $ | 1,203 | ||||||||||||||

| Provision for credit losses |

(20 | ) | 11 | (3 | ) | (18 | ) | 10 | (9 | ) | 7 | |||||||||||||||||

| Net income |

1,584 | 1,234 | 477 | 469 | 392 | 246 | 428 | |||||||||||||||||||||

| Shareholder value added |

782 | 854 | 239 | 246 | 172 | 125 | 313 | |||||||||||||||||||||

| Return on average equity |

20.17 | % | 33.94 | % | 20.39 | % | 21.27 | % | 18.01 | % | 21.71 | % | 39.08 | % | ||||||||||||||

| Efficiency ratio(2) |

58.28 | 52.11 | 55.72 | 54.95 | 59.42 | 65.45 | 44.83 | |||||||||||||||||||||

| Selected Average Balance Sheet Components |

||||||||||||||||||||||||||||

| Total loans and leases |

$ | 44,049 | $ | 37,675 | $ | 47,948 | $ | 45,646 | $ | 44,109 | $ | 38,434 | $ | 37,660 | ||||||||||||||

| Total deposits |

83,049 | 53,996 | 102,488 | 87,904 | 77,069 | 64,467 | 59,784 | |||||||||||||||||||||

| Total earning assets |

85,277 | 55,385 | 104,925 | 90,146 | 79,296 | 66,470 | 62,073 | |||||||||||||||||||||

| Period End (in billions) |

||||||||||||||||||||||||||||

| Assets under management |

$ | 451.5 | $ | 296.7 | $ | 451.5 | $ | 429.5 | $ | 439.6 | $ | 298.7 | $ | 296.7 | ||||||||||||||

| Client brokerage assets |

149.9 | 88.8 | 149.9 | 141.9 | 144.9 | 91.0 | 88.8 | |||||||||||||||||||||

| Assets in custody |

107.0 | 49.9 | 107.0 | 104.0 | 105.2 | 50.6 | 49.9 | |||||||||||||||||||||

| Total client assets |

$ | 708.4 | $ | 435.4 | $ | 708.4 | $ | 675.4 | $ | 689.7 | $ | 440.3 | $ | 435.4 | ||||||||||||||

| (1) | Wealth and Investment Management includes five primary subsegments: Columbia Management Group, The Private Bank, Banc of America Investments, Premier Banking and Other Services. |

| (2) | Fully taxable-equivalent basis |

Certain prior period amounts have been reclassified among the segments to conform to the current period presentation.

Information for period after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

18

Bank of America Corporation

Corporate Other Results(1)

(Dollars in millions)

| Year-to-Date |

Quarterly |

|||||||||||||||||||||||||

| 2004 |

2003 |

4 Qtr 04 |

3 Qtr 04 |

2 Qtr 04 |

1 Qtr 04 |

4 Qtr 03 |

||||||||||||||||||||

| Key Measures |

||||||||||||||||||||||||||

| Total revenue(2) |

$ | 1,064 | $ | 746 | $ | 506 | $ | 246 | $ | 170 | $ | 142 | $ | 111 | ||||||||||||

| Provision for credit losses |

148 | 389 | (139 | ) | (114 | ) | 132 | 269 | 113 | |||||||||||||||||

| Net income(3) |

1,228 | 605 | 126 | 313 | 496 | 293 | (55 | ) | ||||||||||||||||||

| Shareholder value added |

36 | (1,339 | ) | (97 | ) | 47 | 197 | (111 | ) | (475 | ) | |||||||||||||||

| Selected Average Balance Sheet Components |

||||||||||||||||||||||||||

| Total loans and leases |

$ | 127,331 | $ | 95,679 | $ | 136,153 | $ | 131,234 | $ | 130,046 | $ | 111,753 | $ | 111,973 | ||||||||||||

| Total deposits |

23,886 | 14,310 | 27,952 | 27,889 | 25,105 | 14,512 | 13,850 | |||||||||||||||||||

| Total earning assets |

84,733 | 22,327 | 89,042 | 91,444 | 91,310 | 58,142 | 9,776 | |||||||||||||||||||

Corporate Other Sub-Segment Results

| Year-to-Date |

Quarterly |

|||||||||||||||||||||||||||

| 2004 |

2003 |

4 Qtr 04 |

3 Qtr 04 |

2 Qtr 04 |

1 Qtr 04 |

4 Qtr 03 |

||||||||||||||||||||||

| Key Measures |

||||||||||||||||||||||||||||

| Latin America(4) |

||||||||||||||||||||||||||||

| Total revenue(2) |

$ | 834 | $ | 33 | $ | 295 | $ | 262 | $ | 268 | $ | 9 | $ | 5 | ||||||||||||||

| Provision for credit losses |

(195 | ) | 89 | (88 | ) | (157 | ) | (7 | ) | 57 | 25 | |||||||||||||||||

| Net income |

310 | (48 | ) | 126 | 151 | 66 | (33 | ) | (16 | ) | ||||||||||||||||||

| Shareholder value added |

180 | (47 | ) | 83 | 106 | 23 | (32 | ) | (15 | ) | ||||||||||||||||||

| Equity Investments |

||||||||||||||||||||||||||||

| Total revenue(2) |

$ | 440 | ($256 | ) | $ | 338 | $ | 115 | $ | 6 | ($19 | ) | ($55 | ) | ||||||||||||||

| Provision for credit losses |

4 | 25 | 4 | — | — | — | 21 | |||||||||||||||||||||

| Net income |

192 | (249 | ) | 189 | 47 | (14 | ) | (30 | ) | (67 | ) | |||||||||||||||||

| Shareholder value added |

(111 | ) | (475 | ) | 96 | (28 | ) | (94 | ) | (85 | ) | (124 | ) | |||||||||||||||

| Other |

||||||||||||||||||||||||||||

| Total revenue(2) |

($210 | ) | $ | 969 | ($127 | ) | ($131 | ) | ($104 | ) | $ | 152 | $ | 161 | ||||||||||||||

| Provision for credit losses |

339 | 275 | (55 | ) | 43 | 139 | 212 | 67 | ||||||||||||||||||||

| Net income |

726 | 902 | (189 | ) | 115 | 444 | 356 | 28 | ||||||||||||||||||||

| Shareholder value added |

(33 | ) | (817 | ) | (276 | ) | (31 | ) | 268 | 6 | (336 | ) | ||||||||||||||||

| (1) | Corporate Other consists primarily of Latin America, Equity Investments, noninterest income, revenue and security gains and noninterest expense associated with the Asset and Liability Management (ALM) process, and the results of certain consumer finance and commercial lending businesses that are being liquidated. |

| (2) | Fully taxable-equivalent basis |

| (3) | Includes merger and restructuring charges, net of taxes, of $411 in year-to-date 2004, $181 in 4Q04, $147 in 3Q04 and $83 in 2Q04. |

| (4) | Excludes Mexico, which is included in Global Corporate and Investment Banking. |

Certain prior period amounts have been reclassified among the segments to conform to the current period presentation.

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

19

Bank of America Corporation

Outstanding Loans and Leases

(Dollars in millions)

| December 31 2004 |

December 31 2003 |

Increase (Decrease) from 12/31/03 |

||||||||

| Residential mortgage |

$ | 178,103 | $ | 140,513 | $ | 37,590 | ||||

| Home equity lines |

50,126 | 23,859 | 26,267 | |||||||

| Direct/Indirect consumer |

40,513 | 33,415 | 7,098 | |||||||

| Credit card |

51,726 | 34,814 | 16,912 | |||||||

| Other consumer(1) |

7,439 | 7,558 | (119 | ) | ||||||

| Total consumer |

327,907 | 240,159 | 87,748 | |||||||

| Commercial - domestic |

122,095 | 91,491 | 30,604 | |||||||

| Commercial - foreign |

18,401 | 10,754 | 7,647 | |||||||

| Commercial real estate(2) |

32,319 | 19,367 | 12,952 | |||||||

| Commercial lease financing |

21,115 | 9,692 | 11,423 | |||||||

| Total commercial |

193,930 | 131,304 | 62,626 | |||||||

| Total |

$ | 521,837 | $ | 371,463 | $ | 150,374 | ||||

| (1) | Includes consumer finance, foreign consumer and consumer lease financing of $3,395, $3,563 and $481 at December 31, 2004, respectively, and $3,905, $1,969 and $1,684 at December 31, 2003, respectively. |

| (2) | Includes domestic and foreign commercial real estate loans of $31,879 and $440 at December 31, 2004, respectively, and $19,043 and $324 at December 31, 2003, respectively. |

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

20

Bank of America Corporation

Commercial Utilized Credit Exposure by Industry(1)

(Dollars in millions)

| December 31 2004 |

December 31, 2003 |

% Increase (Decrease) from 12/31/03 |

|||||||

| Real Estate (2) |

$ | 36,672 | $ | 22,228 | 65 | % | |||

| Diversified financials |

25,932 | 20,427 | 27 | ||||||

| Banks |

25,265 | 25,088 | 1 | ||||||

| Retailing |

23,149 | 15,152 | 53 | ||||||

| Education and government |

17,429 | 13,919 | 25 | ||||||

| Individuals and trusts |

16,110 | 14,307 | 13 | ||||||

| Materials |

14,123 | 8,860 | 59 | ||||||

| Consumer durables and apparel |

13,427 | 8,313 | 62 | ||||||

| Leisure and sports, hotels and restaurants |

13,331 | 10,099 | 32 | ||||||

| Transportation |

13,234 | 9,355 | 41 | ||||||

| Health care equipment and services |

12,643 | 7,064 | 79 | ||||||

| Capital goods |

12,633 | 8,244 | 53 | ||||||

| Commercial services and supplies |

11,944 | 7,206 | 66 | ||||||

| Food, beverage and tobacco |

11,687 | 9,134 | 28 | ||||||

| Energy |

7,579 | 4,348 | 74 | ||||||

| Media |

6,232 | 4,701 | 33 | ||||||

| Insurance |

5,851 | 3,638 | 61 | ||||||

| Religious and social organizations |

5,710 | 4,272 | 34 | ||||||

| Utilities |

5,615 | 5,012 | 12 | ||||||

| Food and staples retailing |

3,610 | 1,837 | 97 | ||||||

| Technology hardware and equipment |

3,398 | 1,941 | 75 | ||||||

| Software and services |

3,292 | 1,655 | 99 | ||||||

| Telecommunication services |

3,030 | 2,526 | 20 | ||||||

| Automobiles and components |

1,894 | 1,326 | 43 | ||||||

| Pharmaceuticals and biotechnology |

994 | 466 | 113 | ||||||

| Household and personal products |

371 | 302 | 23 | ||||||

| Other |

3,132 | 1,474 | 112 | ||||||

| Total |

$ | 298,287 | $ | 212,894 | 40 | ||||

| (1) | Includes loans and leases, standby letters of credit and financial guarantees, derivative assets, assets held for sale and commercial letters of credit. |

| (2) | Industries are viewed from a variety of perspectives to best isolate the perceived risks. For purposes of this table, the Real Estate industry is defined based upon the borrower’s primary business activity using operating cash flow and source of repayment as key factors. |

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior period has not been restated.

21

Bank of America Corporation

Nonperforming Assets

(Dollars in millions)

| 4Q04 |

3Q04 |

2Q04 |

1Q04 |

4Q03 |

||||||||||||||||

| Residential mortgage |

$ | 554 | $ | 532 | $ | 537 | $ | 486 | $ | 531 | ||||||||||

| Home equity lines |

66 | 51 | 42 | 35 | 43 | |||||||||||||||

| Direct/Indirect consumer |

33 | 26 | 31 | 31 | 28 | |||||||||||||||

| Other consumer |

85 | 94 | 99 | 61 | 36 | |||||||||||||||

| Total consumer |

738 | 703 | 709 | 613 | 638 | |||||||||||||||

| Commercial - domestic |

855 | 991 | 1,246 | 1,229 | 1,388 | |||||||||||||||

| Commercial - foreign |

267 | 473 | 503 | 331 | 578 | |||||||||||||||

| Commercial real estate |

87 | 136 | 164 | 115 | 142 | |||||||||||||||

| Commercial lease financing |

266 | 243 | 257 | 66 | 127 | |||||||||||||||

| Total commercial |

1,475 | 1,843 | 2,170 | 1,741 | 2,235 | |||||||||||||||

| Total nonperforming loans and leases |

2,213 | 2,546 | 2,879 | 2,354 | 2,873 | |||||||||||||||

| Nonperforming securities(1) |

140 | 157 | 156 | — | — | |||||||||||||||

| Foreclosed properties |

102 | 133 | 144 | 131 | 148 | |||||||||||||||

| Total nonperforming assets(2) |

$ | 2,455 | $ | 2,836 | $ | 3,179 | $ | 2,485 | $ | 3,021 | ||||||||||

| Loans past due 90 days or more and still accruing (3) |

$ | 1,294 | $ | 1,120 | $ | 939 | $ | 795 | $ | 860 | ||||||||||

| Nonperforming assets / Total assets |

0.22 | % | 0.26 | % | 0.31 | % | 0.31 | % | 0.42 | % | ||||||||||

| Nonperforming assets / Total loans, leases and foreclosed properties |

0.47 | 0.55 | 0.64 | 0.66 | 0.81 | |||||||||||||||

| Nonperforming loans and leases / Total loans and leases |

0.42 | 0.50 | 0.58 | 0.63 | 0.77 | |||||||||||||||

| Allowance for credit losses: |

||||||||||||||||||||

| Allowance for loan and lease losses |

$ | 8,626 | $ | 8,723 | $ | 8,767 | $ | 6,080 | $ | 6,163 | ||||||||||

| Reserve for unfunded lending commitments |

402 | 446 | 486 | 401 | 416 | |||||||||||||||

| Total |

$ | 9,028 | $ | 9,169 | $ | 9,253 | $ | 6,481 | $ | 6,579 | ||||||||||

| Allowance for loan and lease losses / Total loans and leases |

1.65 | % | 1.70 | % | 1.76 | % | 1.62 | % | 1.66 | % | ||||||||||

| Allowance for loan and lease losses / Total nonperforming loans and leases |

390 | 343 | 305 | 258 | 215 | |||||||||||||||

| Commercial criticized exposure |

$ | 10,249 | $ | 12,025 | $ | 13,420 | $ | 10,401 | $ | 12,650 | ||||||||||

| Commercial criticized exposure / Commercial utilized exposure |

3.44 | % | 4.13 | % | 4.73 | % | 4.94 | % | 5.94 | % | ||||||||||

Loans are classified as domestic or foreign based upon the domicile of the borrower.

| (1) | Primarily related to international securities held in the available-for-sale portfolio. |

| (2) | Balances do not include $151, $100, $103, $82 and $202 of nonperforming assets, primarily loans held for sale, included in Other Assets at December 31, 2004, September 30, 2004, June 30, 2004, March 31, 2004, and December 31, 2003, respectively. |

| (3) | 3Q04 has been adjusted for an understatement related to an available-for-sale portfolio acquired with the Fleet acquisition. |

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

22

Bank of America Corporation

Year-to-Date Net Charge-offs and Net Charge-off Ratios

(Dollars in millions)

| Year Ended December 31 |

|||||||||||||

| 2004 |

2003 |

||||||||||||

| Amount |

Percent |

Amount |

Percent |

||||||||||

| Residential mortgage |

$ | 36 | 0.02 | % | $ | 40 | 0.03 | % | |||||

| Home equity lines |

15 | 0.04 | 12 | 0.05 | |||||||||

| Direct/Indirect consumer |

208 | 0.55 | 181 | 0.55 | |||||||||

| Credit card |

2,305 | 5.31 | 1,514 | 5.37 | |||||||||

| Other consumer |

193 | 2.51 | 255 | 2.89 | |||||||||

| Total consumer |

2,757 | 0.93 | 2,002 | 0.91 | |||||||||

| Commercial - domestic |

177 | 0.15 | 633 | 0.68 | |||||||||

| Commercial - foreign |

173 | 1.05 | 306 | 2.36 | |||||||||

| Commercial real estate |

(3 | ) | (0.01 | ) | 41 | 0.20 | |||||||

| Commercial lease financing |

9 | 0.05 | 124 | 1.23 | |||||||||

| Total commercial |

356 | 0.20 | 1,104 | 0.81 | |||||||||

| Total net charge-offs |

$ | 3,113 | 0.66 | $ | 3,106 | 0.87 | |||||||

| By Business Segment: |

|||||||||||||

| Consumer & small business banking |

$ | 2,594 | 1.89 | % | $ | 1,764 | 1.90 | % | |||||

| Commercial banking |

182 | 0.14 | 446 | 0.48 | |||||||||

| Global corporate & investment banking |

127 | 0.37 | 438 | 1.20 | |||||||||

| Wealth & investment management |

6 | 0.01 | 9 | 0.02 | |||||||||

| Corporate other |

204 | 0.16 | 449 | 0.47 | |||||||||

| Total net charge-offs |

$ | 3,113 | 0.66 | $ | 3,106 | 0.87 | |||||||

Loans are classified as domestic or foreign based upon the domicile of the borrower.

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

23

Bank of America Corporation

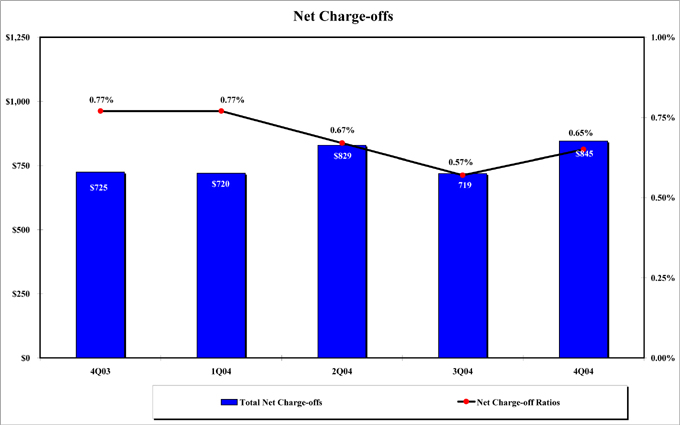

Quarterly Net Charge-offs and Net Charge-off Ratios

(Dollars in millions)

| 4Q04 |

3Q04 |

2Q04 |

1Q04 |

4Q03 |

|||||||||||||||||||||||||||||||

| Amount |

Percent |

Amount |

Percent |

Amount |

Percent |

Amount |

Percent |

Amount |

Percent |

||||||||||||||||||||||||||

| Residential mortgage |

$ | 6 | 0.01 | % | $ | 7 | 0.02 | % | $ | 12 | 0.03 | % | $ | 11 | 0.03 | % | $ | 13 | 0.04 | % | |||||||||||||||

| Home equity lines |

4 | 0.03 | 2 | 0.02 | 5 | 0.05 | 4 | 0.07 | (3 | ) | (0.04 | ) | |||||||||||||||||||||||

| Direct/Indirect consumer |

55 | 0.55 | 56 | 0.57 | 49 | 0.50 | 48 | 0.56 | 48 | 0.57 | |||||||||||||||||||||||||

| Credit card |

691 | 5.57 | 586 | 5.09 | 585 | 5.45 | 443 | 5.05 | 423 | 5.12 | |||||||||||||||||||||||||

| Other consumer(1) |

45 | 2.39 | 49 | 2.53 | 42 | 2.10 | 57 | 3.07 | 66 | 3.37 | |||||||||||||||||||||||||

| Total consumer |

801 | 0.98 | 700 | 0.89 | 693 | 0.92 | 563 | 0.93 | 547 | 0.91 | |||||||||||||||||||||||||

| Commercial - domestic |

27 | 0.09 | 25 | 0.08 | 76 | 0.25 | 49 | 0.22 | 93 | 0.41 | |||||||||||||||||||||||||

| Commercial - foreign |

5 | 0.09 | (4 | ) | (0.09 | ) | 66 | 1.47 | 106 | 3.98 | 76 | 2.60 | |||||||||||||||||||||||

| Commercial real estate |

1 | 0.02 | 1 | 0.02 | (3 | ) | (0.04 | ) | (2 | ) | (0.05 | ) | 9 | 0.18 | |||||||||||||||||||||

| Commercial lease financing |

11 | 0.21 | (3 | ) | (0.07 | ) | (3 | ) | (0.06 | ) | 4 | 0.17 | — | 0.00 | |||||||||||||||||||||

| Total commercial |

44 | 0.09 | 19 | 0.04 | 136 | 0.28 | 157 | 0.48 | 178 | 0.54 | |||||||||||||||||||||||||

| Total net charge-offs |

$ | 845 | 0.65 | $ | 719 | 0.57 | $ | 829 | 0.67 | $ | 720 | 0.77 | $ | 725 | 0.77 | ||||||||||||||||||||

| By Business Segment: |

|||||||||||||||||||||||||||||||||||

| Consumer & small business banking |

$ | 768 | 1.98 | % | $ | 662 | 1.75 | % | $ | 665 | 1.83 | % | $ | 499 | 2.04 | % | $ | 485 | 2.02 | % | |||||||||||||||

| Commercial banking |

45 | 0.12 | 43 | 0.12 | 32 | 0.09 | 62 | 0.26 | 75 | 0.31 | |||||||||||||||||||||||||

| Global corporate & investment banking |

(25 | ) | (0.29 | ) | (6 | ) | (0.07 | ) | 69 | 0.73 | 89 | 1.24 | 50 | 0.64 | |||||||||||||||||||||

| Wealth & investment management |

3 | 0.03 | 1 | 0.01 | (4 | ) | (0.04 | ) | 6 | 0.06 | (1 | ) | (0.01 | ) | |||||||||||||||||||||

| Corporate other |

54 | 0.16 | 19 | 0.06 | 67 | 0.21 | 64 | 0.23 | 116 | 0.41 | |||||||||||||||||||||||||

| Total net charge-offs |

$ | 845 | 0.65 | $ | 719 | 0.57 | $ | 829 | 0.67 | $ | 720 | 0.77 | $ | 725 | 0.77 | ||||||||||||||||||||

Loans are classified as domestic or foreign based upon the domicile of the borrower.

| (1) | Includes lease financing of $5, $7, $5, $10 and $10 for the quarters ended December 31, 2004, September 30, 2004, June 30, 2004, March 31, 2004, and December 31, 2003, respectively. |

Information for periods after April 1, 2004 includes the FleetBoston acquisition; prior periods have not been restated.

24

Bank of America Corporation

Selected Emerging Markets (1)

| (Dollars in millions) |

Loans and Loan Commitments |

Other Financing (2) |

Derivative Assets |

Securities/ Other Investments (3,4) |

Total Cross- border Exposure (5) |

Local Country Exposure Net of Local Liabilities (6) |

Total Foreign Exposure December 31, 2004 |

Increase/ (Decrease) from December 31, 2003 |

|||||||||||||||||

| Region/Country |

|||||||||||||||||||||||||

| Latin America |

|||||||||||||||||||||||||

| Argentina |

$ | 181 | $ | 105 | $ | 0 | $ | 89 | $ | 375 | $ | 16 | $ | 391 | $ | 80 | |||||||||

| Brazil (7) |

1,179 | 268 | 19 | 122 | 1,588 | 1,837 | 3,425 | 2,754 | |||||||||||||||||

| Chile |

215 | 122 | 1 | 3 | 341 | 839 | 1,180 | 1,049 | |||||||||||||||||

| Mexico (8) |

578 | 148 | 136 | 2,004 | 2,866 | 0 | 2,866 | 83 | |||||||||||||||||

| Other Latin America (9) |

311 | 180 | 144 | 248 | 883 | 192 | 1,075 | 358 | |||||||||||||||||

| Total Latin America |

2,464 | 823 | 300 | 2,466 | 6,053 | 2,884 | 8,937 | 4,324 | |||||||||||||||||

| Asia Pacific |

|||||||||||||||||||||||||

| Hong Kong (10) |

225 | 57 | 307 | 129 | 718 | 401 | 1,119 | 249 | |||||||||||||||||

| India |

311 | 268 | 140 | 225 | 944 | 548 | 1,492 | (73 | ) | ||||||||||||||||

| Singapore |

200 | 23 | 70 | 47 | 340 | 0 | 340 | (227 | ) | ||||||||||||||||

| South Korea |

290 | 477 | 89 | 213 | 1,069 | 314 | 1,383 | (235 | ) | ||||||||||||||||

| Taiwan |

214 | 114 | 82 | 42 | 452 | 875 | 1,327 | 786 | |||||||||||||||||

| Other Asia Pacific (9) |

81 | 80 | 58 | 278 | 497 | 157 | 654 | (222 | ) | ||||||||||||||||

| Total Asia Pacific |

1,321 | 1,019 | 746 | 934 | 4,020 | 2,295 | 6,315 | 278 | |||||||||||||||||

| Central and Eastern Europe (9) |

7 | 30 | 31 | 173 | 241 | 0 | 241 | (29 | ) | ||||||||||||||||

| Total |

$ | 3,792 | $ | 1,872 | $ | 1,077 | $ | 3,573 | $ | 10,314 | $ | 5,179 | $ | 15,493 | $ | 4,573 | |||||||||

| (1) | There is no generally accepted definition of emerging markets. The definition that we use includes all countries in Latin America excluding Cayman Islands and Bermuda; all countries in Asia Pacific excluding Japan, Australia and New Zealand; and all countries in Central and Eastern Europe excluding Greece. |

| (2) | Includes acceptances, standby letters of credit, commercial letters of credit and formal guarantees. |

| (3) | Amounts outstanding for Other Latin America and Other Asia Pacific have been reduced by $196 and $14, respectively, at December 31, 2004 and $173 and $13, respectively, at December 31, 2003. These amounts represent the fair value of U.S. Treasury securities held as collateral outside the country of exposure. |

| (4) | Cross-border resale agreements are presented based on the domicile of the counterparty because the counterparty has the legal obligation for repayment. For regulatory reporting under Federal Financial Institutions Examination Council (FFIEC) guidelines, cross-border resale agreements are presented based on the domicile of the issuer of the securities that are held as collateral. |

| (5) | Cross-border exposure includes amounts payable to the Corporation by borrowers with a country of residence other than the one in which the credit is booked, regardless of the currency in which the claim is denominated, consistent with FFIEC reporting rules. |

| (6) | Local country exposure includes amounts payable to the Corporation by borrowers with a country of residence in which the credit is booked, regardless of the currency in which the claim is denominated. Management subtracts local funding or liabilities from local exposures as allowed by the FFIEC. Total amount of local country exposure funded by local liabilities at December 31, 2004 was $17,189 compared to $5,336 at December 31, 2003. Local country exposure funded by local liabilities at December 31, 2004 in Latin America and Asia Pacific was $9,098 and $8,091, respectively, of which $4,240 was in Brazil, $3,432 in Hong Kong, $2,596 in Singapore, $1,662 in Argentina, $1,210 in Chile and $1,092 in Mexico. There were no other countries with local country exposure funded by local liabilities greater than $500 million. |

| (7) | The Corporation has certain risk mitigation instruments associated with Brazil including insurance contracts, other trade-related transfer risk mitigation and third party funding. Ability to file a claim under insurance policies vary with the country’s current political and economic environment. |

| Risk Mitigation |

Brazil | ||

| Total foreign exposure, December 31, 2004 |

$ | 3,425 | |