Subject to Completion

Preliminary Pricing Supplement dated January 31, 2008

| PRICING SUPPLEMENT (To MTN prospectus supplement, general prospectus supplement and prospectus each dated March 31, 2006) Pricing Supplement Number: |

Filed Pursuant to Rule 424(b)(3) Registration No. 333-132911 |

Units

Merrill Lynch & Co., Inc.

Medium-Term Notes, Series C

100% Principal Protected Auto-Callable Notes

Linked to the 2-Year U.S. Dollar Constant Maturity Swap Rate

due February , 2011

(the “Notes”)

$1,000 original public offering price per unit

Information included in this pricing supplement supersedes information in the accompanying MTN prospectus supplement, general prospectus supplement and prospectus to the extent that it is different from that information.

Investing in the Notes involves risks that are described in the “ Risk Factors” section beginning on page PS-6 of this pricing supplement and beginning on page S-3 of the accompanying MTN prospectus supplement.

In connection with this offering, each of Merrill Lynch, Pierce, Fenner & Smith Incorporated and its broker-dealer affiliate, First Republic Securities Company, LLC, is acting in its capacity as a principal.

| Per Unit | Total | ||||

| Public offering price |

$ | 1,000 | $ | ||

| Underwriting discount |

$ | 10 | $ | ||

| Proceeds, before expenses, to Merrill Lynch & Co., Inc. |

$ | 990 | $ | ||

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this pricing supplement or the accompanying MTN prospectus supplement, general prospectus supplement and prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Merrill Lynch & Co.

The date of this pricing supplement is February , 2008.

Pricing Supplement

| PS-3 | ||

| PS-6 | ||

| PS-9 | ||

| PS-12 | ||

| PS-13 | ||

| PS-17 | ||

| PS-18 | ||

| PS-18 | ||

| PS-18 | ||

| PS-20 | ||

| Medium-Term Notes, Series C Prospectus Supplement (the “MTN prospectus supplement”) | ||

| RISK FACTORS |

S-3 | |

| DESCRIPTION OF THE NOTES |

S-4 | |

| UNITED STATES FEDERAL INCOME TAXATION |

S-22 | |

| PLAN OF DISTRIBUTION |

S-29 | |

| VALIDITY OF THE NOTES |

S-30 | |

| Debt Securities, Warrants, Preferred Stock, Depositary Shares and Common Stock Prospectus Supplement (the “general prospectus supplement”) | ||

| MERRILL LYNCH & CO., INC |

S-3 | |

| USE OF PROCEEDS |

S-3 | |

| RATIO OF EARNINGS TO FIXED CHARGES AND RATIO OF EARNINGS TO COMBINED FIXED CHARGES AND PREFERRED STOCK DIVIDENDS |

S-4 | |

| THE SECURITIES |

S-4 | |

| DESCRIPTION OF DEBT SECURITIES |

S-5 | |

| DESCRIPTION OF DEBT WARRANTS |

S-16 | |

| DESCRIPTION OF CURRENCY WARRANTS |

S-18 | |

| DESCRIPTION OF INDEX WARRANTS |

S-20 | |

| DESCRIPTION OF PREFERRED STOCK |

S-25 | |

| DESCRIPTION OF DEPOSITARY SHARES |

S-32 | |

| DESCRIPTION OF PREFERRED STOCK WARRANTS |

S-36 | |

| DESCRIPTION OF COMMON STOCK |

S-38 | |

| DESCRIPTION OF COMMON STOCK WARRANTS |

S-42 | |

| PLAN OF DISTRIBUTION |

S-44 | |

| WHERE YOU CAN FIND MORE INFORMATION |

S-45 | |

| INCORPORATION OF INFORMATION WE FILE WITH THE SEC |

S-46 | |

| EXPERTS |

S-46 | |

| Prospectus | ||

| WHERE YOU CAN FIND MORE INFORMATION |

2 | |

| INCORPORATION OF INFORMATION WE FILE WITH THE SEC |

2 | |

| EXPERTS |

2 | |

PS-2

This summary includes questions and answers that highlight selected information from this pricing supplement and the accompanying MTN prospectus supplement, general prospectus supplement and prospectus to help you understand the 100% Principal Protected Auto-Callable Notes Linked to the 2-Year U.S. Dollar Constant Maturity Swap Rate due February , 2011 (the “Notes“). You should carefully read this pricing supplement and the accompanying MTN prospectus supplement, general prospectus supplement and prospectus to fully understand the terms of the Notes and the tax and other considerations that are important to you in making a decision about whether to invest in the Notes. You should carefully review the “Risk Factors” section of this pricing supplement and the accompanying MTN prospectus supplement, which highlights certain risks associated with an investment in the Notes, to determine whether an investment in the Notes is appropriate for you.

References in this pricing supplement to “ML&Co.”, “we”, “us” and “our” are to Merrill Lynch & Co., Inc., and references to “MLPF&S” are to Merrill Lynch, Pierce, Fenner & Smith Incorporated.

What are the Notes?

The Notes will be a series of senior debt securities issued by ML&Co. entitled “Medium-Term Notes, Series C” and will not be secured by collateral. The Notes will rank equally with all of our other unsecured and unsubordinated debt. The Notes are expected to mature in February 2011, unless automatically called, as described in this pricing supplement. Depending on the date the Notes are priced for initial sale to the public (the “Pricing Date”), which may be any time in February or March, the settlement date may occur in February or March and the maturity date may occur in February or March. Any reference in this pricing supplement to the month in which the settlement date or maturity date will occur is subject to change as specified above.

Each unit will represent a single Note with a $1,000 principal amount. You may transfer the Notes only in whole units. You will not have the right to receive physical certificates evidencing your ownership except under limited circumstances. Instead, we will issue the Notes in the form of a global certificate, which will be held by The Depository Trust Company, also known as DTC, or its nominee. Direct and indirect participants in DTC will record your ownership of the Notes. You should refer to the section entitled “Description of the Debt Securities—Depositary” in the accompanying general prospectus supplement.

Are there any risks associated with my investment?

Yes, an investment in the Notes is subject to certain risks. Please refer to the section entitled “Risk Factors” in this pricing supplement and the accompanying MTN prospectus supplement.

What does the 2-Year U.S. Dollar Constant Maturity Swap Rate reflect?

For purposes of determining whether the Notes are subject to automatic call on any Call Date, the “2-Year U.S. Dollar Constant Maturity Swap Rate” is a constant maturity swap rate that measures the fixed rate legs of a hypothetical fixed-rate-for-floating rate swap transaction, where the fixed rate payment stream is reset each period relative to a regularly available fixed maturity market rate and is exchangeable for a floating 3-month LIBOR-based payment stream, as quoted on Reuters page ISDAFIX3, at 11:00 a.m., New York City time.

For more information, please see the section entitled “Description of the Notes—Automatic Call” in this pricing supplement.

How has the 2-Year U.S. Dollar Constant Maturity Swap Rate performed historically?

We have included a graph showing daily levels of the 2-Year U.S. Dollar Constant Maturity Swap Rate from January 23, 1998 to January 24, 2008 in the section entitled “The 2-Year U.S. Dollar Constant Maturity Swap Rate” in this pricing supplement. We have provided this historical information to help you evaluate the behavior of the 2-Year U.S. Dollar Constant Maturity Swap Rate in various economic environments; however, past behavior is not necessarily indicative of how the 2-Year U.S. Dollar Constant Maturity Swap Rate will perform in the future.

What will I receive on the maturity date of the Notes?

Unless the Notes have been subject to automatic call, you will receive a cash amount equal to $1,000 per unit on the maturity date.

How does the automatic call feature work?

ML&Co. will call and redeem the Notes, in whole but not in part, at the applicable Call Price on a Call Date if the 2-Year U.S. Dollar Constant Maturity Swap Rate on the fifth Business Day prior to such

PS-3

Call Date (an “Observation Date”) is equal to or less than the Strike Rate.

The “Strike Rate” will be a fixed rate which will be not greater than the level of the 2-Year U.S. Dollar Constant Maturity Swap Rate on the Pricing Date plus 0.50%, and not less than such level minus 0.40%. The actual Strike Rate will be determined on the Pricing Date and will be set forth in the final pricing supplement made available in connection with sales of the Notes.

The “Call Price” per unit of the Notes, if automatically called pursuant to its terms, will equal the $1,000 principal amount plus an amount that represents a return of 8.00% per annum from the issue date until the date on which the Notes are automatically called, as set forth in the section entitled “Description of the Notes—Automatic Call”.

Upon automatic call, the Notes will no longer be outstanding and no additional payments will be made on the Notes on any subsequent Call Date or on the maturity date.

A “Call Date” will occur on the day of each month, from and including February , 2009 to and including the maturity date. If a Call Date is not a Business Day, payment of the Call Price will be made on the immediately succeeding Business Day and no additional interest will accrue as a result of such delayed payment.

“Business Day” means any day other than a Saturday or Sunday that is neither a legal holiday nor a day on which banking institutions in The City of New York are authorized or required by law, regulation or executive order to close.

Will I receive interest payments on the Notes?

You will not receive any interest payments on the Notes, but you will instead receive the Call Price per unit of Notes if automatically called on a Call Date. The Call Price will represent a return of 8.00% per annum on the Notes from the issue date until the date on which the Notes are automatically called. If the Notes have not become subject to an automatic call, you will receive a cash amount equal to $1,000 per unit of Notes on the maturity date, and will not receive any return on your investment. We have designed the Notes for investors who are willing to forego interest payments on the Notes, such as fixed or floating interest rates paid on traditional interest bearing debt securities, in exchange for the ability to participate in the possibility that the 2-Year U.S. Dollar Constant Maturity Swap Rate will be equal to or less than the Strike Rate on an Observation Date.

What about taxes?

Each year, you will be required to pay taxes on ordinary income from the Notes over their term based upon an estimated yield for the Notes. We have determined this estimated yield, in accordance with regulations issued by the U.S. Treasury Department, solely in order for you to calculate the amount of taxes that you will owe each year as a result of owning a Note. This estimated yield is neither a prediction nor a guarantee of what the actual yield on the Notes will be. We have determined that this estimated yield will equal % per annum, compounded semi-annually. For further information, see “United States Federal Income Taxation” in this pricing supplement.

Will the Notes be listed on a stock exchange?

The Notes will not be listed on any securities exchange and we do not expect a trading market for the Notes to develop, which may affect the price that you receive for your Notes upon any sale prior to the maturity date or automatic call. You should review the section entitled “Risk Factors— In seeking to provide investors with what we believe to be commercially reasonable terms for the Notes while providing MLPF&S with compensation for its services, we have considered the costs of developing, hedging and distributing the Notes. If a trading market develops for the Notes (and such a market may not develop), these costs are expected to affect the market price you may receive or be quoted for your Notes on a date prior to the stated maturity date” in this pricing supplement.

What price can I expect to receive if I sell the Notes prior to the stated maturity date?

In determining the economic terms of the Notes, and consequently the potential return on the Notes to you, a number of factors are taken into account. Among these factors are certain costs associated with creating, hedging and offering the Notes. In structuring the economic terms of the Notes, we seek to provide investors with what we believe to be commercially reasonable terms and to provide MLPF&S with compensation for its services in developing the Notes.

If you sell your Notes prior to the stated maturity date, you will receive a price determined by market conditions for the Notes. This price may be influenced by many factors, such as interest rates and the volatility of the 2-Year U.S. Dollar Constant Maturity Swap Rate, and the expectations of the amount, if any, by which the 2-Year U.S. Dollar Constant Maturity Swap Rate will increase or decline

PS-4

in the future. In addition, the price, if any, at which you could sell your Notes in a secondary market transaction is expected to be affected by the factors that we considered in setting the economic terms of the Notes, namely the underwriting discount paid in respect of the Notes and other costs associated with the Notes, and compensation for developing and hedging the product. Depending on the impact of these factors, you may receive significantly less than the $1,000 principal amount per unit of your Notes if sold before the stated maturity date.

In a situation where there had been no change in the 2-Year U.S. Dollar Constant Maturity Swap Rate and no changes in the market conditions or any other relevant factors from those existing on the date of this pricing supplement, the price, if any, at which you could sell your Notes in a secondary market transaction is expected to be lower than the $1,000 principal amount per unit. This is due to, among other things, our costs of developing, hedging and distributing the Notes. Any potential purchasers for your Notes in the secondary market are unlikely to consider these factors.

What is the role of MLPF&S?

MLPF&S, our subsidiary, is the underwriter for the offering and sale of the Notes.

After the initial offering, MLPF&S currently intends to buy and sell Notes to create a secondary market for holders of the Notes, and may stabilize or maintain the market price of the Notes during their initial distribution. However, MLPF&S will not be obligated to engage in any of these market activities or continue them once it has started.

What is the role of Merrill Lynch Capital Services, Inc.?

Merrill Lynch Capital Services, Inc. (“MLCS”), our subsidiary, will be our agent for purposes of determining, among other things, whether the Notes will be automatically called on any Call Date (in such capacity, the “Calculation Agent”). Under certain circumstances, these duties could result in a conflict of interest between MLCS as our subsidiary and its responsibilities as Calculation Agent.

What is ML&Co.?

Merrill Lynch & Co., Inc. is a holding company with various subsidiaries and affiliated companies that provide investment, financing, insurance and related services on a global basis.

For information about ML&Co., see the section entitled “Merrill Lynch & Co., Inc.” in the accompanying general prospectus supplement. You should also read the other documents we have filed with the SEC, which you can find by referring to the sections entitled “Where You Can Find More Information” and “Incorporation of Information We File with the SEC” in the accompanying general prospectus supplement and prospectus.

PS-5

Your investment in the Notes will involve certain risks. You should consider carefully the following discussion of risks and the discussion of risks included in the accompanying MTN prospectus supplement before you decide that an investment in the Notes is suitable for you.

You may not earn a return on your investment

If the Notes are not automatically called, payment on the Notes would be limited to the $1,000 principal amount per unit, payable on the maturity date, even if the 2-Year U.S. Dollar Constant Maturity Swap Rate is equal to or less than the Strike Rate on some days during the term of the Notes, but not on any Observation Dates.

The 2-Year U.S. Dollar Constant Maturity Swap Rate may increase or decrease. We have no control over domestic and international economic, financial, political and other events, or the over-all supply and demand for relevant U.S. dollar-denominated securities, that may affect the direction or magnitude of changes in the 2-Year U.S. Dollar Constant Maturity Swap Rate. Historically, the level of the 2-Year U.S. Dollar Constant Maturity Swap Rate has been volatile, and such volatility may occur in the future. However, past experience is not necessarily indicative of what may occur in the future.

Your potential return upon an automatic call is limited

Your investment in the Notes will result in a gain if the 2-Year U.S. Dollar Constant Maturity Swap Rate is equal to or less than the Strike Rate on any Observation Date. If the Notes are automatically called on any Call Date, your return on the Notes will be limited to an annual simple rate of return of 8.00% regardless of the magnitude of the decline in the 2-Year U.S. Dollar Constant Maturity Swap Rate. In addition, the automatic call feature may shorten the term of your investment.

Your yield may be lower than the yield on other debt securities of comparable maturity

The yield that you receive on your Notes may be less than the return you could earn on other investments. Your yield may be less than the yield you would earn if you bought a traditional interest bearing debt security of ML&Co. with the same stated maturity date. Your investment may not reflect the full opportunity cost to you when you take into account factors that affect the time value of money.

In seeking to provide investors with what we believe to be commercially reasonable terms for the Notes while providing MLPF&S with compensation for its services, we have considered the costs of developing, hedging and distributing the Notes. If a trading market develops for the Notes (and such a market may not develop), these costs are expected to affect the market price you may receive or be quoted for your Notes on a date prior to the stated maturity date

The Notes will not be listed on any securities exchange and we do not expect a trading market for the Notes to develop. Although MLPF&S, our affiliate, has indicated that it currently expects to bid for Notes offered for sale to it by holders of the Notes, it is not required to do so and may cease making those bids at any time. The limited trading market for your Notes may affect the price that you receive for your Notes if you do not wish to hold your investment until the maturity date.

In determining the economic terms of the Notes, and consequently the potential return on the Notes to you, a number of factors are taken into account. Among these factors are certain costs associated with creating, hedging and offering the Notes. In structuring the economic terms of the Notes, we seek to provide investors with what we believe to be commercially reasonable terms and to provide MLPF&S with compensation for its services in developing the securities. If MLPF&S makes a market in the Notes, the price it quotes would reflect any changes in market conditions and other relevant factors. In addition, the price, if any, at which you could sell your Notes in a secondary market transaction is expected to be affected by the factors that we considered in setting the economic terms of the Notes, namely the underwriting discount paid in respect of the Notes and other costs associated with the Notes, including compensation for developing and hedging the product. This quoted price could be higher or lower

PS-6

than the principal amount. Furthermore, there is no assurance that MLPF&S or any other party will be willing to buy the Notes. MLPF&S is not obligated to make a market in the Notes.

Assuming there is no change in market conditions or any other relevant factors, the price, if any, at which MLPF&S or another purchaser might be willing to purchase your Notes in a secondary market transaction is expected to be lower than the principal amount of the Notes. This is due to, among other things, the fact that the principal amount included, and secondary market prices are likely to exclude, underwriting discount paid with respect to, and the developing and hedging costs associated with, the Notes.

Many factors affect the trading value of the Notes; these factors interrelate in complex ways and the effect of any one factor may offset or magnify the effect of another factor

The trading value of the Notes will be affected by factors that interrelate in complex ways. The effect of one factor may offset the increase in the trading value of the Notes caused by another factor and the effect of one factor may exacerbate the decrease in the trading value of the Notes caused by another factor. The following paragraphs describe the expected impact on the trading value of the Notes given a change in a specific factor, assuming all other conditions remain constant.

The level of the 2-Year U.S. Dollar Constant Maturity Swap Rate is expected to affect the trading value of the Notes. We expect that the trading value of the Notes will depend substantially on whether the level of the 2-Year U.S. Dollar Constant Maturity Swap Rate is equal to or less than the Strike Rate. In general, the value of the Notes will increase when the 2-Year U.S. Dollar Constant Maturity Swap Rate is equal to less than the Strike Rate and the value of the Notes will decrease when the 2-Year U.S. Dollar Constant Maturity Swap Rate is greater than the Strike Rate.

Changes in the volatility of the 2-Year U.S. Dollar Constant Maturity Swap Rate are expected to affect the trading value of the Notes. Volatility is the term used to describe the size and frequency of price and/or market fluctuations. If the volatility of the 2-Year U.S. Dollar Constant Maturity Swap Rate increases or decreases, the trading value of the Notes may be adversely affected.

Changes in the levels of interest rates are expected to affect the trading value of the Notes. We expect that changes in interest rates will affect the trading value of the Notes. Generally, if United States interest rates increase, we expect the trading value of the Notes will decrease and, conversely, if United States interest rates decrease, we expect the trading value of the Notes will increase.

As the time remaining to the stated maturity date of the Notes decreases, the “time premium” associated with the Notes is expected to decrease. We anticipate that before their stated maturity date, the Notes may trade at a value above that which would be expected based on the level of interest rates and the level of the 2-Year U.S. Dollar Constant Maturity Swap Rate. This difference will reflect a “time premium” due to expectations concerning the level of the 2-Year U.S. Dollar Constant Maturity Swap Rate during the period before the stated maturity date of the Notes. However, as the time remaining to the stated maturity date of the Notes decreases, we expect that this time premium will decrease, lowering the trading value of the Notes.

Changes in our credit ratings may affect the trading value of the Notes. Our credit ratings are an assessment of our ability to pay our obligations. Consequently, real or anticipated changes in our credit ratings may affect the trading value of the Notes. However, because the return on your Notes is dependent upon factors in addition to our ability to pay our obligations under the Notes, such as the change in the level of the 2-Year U.S. Dollar Constant Maturity Swap Rate during the term of the Notes, an improvement in our credit ratings will not reduce the other investment risks related to the Notes.

In general, assuming all relevant factors are held constant, we expect that the effect on the trading value of the Notes of a given change in some of the factors listed above will be less if it occurs later in the term of the Notes than if it occurs earlier in the term of the Notes.

PS-7

Potential conflicts of interest could arise

MLCS, our subsidiary, is our agent for the purposes of determining, among other things, the 2-Year U.S. Dollar Constant Maturity Swap Rate on an Observation Date and whether the Notes will be automatically called on any Call Date. Under certain circumstances, MLCS as our subsidiary and its responsibilities as Calculation Agent for the Notes could give rise to conflicts of interests. These conflicts could occur, for instance, in connection with judgments that it would be required to make in the event of unavailability of the 2-Year U.S. Dollar Constant Maturity Swap Rate. MLCS is required to carry out its duties as Calculation Agent in good faith and using its reasonable judgment. However, because we control MLCS, potential conflicts of interest could arise.

We expect to enter into arrangements to hedge the market risks associated with our obligation to pay the amounts due on the maturity date on the Notes. We may seek competitive terms in entering into the hedging arrangements for the Notes, but are not required to do so, and we may enter into such hedging arrangements with one of our subsidiaries or affiliated companies. Such hedging activity is expected to result in a profit to those engaging in the hedging activity, which could be more or less than initially expected, but which could also result in a loss for the hedging counterparty.

PS-8

ML&Co. will issue the Notes as a series of senior unsecured debt securities entitled “Medium-Term Notes, Series C,” which is more fully described in the MTN prospectus supplement, under the 1983 Indenture, which is more fully described in the accompanying general prospectus supplement. The Bank of New York has succeeded JPMorgan Chase Bank, N.A. as the trustee under such indenture. Unless called and redeemed automatically on any earlier Call Date, the Notes will mature on February , 2011. Information included in this pricing supplement supersedes information in the accompanying MTN prospectus supplement, general prospectus supplement and prospectus to the extent that it is different from that information. The CUSIP number for the Notes is .

There will be no payments on the Notes prior to the maturity date or, if automatically called, as the case may be, prior to the applicable Call Date. There will be no payment of interest, periodic or otherwise, on the Notes.

Other than pursuant to an automatic call in accordance with its terms, the Notes are not redeemable prior to maturity, nor are they subject to repayment at the option of the holder prior to the maturity date.

ML&Co. will issue the Notes in denominations of whole units each with a $1,000 principal amount per unit. You may transfer the Notes only in whole units. You will not have the right to receive physical certificates evidencing your ownership except under limited circumstances. Instead, we will issue the Notes in the form of a global certificate, which will be held by The Depository Trust Company, also known as DTC, or its nominee. Direct and indirect participants in DTC will record your ownership of the Notes. You should refer to the section entitled “Description of Debt Securities—Depositary” in the accompanying general prospectus supplement.

The Notes will not have the benefit of any sinking fund.

Payment on the Maturity Date

Unless the Notes have been subject to automatic call, you will be entitled to receive a cash amount equal to $1,000 per unit of Notes on the maturity date.

Automatic Call

ML&Co. will call and redeem the Notes, in whole but not in part, at the applicable Call Price on a Call Date if the 2-Year U.S. Dollar Constant Maturity Swap Rate on the fifth Business Day prior to such Call Date (an “Observation Date”) is less than or equal to the Strike Rate.

The “Strike Rate” will be a fixed rate which will be not greater than the level of the 2-Year U.S. Dollar Constant Maturity Swap Rate on the date the Notes are priced for initial sale to the public (the “Pricing Date”) plus 0.50%, and not less than such level minus 0.40%. The actual Strike Rate will be determined on the Pricing Date, and will be set forth in the final pricing supplement made available in connection with sales of the Notes.

The “2-Year U.S. Dollar Constant Maturity Swap Rate” is a constant maturity swap rate that measures the fixed rate legs of a hypothetical fixed-rate-for-floating rate swap transaction, where the fixed rate payment stream is reset each period relative to a regularly available fixed maturity market rate and is exchangeable for a floating 3-month LIBOR-based payment stream, as quoted on Reuters page ISDAFIX3, at 11:00 a.m., New York City time.

If the 2-Year U.S. Dollar Constant Maturity Swap Rate is not quoted on Reuters page ISDAFIX3, or any page substituted therefor, then the 2-Year U.S. Dollar Constant Maturity Swap Rate will be a percentage determined on the basis of the mid-market semi-annual swap rate quotations provided by three banks chosen by the Calculation Agent at approximately 11:00 a.m., New York City time, on that day, and, for this purpose, the semi-annual swap rate means the mean of the bid and offered rates for the semi-annual fixed leg, calculated on the basis of a 360-day year consisting of twelve 30-day months, of a fixed for floating U.S. dollar interest rate swap transaction with a term equal to 2 years, commencing on the applicable date and in a representative amount with an acknowledged dealer of good credit in the swap market, where the floating leg, calculated on the actual number of days in a 360-day year, is equivalent to USD-LIBOR-BBA, as quoted on Reuters page LIBOR01 at 11:00 a.m., New York City time, with a designated maturity of three months. The Calculation Agent will request the principal New York City office of each of the three banks chosen by the Calculation Agent to provide a quotation of its rate. If at least three quotations are

PS-9

provided, the rate for the relevant date will be the arithmetic mean of the quotations. If two quotations are provided, the rate for the relevant date will be the arithmetic mean of the two quotations. If only one quotation is provided, the rate for the relevant date will equal that one quotation. If no quotations are available, then the 2-Year U.S. Dollar Constant Maturity Swap Rate will be the rate the Calculation Agent, in its sole discretion, determines to be fair and reasonable under the circumstances at approximately 11:00 a.m., New York City time, on the relevant date. For more information on the 2-Year U.S. Dollar Constant Maturity Swap Rate, please see the section entitled “The 2-Year U.S. Dollar Constant Maturity Swap Rate” in this pricing supplement.

The “Call Price” per unit of the Notes, if automatically called pursuant to its terms, will equal the $1,000 principal amount plus an amount that represents a return of 8.00% per annum from the issue date until the date on which the Notes are automatically called as set forth below:

| Call Date | Call Price per unit | Total rate of return on the Notes |

||||||||||||

| February , |

2009 | $1,080.00 | 8.000% | |||||||||||

| March , |

2009 | $1,086.67 | 8.667% | |||||||||||

| April , |

2009 | $1,093.33 | 9.333% | |||||||||||

| May , |

2009 | $1,100.00 | 10.000% | |||||||||||

| June , |

2009 | $1,106.67 | 10.667% | |||||||||||

| July , |

2009 | $1,113.33 | 11.333% | |||||||||||

| August , |

2009 | $1,120.00 | 12.000% | |||||||||||

| September , |

2009 | $1,126.67 | 12.667% | |||||||||||

| October , |

2009 | $1,133.33 | 13.333% | |||||||||||

| November , |

2009 | $1,140.00 | 14.000% | |||||||||||

| December , |

2009 | $1,146.67 | 14.667% | |||||||||||

| January , |

2010 | $1,153.33 | 15.333% | |||||||||||

| February , |

2010 | $1,160.00 | 16.000% | |||||||||||

| March , |

2010 | $1,166.67 | 16.667% | |||||||||||

| April , |

2010 | $1,173.33 | 17.333% | |||||||||||

| May , |

2010 | $1,180.00 | 18.000% | |||||||||||

| June , |

2010 | $1,186.67 | 18.667% | |||||||||||

| July , |

2010 | $1,193.33 | 19.333% | |||||||||||

| August , |

2010 | $1,200.00 | 20.000% | |||||||||||

| September , |

2010 | $1,206.67 | 20.667% | |||||||||||

| October , |

2010 | $1,213.33 | 21.333% | |||||||||||

| November , |

2010 | $1,220.00 | 22.000% | |||||||||||

| December , |

2010 | $1,226.67 | 22.667% | |||||||||||

| January , |

2011 | $1,233.33 | 23.333% | |||||||||||

| February , |

2011 | $1,240.00 | 24.000% | |||||||||||

Upon automatic call, the Notes will no longer be outstanding and no additional payments will be made on the Notes on any subsequent Call Date or on the maturity date.

A “Call Date” will occur on the day of each month, from and including February , 2009 to and including the maturity date. If a Call Date is not a Business Day, payment of the Call Price will be made on the immediately succeeding Business Day and no additional interest will accrue as a result of such delayed payment.

“Business Day” means any day other than a Saturday or Sunday that is neither a legal holiday nor a day on which banking institutions in The City of New York are authorized or required by law, regulation or executive order to close.

ML&Co. will give notice of any automatic call to the trustee no later than the second Business Day immediately succeeding the applicable Observation Date. The notice to the trustee will specify the Call Date on which the Notes will be automatically called and the applicable Call Price. The trustee will provide notice of the automatic call to the registered holder of the Notes, specifying the Call Date and the Call Price. The depositary, as the registered holder, will receive the notice of the automatic call. So long as the depositary is the registered holder of the Notes, notice of the automatic call shall be deemed duly given upon receipt by the depositary. See

PS-10

“Description of Debt Securities—Depositary” in the accompanying general prospectus supplement for a description of how a notice of automatic call would be forwarded by the depositary.

All determinations made by the Calculation Agent, absent a determination of manifest error, will be conclusive for all purposes and binding on ML&Co. and the holders and beneficial owners of the Notes.

Events of Default and Acceleration

In case an Event of Default with respect to any Notes has occurred and is continuing, the amount payable to a holder of Notes upon any acceleration permitted by the Notes, with respect to each unit of Notes, will be equal to an amount as described under “—Payment on the Maturity Date” above, calculated as though the date of default were the maturity date for the Notes.

In case of default in payment of the Notes, whether on the stated maturity date, a Call Date or upon acceleration, from and after that date the Notes will bear interest, payable upon demand of their holders, at the then current Federal Funds Rate, reset daily, as determined by reference to Reuters page FEDFUNDS1 under the heading “EFFECT”, to the extent that payment of such interest shall be legally enforceable, on the unpaid amount due and payable on that date in accordance with the terms of the Notes to the date payment of that amount has been made or duly provided for. “Reuters page FEDFUNDS1” means such page or any successor page, or page on a successor service, displaying such rate. If the Federal Funds Rate cannot be determined by reference to Reuters page FEDFUNDS1, such rate will be determined in accordance with the procedures set forth in the accompanying MTN prospectus supplement relating to the determination of the Federal Funds Rate in the event of the unavailability of Moneyline Telerate page 120 (the predecessor of Reuters page FEDFUNDS1).

PS-11

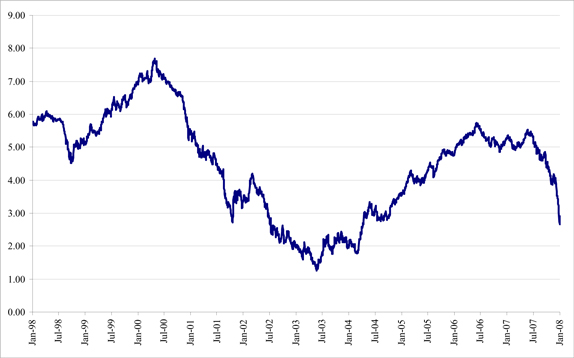

THE 2-YEAR U.S. DOLLAR CONSTANT MATURITY SWAP RATE

The 2-Year U.S. Dollar Constant Maturity Swap Rate is the constant maturity swap rate that measures the fixed rate legs of a hypothetical fixed-rate-for-floating rate swap transaction, where the fixed rate payment stream is reset each period relative to a regularly available fixed maturity market rate and is exchangeable for a floating 3-month LIBOR-based payment stream.

The following graph sets forth the daily levels of the 2-Year U.S. Dollar Constant Maturity Swap Rate for the period from January 23, 1998 to January 24, 2008. The historical data on the 2-Year U.S. Dollar Constant Maturity Swap Rate is not necessarily indicative of the future performance of the 2-Year U.S. Dollar Constant Maturity Swap Rate or what the value of the Notes may be. Any historical upward or downward trend in the level of the 2-Year U.S. Dollar Constant Maturity Swap Rate during any period set forth below is not an indication that the level of the 2-Year U.S. Dollar Constant Maturity Swap Rate is more or less likely to increase or decrease at any time over the term of the Notes. On January 24, 2008, the 2-Year U.S. Dollar Constant Maturity Swap Rate was 2.90%.

PS-12

UNITED STATES FEDERAL INCOME TAXATION

Set forth in full below is the opinion of Sidley Austin LLP, tax counsel to ML&Co., as to certain United States federal income tax consequences of the purchase, ownership and disposition of the Notes. This opinion is based upon laws, regulations, rulings and decisions now in effect, all of which are subject to change (including retroactive changes in effective dates) or possible differing interpretations. The discussion below supplements the discussion set forth under the section entitled “United States Federal Income Taxation” that is contained in the accompanying MTN prospectus supplement and supersedes that discussion to the extent that it contains information that is inconsistent with that which is contained in the accompanying MTN prospectus supplement. The discussion below deals only with Notes held as capital assets and does not purport to deal with persons in special tax situations, such as financial institutions, insurance companies, regulated investment companies, real estate investment trusts, dealers in securities or currencies, traders in securities that elect to mark to market, tax-exempt entities or persons holding Notes in a tax-deferred or tax-advantaged account (except to the extent specifically discussed below), persons whose functional currency is not the United States dollar, persons subject to the alternative minimum tax or persons holding Notes as a hedge against currency risks, as a position in a “straddle” or as part of a “hedging”, “conversion” or “integrated” transaction for tax purposes. It also does not deal with holders other than original purchasers (except where otherwise specifically noted in this pricing supplement). The following discussion also assumes that the issue price of the Notes, as determined for United States federal income tax purposes, equals the principal amount thereof. If a partnership holds the Notes, the tax treatment of a partner in the partnership will generally depend upon the status of the partner and the activities of the partnership. Thus, persons who are partners in a partnership holding the Notes should consult their own tax advisors. Moreover, all persons considering the purchase of the Notes should consult their own tax advisors concerning the application of the United States federal income tax laws to their particular situations as well as any consequences of the purchase, ownership and disposition of the Notes arising under the laws of any other taxing jurisdiction.

As used in this pricing supplement, the term “U.S. Holder” means a beneficial owner of a Note that is for United States federal income tax purposes (a) a citizen or resident of the United States, (b) a corporation, partnership or other entity treated as a corporation or a partnership that is created or organized in or under the laws of the United States, any state thereof or the District of Columbia (other than a partnership that is not treated as a United States person under any applicable Treasury regulations), (c) an estate the income of which is subject to United States federal income taxation regardless of its source, (d) a trust if a court within the United States is able to exercise primary supervision over the administration of the trust and one or more United States persons have the authority to control all substantial decisions of the trust or (e) any other person whose income or gain in respect of a Note is effectively connected with the conduct of a United States trade or business. Notwithstanding clause (d) of the preceding sentence, to the extent provided in Treasury regulations, certain trusts in existence on August 20, 1996, and treated as United States persons prior to that date that elect to continue to be treated as United States persons also will be U.S. Holders. As used herein, the term “non-U.S. Holder” means a beneficial owner of a Note that is not a U.S. Holder.

General

There are no statutory provisions, regulations, published rulings or judicial decisions addressing or involving the characterization, for United States federal income tax purposes, of the Notes or securities with terms substantially the same as the Notes. However, although the matter is not free from doubt, under current law, each Note should be treated as a debt instrument of ML&Co. for United States federal income tax purposes. ML&Co. currently intends to treat each Note as a debt instrument of ML&Co. for United States federal income tax purposes and, where required, intends to file information returns with the Internal Revenue Service (the “IRS”) in accordance with this treatment, in the absence of any change or clarification in the law, by regulation or otherwise, requiring a different characterization of the Notes. Prospective investors in the Notes should be aware, however, that the IRS is not bound by ML&Co.’s characterization of the Notes as indebtedness, and the IRS could possibly take a different position as to the proper characterization of the Notes for United States federal income tax purposes. The following discussion of the principal United States federal income tax consequences of the purchase, ownership and disposition of the Notes is based upon the assumption that each Note will be treated as a debt instrument of ML&Co. for United States federal income tax purposes. If the Notes are not in fact treated as debt instruments of ML&Co. for United States federal income tax purposes, then the United States federal income tax treatment of the purchase, ownership and disposition of the Notes could differ from the treatment discussed below with the result

PS-13

that the timing and character of income, gain or loss recognized in respect of a Note could differ from the timing and character of income, gain or loss recognized in respect of a Note had the Notes in fact been treated as debt instruments of ML&Co. for United States federal income tax purposes.

U.S. Holders

ML&Co. has determined that it is not significantly more likely than not that the Notes will be automatically called on any particular Call Date. Accordingly, ML&Co. and each holder or beneficial owner of a Note agree to treat the Notes as debt instruments that are subject to the final Treasury regulations (the “CPDI Regulations”) concerning the proper United States federal income tax treatment of contingent payment debt instruments. In general, the CPDI Regulations cause the timing and character of income, gain or loss reported on a contingent payment debt instrument to substantially differ from the timing and character of income, gain or loss reported on a conventional noncontingent payment debt instrument. Specifically, the CPDI Regulations generally require a U.S. Holder of such an instrument to include future contingent and noncontingent interest payments in income as that interest accrues based upon a projected payment schedule. Moreover, in general, under the CPDI Regulations, any gain recognized by a U.S. Holder on the sale, exchange, or retirement of a contingent payment debt instrument is treated as ordinary income, and all or a portion of any loss realized could be treated as ordinary loss as opposed to capital loss (depending upon the circumstances). The CPDI Regulations provide no definitive guidance as to whether or not an instrument is properly characterized as a debt instrument for United States federal income tax purposes.

In particular, solely for purposes of applying the CPDI Regulations to the Notes, ML&Co. has determined that the projected payment schedule for the Notes will consist of a payment on the maturity date equal to $ per unit (the “Projected Call Price”). This represents an estimated yield on the Notes equal to % per annum, compounded semi-annually. Accordingly, during the term of the Notes, a U.S. Holder of a Note will be required to include in income as ordinary interest an amount equal to the sum of the daily portions of interest on the Note that are deemed to accrue at this estimated yield for each day during the taxable year (or portion of the taxable year) on which the U.S. Holder holds the Note. The amount of interest that will be deemed to accrue in any accrual period (i.e., generally each one-month period during which the Notes are outstanding) will equal the product of this estimated yield (properly adjusted for the length of the accrual period) and the Note’s adjusted issue price (as defined below) at the beginning of the accrual period. The daily portions of interest will be determined by allocating to each day in the accrual period the ratable portion of the interest that is deemed to accrue during the accrual period. In general, for these purposes a Note’s adjusted issue price will equal the Note’s issue price (i.e., $1,000), increased by the interest previously accrued on the Note. At maturity of a Note, in the event that the actual amount payable at maturity (the “Maturity Payment”) exceeds $ per unit (i.e., the Projected Call Price), a U.S. Holder will be required to include the excess of the Maturity Payment over $ per unit (i.e., the Projected Call Price) in income as ordinary interest on the stated maturity date. Alternatively, in the event that the Maturity Payment is less than $ per unit (i.e., the Projected Call Price), the amount by which the Projected Call Price (i.e., per unit) exceeds the Maturity Payment will be treated first as an offset to any interest otherwise includible in income by the U.S. Holder with respect to the Note for the taxable year in which the stated maturity date occurs to the extent of the amount of that includible interest. Further, a U.S. Holder will be permitted to recognize and deduct, as an ordinary loss that is not subject to the limitations applicable to miscellaneous itemized deductions, any remaining portion of the Projected Call Price (i.e., per unit) in excess of the Maturity Payment that is not treated as an interest offset pursuant to the foregoing rules.

Upon the sale, exchange or redemption of a Note prior to the maturity date, a U.S. Holder will be required to recognize taxable gain or loss in an amount equal to the difference, if any, between the amount realized by the U.S. Holder upon that sale, exchange or redemption and the U.S. Holder’s adjusted tax basis in the Note as of the date of disposition. A U.S. Holder’s adjusted tax basis in a Note generally will equal the U.S. Holder’s initial investment in the Note increased by any interest previously included in income with respect to the Note by the U.S. Holder. Any taxable gain will be treated as ordinary income. Any taxable loss will be treated as ordinary loss to the extent of the U.S. Holder’s total interest inclusions on the Note. Any remaining loss generally will be treated as long-term or short-term capital loss (depending upon the U.S. Holder’s holding period for the Note as of the date of such sale, exchange or redemption). All amounts includible in income by a U.S. Holder as ordinary interest pursuant to the CPDI Regulations will be treated as original issue discount.

All prospective investors in the Notes should consult their own tax advisors concerning the application of the CPDI Regulations to their investment in the Notes. Investors in the Notes may obtain the projected payment

PS-14

schedule, as determined by ML&Co. for purposes of applying the CPDI Regulations to the Notes, by submitting a written request for that information to Merrill Lynch & Co., Inc., Corporate Secretary’s Office, 222 Broadway, 17th Floor, New York, New York 10038, (212) 670-0432, corporatesecretary@exchange.ml.com.

The projected payment schedule (including both the Projected Call Price and the estimated yield on the Notes) has been determined solely for United States federal income tax purposes (i.e., for purposes of applying the CPDI Regulations to the Notes), and is neither a prediction nor a guarantee of what the actual yield on the Notes will be or that the actual yield on the Notes will even exceed zero.

Hypothetical Table

The following table sets forth the amount of interest that would be deemed to have accrued with respect to each Note during each accrual period over an assumed term of three years for the Notes based upon a hypothetical projected payment schedule for the Notes (including both a hypothetical Projected Call Price and a hypothetical estimated yield equal to 3.78% per annum (compounded semi-annually)) as determined by ML&Co. for purposes of illustrating the application of the CPDI Regulations to the Notes as if the Notes had been issued on January 29, 2008 and were scheduled to mature on January 29, 2011. The following table is for illustrative purposes only. The actual projected payment schedule for the Notes (including both the actual Projected Call Price and the actual estimated yield) will be determined by ML&Co. in connection with the issuance of the Notes and will depend upon actual market interest rates (and thus ML&Co.’s borrowing costs for debt instruments with comparable maturities) at that time. The actual projected payment schedule for the Notes (including both the actual Projected Call Price and the actual estimated yield) and the actual tax accrual table will be set forth in the final pricing supplement delivered to investors in connection with the initial sale of the Notes.

| Accrual Period | Interest deemed to accrue on (per Unit) |

Total interest deemed to have accrued on Notes as of end of accrual period (per Unit) | ||

| January 29, 2008 through July 29, 2008 |

$18.90 | $18.90 | ||

| July 30, 2008 through January 29, 2009 |

$19.26 | $38.16 | ||

| January 30, 2009 through July 29, 2009 |

$19.62 | $57.78 | ||

| July 30, 2009 through January 29, 2010 |

$19.99 | $77.77 | ||

| January 30, 2010 through July 29, 2010 |

$20.37 | $98.14 | ||

| July 30, 2010 through January 29, 2011 |

$20.75 | $118.89 |

Hypothetical Projected Call Price = $1,118.89 per Unit.

Unrelated Business Taxable Income

Section 511 of the Internal Revenue Code of 1986, as amended (the “Code”), generally imposes a tax, at regular corporate or trust income tax rates, on the “unrelated business taxable income” of certain tax-exempt organizations, including qualified pension and profit sharing plan trusts and individual retirement accounts. In general, if the Notes are held for investment purposes, the amount of income or gain realized with respect to the Notes will not constitute unrelated business taxable income. However, if a Note constitutes debt-financed property (as defined in Section 514(b) of the Code) by reason of indebtedness incurred by a holder of a Note to purchase the Note, all or a portion of any income or gain realized with respect to such Note may be classified as unrelated business taxable income pursuant to Section 514 of the Code. Moreover, prospective investors in the Notes should be aware that whether or not any income or gain realized with respect to a Note which is owned by an organization that is generally exempt from U.S. federal income taxation pursuant to Section 501(a) of the Code constitutes unrelated business taxable income will depend upon the specific facts and circumstances applicable to such organization. Accordingly, any potential investors in the Notes that are generally exempt from U.S. federal income taxation pursuant to Section 501(a) of the Code are urged to consult with their own tax advisors concerning the U.S. federal income tax consequences to them of investing in the Notes.

PS-15

Non-U.S. Holders

A non-U.S. Holder will not be subject to United States federal income taxes on payments of principal, premium (if any) or interest (including original issue discount) on a Note, unless the non-U.S. Holder is a direct or indirect 10% or greater shareholder of ML&Co., a controlled foreign corporation related to ML&Co. or a bank receiving interest described in Section 881(c)(3)(A) of the Code. However, income allocable to non-U.S. Holders will generally be subject to annual tax reporting on IRS Form 1042-S. For a non-U.S. Holder to qualify for the exemption from taxation, any person, U.S. or foreign, that has control, receipt or custody of an amount subject to withholding, or who can disburse or make payments of an amount subject to withholding (the “Withholding Agent”) must have received a statement that (a) is signed by the beneficial owner of the Note under penalties of perjury, (b) certifies that the owner is a non-U.S. Holder and (c) provides the name and address of the beneficial owner. The statement may generally be made on IRS Form W-8BEN (or other applicable form) or a substantially similar form, and the beneficial owner must inform the Withholding Agent of any change in the information on the statement within 30 days of that change by filing a new IRS Form W-8BEN (or other applicable form). Generally, an IRS Form W-8BEN provided without a U.S. taxpayer identification number will remain in effect for a period starting on the date the form is signed and ending on the last day of the third succeeding calendar year, unless a change in circumstances makes any information on the form incorrect. If a Note is held through a securities clearing organization or certain other financial institutions, the organization or institution may provide a signed statement to the Withholding Agent. Under certain circumstances, the signed statement must be accompanied by a copy of the applicable IRS Form W-8BEN (or other applicable form) or the substitute form provided by the beneficial owner to the organization or institution.

Under current law, a Note will not be includible in the estate of a non-U.S. Holder unless the individual is a direct or indirect 10% or greater shareholder of ML&Co. or, at the time of the individual’s death, payments in respect of that Note would have been effectively connected with the conduct by the individual of a trade or business in the United States.

Backup withholding

Backup withholding at the applicable statutory rate of United States federal income tax may apply to payments made in respect of the Notes to registered owners who are not “exempt recipients” and who fail to provide certain identifying information (such as the registered owner’s taxpayer identification number) in the required manner. Generally, individuals are not exempt recipients, whereas corporations and certain other entities generally are exempt recipients. Payments made in respect of the Notes to a U.S. Holder must be reported to the IRS, unless the U.S. Holder is an exempt recipient or establishes an exemption. Compliance with the identification procedures described in the preceding section would establish an exemption from backup withholding for those non-U.S. Holders who are not exempt recipients.

In addition, upon the sale of a Note to (or through) a broker, the broker must withhold on the entire purchase price, unless either (a) the broker determines that the seller is a corporation or other exempt recipient or (b) the seller provides, in the required manner, certain identifying information (e.g., an IRS Form W-9) and, in the case of a non-U.S. Holder, certifies that the seller is a non-U.S. Holder (and certain other conditions are met). This type of sale must also be reported by the broker to the IRS, unless either (a) the broker determines that the seller is an exempt recipient or (b) the seller certifies its non-U.S. status (and certain other conditions are met). Certification of the registered owner’s non-U.S. status would be made normally on an IRS Form W-8BEN (or other applicable form) under penalties of perjury, although in certain cases it may be possible to submit other documentary evidence.

Any amounts withheld under the backup withholding rules from a payment to a beneficial owner would be allowed as a refund or a credit against the beneficial owner’s United States federal income tax provided the required information is furnished to the IRS.

PS-16

Each fiduciary of a pension, profit-sharing or other employee benefit plan subject to the Employee Retirement Income Security Act of 1974, as amended (“ERISA”) (a “Plan”), should consider the fiduciary standards of ERISA in the context of the Plan’s particular circumstances before authorizing an investment in the Notes. Accordingly, among other factors, the fiduciary should consider whether the investment would satisfy the prudence and diversification requirements of ERISA and would be consistent with the documents and instruments governing the Plan.

In addition, we and certain of our subsidiaries and affiliates, including MLPF&S, may be each considered a party in interest within the meaning of ERISA, or a disqualified person within the meaning of the Internal Revenue Code of 1986, as amended (the “Code”), with respect to many Plans, as well as many individual retirement accounts and Keogh plans (also “Plans”). Prohibited transactions within the meaning of ERISA or the Code would likely arise, for example, if the securities are acquired by or with the assets of a Plan with respect to which MLPF&S or any of its affiliates is a party in interest, unless the securities are acquired pursuant to an exemption from the prohibited transaction rules. A violation of these prohibited transaction rules could result in an excise tax or other liabilities under ERISA and/or Section 4975 of the Code for such persons, unless exemptive relief is available under an applicable statutory or administrative exemption.

Under ERISA and various prohibited transaction class exemptions (“PTCEs”) issued by the U.S. Department of Labor, exemptive relief may be available for direct or indirect prohibited transactions resulting from the purchase, holding or disposition of the securities. Those exemptions are PTCE 96-23 (for certain transactions determined by in-house asset managers), PTCE 95-60 (for certain transactions involving insurance company general accounts), PTCE 91-38 (for certain transactions involving bank collective investment funds), PTCE 90-1 (for certain transactions involving insurance company separate accounts), PTCE 84-14 (for certain transactions determined by independent qualified asset managers), and the exemption under new Section 408(b)(17) of ERISA and new Section 4975(d)(20) of the Code for certain arm’s-length transactions with a person that is a party in interest solely by reason of providing services to Plans or being an affiliate of such a service provider (the “Service Provider Exemption”).

Because we may be considered a party in interest with respect to many Plans, the securities may not be purchased, held or disposed of by any Plan, any entity whose underlying assets include plan assets by reason of any Plan’s investment in the entity (a “Plan Asset Entity”) or any person investing plan assets of any Plan, unless such purchase, holding or disposition is eligible for exemptive relief, including relief available under PTCE 96-23, 95-60, 91-38, 90-1, or 84-14 or the Service Provider Exemption, or such purchase, holding or disposition is otherwise not prohibited. Any purchaser, including any fiduciary purchasing on behalf of a Plan, transferee or holder of the securities will be deemed to have represented, in its corporate and its fiduciary capacity, by its purchase and holding of the securities that either (a) it is not a Plan or a Plan Asset Entity and is not purchasing such securities on behalf of or with plan assets of any Plan or with any assets of a governmental, church or foreign plan that is subject to any federal, state, local or foreign law that is substantially similar to the provisions of Section 406 of ERISA or Section 4975 of the Code or (b) its purchase, holding and disposition are eligible for exemptive relief or such purchase, holding and disposition are not prohibited by ERISA or Section 4975 of the Code (or in the case of a governmental, church or foreign plan, any substantially similar federal, state, local or foreign law).

Under ERISA, assets of a Plan may include assets held in the general account of an insurance company which has issued an insurance policy to such plan or assets of an entity in which the Plan has invested. Accordingly, insurance company general accounts that include assets of a Plan must ensure that one of the foregoing exemptions is available. Due to the complexity of these rules and the penalties that may be imposed upon persons involved in non-exempt prohibited transactions, it is particularly important that fiduciaries or other persons considering purchasing the securities on behalf of or with “plan assets” of any Plan consult with their counsel regarding the availability of exemptive relief under PTCE 96-23, 95-60, 91-38, 90-1 or 84-14 or the Service Provider Exemption.

Purchasers of the securities have exclusive responsibility for ensuring that their purchase, holding and disposition of the securities do not violate the prohibited transaction rules of ERISA or the Code or any similar regulations applicable to governmental or church plans, as described above.

PS-17

The net proceeds from the sale of the Notes will be used as described under “Use of Proceeds” in the accompanying general prospectus supplement and to hedge market risks of ML&Co. associated with its obligations in connection with the Notes.

SUPPLEMENTAL PLAN OF DISTRIBUTION

MLPF&S has advised ML&Co. that it proposes initially to offer all or part of the Notes directly to the public on a fixed price basis at the offering price set forth on the cover page of this pricing supplement. After the initial public offering, the public offering price may be changed. The obligations of MLPF&S are subject to certain conditions and it is committed to take and pay for all of the Notes if any are taken.

If you place an order to purchase these offered securities, you are consenting to each of MLPF&S and its broker-dealer affiliate, First Republic Securities Company, LLC, acting as a principal in effecting the transaction for your account. MLPF&S is acting as an underwriter and/or selling agent for this offering and will receive underwriting compensation from the issuer of the securities.

MLPF&S and First Republic Securities Company, LLC, each a broker-dealer subsidiary of ML&Co., is a member of the Financial Industry Regulatory Authority, Inc. (formerly the National Association of Securities Dealers, Inc. (the “NASD”)) and will participate in distribution of the notes. Accordingly, offerings of the notes will conform to the requirements of NASD Rule 2720.

MLPF&S and First Republic Securities Company, LLC may use this Note Prospectus for offers and sales in secondary market transactions and market-making transactions in the Notes but are not obligated to engage in such secondary market transactions and/or market-making transactions. MLPF&S and First Republic Securities Company, LLC may act as principal or agent in these transactions, and the sales will be made at prices related to prevailing market prices at the time of the sale.

The consolidated financial statements and management’s report on the effectiveness of internal control over financial reporting, included as Exhibit 99.1 in the Current Report on Form 8-K dated November 13, 2007 (“November 13, 2007 Form 8-K”) and the related financial statement schedule included in ML&Co.’s Form 10-K for the year ended December 29, 2006 are incorporated in this pricing supplement by reference, and have been audited by Deloitte & Touche LLP, an independent registered public accounting firm, as stated in their reports, which are incorporated herein by reference (which reports (1) express an unqualified opinion on the consolidated financial statements and the related financial statement schedule and include an explanatory paragraph regarding the change in accounting method in 2006 for share-based payments to conform to Statement of Financial Accounting Standard No. 123 (revised 2004), Share-Based Payment, (2) express an unqualified opinion on management’s assessment regarding the effectiveness of internal control over financial reporting, and (3) express an unqualified opinion on the effectiveness of internal control over financial reporting), and have been so incorporated in reliance upon the reports of such firm given upon their authority as experts in accounting and auditing.

With respect to the unaudited condensed consolidated interim financial information for the three-month periods ended March 30, 2007 and March 31, 2006, the three-month and six-month periods ended June 29, 2007 and June 30, 2006, and the three-month and nine-month periods ended September 28, 2007 and September 29, 2006 which is incorporated herein by reference, Deloitte & Touche LLP, an independent registered public accounting firm, have applied limited procedures in accordance with the standards of the Public Company Accounting Oversight Board (United States) for a review of such information. However, as stated in their reports for the quarters ended March 30, 2007, included as Exhibit 99.3 in the November 13, 2007 Form 8-K, June 29, 2007, included as Exhibit 99.2 in the November 13, 2007 Form 8-K, and September 28, 2007 included in ML&Co.’s Quarterly Reports on Form 10-Q (which reports include an explanatory paragraph regarding the adoption of Statement of Financial Accounting Standards No. 157, “Fair Value Measurement”, Statement of Financial Accounting Standards No. 159, “The Fair Value Option for Financial Assets and Financial Liabilities—Including an amendment of FASB Statement No. 115,” and FASB Interpretation No. 48, “Accounting for Uncertainty in Income Taxes, an

PS-18

Interpretation of FASB Statement No. 109”) and incorporated by reference herein, they did not audit and they do not express an opinion on that interim financial information. Accordingly, the degree of reliance on their reports on such information should be restricted in light of the limited nature of the review procedures applied. Deloitte & Touche LLP are not subject to the liability provisions of Section 11 of the Securities Act of 1933 (the “Act”) for their reports on the unaudited condensed consolidated interim financial information because those reports are not “reports” or a “part” of the registration statement prepared or certified by an accountant within the meaning of Sections 7 and 11 of the Act.

PS-19

INDEX OF CERTAIN DEFINED TERMS

| Business Day |

PS-4 | |

| Call Date |

PS-4 | |

| Call Price |

PS-4 | |

| Notes |

PS-1 | |

| Observation Date |

PS-4 | |

| Pricing Date |

PS-3 | |

| Strike Rate |

PS-4 | |

| 2-Year U.S. Dollar Constant Maturity Swap Rate |

PS-3 |

Capitalized terms used in this pricing supplement and not otherwise defined shall have the meanings ascribed to them in the accompanying MTN prospectus supplement, general prospectus supplement and prospectus, as applicable.

PS-20

Units

Merrill Lynch & Co., Inc.

Medium-Term Notes, Series C

100% Principal Protected Auto-Callable Notes

Linked to the 2-Year U.S. Dollar Constant Maturity Swap Rate

due February , 2011

(the “Notes”)

$1,000 original public offering price per unit

|

PRICING SUPPLEMENT

|

Merrill Lynch & Co.

February , 2008