Filed Pursuant to Rule 424(b)(3)

Registration No. 333-132911

The Notes will have the terms specified in this term sheet as supplemented by the documents indicated herein under “Additional Note Terms” (together the “Note Prospectus”). Investing in the Notes involves a number of risks. See “ Risk Factors” and “Additional Risk Factors” on page TS-5 of this term sheet and beginning on page PS-4 of product supplement ARN-4.

In connection with this offering, each of Merrill Lynch, Pierce, Fenner & Smith Incorporated and its broker-dealer affiliate First Republic Securities Company, LLC is acting in its capacity as a principal.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this Note Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Unit | Total | |||

| Public offering price (1) |

$10.00 | $18,500,00 | ||

| Underwriting discount (1) |

$.20 | $370,000 | ||

| Proceeds, before expenses, to Merrill Lynch & Co., Inc. |

$9.80 | $18,130,000 |

| (1) | The public offering price and underwriting discount for any purchase of 500,000 units or more in a single transaction by an individual investor will be $9.95 per unit and $.15 per unit, respectively. |

“Accelerated Return NotesSM” is a service mark of Merrill Lynch & Co., Inc.

“ARNs®” is a registered service mark of Merrill Lynch & Co., Inc.

“WilderHill New Energy Global Innovation Index” and “NEX” are trade marks of WilderHill New Energy Finance LLC, and have been licensed for use by Merrill Lynch & Co.

Merrill Lynch & Co.

March 27, 2008

Summary

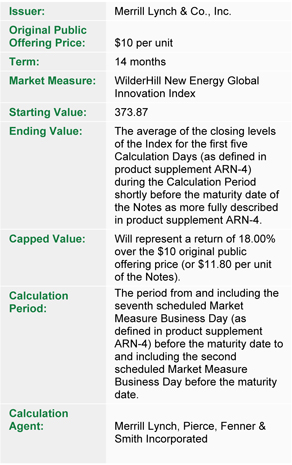

The Accelerated Return Notes Linked to the WilderHill New Energy Global Innovation Index due June 3, 2009 (the “Notes”) are senior, unsecured debt securities of Merrill Lynch & Co., Inc. that provide a leveraged return for investors, subject to a cap, if the level of the WilderHill New Energy Global Innovation Index (the “Index”) increases moderately from the Starting Value of the Index, determined on March 27, 2008, the date the Notes were priced for initial sale to the public (the “Pricing Date”), to the Ending Value of the Index, determined on Calculation Days shortly prior to the maturity date of the Notes. Investors must be willing to forego interest payments on the Notes and willing to accept a return that is capped or a repayment that is less, and potentially significantly less, than the original public offering price of the Notes.

| Terms of the Notes | Determining Payment at Maturity for the Notes | |

|

| |

TS-2

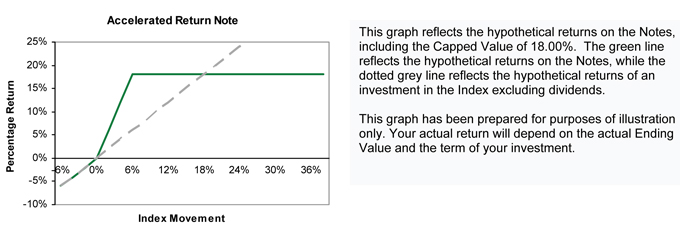

Hypothetical Payout Profile

|

Hypothetical Payments at Maturity

Examples

Set forth below are three examples of payment at maturity calculations, reflecting the Starting Value of 373.87 and the Capped Value of $11.80.

Example 1—The hypothetical Ending Value is 80% of the Starting Value:

Starting Value: 373.87

Hypothetical Ending Value: 299.10

| $10 × |

( | 299.10

|

) | = $ | 8.00 | ||||||

|

373.87 |

Payment at maturity (per unit) = $8.00

Example 2—The hypothetical Ending Value is 103% of the Starting Value:

Starting Value: 373.87

Hypothetical Ending Value: 385.09

| $10 + |

( | $ | 30 | × | ( | 385.09 - 373.87

|

) | ) | = $ | 10.90 | |||||||||

|

373.87 |

Payment at maturity (per unit) = $10.90

Example 3—The hypothetical Ending Value is 120% of the Starting Value:

Starting Value: 373.87

Hypothetical Ending Value: 448.64

| $10 + |

( | $ | 30 | × | ( | 448.64 - 373.87

|

) | ) | = $ | 16.00 | |||||||||

|

373.87 |

Payment at maturity (per unit) = $11.80 (Payment at maturity cannot be greater than the Capped Value)

TS-3

The following table illustrates, for the Starting Value of 373.87 and a range of hypothetical Ending Values of the Index:

| § | the percentage change from the Starting Value to the hypothetical Ending Value; |

| § | the total amount payable on the maturity date per unit; |

| § | the total rate of return to holders of the Notes; |

| § | the pretax annualized rate of return to holders of the Notes; and |

| § | the pretax annualized rate of return of a hypothetical investment in the stocks included in the Index, which includes an assumed aggregate dividend yield of 1.010% per annum, as more fully described below. |

The table below reflects the Capped Value of $11.80.

| Hypothetical Ending Value |

Percentage change to the hypothetical Ending Value |

Total amount payable on the maturity date per unit |

Total rate of return on the Notes |

Pretax annualized rate of return on the Notes (1) |

Pretax annualized rate of return of the stocks included in the Index (1)(2) | |||||

| 186.94 |

-50.00% | $5.00 | -50.00% | -51.40% | -50.20% | |||||

| 224.32 |

-40.00% | $6.00 | -40.00% | -39.32% | -38.19% | |||||

| 261.71 |

-30.00% | $7.00 | -30.00% | -28.35% | -27.26% | |||||

| 299.10 |

-20.00% | $8.00 | -20.00% | -18.24% | -17.18% | |||||

| 336.48 |

-10.00% | $9.00 | -10.00% | -8.83% | -7.80% | |||||

| 343.96 |

-8.00% | $9.20 | -8.00% | -7.02% | -5.99% | |||||

| 351.44 |

-6.00% | $9.40 | -6.00% | -5.23% | -4.21% | |||||

| 358.92 |

-4.00% | $9.60 | -4.00% | -3.47% | -2.45% | |||||

| 366.39 |

-2.00% | $9.80 | -2.00% | -1.72% | -0.71% | |||||

| 373.87 (3) |

0.00% | $10.00 | 0.00% | 0.00% | 1.01% | |||||

| 381.35 |

2.00% | $10.60 | 6.00% | 5.06% | 2.71% | |||||

| 388.82 |

4.00% | $11.20 | 12.00% | 9.95% | 4.40% | |||||

| 396.30 |

6.00% | $11.80 (4) | 18.00% | 14.70% | 6.06% | |||||

| 403.78 |

8.00% | $11.80 | 18.00% | 14.70% | 7.71% | |||||

| 411.26 |

10.00% | $11.80 | 18.00% | 14.70% | 9.33% | |||||

| 448.64 |

20.00% | $11.80 | 18.00% | 14.70% | 17.24% | |||||

| 486.03 |

30.00% | $11.80 | 18.00% | 14.70% | 24.78% |

| (1) | The annualized rates of return specified in this column are calculated on a semiannual bond equivalent basis and assume an investment term from April 3, 2008 to June 3, 2009, the term of the Notes. |

| (2) | This rate of return assumes: |

| (a) | a percentage change in the aggregate price of the stocks included in the Index that equals the percentage change in the level of the Index from the Starting Value to the relevant hypothetical Ending Value; |

| (b) | a constant dividend yield of 1.010% per annum, paid quarterly from the date of initial delivery of the Notes, applied to the level of the Index at the end of each quarter assuming this value increases or decreases linearly from the Starting Value to the applicable hypothetical Ending Value; and |

| (c) | no transaction fees or expenses. |

| (3) | This is the Starting Value. |

| (4) | The total amount payable on the maturity date per unit of the Notes cannot exceed the Capped Value of $11.80. |

The above figures are for purposes of illustration only. The actual amount you receive and the resulting total and pretax annualized rates of return will depend on the actual Ending Value and the term of your investment.

TS-4

An investment in the Notes involves significant risks. The following is a list of certain of the risks involved in investing in the Notes. You should carefully review the more detailed explanation of risks relating to the Notes in the “Risk Factors” sections included in the product supplement and MTN prospectus supplement identified below under “Additional Note Terms”. We also urge you to consult your investment, legal, tax, accounting and other advisers before you invest in the Notes.

| § | Your investment may result in a loss. |

| § | Your yield may be lower than the yield on other debt securities of comparable maturity. |

| § | You must rely on your own evaluations regarding the merits of an investment linked to the Index. |

| § | Your return is limited and may not reflect the return on a direct investment in the stocks included in the Index. |

| § | You will not have the right to receive cash dividends or exercise ownership rights with respect to the stocks included in the Index. |

| § | Your return may be affected by factors affecting international securities markets. |

| § | Exchange rate movements may impact the value of the Notes. |

| § | In seeking to provide investors with what we believe to be commercially reasonable terms for the Notes while providing MLPF&S with compensation for its services, we have considered the costs of developing, hedging and distributing the Notes. If a trading market develops for the Notes (and such a market may not develop), these costs are expected to affect the market price you may receive or be quoted for your Notes on a date prior to the stated maturity date. |

| § | The publisher of the Index may adjust the Index in a way that affects its level, and such publisher has no obligation to consider your interests. |

| § | Many factors affect the trading value of the Notes; these factors interrelate in complex ways and the effect of any one factor may offset or magnify the effect of another factor. |

| § | Purchases and sales of the stocks underlying the Index by us and our affiliates may affect your return. |

| § | Potential conflicts of interest could arise. |

| § | Tax consequences are uncertain. |

Additional Risk Factors

The stocks included in the Index are concentrated in one industry. All of the stocks included in the Index (each an “Index Component” and together, the “Index Components”) are issued by companies concentrated in wind, solar, biofuels, hydro, wave and tidal, geothermal and other relevant renewable energy businesses, as well as energy conversion, storage, conservation, efficiency, materials, pollution control, emerging hydrogen and fuel cells. As a result, the Index Components that will determine the performance of the Notes are concentrated in one industry. Although an investment in the Notes will not give holders any ownership or other direct interests in the Index Components, the return on an investment in the Notes will be subject to certain risks associated with direct equity investments in the renewable energy sector.

The Index is not necessarily representative of the renewable energy sector. While the Index Components are common stocks of companies generally considered to be involved in various segments of the renewable energy sector, the Index Components and the Index may not necessarily follow the price movements of the entire renewable energy sector generally. If the Index Components decline in value, the Index will decline in value even if common stock prices in the renewable energy sector generally increase in value.

Investor Considerations

TS-5

Other Provisions

We may deliver the Notes against payment therefor in New York, New York on a date that is greater than three business days following the Pricing Date. Under Rule 15c6-1 of the Securities Exchange Act of 1934, trades in the secondary market generally are required to settle in three business days, unless the parties to any such trade expressly agree otherwise. Accordingly, if the initial settlement on the Notes occurs more than three business days from the Pricing Date, purchasers who wish to trade Notes more than three business days prior to the original issue date will be required to specify alternative settlement arrangements to prevent a failed settlement.

If you place an order to purchase these offered securities, you are consenting to each of MLPF&S and its broker-dealer affiliate First Republic Securities Company LLC, acting as a principal in effecting the transaction for your account. MLPF&S is acting as an underwriter and/or selling agent for this offering and will receive underwriting compensation from the issuer of the securities.

Supplement to the Plan of Distribution

MLPF&S and First Republic Securities Company, LLC, each a broker-dealer subsidiary of ML&Co., are members of the Financial Industry Regulatory Authority, Inc. (formerly the National Association of Securities Dealers, Inc. (the “NASD”)) and will participate in the distribution of the Notes. Accordingly, offerings of the Notes will conform to the requirements of NASD Rule 2720.

MLPF&S and First Republic Securities Company, LLC may use this Note Prospectus for offers and sales in secondary market transactions and market-making transactions in the Notes but are not obligated to engage in such secondary market transactions and/or market-making transactions. MLPF&S and First Republic Securities Company, LLC may act as principal or agent in these transactions, and any such sales will be made at prices related to prevailing market prices at the time of the sale.

TS-6

The Index

All disclosure in this term sheet regarding the Index, including without limitation, its make-up, method of calculation and changes in its components, is derived from public information made available by WilderHill New Energy Finance, LLC (the “Index Publisher”). This information reflects the policies of the Index Publisher and is subject to change by the Index Publisher at its discretion. The Index Publisher has no obligation to continue to publish, and may discontinue publication of, the Index.

The index constituents (“Index Components”) are generally companies around the world whose innovative technologies focus on generation and use of cleaner energy, conservation, efficiency, and advancement of renewable energy in general. The Index Components are also mainly companies worldwide focused in wind, solar, biofuels, hydro, wave and tidal, geothermal and other relevant renewable energy businesses, as well as energy conversion, storage, conservation, efficiency, materials, pollution control, emerging hydrogen and fuel cells. As of December 31, 2007, there were 86 stocks underlying the Index, as set forth in Annex A.

The Index was created by, and is a service mark of the Index Publisher and is calculated by Dow Jones Indexes (the “Index Calculation Agent”).

Eligibility Criteria

To adequately reflect the worldwide nature of the emerging lower-carbon sector, in general at least half of the companies comprising the Index are listed on stock exchanges outside the United States.

For a stock to be included in the selection universe, the company must be identified as one that has a meaningful exposure to clean energy, either as a technology, equipment, service or finance provider, such that profitable growth of the industry can be expected to have a positive impact on that company’s performance. Generally, meaningful exposure is taken to mean that the company derives at least 10% of its market value from activities in clean energy, in the judgment of the Index Publisher.

Stock selection for the Index is biased in favor of the “purer-play” companies in renewable energy and those in cleaner energy generally. “Purer-play” in this context means those that, as estimated by the Index Publisher, derive more than 50% of their market value from their clean energy activities. Consequently, and owing to the fact that the clean energy industry is in the early stages of its growth cycle, the smaller-cap and mid-cap companies may have a leading role in the composition of the Index. As new energy technologies are developed, these may be added to the Index when significant to the sector.

Larger companies with diversified (including business lines outside clean energy) businesses may be included, but will only be considered in the following circumstances, if in the opinion of the Index Publisher:

• Clean energy is a rapidly growing part of the business and is estimated to account for above 10% of the market value of the company.

• The company is already or closely positioned to be the dominant market player in the specific sector of the clean energy industry that it is operating in.

• The company is one of the very few quoted companies that offer exposure to a specific sector that has been chosen as an area of the clean energy industry to reflect the Index.

However, the number of conglomerates will be capped to be less than 20% of the Index by component count.

The Index will not include the stocks of funds investing in quoted equities, as these can themselves qualify for direct inclusion in the Index. The Index may, however, include the stocks of companies or funds whose main activity is investing in or holding portfolios of renewable energy generating capacity or other infrastructure, as long as they meet the other criteria for inclusion. It may also include companies or quoted funds that invest in privately-held equity of qualifying companies.

Liquidity and Trading Status

To be included in the Index, Index Components must meet the following criteria relating to liquidity and trading status:

i. Listing on a National Exchange or Primary Listing Market

Each Index Component will be listed on a major international or national exchange: the NYSE, AMEX or NASDAQ in the USA; in Europe one of the major exchanges such as London, Paris (Euronext), Madrid, Frankfurt (XETRA) or Copenhagen; in Asia these may include, but not be limited to the Australian Stock Exchange (ASX), Tokyo, Hong Kong, Shanghai, Shenzhen, Mumbai and the National Stock Exchange of India. Where an additional or secondary listing on a major international market is available (e.g. ADRs and GDRs) and the Index Publisher determines such listing offers more attractive trading characteristics than the main listing on a domestic market, exposure to the company through the additional or secondary listing will be considered by the Index Publisher. Listing on bulletin-board or over-the-counter exchanges is not considered for inclusion in the Index.

ii. Three-month average market capitalization is at least $100 million

Each Index Component will have three-month average market capitalization of at least $100 million. Market capitalization is measured by the Index Publisher over the preceding 3-month period, and the average of the closing market capitalization on each trading day of that 3-month period is taken into account. The measurement period of 3 months may be reduced if a company has a trading history of less than 3 months, as typically encountered in the case of new IPOs. Market capitalization for a majority of Index Components is typically above $250 million. To account for the notable but smaller companies sometimes significant to the clean energy field, as determined by the Index Publisher, a minority of Index Components may have market capitalizations between $100 million and $250 million.

iii. Significant trading volume

Each Index Component will have a minimum average daily trading volume of $1,000,000 over the preceding 30 days. In addition, at least 250,000 shares of each Index Component were traded each of the last 6 months. Newly IPO’d stocks may be included, but will only be considered in certain circumstances. For stocks quoted on US exchanges strong preference is given to stocks with a price of over $3.00 per share. In exceptional circumstances, as determined by the Index Publisher, prices of between $1.00 and $3.00 may be considered.

TS-7

A small number of Index Components may at any time not meet these criteria.

The Index Publisher will have complete discretion over which companies are included in the Index, their weightings, and the definitions and weightings of the sectors. The Index Publisher may at any time and from time to time, change the number of Index Components by adding or deleting one or more Index Components, or replacing one or more Index Components with one or more substitute stocks of its choice, if in Index Publisher’s opinion such addition, deletion or substitution is necessary or appropriate to maintain the quality and/or character of the industry groups to which the Index relates.

Index Methodology

The Index is calculated using a modified equal-dollar weighting methodology. At the time of rebalancing each Index Sector (as defined below) is assigned an overall weight in line with that sector’s market capitalization within the Index’s component selection universe, adjusted if necessary by the Index Publisher to avoid problems of illiquidity or over-concentration on any individual sector.

Each sector’s components are divided into two categories, large and small. Large components are given three and half times the weight of small components within their sector, and are defined as having an individual market capitalization of over $750 million. Index Components may be reassigned between large and small categories within their relevant sectors at the discretion of the Index Publisher in order to alleviate concerns of individual Index Component liquidity or restricted availability. Index Components quoted on those markets that restrict ownership or trading by foreign investors will not be excluded altogether but may be allocated to the small component category within their respective sectors. All Index Components are limited individually to five percent (5%) of the Index by weight at rebalancing notwithstanding any other rules. As of April 1, 2007, China and India impose certain restrictions on foreign ownership and trading which could affect the composition of the Index.

Index Sectors

The Index is made up of companies active in the following seven Sectors:

1. Renewables - Wind

2. Renewables - Solar

3. Renewables - Biofuels & Biomass

4. Renewables - Other

5. Hydrogen & Fuel Cells

6. Power Storage

7. Energy Efficiency

Index Rebalancing

The Index is rebalanced on the last business day of March, June, September and December. Changes to the Index composition typically take effect after the close of trading on the next to last business day of each calendar quarter (“Rebalance Date”). The Index Components will be determined and announced at the close of trading two days prior to the Rebalance Date.

After the Stock Selection Committee (as defined below) meeting for each quarterly rebalancing, the Index Publisher will provide to the Index Calculation Agent the Index Components with determined additions and/or removals as well as sector weights and other related changes for the next quarter at least five business days prior to the Rebalance Date.

The Index divisor was initially determined to yield a benchmark value of 100.00 at the close of trading, December 30, 2002. At each quarterly rebalancing, each Index Component’s index weight is determined and then floats over that quarter according to share price. The individual weights float (are rebased) from one trading day to the next as follows:

The new weight is obtained by dividing the value represented by that specific Index Component (its index shares multiplied by its share price at the end of the trading day) by the total value of the Index at the end of the same trading day. The new weight is applied to the open share prices of the Index Components on the next trading day.

Corporate Actions

The Index Publisher may substitute Index Components or change the number of issues included in the Index, based on changing conditions in the industry or in the event of certain types of corporate actions, including mergers, acquisitions, spin-offs, and reorganizations subject to eligibility requirements as defined below.

In the event of Index Component or share weight changes to the Index, the payment of dividends other than ordinary cash dividends, spin-offs, rights offerings, re-capitalization, or other corporate actions affecting an Index Component; the Index divisor may be adjusted to ensure that there are no changes to the Index level as a result of non-market forces.

Mergers and acquisitions

Surviving Index Components are reviewed for eligibility by the Index Publisher. In the event of a merger between two components, the share weight of the surviving entity may be adjusted to account for any shares issued in the acquisition.

| • | Spin-offs and reorganizations |

Each corporate action is reviewed by the Index Publisher to determine if the resulting securities are eligible for continued inclusion.

| • | Share issuance or buybacks |

The Index is not adjusted for changes in shares outstanding.

TS-8

| • | IPOs |

IPOs in-between the quarterly reviews can be included in the Index at the next rebalancing.

| • | Stock Splits |

Stock splits and stock dividends are determined by the Index Publisher to be routine actions and shall result in no impact to the Index level.

| • | Stock Deletion |

If any of the corporate events result in a stock being removed from the Index (a “Deleted Component”) such Deleted Component will not be replaced until the next Rebalancing Date. The weight of the Deleted Component will be redistributed to the remaining Index Components amongst their respective weights upon the ex-date of the deletion.

| • | Special Dividends |

Special dividends, non-routine dividend payments and return of capital distributions will cause a price adjustment and divisor change on ex-date resulting in reinvestment of the distribution across the Index.

| • | Bankruptcies |

If the company underlying an Index Component has filed for bankruptcy, the Index Component will be a Deleted Component. The weight of the Deleted Component will be redistributed to the remaining Index Components amongst their respective weights upon the ex-date of the bankruptcy.

Governance

The Index is managed by the Index Publisher with input from the following two bodies:

| • | An Advisory Board, made up of prominent individuals from the worlds of finance, climate science, technology, politics and communications, which is responsible for devising an overall strategy for the Index. |

| • | A Stock Selection Committee, made up of individuals with knowledge of companies and markets that make up the clean energy industry, which is responsible for day-to-day management of the Index and quarterly rebalancings. |

Index Dissemination

The closing value of the Index is calculated on a 24-hour day that ends at 5:30 PM New York time. The end-of-day Index calculations uses WM closing spot exchange rates as of 4 PM London time and each Index Component’s closing price on its primary market.

Whenever practical, in conjunction with the Index Publisher, the Calculation Agent will pre-announce stock additions and/or deletions as well as certain Index share weight changes at least two trading days prior to the Rebalance Date.

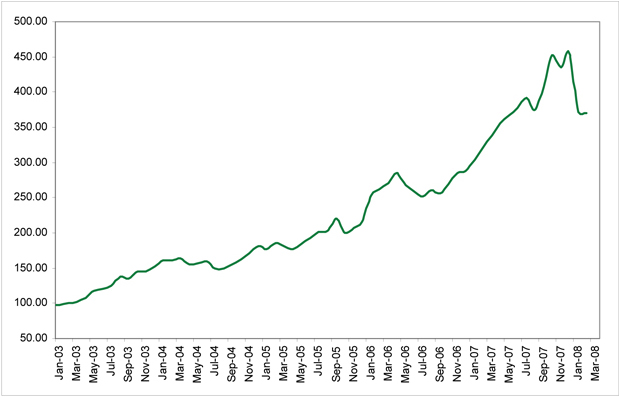

The following graph sets forth the historical performance of the Index in the period from January 2003 through February 2008. This historical data on the Index is not necessarily indicative of the future performance of the Index or what the value of the Notes may be. Any historical upward or downward trend in the level of the Index during any period set forth below is not an indication that the Index is more or less likely to increase or decrease at any time over the term of the Notes. On the Pricing Date, the closing level of the Index was 373.87.

TS-9

Disclaimer

WilderHill New Energy Global Innovation Index (the “NEX”) is published by WilderHill New Energy Finance LLC and is calculated by Dow Jones Indexes, a business unit of Dow Jones & Company, Inc. (“Dow Jones”). The “Accelerated Return Notes Linked to the WilderHill New Energy Global Innovation Index” based on the NEX, are not sponsored, endorsed, sold or promoted by WilderHill New Energy Finance LLC or Dow Jones Indexes, and WilderHill New Energy Finance LLC and Dow Jones Indexes make no representation regarding the advisability of investing in such product(s).

WilderHill New Energy Finance, LLC, its affiliates, sources and distribution agents (collectively, the “Index Publisher”) and Dow Jones, its affiliates, sources and distribution agents (collectively, the “Index Calculation Agent”) shall not be liable to ML&Co., any customer or any third party for any loss or damage, direct, indirect or consequential, arising from (i) any inaccuracy or incompleteness in, or delays, interruptions, errors or omissions in the delivery of the NEX or any data related thereto (the “Index Data”) or (ii) any decision made or action taken by ML&Co., any customer or third party in reliance upon the Index Data. The Index Publisher and the Index Calculation Agent do not make any warranties, express or implied, to ML&Co., any of its customers or any one else regarding the Index Data, including, without limitation, any warranties with respect to the timeliness, sequence, accuracy, completeness, currentness, merchantability, quality or fitness for a particular purpose or any warranties as to the results to be obtained by ML&Co., any of its customers or other person in connection with the use of the Index Data. The Index Publisher and the Index Calculation Agent shall not be liable to ML&Co., its customers or other third parties for loss of business revenues, lost profits or any indirect, consequential, special or similar damages whatsoever, whether in contract, tort or otherwise, even if advised of the possibility of such damages.

TS-10

Certain U.S. Federal Income Taxation Considerations

Set forth below is a summary of certain U.S. federal income tax considerations relating to an investment in the Notes. The following summary is not complete and is qualified in its entirety by the discussion under the section entitled “United States Federal Income Taxation” in the accompanying product supplement ARN-4 and MTN prospectus supplement, which you should carefully review prior to investing in the Notes.

General. There are no statutory provisions, regulations, published rulings or judicial decisions addressing or involving the characterization and treatment, for United States federal income tax purposes, of the Notes or securities with terms substantially the same as the Notes. Accordingly, the proper United States federal income tax characterization and treatment of the Notes is uncertain. Pursuant to the terms of the Notes, ML&Co. and every holder of a Note agree (in the absence of an administrative determination, judicial ruling or other authoritative guidance to the contrary) to characterize and treat a Note for all tax purposes as a pre-paid cash-settled forward contract linked to the level of the Index. Due to the absence of authorities that directly address instruments that are similar to the Notes, significant aspects of the United States federal income tax consequences of an investment in the Notes are not certain, and no assurance can be given that the Internal Revenue Service (the “IRS”) or the courts will agree with the characterization and tax treatment described above. Accordingly, prospective purchasers are urged to consult their own tax advisors regarding the United States federal income tax consequences of an investment in the Notes (including alternative characterizations and tax treatments of the Notes) and with respect to any tax consequences arising under the laws of any state, local or foreign taxing jurisdiction.

Payment on the Maturity Date. Assuming that the Notes are properly characterized and treated as pre-paid cash-settled forward contracts linked to the level of the Index, upon the receipt of cash on the maturity date of the Notes, a U.S. Holder (as defined in the accompanying product supplement ARN-4) will recognize gain or loss. The amount of such gain or loss will be the extent to which the amount of the cash received differs from the U.S. Holder’s tax basis in the Note. A U.S. Holder’s tax basis in a Note generally will equal the amount paid by the U.S. Holder to purchase the Note. It is uncertain whether any such gain or loss would be treated as ordinary income or loss or capital gain or loss. Absent a future clarification in current law (by an administrative determination, judicial ruling or otherwise), where required, ML&Co. intends to report any such gain or loss to the IRS in a manner consistent with the treatment of such gain or loss as capital gain or loss. If such gain or loss is treated as capital gain or loss, then any such gain or loss will be short-term or long-term capital gain or loss, depending upon the U.S. Holder’s holding period for the Note as of the maturity date.

Sale or Exchange of the Notes. Assuming that the Notes are properly characterized and treated as pre-paid cash-settled forward contracts linked to the level of the Index, upon a sale or exchange of a Note prior to the maturity date of the Notes, a U.S. Holder will generally recognize capital gain or loss in an amount equal to the difference between the amount realized on such sale or exchange and such U.S. Holder’s tax basis in the Note so sold or exchanged. Any such capital gain or loss will be short-term or long-term capital gain or loss, depending upon the U.S. Holder’s holding period for the Note as of the date of such sale or exchange.

Constructive Ownership Law. Section 1260 of the Internal Revenue Code of 1986, as amended (the “Code”), treats a taxpayer owning certain types of derivative positions in property as having “constructive ownership” of that property, with the result that all or a portion of any long-term capital gain recognized by that taxpayer with respect to the derivative position will be recharacterized as ordinary income. Although the matter is not entirely certain, in its current form, Section 1260 of the Code should not apply to the Notes. If Section 1260 of the Code were to apply to the Notes in the future, however, the effect on a U.S. Holder of a Note would be to treat all or a portion of any long-term capital gain recognized by the U.S. Holder on the sale, exchange or maturity of a Note as ordinary income. In addition, Section 1260 of the Code would impose an interest charge on any gain that was recharacterized. U.S. Holders should consult their tax advisors regarding the potential application of Section 1260 of the Code, if any, to the purchase, ownership and disposition of a Note.

Possible Future Tax Law Changes. On December 7, 2007, the IRS released a notice that could possibly affect the taxation of holders of the Notes. According to the notice, the IRS and the U.S. Department of the Treasury (the “Treasury Department”) are actively considering, among other things, whether the holder of an instrument having terms similar to the Notes should be required to accrue either ordinary income or capital gain on a current basis, and they are seeking comments on the subject. It is not possible to determine what guidance they will ultimately issue, if any. It is possible, however, that under such guidance, holders of instruments having terms similar to the Notes will ultimately be required to accrue income currently and this could be applied on a retroactive basis. The IRS and the Treasury Department are also considering other relevant issues, including whether additional gain or loss from such instruments should be treated as ordinary or capital, whether foreign holders of such instruments should be subject to withholding tax on any deemed income accruals, whether the tax treatment of such instruments should vary depending upon whether or not such instruments are traded on a securities exchange, whether such instruments should be treated as indebtedness, whether the tax treatment of such instruments should vary depending upon the nature of the underlying asset, and whether the special “constructive ownership rules” contained in Section 1260 of the Code might be applied to such instruments. Holders are urged to consult their tax advisors concerning the significance, and the potential impact, if any, of the above considerations to their investment in the Notes. ML&Co. intends to continue to treat the Notes for U.S. federal income tax purposes in accordance with the treatment described herein unless and until such time as the Treasury Department and IRS determine that some other treatment is more appropriate.

Prospective purchasers of the Notes should consult their own tax advisors concerning the tax consequences, in light of their particular circumstances, under the laws of the United States and any other taxing jurisdiction, of the purchase, ownership and disposition of the Notes. See the discussion under the section entitled “United States Federal Income Taxation” in the accompanying product supplement ARN-4.

Experts

The consolidated financial statements incorporated by reference in this term sheet from Merrill Lynch & Co., Inc.’s Annual Report on Form 10-K for the year ended December 28, 2007 and the effectiveness of Merrill Lynch & Co., Inc. and subsidiaries’ internal control over financial reporting have been audited by Deloitte & Touche LLP, an independent registered public accounting firm, as stated in their reports, incorporated herein by reference (which reports (1) expressed an unqualified opinion on the consolidated financial statements and included an explanatory paragraph regarding the changes in accounting methods in 2007 relating to the adoption of Statement of Financial Accounting Standards No. 157, “Fair Value Measurement,” Statement of Financial Accounting Standards No. 159, “The Fair Value Option for Financial Assets and Financial Liabilities—Including an amendment of FASB Statement No. 115,” and FASB Interpretation No. 48, “Accounting for Uncertainty in Income Taxes, an Interpretation of FASB Statement No. 109,” and in 2006 for share-based payments to conform to Statement of Financial Accounting Standards No. 123 (revised 2004), “Share-Based Payment,” and included an explanatory paragraph relating to the restatement discussed in Note 20 to the consolidated financial statements and (2) expressed an unqualified opinion on the effectiveness of internal control over financial reporting). Such consolidated financial statements have been so incorporated in reliance upon the reports of such firm given upon their authority as experts in accounting and auditing.

TS-11

Additional Note Terms

You should read this term sheet, together with the documents listed below (collectively, the “Note Prospectus”), which together contain the terms of the Notes and supersede all prior or contemporaneous oral statements as well as any other written materials. You should carefully consider, among other things, the matters set forth under “Risk Factors” in the sections indicated on the cover of this term sheet. The Notes involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisers before you invest in the Notes.

You may access the following documents on the SEC Website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC Website):

| § | Product supplement ARN-4 dated November 27, 2007: |

http://www.sec.gov/Archives/edgar/data/65100/000119312507253700/d424b2.htm

| § | MTN prospectus supplement dated March 31, 2006: |

http://www.sec.gov/Archives/edgar/data/65100/000119312506070946/d424b5.htm

| § | General prospectus supplement dated March 31, 2006: |

http://www.sec.gov/Archives/edgar/data/65100/000119312506070973/d424b5.htm

| § | Prospectus dated March 31, 2006: |

http://www.sec.gov/Archives/edgar/data/65100/000119312506070817/ds3asr.htm

Our Central Index Key, or CIK, on the SEC Website is 65100. References in this term sheet to “ML&Co.”, “we”, “us” and “our” are to Merrill Lynch & Co., Inc., and references to “MLPF&S” are to Merrill Lynch, Pierce, Fenner & Smith Incorporated.

ML&Co. has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (the “SEC”) for the offering to which this term sheet relates. Before you invest, you should read the prospectus in that registration statement, and the other documents relating to this offering that ML&Co. has filed with the SEC for more complete information about ML&Co. and this offering. You may get these documents without cost by visiting EDGAR on the SEC Website at www.sec.gov. Alternatively, ML&Co., any agent or any dealer participating in this offering, will arrange to send you the Note Prospectus if you so request by calling toll-free 1-866-500-5408.

Structured Investments Classification

ML&Co. classifies certain of its structured investments (the “Structured Investments”), including the Notes, into four categories, each with different investment characteristics. The description below is intended to briefly describe the four categories of Structured Investments offered: Principal Protection, Enhanced Income, Market Participation, and Enhanced Participation. A Structured Investment may, however, combine characteristics that are relevant to one or more of the other categories. As such, a category should not be relied upon as a description of any particular Structured Investment.

Principal Protection: Principal Protected Structured Investments offer full or partial principal protection at maturity, while offering market exposure and the opportunity for a better return than may be available from comparable fixed income securities. Principal protection may not be achieved if the investment is sold prior to maturity.

Enhanced Income: Structured Investments offering enhanced income may offer an enhanced income stream through interim fixed or variable coupon payments. However, in exchange for receiving current income, investors may forfeit upside potential on the underlying asset. These investments generally do not include the principal protection feature.

Market Participation: Market Participation Structured Investments can offer investors exposure to specific market sectors, asset classes and/or strategies that may not be readily available through traditional investment alternatives. Returns obtained from these investments are tied to the performance of the underlying asset. As such, subject to certain fees, the returns will generally reflect any increases or decreases in the value of such assets. These investments are not structured to include the principal protection feature.

Enhanced Participation: Enhanced Participation Structured Investments may offer investors the potential to receive better than market returns on the performance of the underlying asset. Some structures may offer leverage in exchange for a capped or limited upside potential and also in exchange for downside risk. These investments are not structured to include the principal protection feature.

The classification of Structured Investments is meant solely for informational purposes and is not intended to fully describe any particular Structured Investment nor guarantee any particular performance.

TS-12

ANNEX A

The following table lists the stocks comprising the WilderHill New Energy Total Return Index as of December 31, 2007 and the country of the exchanges in which the stocks are listed. These stocks are subject to change at any time. The next rebalancing of the Index is scheduled to occur on the last business day of March.

| Name | Country | % Weight in the Index | ||

| Abengoa SA |

SPAIN | 1.779 | ||

| Acciona SA |

SPAIN | 2.057 | ||

| Actelios SpA |

ITALY | 0.571 | ||

| American Superconductor Corp |

UNITED STATES | 1.032 | ||

| Anhui BBCA Biochemical Co Ltd |

CHINA | 0.628 | ||

| Arima Optoelectronics Corp |

TAIWAN | 0.388 | ||

| Aventine Renewable Energy Holdings Inc |

UNITED STATES | 0.348 | ||

| Babcock & Brown Wind Partners |

AUSTRALIA | 2.130 | ||

| Baldor Electric Co |

UNITED STATES | 1.304 | ||

| Ballard Power Systems Inc |

CANADA | 0.477 | ||

| BKW FMB Energie AG |

SWITZERLAND | 1.511 | ||

| Brasil Ecodiesel Industria e Comercio de |

BRAZIL | 0.358 | ||

| Byd Co Ltd |

CHINA | 0.170 | ||

| Canadian Hydro Developers Inc |

CANADA | 1.195 | ||

| Capstone Turbine Corp |

UNITED STATES | 0.460 | ||

| CENTROTEC Sustainable AG |

GERMANY | 0.430 | ||

| Comverge Inc |

UNITED STATES | 0.317 | ||

| Conergy AG |

GERMANY | 1.128 | ||

| Contact Energy Ltd |

NEW ZEALAND | 1.291 | ||

| Cosan SA Industria e Comercio |

BRAZIL | 2.454 | ||

| Cree Inc |

UNITED STATES | 2.164 | ||

| Ebara Corp |

JAPAN | 1.466 | ||

| Echelon Corp |

UNITED STATES | 0.298 | ||

| EDF Energies Nouvelles SA |

FRANCE | 2.273 | ||

| Energy Conversion Devices Inc |

UNITED STATES | 1.469 | ||

| Energy Developments Ltd |

AUSTRALIA | 0.474 | ||

| EnerNOC Inc |

UNITED STATES | 1.073 | ||

| Envitec Biogas AG |

GERMANY | 0.347 | ||

| Ersol Solar Energy AG |

GERMANY | 1.605 | ||

| Evergreen Solar Inc |

UNITED STATES | 1.153 | ||

| First Solar Inc |

UNITED STATES | 1.444 | ||

| Fortum Oyj |

FINLAND | 1.870 | ||

| FuelCell Energy Inc |

UNITED STATES | 1.291 | ||

| Gamesa Corp Tecnologica SA |

SPAIN | 2.154 | ||

| Greentech Energy Systems |

DENMARK | 1.963 | ||

| GS Yuasa Corp |

JAPAN | 0.628 | ||

| Gurit Holding AG |

SWITZERLAND | 0.629 | ||

| Hansen Transmissions International NV |

BELGIUM | 2.173 | ||

| Iberdrola Renovables |

SPAIN | 2.185 | ||

| International Rectifier Corp |

UNITED STATES | 1.125 | ||

| Itron Inc |

UNITED STATES | 1.281 | ||

| JA Solar Holdings Co Ltd |

CHINA | 1.309 | ||

| Japan Wind Development Co Ltd |

JAPAN | 1.079 | ||

| Kingspan Group Plc |

IRELAND | 1.448 | ||

| LDK Solar Co Ltd |

CHINA | 1.321 | ||

| Maxwell Technologies Inc |

UNITED STATES | 0.194 | ||

| Medis Technologies Ltd |

UNITED STATES | 0.352 | ||

| Meidensha Corp |

JAPAN | 0.395 |

TS-13

| MEMC Electronic Materials Inc |

UNITED STATES | 1.530 | ||

| Nordex AG |

GERMANY | 2.073 | ||

| Novozymes A/S |

DENMARK | 1.450 | ||

| Ormat Technologies Inc |

UNITED STATES | 1.116 | ||

| Pacific Ethanol Inc |

UNITED STATES | 0.363 | ||

| Plug Power Inc |

UNITED STATES | 0.332 | ||

| PNOC Energy Development Corp |

PHILIPPINES | 1.262 | ||

| Power Integrations Inc |

UNITED STATES | 1.318 | ||

| Power-One Inc |

UNITED STATES | 0.275 | ||

| PV Crystalox Solar PLC |

BRITAIN | 1.775 | ||

| Q-Cells AG |

GERMANY | 1.334 | ||

| Renewable Energy Corp AS |

NORWAY | 1.102 | ||

| REpower Systems AG |

GERMANY | 2.928 | ||

| Roth & Rau AG |

GERMANY | 1.493 | ||

| Saft Groupe SA |

FRANCE | 0.611 | ||

| Sanyo Electric Co Ltd |

JAPAN | 0.653 | ||

| Schmack Biogas AG |

GERMANY | 0.333 | ||

| Scottish & Southern Energy PLC |

BRITAIN | 2.340 | ||

| Sechilienne-Sidec |

FRANCE | 1.608 | ||

| Sharp Corp |

JAPAN | 1.946 | ||

| Solar Millennium AG |

GERMANY | 0.480 | ||

| Solaria Energia y Medio Ambiente SA |

SPAIN | 1.041 | ||

| Solarworld AG |

GERMANY | 1.563 | ||

| Solon AG Fuer Solartechnik |

GERMANY | 1.549 | ||

| Sunpower Corp |

UNITED STATES | 1.018 | ||

| Suntech Power Holdings Co Ltd |

CHINA | 0.975 | ||

| Takuma Co Ltd |

JAPAN | 0.316 | ||

| Theolia SA |

FRANCE | 2.407 | ||

| Ultralife Batteries Inc |

UNITED STATES | 0.150 | ||

| Umicore |

BELGIUM | 0.601 | ||

| VeraSun Energy Corp |

UNITED STATES | 1.158 | ||

| Verbio AG |

GERMANY | 0.298 | ||

| Verbund |

AUSTRIA | 1.448 | ||

| Verenium Corp |

UNITED STATES | 0.375 | ||

| Vestas Wind Systems A/S |

DENMARK | 2.595 | ||

| Yingli Green Energy Holding Co Ltd |

CHINA | 0.925 | ||

| Zhejiang Yankon Group Co Ltd |

CHINA | 0.563 | ||

| Zoltek Cos Inc |

UNITED STATES | 1.506 |

TS-14