Exhibit 4.1

BANK OF AMERICA CORPORATION

Medium-Term Senior Note, Series L

REGISTERED GLOBAL SENIOR NOTE

This Note is a global security within the meaning of the Indenture dated as of January 1, 1995, as supplemented from time to time (the “Indenture”), between Bank of America Corporation and The Bank of New York Mellon Trust Company, N.A., as successor trustee (the “Trustee”) under the Indenture and is registered in the name of Cede & Co., as the nominee of The Depository Trust Company (the “Depository”). This Note is not exchangeable for definitive or other Notes registered in the name of a person other than the Depository or its nominee, except in the limited circumstances described in the Indenture or in this Note, and no transfer of this Note (other than a transfer as a whole by the Depository to a nominee of the Depository or by a nominee of the Depository to the Depository or another nominee of the Depository or by the Depository or any such nominee to a successor depository or a nominee of such successor depository) may be registered except in the limited circumstances described in the Indenture.

Unless this Note is presented by an authorized representative of The Depository Trust Company (the “Depository”) (55 Water Street, New York, New York) to the Issuer or its agent for registration of transfer, exchange or payment, and this Note is registered in the name of CEDE & CO., or such other name as requested by an authorized representative of The Depository Trust Company, and unless any payment is made to CEDE & CO., ANY TRANSFER, PLEDGE OR OTHER USE HEREOF FOR VALUE OR OTHERWISE BY OR TO ANY PERSON IS WRONGFUL, since the registered owner hereof, CEDE & CO., has an interest herein.

THIS NOTE IS NOT A SAVINGS ACCOUNT OR A DEPOSIT AND IS NOT INSURED BY THE FEDERAL DEPOSIT INSURANCE CORPORATION OR ANY OTHER GOVERNMENTAL AGENCY AND IS NOT AN OBLIGATION OF OR GUARANTEED BY BANK OF AMERICA, N.A. OR ANY OTHER BANKING OR NONBANKING AFFILIATE OF BANK OF AMERICA CORPORATION. THIS DEBT IS NOT GUARANTEED BY THE FEDERAL DEPOSIT INSURANCE CORPORATION’S TEMPORARY LIQUIDITY GUARANTEE PROGRAM.

THIS NOTE IS A DIRECT, UNCONDITIONAL, UNSECURED AND UNSUBORDINATED GENERAL OBLIGATION OF BANK OF AMERICA CORPORATION. THE OBLIGATIONS EVIDENCED BY THIS NOTE RANK PARI PASSU WITH ALL OTHER UNSECURED AND UNSUBORDINATED OBLIGATIONS OF BANK OF AMERICA CORPORATION, EXCEPT OBLIGATIONS THAT ARE SUBJECT TO ANY PRIORITIES OR PREFERENCES UNDER APPLICABLE LAW.

THIS NOTE IS SOLD IN MINIMUM DENOMINATIONS AS NOTED HEREIN AND IN THE FINAL TERMS OR INDEXED PAYMENT RIDER ATTACHED HERETO AND CANNOT BE EXCHANGED FOR NOTES IN SMALLER DENOMINATIONS. EACH OWNER OF A BENEFICIAL INTEREST IN THIS NOTE IS REQUIRED TO HOLD A BENEFICIAL INTEREST OF A PRINCIPAL AMOUNT OF THIS NOTE EQUAL TO THE MINIMUM AUTHORIZED DENOMINATION AT ALL TIMES.

| No. R- |

Registered | |

| CUSIP No.: 060900230 |

||

| Principal Amount: $22,400,000 | ||

| Total Units: 2,240,000 |

BANK OF AMERICA CORPORATION

Medium-Term Senior Note, Series L

BEAR MARKET STRATEGIC ACCELERATED REDEMPTION SECURITIES®, LINKED TO THE S&P SMALL CAP REGIONAL BANKS INDEX, DUE AUGUST 31, 2010

REGISTERED GLOBAL SENIOR NOTE

| ORIGINAL ISSUE DATE: March 5, 2009 |

¨ | This Note is an Extendible Note at the Holder’s Option. [See attached Rider] | ||||||

| STATED MATURITY DATE: August 31, 2010 | ¨ | This Note is an Extendible Note at the Issuer’s Option. [See attached Rider] | ||||||

| CURRENCY: | ¨ | This Note is an Amortizing Note. [See payment schedule in attached Final Terms] | ||||||

| x | U.S. Dollars | |||||||

| ¨ | Other (specify): | |||||||

| ¨ | FIXED RATE NOTE | |||||||

| ¨ | FLOATING RATE NOTE | x | See attached Final Term Sheet dated February 26, 2009 and Product Supplement No. STR-1 dated January 2, 2009 (collectively, the “Final Terms”) | |||||

| x | INDEXED NOTE | ¨ | See attached Principal Repayment Amount Rider | |||||

| ¨ |

See attached Interest Payment Amounts or Supplemental Payment Amount Rider | |||||||

| ¨ | FLOATING RATE/FIXED RATE NOTE | |||||||

| RECORD DATES: Not Applicable | CALCULATION AGENT: Merrill Lynch, Pierce, Fenner & Smith Incorporated | |||||||

BANK OF AMERICA CORPORATION, a Delaware corporation (herein called the “Issuer,” which term includes any successor corporation), for value received, hereby promises to pay to CEDE & CO., as nominee for The Depository Trust Company, or its registered assigns, the principal amount specified above and any other amounts calculated in accordance with the provisions set forth in the Final Terms attached hereto, as adjusted in accordance with Schedule 1 hereto, on the Stated Maturity Date specified above (except to the extent redeemed or repaid prior to the Stated Maturity Date). “Maturity,” when used herein, means the date on which the principal of this Note or an installment of principal becomes due and payable in full in accordance with the terms of this Note and of the Indenture, whether at the Stated Maturity Date or by declaration of acceleration, call for redemption, prepayment at the holder’s option or otherwise.

2

The principal or any other amounts so payable, and punctually paid or duly provided for, at Maturity will be paid to the person in whose name this Note (or one or more predecessor Notes evidencing all or a portion of the same debt as this Note) is registered at the time of payment. Any such principal or other amounts not punctually paid or duly provided for shall be payable as provided in this Note and in the Indenture.

Payment of principal of, and premium, if any, and other amounts, if any, on, this Note due at Maturity will be made in immediately available funds upon presentation and surrender of this Note at the office of the Trustee maintained for that purpose, and in accordance with the procedures of the depository or clearing system noted hereon; provided, that this Note is presented to the Trustee in time for the Trustee to make such payment in accordance with its normal procedures.

The Issuer will pay any administrative costs imposed by any bank in making payments in immediately available funds, but any tax, assessment or governmental charge imposed upon payments hereunder, including, without limitation, any withholding tax, will be borne by the holder hereof.

By its acceptance of this Note, the holder of this Note agrees, in the absence of an administrative determination or judicial ruling to the contrary, to treat this Note for all tax purposes as a callable single financial contract linked to the S&P Small Cap Regional Banks Index that (1) requires the holder of this Note to pay to the Issuer on the Original Issue Date an amount equal to the purchase price of this Note and (2) entitles the holder of this Note to receive at the Stated Maturity Date an amount in cash linked to the value of the S&P Small Cap Regional Banks Index.

Reference is made to the further provisions of this Note set forth on the reverse hereof and in the Final Terms attached hereto, which shall have the same effect as though fully set forth at this place. In the event of any conflict between the provisions contained herein or on the reverse hereof and the provisions contained in the Final Terms attached hereto, the latter shall control. References herein to “this Note,” “hereof,” “herein” and comparable terms shall include the Final Terms attached hereto.

Unless the certificate of authentication hereon has been executed by the Trustee (or other authentication agent duly appointed in accordance with the Indenture), by manual signature of an authorized signatory, this Note shall not be entitled to any benefit under the Indenture or be valid or obligatory for any purpose.

3

IN WITNESS WHEREOF, Bank of America Corporation has caused this instrument to be duly executed on its behalf, by manual or facsimile signature.

| Dated: March 5, 2009 | BANK OF AMERICA CORPORATION | |||||||

| [CORPORATE SEAL] | ||||||||

| By: |

| |||||||

| ATTEST: | Name: | |||||||

| Title: | ||||||||

| By: |

|

|||||||

| Title: | Assistant Secretary | |||||||

4

CERTIFICATE OF AUTHENTICATION

This is one of the Securities of the series designated therein referred to in the within-mentioned Indenture.

| Dated: March 5, 2009 | THE BANK OF NEW YORK MELLON TRUST COMPANY, N.A., | |||||

| as Trustee | ||||||

| By: | ||||||

| Authorized Signatory | ||||||

5

[ATTACH FINAL TERMS]

6

The notes are being offered by Bank of America Corporation (“BAC”). The notes will have the terms specified in this term sheet as supplemented by the documents indicated herein under “Additional Terms” (together the “Note Prospectus”). Investing in the notes involves a number of risks. See “Risk Factors” and “Additional Risk Factors” on page TS-6 of this term sheet and beginning on page S-10 of product supplement STR-1.

Unless otherwise indicated or unless the context requires otherwise, all references in this document to “we,” “us,” “our,” or similar references are to BAC. References to “MLPF&S” are to Merrill Lynch, Pierce, Fenner & Smith Incorporated.

In connection with this offering, each of MLPF&S and its broker-dealer affiliate First Republic Securities Company, LLC is acting in its capacity as a principal.

None of the Securities and Exchange Commission (the “SEC”), any state securities commission, or any other regulatory body has approved or disapproved of these securities or determined if this Note Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Unit | Total | |||

| Public offering price (1) |

$10.00 | $22,400,000 | ||

| Underwriting discount (1) |

$.15 | $336,000 | ||

| Proceeds, before expenses, to Bank of America Corporation |

$9.85 | $22,064,000 |

| (1) | The public offering price and underwriting discount for any purchase of 500,000 or more units in a single transaction by an individual investor will be $9.95 per unit and $.10 per unit, respectively. |

“Strategic Accelerated Redemption Securities®” is a registered service mark of our subsidiary, Merrill Lynch & Co., Inc.

Standard & Poor’s,®” “Standard & Poor’s Small Cap 600 Index,” “S&P 600,” “Standard & Poor’s SmallCap 600,” and “S&P®” are trademarks of The McGraw Hill Companies, Inc. and have been licensed for use in this offering by our subsidiary, MLPF&S. The notes are not sponsored, endorsed, sold, or promoted by Standard & Poor’s® and Standard & Poor’s® makes no representation regarding the advisability of investing in the notes.

Merrill Lynch & Co.

February 26, 2009

Summary

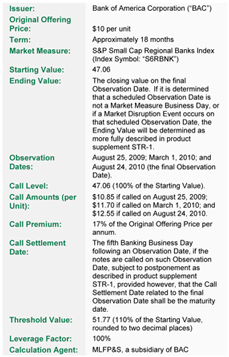

The Bear Market Strategic Accelerated Redemption Securities® Linked to the S&P Small Cap Regional Banks Index, due August 31, 2010 (the “notes”), are our senior unsecured debt securities and are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The notes will rank equally with all of our other unsecured and unsubordinated debt, and any payments due on the notes, including any repayment of principal, will be subject to the credit risk of BAC. The notes are designed for, but not limited to, investors who anticipate that the Observation Level of the S&P Small Cap Regional Banks Index (the “Index”) on any Observation Date will be less than or equal to the Call Level. The notes provide for an automatic call if the Observation Level of the Index on any Observation Date is less than or equal to the Call Level. If the notes are called on any Observation Date, you will receive on the Call Settlement Date an amount per unit (the “Call Amount”) equal to the $10 Original Offering Price of the notes plus the applicable Call Premium. If your notes are not called, the amount you receive on the maturity date (the “Redemption Amount”) will not be greater than the Original Offering Price per unit and will be based on the direction of and percentage increase in the closing level of the Index from the Starting Value, as determined on February 26, 2009, the pricing date, to the Ending Value, as determined on the final Observation Date. Investors must be willing to forgo interest payments on the notes and be willing to accept a repayment that may be less, and potentially significantly less, than the Original Offering Price of the notes. Investors also must be prepared to have their notes called by us on any Observation Date.

Capitalized terms used but not defined in this term sheet have the meanings set forth in product supplement STR-1.

| Terms of the Notes | Determining Payment for the Notes | |||

|

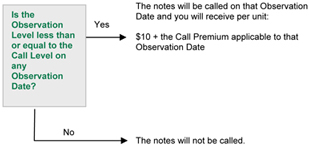

Automatic Call Provision:

The notes will be automatically called on an Observation Date if the Observation Level on such Observation Date is less than or equal to the applicable Call Level. If the notes are called, you will receive on the Call Settlement Date the Call Amount per unit applicable to such Observation Date, which is equal to the $10 Original Offering Price per unit plus the Call Premium.

Payment at Maturity:

If the notes are not called prior to the maturity date, you will receive the Redemption Amount per unit on the maturity date, calculated as follows:

| |||

TS-2

Hypothetical Payments

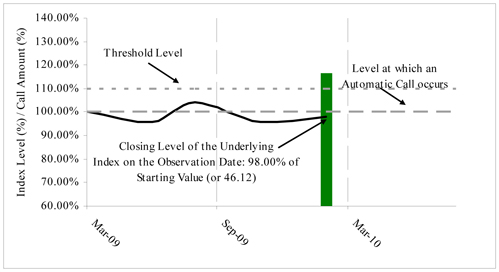

Set forth below are five hypothetical examples of payment calculations, reflecting:

1) the Starting Value of 47.06, the closing level of the Index on February 26, 2009;

2) the Threshold Value of 51.77, or 110% of the Starting Value (rounded to two decimal places);

3) the Call Level of 47.06, or 100% of the Starting Value;

4) the term of the notes from March 5, 2009 to August 31, 2010;

5) the Call Premium of 17% of the $10.00 Original Offering Price per unit per annum; and

6) Observation Dates occurring on August 25, 2009, March 1, 2010, and August 24, 2010.

The Notes Are Called on One of the Observation Dates

The notes have not been previously called and the Observation Level on the relevant Observation Date is less than or equal to the Call Level. Consequently, the notes will be called at the Call Amount per unit equal to $10.00 plus the applicable Call Premium.

Example 1

If the call is related to the Observation Date that falls on August 25, 2009, the Call Amount per unit will be:

$10.00 plus the Call Premium of $0.85 = $10.85 per unit.

![]()

Example 2

If the call is related to the Observation Date that falls on March 1, 2010, the Call Amount per unit will be:

$10.00 plus the Call Premium of $1.70 = $11.70 per unit.

TS-3

Example 3

If the call is related to the Observation Date that falls on August 24, 2010, the Call Amount per unit will be:

$10.00 plus the Call Premium of $2.55 = $12.55 per unit.

The Notes Are Not Called on Any of the Observation Dates

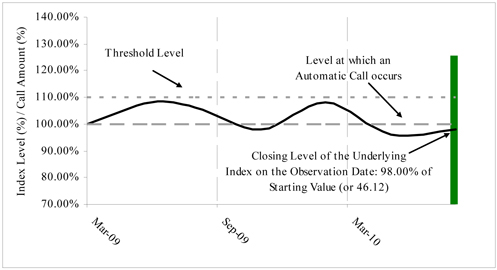

Example 4

The notes are not called on any of the Observation Dates and the hypothetical Ending Value of the Index on the final Observation Date is not greater than 51.77, the Threshold Value. The amount received at maturity per unit will therefore be $10.00.

TS-4

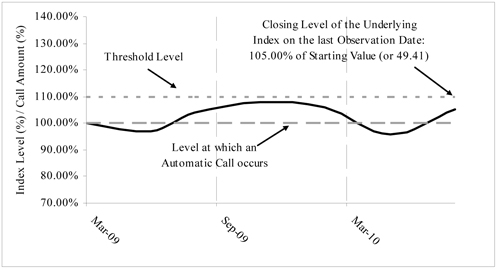

Example 5

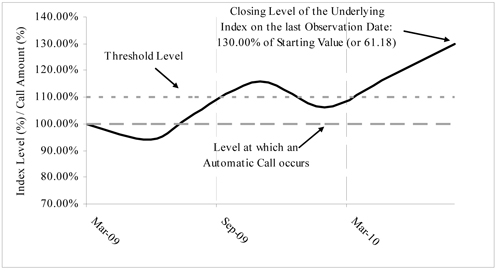

The notes are not called on any of the Observation Dates and the hypothetical Ending Value of the Index on the final Observation Date is greater than 51.77, the Threshold Value. The amount received at maturity will be less, and possibly significantly less, than the Original Offering Price of $10 per unit.

If the Ending Value is 61.18, or 130% of the Starting Value, the payment at maturity will be:

$10 + [$10 x (51.77 – 61.18) / 47.06] = $8.00 per unit

These examples have been prepared for purposes of illustration only. Your actual return will depend on the Observation Level of the Index on the applicable Observation Date, the Ending Value, if applicable, and the term of your investment.

| Summary of the Hypothetical Examples | ||||||

| Notes Are Called on an Observation Date |

Observation Date on August 25, 2009 |

Observation Date on March 1, 2010 |

Observation Date on August 24, 2010 | |||

| Starting Value |

47.06 | 47.06 | 47.06 | |||

| Call Level |

47.06 | 47.06 | 47.06 | |||

| Hypothetical Observation Level on the Observation Date |

45.18 | 46.12 | 46.12 | |||

| Return of the Index (excluding any dividends) |

-4.00% | -2.00% | -2.00% | |||

| Return of the Notes |

8.50% | 17.00% | 25.50% | |||

| Call Amount per Unit |

$10.85 | $11.70 | $12.55 | |||

| Notes Are Not Called on Any Observation Date |

Hypothetical Ending Value Is Less than the Threshold Value |

Hypothetical Ending Value Is Greater than the Threshold Value | ||

| Starting Value |

47.06 | 47.06 | ||

| Hypothetical Ending Value |

49.41 | 61.18 | ||

| Threshold Value |

51.77 | 51.77 | ||

| Is the hypothetical Ending Value greater than the Threshold Value? | No | Yes | ||

| Return of the Index (excluding any dividends) |

5.00% | 30.00% | ||

| Return of the Notes |

0.00% | -20.00% | ||

| Redemption Amount per Unit |

$10.00 | $8.00 | ||

TS-5

An investment in the notes involves significant risks. The following is a list of certain of the risks involved in investing in the notes. You should carefully review the more detailed explanation of risks relating to the notes in the “Risk Factors” sections included in the product supplement STR-1 and MTN prospectus supplement identified below under “Additional Terms.” We also urge you to consult your investment, legal, tax, accounting, and other advisers before you invest in the notes.

| § | If the notes are not called, your investment may result in a loss; there is no guaranteed return of principal. |

| § | Your return, if any, is limited to the Call Premium. |

| § | Your yield may be less than the yield on a conventional debt security of comparable maturity. |

| § | Your investment return may be less than a comparable investment directly in shares of the stocks included in the Index. |

| § | You must rely on your own evaluation of the merits of an investment linked to the Index. |

| § | In seeking to provide you with what we believe to be commercially reasonable terms for the notes while providing the selling agents with compensation for their services, we have considered the costs of developing, hedging, and distributing the notes. |

| § | We cannot assure you that a trading market for your notes will ever develop or be maintained. |

| § | The amount that you receive at maturity or upon a call will not be affected by all developments relating to the Index. |

| § |

S&P® may adjust the Index in a way that affects its value, and S&P® has no obligation to consider your interests. |

| § | You will have no rights as a securityholder of the securities represented by the Index, and you will not be entitled to receive any of those securities or dividends or other distributions by the issuers of those securities. |

| § | We do not control any company included in the Index, and are not responsible for any disclosure made by any such company. |

| § | If you attempt to sell notes prior to maturity, their market value, if any, will be affected by various factors that interrelate in complex ways, and their market value may be less than their Original Offering Price. |

| § | Payments on the notes are subject to our credit risk, and changes in our credit ratings are expected to affect the value of the notes. |

| § | Purchases and sales by us and our affiliates may affect your return. |

| § | Our trading and hedging activities may create conflicts of interest with you. |

| § | Our hedging activities may affect your return at maturity and the market value of the notes. |

| § | Our business activities relating to the companies represented by the Index may create conflicts of interest with you. |

| § | There may be potential conflicts of interest involving the calculation agent. We have the right to appoint and remove the calculation agent. |

| § | The U.S. federal income tax consequences of the notes are uncertain, and may be adverse to a holder of the notes. See “Certain U.S. Federal Income Taxation Considerations” below. |

The stocks represented by the Index are concentrated in one industry.

All of the stocks included in the Index are issued by companies involved directly or indirectly in the U.S. banking industry. As a result, the stocks that will determine the performance of the Index and hence, the value of the notes, are concentrated in one industry. Although an investment in the notes will not give you any ownership or other rights in the stocks represented by the Index, the return on an investment in the notes will be subject to certain risks associated with direct equity investments in the U.S. banking industry. Accordingly, depending upon the performance of the Index, your investment in the notes may produce a lower return than an investment in a more diversified Market Measure.

Legislative and regulatory actions by the U.S. government may increase the value of the Index, which would reduce your return on the notes.

As a result of the ongoing global financial crisis, the U.S. government has implemented a series of unprecedented intervention programs and policies. For example, the Federal Reserve Board has approved expansion of its liquidity programs and established programs to encourage lending in and by the U.S. banking sector. In October 2008, the Emergency Economic Stabilization Act of 2008 established the Troubled Assets Relief Plan, a $700 billion spending plan. Under this plan, the Secretary of the Treasury established the Capital Purchase Program to provide capital to banking institutions in the U.S., including many institutions included in the Index. Also in October 2008, the Federal Deposit Insurance Corporation established a guarantee program under which qualifying financial institutions can issue debt backed by the full faith and credit of the U.S. More recently, legislation has been proposed to further stimulate the U.S. economy and reverse the impact of the financial crisis. Additional programs, policies and legislation, or expansion of existing programs, may be established by the U.S. or one or more states. Many of these actions are designed to strengthen the balance sheets of financial institutions to permit increased lending, and stabilize and reduce credit losses in assets held by these financial institutions. If these efforts are successful, the market value of the equity securities of U.S. banks, and therefore, the value of the Index, may increase, in which case your return on the notes would decrease.

TS-6

Investor Considerations

Other Provisions

We will deliver the notes against payment therefor in New York, New York on a date that is in excess of three business days following the pricing date. Under Rule 15c6-1 of the Securities Exchange Act of 1934, trades in the secondary market generally are required to settle in three business days, unless the parties to any such trade expressly agree otherwise. Accordingly, purchasers who wish to trade notes more than three business days prior to the original issue date will be required to specify alternative settlement arrangements to prevent a failed settlement.

If you place an order to purchase these offered securities, you are consenting to each of MLPF&S and its broker-dealer affiliate First Republic Securities Company, LLC acting as a principal in effecting the transaction for your account. MLPF&S is acting as an underwriter and/or selling agent for this offering and will receive underwriting compensation from BAC.

Supplement to the Plan of Distribution

MLPF&S and First Republic Securities Company, LLC, each a broker-dealer subsidiary of BAC, are members of the Financial Industry Regulatory Authority, Inc. (formerly the National Association of Securities Dealers, Inc. (the “NASD”)) and will participate in distribution of the notes. Accordingly, offerings of the notes will conform to the requirements of NASD Rule 2720. In the original offering of the notes, the notes will be sold in minimum investment amounts of 100 units.

MLPF&S and First Republic Securities Company, LLC may use this Note Prospectus for offers and sales in secondary market transactions and market-making transactions in the notes but are not obligated to engage in such secondary market transactions and/or market-making transactions. MLPF&S and First Republic Securities Company, LLC may act as principal or agent in these transactions, and any such sales will be made at prices related to prevailing market prices at the time of the sale.

TS-7

The Index

The S&P Small Cap Regional Banks Index

We have obtained all information regarding the Index contained in this term sheet, including its make up, method of calculation, and changes in its components, from publicly available information. That information reflects the policies of, and is subject to change by, Standard & Poor’s®, a division of The McGraw-Hill Companies, Inc. (“S&P®” or “Standard & Poor’s”). S&P®, which owns the copyright and all other rights to the S&P Small Cap Regional Banks Index, has no obligation to continue to publish, and may discontinue publication of, the S&P Small Cap Regional Banks Index. The consequences of S&P® discontinuing publication of the S&P Small Cap Regional Banks Index are discussed in the section of product supplement STR-1 entitled “Description of the Notes—Discontinuance of a Non-Exchange Traded Fund Market Measure.” We do not assume any responsibility for the accuracy or completeness of any information relating to the S&P Small Cap Regional Banks Index.

The Index is a capitalization weighted index. The Index is a sub-index of the S&P SmallCap 600 Index and is comprised of the regional banks included in the “Financials” sector of the S&P SmallCap 600 Index. Regional banks are defined as commercial banks whose businesses are derived primarily from commercial lending operations and have significant business activity in retail banking and small and medium corporate lending. Regional banks tend to operate in limited geographic regions. The Index excludes companies classified according to the Global Industry Classification Standard (“GICS”) in the Diversified Banks and Thrifts & Mortgage Banks sub-industries and also excludes investment banks classified in the Investment Banking & Brokerage Sub-Industry. The GICS methodology has been widely accepted as an industry analysis framework for investment research, portfolio management, and asset allocation. The Index was developed with a base value of 100 as of December 31, 1993.

Of the companies included in the S&P SmallCap 600 Index, 41 were included in the Index as of February 26, 2009. These companies and their respective weights were obtained from Bloomberg, without independent verification. As of that date, the companies and their respective weights were as follows:

| Company Name |

Symbol | Percentage Weight in the Index | ||

| Boston Private Financial Holdings Inc |

BPFH | 1.359803 | ||

| Cascade Bancorp |

CACB | 0.204215 | ||

| Central Pacific Financial Corp |

CPF | 0.773329 | ||

| Columbia Banking System Inc |

COLB | 0.918319 | ||

| Community Bank System Inc |

CBU | 3.433084 | ||

| East West Bancorp Inc |

EWBC | 2.74293 | ||

| First Bancorp/Puerto Rico |

FBP | 2.010143 | ||

| First Commonwealth Financial Corp |

FCF | 3.779863 | ||

| First Financial Bancorp |

FFBC | 1.541016 | ||

| First Financial Bankshares Inc |

FFIN | 5.486339 | ||

| First Midwest Bancorp Inc/IL |

FMBI | 2.37658 | ||

| Frontier Financial Corp |

FTBK | 0.517073 | ||

| Glacier Bancorp Inc |

GBCI | 5.740705 | ||

| Hancock Holding Co |

HBHC | 4.129617 | ||

| Hanmi Financial Corp |

HAFC | 0.256941 | ||

| Home Bancshares Inc/Conway AR |

HOMB | 1.483808 | ||

| Independent Bank Corp/MI |

IBCP | 0.126254 | ||

| Independent Bank Corp/Rockland MA |

INDB | 1.430957 | ||

| Irwin Financial Corp |

IFC | 0.205633 | ||

| Nara Bancorp Inc |

NARA | 0.38832 | ||

| National Penn Bancshares Inc |

NPBC | 3.60838 | ||

| Old National Bancorp/IN |

ONB | 4.871053 | ||

| PrivateBancorp Inc |

PVTB | 2.166172 | ||

| Prosperity Bancshares Inc |

PRSP | 6.589101 | ||

| Provident Bankshares Corp |

PBKS | 1.313695 | ||

| S&T Bancorp Inc |

STBA | 3.290801 | ||

| Signature Bank/New York NY |

SBNY | 5.502857 | ||

| South Financial Group Inc/The |

TSFG | 0.608381 | ||

| Sterling Bancorp/NY |

STL | 1.008205 | ||

| Sterling Bancshares Inc/TX |

SBIB | 2.481429 | ||

| Sterling Financial Corp/WA |

STSA | 0.482417 | ||

TS-8

| Company Name |

Symbol | Percentage Weight in the Index | ||

| Susquehanna Bancshares Inc |

SUSQ | 4.848412 | ||

| Tompkins Financial Corp |

TMP | 1.591649 | ||

| UCBH Holdings Inc |

UCBH | 1.23329 | ||

| UMB Financial Corp |

UMBF | 6.894848 | ||

| Umpqua Holdings Corp |

UMPQ | 3.226173 | ||

| United Bankshares Inc |

UBSI | 3.651946 | ||

| United Community Banks Inc/GA |

UCBI | 0.879411 | ||

| Whitney Holding Corp/LA |

WTNY | 4.434916 | ||

| Wilshire Bancorp Inc |

WIBC | 0.565514 | ||

| Wintrust Financial Corp |

WTFC | 1.846419 | ||

The S&P SmallCap 600 Index

S&P® publishes the S&P SmallCap 600 Index. The S&P SmallCap 600 Index is intended to provide a benchmark for performance measurement of the small capitalization segment of the U.S. equity markets. It tracks the stock price movement of 600 companies with small market capitalizations, primarily ranging from $200 million to $1.0 billion. The calculation of the value of the S&P SmallCap 600 Index, discussed below in further detail, is based on the relative market value of the common stocks of 600 companies (the “Component Stocks”) as of a particular time as compared to the market value of the common stocks of 600 similar companies on the base date of December 31, 1993. S&P® chooses companies for inclusion in the S&P SmallCap 600 Index with an aim of achieving a distribution by broad industry groupings that approximates the distribution of these groupings in the common stock population of the small capitalization segment of the U.S. equity market. S&P® may from time to time, in its sole discretion, add companies to, or delete companies from, the S&P SmallCap 600 Index to achieve the objectives stated above. Relevant criteria employed by S&P® include U.S. company status, a market cap range between $200 million and $1.0 billion, financial viability, a public float of at least 50%, adequate liquidity and reasonable price, sector representation, and status as an operating company.

As of January 30, 2009, the Component Stocks had an aggregate market capitalization of approximately $284 billion. As of January 30, 2009, 283 companies or 52.8% of the market capitalization of the S&P SmallCap 600 Index companies traded on the New York Stock Exchange, 314 companies or 46.7% of the market capitalization of the S&P SmallCap 600 Index companies traded on The NASDAQ Stock Market, and 3 companies or 0.4% of the market capitalization of the S&P SmallCap 600 Index companies traded on the NYSE Alternext U.S. stock exchange. As of January 30, 2009, ten main groups of companies comprise the S&P SmallCap 600 Index with the number of companies currently included in each group indicated in parentheses: Consumer Discretionary (118), Consumer Staples (21), Energy (24), Financials (107), Health Care (71), Industrials (97), Information Technology (119), Materials (31), Telecommunication Services (2), and Utilities (16).

Computation of the S&P SmallCap 600 Index

While S&P® currently employs the following methodology to calculate the S&P SmallCap 600 Index, no assurance can be given that S&P® will not modify or change this methodology in a manner that may affect the amount an investor receives on the maturity date or upon automatic call of the notes.

The S&P SmallCap 600 Index is calculated using a base-weighted aggregate methodology: the level of the index reflects the total market value of all 600 Component Stocks relative to the base date of December 31, 1993. An indexed number is used to represent the results of this calculation in order to make the value easier to work with and track over time.

The actual total market value of the Component Stocks on the base date of December 31, 1993 has been set equal to an indexed value of 100. This is often indicated by the notation December 31, 1993=100. In practice, the daily calculation of the S&P SmallCap 600 Index is computed by dividing the total market value of the Component Stocks by the index divisor. By itself, the index divisor is an arbitrary number. However, in the context of the calculation of the S&P SmallCap 600 Index, it serves as a link to the original base period value of the index. The index divisor keeps the index comparable over time and is the manipulation point for all adjustments to the S&P SmallCap 600 Index, which is index maintenance. Index maintenance includes monitoring and completing the adjustments for company additions and deletions, share changes, stock splits, stock dividends, and stock price adjustments due to company restructurings or spinoffs.

In March 2005, S&P® began shifting the S&P SmallCap 600 Index half way from a market capitalization weighted formula to a float-adjusted formula, before moving the S&P SmallCap 600 Index to full float adjustment on September 16, 2005. S&P®’s criteria for selecting stocks for the S&P SmallCap 600 Index did not change by the shift to float adjustment. However, the adjustment affects each company’s weight in the S&P SmallCap 600 Index.

Under float adjustment, the share counts used in calculating the S&P SmallCap 600 Index will reflect only those shares that are available to investors, not all of a company’s outstanding shares. S&P® defines three groups of shareholders whose holdings are subject to float adjustment:

| • | holdings by other publicly traded corporations, venture capital firms, private equity firms, strategic partners, or leveraged buyout groups; |

| • | holdings by government entities, including all levels of government in the U.S. or foreign countries; and |

| • | holdings by current or former officers and directors of the company, founders of the company, or family trusts of officers, directors, or founders, as well as holdings of trusts, foundations, pension funds, employee stock ownership plans, or other investment vehicles associated with and controlled by the company. |

However, treasury stock, stock options, restricted shares, equity participation units, warrants, preferred stock, convertible stock, and rights are not part of the float. In cases where holdings in a group exceed 10% of the outstanding shares of a company, the holdings of that group are excluded

TS-9

from the float-adjusted count of shares to be used in the index calculation. Mutual funds, investment advisory firms, pension funds, or foundations not associated with the company and investment funds in insurance companies, shares of a U.S. company traded in Canada as “exchangeable shares,” shares that trust beneficiaries may buy or sell without difficulty or significant additional expense beyond typical brokerage fees, and, if a company has multiple classes of stock outstanding, shares in an unlisted or non-traded class if such shares are convertible by shareholders without undue delay and cost, are also part of the float.

For each stock, an investable weight factor (“IWF”) is calculated by dividing the available float shares, defined as the total shares outstanding less shares held in one or more of the three groups listed above where the group holdings exceed 10% of the outstanding shares, by the total shares outstanding. The float-adjusted index is then calculated by dividing the sum of the IWF multiplied by both the price and the total shares outstanding for each stock by the index divisor. For companies with multiple classes of stock, S&P® calculates the weighted average IWF for each stock using the proportion of the total company market capitalization of each share class as weights.

S&P SmallCap 600 Index Maintenance

S&P SmallCap 600 Index maintenance includes monitoring and completing the adjustments for company additions and deletions, share changes, stock splits, stock dividends, and stock price adjustments due to company restructuring or spinoffs. Some corporate actions, such as stock splits and stock dividends, require changes in the common shares outstanding and the stock prices of the companies in the S&P SmallCap 600 Index, and do not require index divisor adjustments.

To prevent the level of the S&P SmallCap 600 Index from changing due to corporate actions, corporate actions which affect the total market value of the S&P SmallCap 600 Index require an index divisor adjustment. By adjusting the index divisor for the change in market value, the level of the S&P SmallCap 600 Index remains constant and does not reflect the corporate actions of individual companies in the S&P SmallCap 600 Index. Index divisor adjustments are made after the close of trading and after the calculation of the S&P SmallCap 600 Index closing level.

Changes in a company’s shares outstanding of 5.00% or more due to mergers, acquisitions, public offerings, private placements, tender offers, Dutch auctions, or exchange offers are made as soon as reasonably possible. All other changes of 5.00% or more (due to, for example, company stock repurchases, redemptions, exercise of options, warrants, subscription rights, conversion of preferred stock, notes, debt, equity participation units, or other recapitalizations) are made weekly and are announced on Tuesdays for implementation after the close of trading on Wednesday. Changes of less than 5.00% are accumulated and made quarterly on the third Friday of March, June, September, and December, and are usually announced two days prior.

Changes in IWFs of more than ten percentage points caused by corporate actions (such as merger and acquisition activity, restructurings, or spinoffs) will be made as soon as reasonably possible. Other changes in IWFs will be made annually, in September, when IWFs are reviewed.

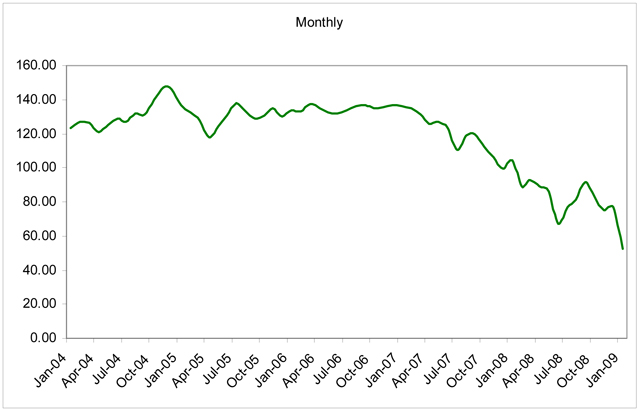

Historical Data

The following graph sets forth the monthly historical performance of the Index in the period from January 2004 through January 2009. This historical data on the Index is not necessarily indicative of the future performance of the Index or what the value of the notes may be. Any historical upward or downward trend in the value of the Index during any period set forth below is not an indication that the Index is more or less likely to increase or decrease at any time over the term of the notes. On the pricing date, the closing value of the Index was 47.06.

TS-10

Before investing in the notes, you should consult publicly available sources for the values and trading pattern of the Index. The generally unsettled international environment and related uncertainties, including the risk of terrorism, may result in financial markets generally and the Index exhibiting greater volatility than in earlier periods.

License Agreement

S&P® does not guarantee the accuracy and/or the completeness of the Index or any data included in the Index. S&P® shall have no liability for any errors, omissions, or interruptions in the Index. S&P® makes no warranty, express or implied, as to results to be obtained by MLPF&S, us, holders of the notes, or any other person or entity from the use of the Index or any data included in the Index in connection with the rights licensed under the license agreement described in this term sheet or for any other use. S&P® makes no express or implied warranties, and hereby expressly disclaims all warranties of merchantability or fitness for a particular purpose with respect to the Index or any data included in the Index. Without limiting any of the above information, in no event shall S&P® have any liability for any special, punitive, indirect or consequential damages; including lost profits, even if notified of the possibility of these damages.

S&P® and MLPF&S have entered into a non-exclusive license agreement providing for the license to MLPF&S, in exchange for a fee, of the right to use the Index in connection with this offering. The license agreement provides that the following language must be stated in this term sheet:

“The notes are not sponsored, endorsed, sold or promoted by S&P®. S&P® makes no representation or warranty, express or implied, to the holders of the notes or any member of the public regarding the advisability of investing in securities generally or in the notes particularly or the ability of the Index to track general stock market performance. S&P®’s only relationship to MLPF&S and to us (other than transactions entered into in the ordinary course of business) is the licensing of certain trademarks and trade names of S&P® and of the Index which is determined, composed, and calculated by S&P® without regard to MLPF&S, us or the notes. S&P® has no obligation to take the needs of MLPF&S, our needs, or the needs of the holders of the notes into consideration in determining, composing, or calculating the Index. S&P® is not responsible for and has not participated in the determination of the timing of the sale of the notes, prices at which the notes are to initially be sold, or quantities of the notes to be issued or in the determination or calculation of the equation by which the notes are to be converted into cash. S&P® has no obligation or liability in connection with the administration, marketing, or trading of the notes.”

TS-11

Summary Tax Consequences

You should consider the U.S. federal income tax consequences of an investment in the notes, including the following:

| • | You agree with us (in the absence of an administrative determination, or judicial ruling to the contrary) to characterize and treat the notes for all tax purposes as a callable single financial contract linked to the Index that requires you to pay us at inception an amount equal to the purchase price of the notes and that entitles you to receive at maturity or upon earlier redemption an amount in cash linked to the value of the Index. |

| • | Under this characterization and tax treatment of the notes, upon receipt of a cash payment at maturity or upon a sale, exchange, or redemption of the notes prior to maturity, you generally will recognize capital gain or loss. This capital gain or loss generally will be long-term capital gain or loss if you hold the notes for more than one year. |

Certain U.S. Federal Income Taxation Considerations

Set forth below is a summary of certain U.S. federal income tax considerations relating to an investment in the notes. The following summary is not complete and is qualified in its entirety by the discussion under the section entitled “U.S. Federal Income Tax Summary,” as set forth in product supplement STR-1, which you should carefully review prior to investing in the notes.

General. Although there is no statutory, judicial, or administrative authority directly addressing the characterization of the notes, we intend to treat the notes for all tax purposes as a callable single financial contract linked to the Index that requires you to pay us at inception an amount equal to the purchase price of the notes and that entitles you to receive at maturity or upon earlier redemption an amount in cash linked to the value of the Index. Under the terms of the notes, we and every investor in the notes agree, in the absence of an administrative determination or judicial ruling to the contrary, to treat the notes as described in the preceding sentence. This discussion assumes that the notes constitute a callable single financial contract linked to the Index for U.S. federal income tax purposes. If the notes did not constitute a callable single financial contract, the tax consequences described below would be materially different.

This characterization of the notes is not binding on the Internal Revenue Service (“IRS”) or the courts. No statutory, judicial, or administrative authority directly addresses the characterization of the notes or any similar instruments for U.S. federal income tax purposes, and no ruling is being requested from the IRS with respect to their proper characterization and treatment. Due to the absence of authorities on point, significant aspects of the U.S. federal income tax consequences of an investment in the notes are not certain, and no assurance can be given that the IRS or any court will agree with the characterization and tax treatment as set forth in product supplement STR-1. Accordingly, you are urged to consult your tax advisor regarding all aspects of the U.S. federal income tax consequences of an investment in the notes, including possible alternative characterizations. The discussion in this section and in the section entitled “U.S. Federal Income Tax Summary,” as set forth in product supplement STR-1, assume that there is a significant possibility of a significant loss of principal on an investment in the notes.

Settlement at Maturity or Sale, Exchange, or Redemption Prior to Maturity. Assuming that the notes are properly characterized and treated as callable single financial contracts linked to the Index for U.S. federal income tax purposes, upon receipt of a cash payment at maturity or upon a sale, exchange, or redemption of the notes prior to maturity, a U.S. Holder (as set forth in product supplement STR-1) generally will recognize capital gain or loss equal to the difference between the amount realized and the U.S. Holder’s basis in the notes. This capital gain or loss generally will be long-term capital gain or loss if the U.S. Holder holds the notes for more than one year. The deductibility of capital losses is subject to limitations.

Possible Future Tax Law Changes. On December 7, 2007, the IRS released Notice 2008-2 (“Notice”) seeking comments from the public on the taxation of financial instruments currently taxed as “prepaid forward contracts.” This Notice addresses instruments such as the notes. According to the Notice, the IRS and Treasury are considering whether a holder of an instrument such as the notes should be required to accrue ordinary income on a current basis, regardless of whether any payments are made prior to maturity. It is not possible to determine what guidance the IRS and Treasury will ultimately issue, if any. Any such future guidance may affect the amount, timing, and character of income, gain, or loss in respect of the notes, possibly with retroactive effect. The IRS and Treasury are also considering additional issues, including whether additional gain or loss from such instruments should be treated as ordinary or capital, whether foreign holders of such instruments should be subject to withholding tax on any deemed income accruals, whether Section 1260 of the Internal Revenue Code of 1986, as amended, concerning certain “constructive ownership transactions,” generally applies or should generally apply to such instruments, and whether any of these determinations depend on the nature of the underlying asset. We urge you to consult your own tax advisors concerning the impact and the significance of the above considerations. We intend to continue treating the notes for U.S. federal income tax purposes in the manner described herein unless and until such time as we determine, or the IRS or Treasury determines, that some other treatment is more appropriate.

You should consult your own tax advisor concerning the U.S. federal income tax consequences to you of acquiring, owning, and disposing of the notes, as well as any tax consequences arising under the laws of any state, local, foreign, or other tax jurisdiction and the possible effects of changes in U.S. federal or other tax laws. See the discussion under the section entitled “U.S. Federal Income Tax Summary,” as set forth in product supplement STR-1.

TS-12

Additional Terms

You should read this term sheet, together with the documents listed below, which together contain the terms of the notes and supersede all prior or contemporaneous oral statements as well as any other written materials. You should carefully consider, among other things, the matters set forth under “Risk Factors” in the sections indicated on the cover of this term sheet. The notes involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting, and other advisers before you invest in the notes.

You may access the following documents on the SEC Website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC Website):

| § | Product supplement STR-1 dated January 2, 2009: |

http://www.sec.gov/Archives/edgar/data/70858/000119312509000237/d424b5.htm

| § | Series L MTN prospectus supplement dated April 10, 2008 and prospectus dated May 5, 2006: |

http://www.sec.gov/Archives/edgar/data/70858/000119312508079745/d424b5.htm

Our Central Index Key, or CIK, on the SEC Website is 70858.

We have filed a registration statement (including a product supplement, a prospectus supplement, and a prospectus) with the SEC for the offering to which this term sheet relates. Before you invest, you should read the product supplement, the prospectus supplement, and the prospectus in that registration statement, and the other documents relating to this offering that we have filed with the SEC for more complete information about us and this offering. You may get these documents without cost by visiting EDGAR on the SEC Website at www.sec.gov. Alternatively, we, any agent or any dealer participating in this offering, will arrange to send you the Note Prospectus if you so request by calling MLPF&S toll-free 1-866-500-5408.

Structured Investments Classification

MLPF&S classifies structured investments (the “Structured Investments”), including the notes, into four categories, each with different investment characteristics. The description below is intended to briefly describe the four categories of Structured Investments offered: Principal Protection, Enhanced Income, Market Participation, and Enhanced Participation. A Structured Investment may, however, combine characteristics that are relevant to one or more of the other categories. As such, a category should not be relied upon as a description of any particular Structured Investment.

Principal Protection: Principal Protected Structured Investments offer full or partial principal protection at maturity, while offering market exposure and the opportunity for a better return than may be available from comparable fixed income securities. Principal protection may not be achieved if the investment is sold prior to maturity.

Enhanced Income: Structured Investments offering enhanced income may offer an enhanced income stream through interim fixed or variable coupon payments. However, in exchange for receiving current income, investors may forfeit upside potential on the underlying asset. These investments generally do not include the principal protection feature.

Market Participation: Market Participation Structured Investments can offer investors exposure to specific market sectors, asset classes, and/or strategies that may not be readily available through traditional investment alternatives. Returns obtained from these investments are tied to the performance of the underlying asset. As such, subject to certain fees, the returns will generally reflect any increases or decreases in the value of such assets. These investments are not structured to include the principal protection feature.

Enhanced Participation: Enhanced Participation Structured Investments may offer investors the potential to receive better than market returns on the performance of the underlying asset. Some structures may offer leverage in exchange for a capped or limited upside potential and also in exchange for downside risk. These investments are not structured to include the principal protection feature.

The classification of Structured Investments is meant solely for informational purposes and is not intended to fully describe any particular Structured Investment nor guarantee any particular performance.

TS-13

| Product Supplement No. STR-1 |

||

| (To Prospectus dated May 5, 2006 |

||

| and Series L Prospectus Supplement dated April 10, 2008) |

||

| January 2, 2009 |

Strategic Accelerated Redemption Securities®

| • |

Strategic Accelerated Redemption Securities® (the “notes”) are unsecured senior notes issued by Bank of America Corporation. The notes are not principal protected, and we will not pay interest on the notes. |

| • | This product supplement describes the general terms of the notes and the general manner in which they may be offered and sold. For each offering of the notes, we will provide you with a pricing supplement (which we may refer to as a “term sheet”) that will describe the specific terms of that offering. The term sheet will identify any additions or changes to the terms specified in this product supplement. |

| • | The term sheet will also identify the underlying “Market Measure,” which may be one or more equity-based or commodity-based indices, one or more exchange traded funds, one or more equity securities, commodities, or other assets, any other statistical measure of economic or financial performance, including, but not limited to, any currency, currency index, consumer price index or mortgage index, interest rate, or any combination of the foregoing. We also may describe the Market Measure in an additional supplement to the prospectus, which we refer to as an “index supplement.” |

| • | The notes will be automatically called if the Observation Level (as defined below) of the applicable Market Measure on any Observation Date (as defined below) is greater than or equal to the applicable Call Level (as defined below) for that Observation Date, all as set forth in the applicable term sheet. If the notes are called, you will receive a cash payment for each unit of notes (the “Call Amount”) that will be set forth in the applicable term sheet. If specified in the applicable term sheet, your notes may be “bear notes,” which will be called if the Observation Level of the applicable Market Measure on any Observation Date is less than or equal to the applicable Call Level for that Observation Date. Except where otherwise specifically provided in this product supplement, all references in this product supplement to “notes” shall be deemed to include a reference to bear notes. |

| • | At maturity, if the notes have not been called, for each unit of notes you own, you will receive a cash payment (the “Redemption Amount”) based on the direction of and percentage change in the value of the applicable Market Measure from the Starting Value to the Ending Value (each as defined below), calculated as described in this product supplement. |

| • | If the Ending Value is greater than or equal to (or, in the case of bear notes, less than or equal to) the “Threshold Value” specified in the applicable term sheet, you will receive the Original Offering Price (as defined below) per unit. We will determine the Threshold Value on the pricing date of the notes, which will be the date the notes are priced for initial sale to the public. |

| • | If the Ending Value is less than (or, in the case of bear notes, greater than) the Threshold Value, you will lose a percentage of the principal amount of your notes based on the percentage decline (or, in the case of bear notes, percentage increase) in the value of the Market Measure in excess of the Threshold Value, from the Starting Value to the Ending Value, multiplied by a “Leverage Factor” specified in the applicable term sheet. The applicable Leverage Factor may be 100%. |

| • | The notes will be issued in denominations of whole units. Each unit will have a public offering price as set forth in the applicable term sheet (the “Original Offering Price”). The term sheet may also set forth a minimum number of units that you must purchase. |

| • | If provided for in the applicable term sheet, we may apply to have your notes listed on a securities exchange or quotation system. If approval of such an application is granted, your notes will be listed on the securities exchange or quotation system at the time of such approval. We make no representations, however, that your notes will be listed or, if listed, will remain listed for the entire term of your notes. |

| • | One or more of our affiliates, including Merrill Lynch, Pierce, Fenner & Smith Incorporated (“MLPF&S”), may act as our selling agents to offer the notes. |

The notes are unsecured and are not savings accounts, deposits, or other obligations of a bank. The notes are not guaranteed by Bank of America, N.A. or any other bank, are not insured by the Federal Deposit Insurance Corporation or any other governmental agency and involve investment risks. Potential purchasers of the notes should consider the information in “Risk Factors ” beginning on page S-10. You may lose some or all of your investment in the notes.

None of the Securities and Exchange Commission (the “SEC”), any state securities commission, or any other regulatory body has approved or disapproved of these notes or passed upon the adequacy or accuracy of this product supplement, the prospectus supplement, or the prospectus. Any representation to the contrary is a criminal offense.

Merrill Lynch & Co.

| Page | ||

| S-3 | ||

| S-10 | ||

| S-23 | ||

| S-24 | ||

| S-41 | ||

| S-41 | ||

| S-48 | ||

Strategic Accelerated Redemption Securities® is a registered service mark of our subsidiary, Merrill Lynch & Co., Inc.

S-2

This product supplement relates only to the notes and does not relate to any underlying asset that comprises the Market Measure described in any term sheet. This summary includes questions and answers that highlight selected information from the prospectus, prospectus supplement, and this product supplement to help you understand the notes. You should read carefully the entire prospectus, prospectus supplement, and product supplement, together with the applicable term sheet and any applicable index supplement, to understand fully the terms of your notes, as well as the tax and other considerations important to you in making a decision about whether to invest in any notes. In particular, you should review carefully the section in this product supplement entitled “Risk Factors,” which highlights a number of risks of an investment in the notes, to determine whether an investment in the notes is appropriate for you. If information in this product supplement is inconsistent with the prospectus or prospectus supplement, this product supplement will supersede those documents. However, if information in any term sheet or index supplement is inconsistent with this product supplement, that term sheet or index supplement will supersede this product supplement.

Certain capitalized terms used and not defined in this product supplement have the meanings ascribed to them in the prospectus supplement and prospectus.

In light of the complexity of the transactions described in this product supplement, you are urged to consult with your own attorneys and business and tax advisors before making a decision to purchase any notes.

The information in this “Summary” section is qualified in its entirety by the more detailed explanation set forth elsewhere in this product supplement, the prospectus supplement, and prospectus, as well as the applicable term sheet and any index supplement. You should rely only on the information contained in those documents. We have not authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. Neither we nor any selling agent is making an offer to sell the notes in any jurisdiction where the offer or sale is not permitted. You should assume that the information in this product supplement, the prospectus supplement, and prospectus, together with the term sheet and any index supplement, is accurate only as of the date on their respective front covers.

What are the notes?

The notes are senior debt securities issued by Bank of America Corporation, and are not secured by collateral. The notes will rank equally with all of our other unsecured senior indebtedness from time to time outstanding, and any payments due on the notes, including any repayment of principal, will be subject to our credit risk. Each series of notes will mature on the date set forth in the applicable term sheet, unless we call the notes on an earlier date, as described in this product supplement and in the applicable term sheet. The notes are not principal protected.

The notes are designed for investors who seek an early exit prior to maturity at a premium if the value of the applicable Market Measure (such as the level of an index or the price of a share of an exchange traded fund) is at or above (or, in the case of bear notes, at or below) its applicable Call Level on the relevant Observation Date. You should be willing to lose some or all of your principal if the notes are not called prior to their maturity, and the applicable Market Measure has declined below (or, in the case of bear notes, has increased above) the Threshold Value on the final Observation Date shortly before the maturity date. The notes may or may not pay periodic interest. Unless specified in the applicable term sheet, your notes will not pay interest. You must be willing to forgo interest payments on your investment (such as fixed or floating interest rates paid on conventional non-callable debt securities) if the

S-3

notes are non-interest bearing, accept a return that will not exceed the Call Amount, and bear the risk of loss of all or substantially all of your investment. You should also be aware that the automatic call feature may shorten the term of an investment in the notes, and be willing to accept that your notes may be called on any Observation Date. The Call Level, Observation Dates, Threshold Value, and Call Amount will be set forth in the applicable term sheet.

Are the notes equity or debt securities?

The notes are our senior debt securities. However, the notes will differ from traditional debt securities in that their return is linked to the performance of the underlying Market Measure, they will not be principal protected, and unless otherwise specified in the applicable term sheet, you will not receive interest payments.

If the notes are called prior to the maturity date, the total cash amount that you will receive as payment on the notes will equal the Call Amount specified in the applicable term sheet. If the notes are not called prior to the maturity date, you may receive an amount that is less than the Original Offering Price, depending upon the performance of the Market Measure over the term of the notes. We describe below how this amount at maturity is determined.

Will you receive interest on the notes?

Unless otherwise specified in the applicable term sheet, you will not receive any interest payments on the notes. If the applicable term sheet provides for the payment of interest on the notes, the applicable term sheet will indicate the relevant terms on which you will receive interest payments. See “Description of the Notes—Interest.”

Is it possible for you to lose some or all of your investment in the notes?

Yes. Unless the applicable term sheet provides for the payment of interest on the notes, you will only earn a positive return on your notes if they are automatically called prior to their maturity date, as described in this product supplement and the applicable term sheet. If your notes are not called prior to maturity, your investment in the notes will not yield a positive return.

Further, if the Ending Value is less than (or, in the case of bear notes, greater than) the applicable Threshold Value on the final Observation Date shortly before the maturity date, then you will receive at maturity a cash amount that is less than the Original Offering Price of your notes.

As a result, you may lose all or a substantial portion of the amount that you invested to purchase the notes. Further, if you sell the notes prior to maturity, you may find that the market value per unit is less than the Original Offering Price.

What is the Market Measure?

The Market Measure may consist of one or more of the following:

| • | U.S. broad-based equity indices; |

| • | U.S. sector or style-based equity indices; |

| • | non-U.S. or global equity indices; |

| • | commodity-based indices; |

S-4

| • | exchange traded funds; |

| • | the value of one or more commodities, equity securities, or other assets; |

| • | any other statistical measure of U.S. or non-U.S. economic or financial performance, including, but not limited to, any currency or currency index, consumer price index, mortgage index, or interest rate; or |

| • | any combination of any of the above. |

The Market Measure may consist of a group, or “Basket,” of the foregoing. We refer to each component included in any Basket as a “Basket Component.” If the Market Measure to which your notes are linked is a Basket, the Basket Components will be set forth in the applicable term sheet.

The applicable term sheet or index supplement will set forth information as to the specific Market Measure, including information as to the historical values of the Market Measure. However, historical values of the Market Measure are not indicative of the future performance of the Market Measure or the performance of your notes.

Under what circumstances will the notes be called?

The notes will automatically be called on an Observation Date if the Observation Level of the Market Measure on that Observation Date is greater than or equal to (or, in the case of bear notes, is less than or equal to) the applicable Call Level set forth in the applicable term sheet. We cannot otherwise redeem the notes at any earlier date.

What will you receive if we call the notes?

If your notes are called, you will receive the Call Amount applicable to such Observation Date. The Call Amount will be equal to the Original Offering Price per unit plus the Call Premium. The “Call Premium” will be a percentage of the Original Offering Price that will be set forth in the applicable term sheet. If the notes are automatically called on an Observation Date other than the final Observation Date, we will redeem each note and pay the applicable Call Amount on the fifth Banking Business Day (as defined below) after the applicable Observation Date, subject to postponement as described in the section entitled “Description of the Notes—Automatic Call.” If the Notes are called on the final Observation Date, we will redeem each Note and pay the Call Amount on the maturity date.

S-5

How is the payment at maturity calculated?

If your notes are not called, then at maturity, subject to our credit risk as issuer of the notes, and unless the applicable term sheet provides otherwise, you will receive the Redemption Amount per unit of notes that you hold, denominated in U.S. dollars. The Redemption Amount will be calculated as follows:

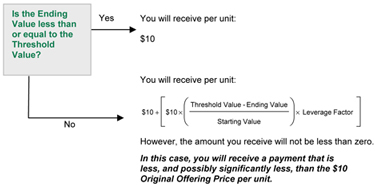

| • | If the Ending Value is equal to or greater than the Threshold Value, then the Redemption Amount will equal the Original Offering Price per unit; or |

| • | If the Ending Value is less than the Threshold Value, then the Redemption Amount will equal: |

| Original Offering Price + | (

|

Original Offering Price x | (

|

Ending Value - Threshold Value | )

|

x Leverage Factor | )

|

|||||||||||

| Starting Value |

In the case of bear notes, the Redemption Amount will be calculated as follows:

| • | If the Ending Value is equal to or less than the Threshold Value, then the Redemption Amount will equal the Original Offering Price; or |

| • | If the Ending Value is greater than the Threshold Value, then the Redemption Amount will equal: |

| Original Offering Price + | (

|

Original Offering Price x | (

|

Threshold Value - Ending Value | )

|

x Leverage Factor | )

|

|||||||||||

| Starting Value |

The “Threshold Value” will represent a percentage of the Starting Value, and will be determined on the pricing date and set forth in the applicable term sheet. If the Threshold Value is equal to 100% of the Starting Value, then the Redemption Amount for each note will be less than the Original Offering Price if there is any decrease (or, in the case of bear notes, increase) in the value of the Market Measure from the Starting Value to the Ending Value.

The “Leverage Factor” represents a percentage of any decline (or, in the case of bear notes, an increase) beyond the Threshold Value that will be reflected in the Redemption Amount, and will be set forth in the applicable term sheet. The Leverage Factor may equal 100%, but will not be greater than a number that, considering the Threshold Value, could cause you to lose more than your entire investment in the notes.

Unlike ordinary debt securities, the notes are not principal protected, and you may receive a Redemption Amount that is less than the Original Offering Price of your notes. In either case, in no event will the Redemption Amount be less than zero.

How will the Starting Value, Ending Value, and Observation Level be determined?

Unless otherwise specified in the applicable term sheet, the “Starting Value” will be:

| • | as to Market Measures other than exchange traded funds, the closing value of the Market Measure or a percentage of the closing value of the Market Measure on the pricing date (or on such date or dates other than the pricing date as specified in the applicable term sheet) as determined by the calculation agent; provided, however, that if the Market Measure is linked to one or more commodities or commodity |

S-6

| indices, and a Market Disruption Event (as defined below) occurs on the pricing date, then the calculation agent will establish the Starting Value as set forth in the section “Description of the Notes—Determining the Observation Level, the Starting Value, and the Ending Value”; and |

| • | as to exchange traded fund Market Measures, the volume weighted average price, which is, absent a determination of manifest error, the price shown on page “AQR” on Bloomberg L.P. for trading in shares of the Market Measure taking place between approximately 9:30 a.m. to 4:02 p.m. on all U.S. exchanges on the pricing date, or on such date or dates other than the pricing date as specified in the applicable term sheet. |

If the Market Measure consists of a Basket, the “Starting Value” will be equal to 100. We will assign each Basket Component a weighting (the “Initial Component Weight”) so that each Basket Component represents a percentage of the Starting Value on the pricing date. We may assign the Basket Components equal Initial Component Weights, or we may assign the Basket Components unequal Initial Component Weights. The Initial Component Weight for each Basket Component will be set forth in the applicable term sheet. See “Description of the Notes—Basket Market Measures.”

Unless otherwise specified in the applicable term sheet, the “Ending Value” will be:

| • | as to Market Measures other than exchange traded funds, the closing value of the Market Measure on the final Observation Date; and |

| • | as to exchange traded fund Market Measures, the Closing Market Price (as defined below) of the Market Measure on the final Observation Date multiplied by the Price Multiplier (as defined below). |

Unless otherwise specified in the applicable term sheet, the “Observation Level” will be:

| • | as to Market Measures other than exchange traded funds, the closing value of the Market Measure on any Observation Date; and |

| • | as to exchange traded fund Market Measures, the Closing Market Price of the Market Measure on any Observation Date multiplied by the Price Multiplier. |

See “Description of the Notes—Determining the Observation Level, the Starting Value, and the Ending Value.”

Is the return on the notes limited in any way?

Yes. Unless the applicable term sheet provides for the payment of interest on the notes, you will only receive a positive return on the notes if your notes are called. Even if the notes are called, unless otherwise provided in the applicable term sheet, your return on the notes will be limited to the Original Offering Price plus the applicable Call Premium. As a result, your participation in any upside potential (or, in the case of bear notes, downside potential) of the Market Measure underlying your notes will not be greater than the Call Premium. Each term sheet will set forth examples of hypothetical Ending Values, Call Levels, and Threshold Values, and the impact of the call feature on your notes.

S-7

Who will determine the amounts payable on notes?

The calculation agent will make all the calculations associated with the notes, such as determining the Observation Level, the Starting Value, the Ending Value, the Threshold Value, the Call Level, and the Redemption Amount. Unless otherwise set forth in the applicable term sheet, we will appoint our affiliate, MLPF&S, or one of our other affiliates, to act as calculation agent for the notes. See the section entitled “Description of the Notes—Role of the Calculation Agent.”

Will you have an ownership interest in the securities, commodities, or other assets that are represented by the Market Measure?

No. An investment in the notes does not entitle you to any ownership interest, including any voting rights, dividends paid, interest payments, or other distributions, in the securities of any of the companies included in an equity-based Market Measure or in an exchange traded fund Market Measure, or in any futures contract for a commodity included in the Market Measure. If the Market Measure is not an exchange traded fund Market Measure, or is not equity-based or commodity-based, you similarly will not have any right to receive the relevant asset underlying the Market Measure. The notes will be payable only in U.S. dollars.

Who are the selling agents for the notes?

One or more of our affiliates, including MLPF&S, will act as our selling agents in connection with each offering of the notes and will receive a commission or underwriting discount based on the number of units of the notes sold. None of the selling agents is your fiduciary or advisor, and you should not rely upon any communication from it in connection with the notes as investment advice or a recommendation to purchase the notes. You should make your own investment decision regarding the notes after consulting with your legal, tax, and other advisors.

How are the notes being offered?

We have registered the notes with the SEC in the United States. However, we will not register the notes for public distribution in any jurisdiction other than the United States. The selling agents may solicit offers to purchase the notes from non-U.S. investors in reliance on available private placement exemptions. See the section entitled “Supplemental Plan of Distribution—Selling Restrictions” in the prospectus supplement.

Will the notes be listed on an exchange?

If provided for in the applicable term sheet, we will apply to have your notes listed on a securities exchange or quotation system. If approval of such an application is granted, your notes will be listed on the securities exchange or quotation system at the time of such approval. We make no representations, however, that your notes will be listed or, if listed, will remain listed for the entire term of your notes.

Can the maturity date be postponed if a Market Disruption Event occurs?

No. See the section entitled “Description of the Notes—Market Disruption Events.”

Does ERISA impose any limitations on purchases of the notes?

Yes. An employee benefit plan subject to the fiduciary responsibility provisions of the Employee Retirement Income Security Act of 1974, as amended (commonly referred to as

S-8

“ERISA”), or a plan that is subject to Section 4975 of the Internal Revenue Code of 1986, as amended, or the “Code,” including individual retirement accounts, individual retirement annuities, or Keogh plans, or any entity the assets of which are deemed to be “plan assets” under the ERISA regulations, should not purchase, hold, or dispose of the notes unless that plan or entity has determined that its purchase, holding, or disposition of the notes will not constitute a prohibited transaction under ERISA or Section 4975 of the Code.

Any plan or entity purchasing the notes will be deemed to be representing that it has made that determination, or that a prohibited transaction class exemption (“PTCE”) or other statutory or administrative exemption exists and can be relied upon by such plan or entity. See the section entitled “ERISA Considerations.”

Are there any risks associated with your investment?

Yes. An investment in the notes is subject to risk. The notes are not principal protected. Please refer to the section entitled “Risk Factors” beginning on page S-10 of this product supplement and page S-4 of the prospectus supplement. If the applicable term sheet or index supplement sets forth any additional risk factors, you should read those carefully before purchasing any notes.

S-9

Your investment in the notes entails significant risks. Your decision to purchase the notes should be made only after carefully considering the risks of an investment in the notes, including those discussed below, with your advisors in light of your particular circumstances. The notes are not an appropriate investment for you if you are not knowledgeable about significant elements of the notes or financial matters in general.

General Risks Relating to the Notes