Filed Pursuant to Rule 433

Registration No. 333-158663

Subject to Completion

Preliminary Term Sheet dated May 23, 2011

The ARNs® are being offered by Bank of America Corporation (“BAC”). The ARNs will have the terms specified in this term sheet as supplemented by the documents indicated below under “Additional Terms” (together, the “Note Prospectus”). Investing in the ARNs involves a number of risks. There are important differences between the ARNs and a conventional debt security, including different investment risks. See “Risk Factors” and “Additional Risk Factors” beginning on page TS-5 of this term sheet and “Risk Factors” beginning on page S-10 of product supplement ARN-3. The ARNs:

|

Are Not FDIC Insured |

Are Not Bank Guaranteed |

May Lose Value |

In connection with this offering, Merrill Lynch, Pierce, Fenner & Smith Incorporated (“MLPF&S”) is acting in its capacity as principal for your account.

None of the Securities and Exchange Commission (the “SEC”), any state securities commission, or any other regulatory body has approved or disapproved of these securities or determined if this Note Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Unit |

Total |

|||||||

| Public offering price (1) |

$10.00 | $ | ||||||

| Underwriting discount (1) |

$ 0.20 | $ | ||||||

| Proceeds, before expenses, to Bank of America Corporation |

$ 9.80 | $ | ||||||

| (1) | The public offering price and underwriting discount for any purchase of 500,000 units or more in a single transaction by an individual investor will be $9.95 per unit and $0.15 per unit, respectively. The public offering price and underwriting discount for any purchase by certain fee-based trusts and fee-based discretionary accounts managed by U.S. Trust operating through Bank of America, N.A. will be $9.80 per unit and $0.00 per unit, respectively. |

* Depending on the date the ARNs are priced for initial sale to the public (the “pricing date”), any reference in this term sheet to the month in which the pricing date, settlement date, or maturity date will occur is subject to change.

| Merrill Lynch & Co.

May , 2011 |

| |||

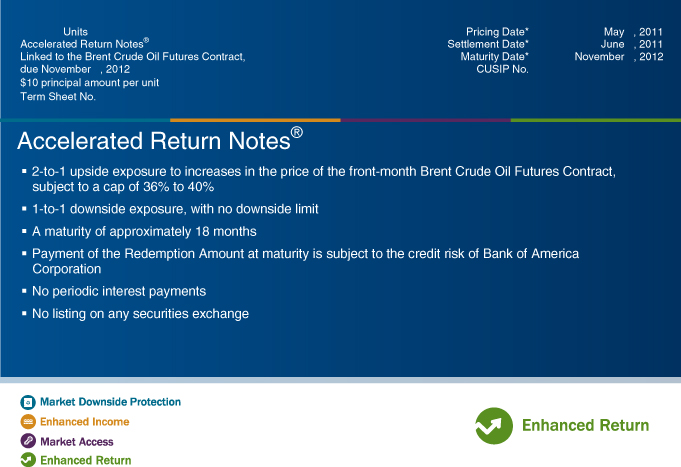

UnitAccelerated Return Notes®

Linked to the Brent Crude Oil Futures Contract,

due November , 2012

$10 principal amount per unit

Term Sheet No.

Pricing Date*

Settlement Date*

Maturity Date*

CUSIP No.

May , 2011

June , 2011

November , 2012

Accelerated Return Notes®

2-to-1 upside exposure to increases in the price of the front-month Brent Crude Oil Futures Contract, subject to a cap of 36% to 40%

1-to-1 downside exposure, with no downside limit

A maturity of approximately 18 months

Payment of the Redemption Amount at maturity is subject to the credit risk of Bank of America Corporation

No periodic interest payments

No listing on any securities exchange market downside protection enhanced income market access enhancedreturn

Summary

The Accelerated Return Notes® Linked to the Brent Crude Oil Futures Contract, due November , 2012 (the “ARNs”) are our senior unsecured debt securities. The ARNs are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The ARNs will rank equally with all of our other unsecured and unsubordinated debt, and any payments due on the ARNs, including any repayment of principal, will be subject to the credit risk of BAC. The ARNs provide a leveraged return for investors, subject to a cap, if the price of Brent blend crude oil, as measured by the price of the Brent Crude Oil Futures Contract (as defined and described below), increases moderately from the Starting Value, determined on the pricing date, to the Ending Value, determined on a calculation day shortly before the maturity date. Investors must be willing to forgo interest payments on the ARNs and be willing to accept a return that is capped or a repayment that is less, and potentially significantly less, than the Original Offering Price.

Capitalized terms used but not defined in this term sheet have the meanings set forth in product supplement ARN-3. Unless otherwise indicated or unless the context requires otherwise, all references in this document to “we,” “us,” “our,” or similar references are to BAC.

|

Accelerated Return Notes® |

TS-2 |

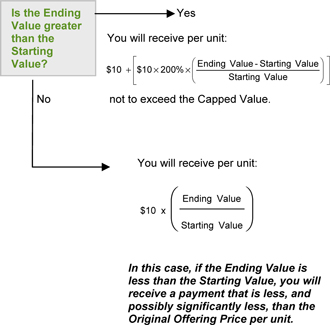

Hypothetical Payout Profile

|

This graph reflects the hypothetical returns on the ARNs, based on

the

This graph has been prepared for purposes of illustration only. Your |

Hypothetical Redemption Amounts

Examples

Set forth below are three examples of Redemption Amount calculations (rounded to two decimal places) payable at maturity, based upon the Participation Rate of 200%, a hypothetical Starting Value of 111.42 (the official settlement price of the Brent Crude Oil Futures Contract on May 19, 2011), and a hypothetical Capped Value of $13.80 per unit, the midpoint of the Capped Value range of $13.60 to $14.00.

Example 1 — The hypothetical Ending Value is 80% of the hypothetical Starting Value:

| Hypothetical Starting Value: |

111.42 | |||||

| Hypothetical Ending Value: |

89.14 |

| $10 |

× | ( | 89.14 | ) | = $8.00 | |||||||||

| 111.42 |

Hypothetical Redemption Amount (per unit) = $8.00

Example 2 — The hypothetical Ending Value is 104% of the hypothetical Starting Value:

| Hypothetical Starting Value: |

111.42 | |||||

| Hypothetical Ending Value: |

115.88 |

| $10 + |

[ | $10 × 200% × | ( | 115.88 – 111.42 | ) | ] | = $10.80 | |||||||||||

| 111.42 |

Hypothetical Redemption Amount (per unit) = $10.80

Example 3 — The hypothetical Ending Value is 150% of the hypothetical Starting Value:

| Hypothetical Starting Value: |

111.42 | |||||

| Hypothetical Ending Value: |

167.13 |

| $10 + |

[ | $10 × 200% × | ( | 167.13 – 111.42 | ) | ] | = $20.00 | |||||||||||

| 111.42 |

Hypothetical Redemption Amount (per unit) = $13.80 (The Redemption Amount cannot be greater than the Capped Value.)

|

Accelerated Return Notes® |

TS-3 |

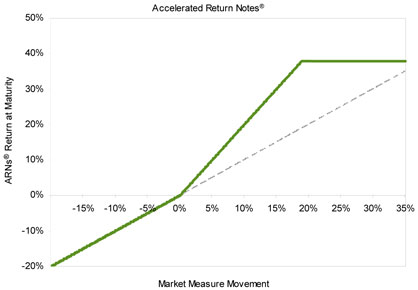

The following table illustrates, for a hypothetical Starting Value of 111.42 (the official settlement price of the Brent Crude Oil Futures Contract on May 19, 2011) and a range of hypothetical Ending Values:

| § | the percentage change from the hypothetical Starting Value to the hypothetical Ending Value; |

| § | the hypothetical Redemption Amount per unit of the ARNs (rounded to two decimal places); and |

| § | the hypothetical total rate of return to holders of the ARNs. |

The table below is based on the Participation Rate of 200% and a hypothetical Capped Value of $13.80 (per unit), the midpoint of the Capped Value range of $13.60 to $14.00.

| Hypothetical |

Percentage Change from the Hypothetical Starting |

Hypothetical |

Hypothetical | |||||||||||||||

| 55.71 | -50.00 | % | $5.00 | -50.00 | % | |||||||||||||

| 66.85 | -40.00 | % | $6.00 | -40.00 | % | |||||||||||||

| 77.99 | -30.00 | % | $7.00 | -30.00 | % | |||||||||||||

| 89.14 | -20.00 | % | $8.00 | -20.00 | % | |||||||||||||

| 100.28 | -10.00 | % | $9.00 | -10.00 | % | |||||||||||||

| 102.51 | -8.00 | % | $9.20 | -8.00 | % | |||||||||||||

| 104.73 | -6.00 | % | $9.40 | -6.00 | % | |||||||||||||

| 106.96 | -4.00 | % | $9.60 | -4.00 | % | |||||||||||||

| 109.19 | -2.00 | % | $9.80 | -2.00 | % | |||||||||||||

| 111.42 | (1) | 0.00 | % | $10.00 | 0.00 | % | ||||||||||||

| 113.65 | 2.00 | % | $10.40 | 4.00 | % | |||||||||||||

| 115.88 | 4.00 | % | $10.80 | 8.00 | % | |||||||||||||

| 118.11 | 6.00 | % | $11.20 | 12.00 | % | |||||||||||||

| 120.33 | 8.00 | % | $11.60 | 16.00 | % | |||||||||||||

| 122.56 | 10.00 | % | $12.00 | 20.00 | % | |||||||||||||

| 133.70 | 20.00 | % | $13.80 | (2) | 38.00 | % | ||||||||||||

| 144.85 | 30.00 | % | $13.80 | 38.00 | % | |||||||||||||

| 155.99 | 40.00 | % | $13.80 | 38.00 | % | |||||||||||||

| 167.13 | 50.00 | % | $13.80 | 38.00 | % | |||||||||||||

| (1) | This is the hypothetical Starting Value, which was the official settlement price of the Brent Crude Oil Futures Contract on May 19, 2011. The actual Starting Value will be determined on the pricing date and set forth in the final term sheet that will be made available in connection with sales of the ARNs. |

| (2) | The Redemption Amount per unit of the ARNs cannot exceed the hypothetical Capped Value of $13.80 (the midpoint of the Capped Value range of $13.60 to $14.00). The actual Capped Value will be determined on the pricing date and set forth in the final term sheet that will be made available in connection with sales of the ARNs. |

The above figures are for purposes of illustration only. The actual amount you receive and the resulting total rate of return will depend on the actual Starting Value, Ending Value, Capped Value, and the term of your investment.

|

Accelerated Return Notes® |

TS-4 |

Risk Factors

There are important differences between the ARNs and a conventional debt security. An investment in the ARNs involves significant risks, including those listed below. You should carefully review the more detailed explanation of risks relating to the ARNs in the “Risk Factors” sections beginning on page S-10 of product supplement ARN-3 and page S-4 of the MTN prospectus supplement identified below under “Additional Terms.” We also urge you to consult your investment, legal, tax, accounting, and other advisors before you invest in the ARNs.

| § | Your investment may result in a loss; there is no guaranteed return of principal. |

| § | Your yield may be less than the yield on a conventional debt security of comparable maturity. |

| § | Your investment return, if any, is limited to the return represented by the Capped Value. |

| § | Your investment return, if any, may be less than a comparable investment directly in the Brent Crude Oil Futures Contract. |

| § | You must rely on your own evaluation of the merits of an investment linked to the price of the Brent Crude Oil Futures Contract. |

| § | In seeking to provide you with what we believe to be commercially reasonable terms for the ARNs while providing the selling agent with compensation for its services, we have considered the costs of developing, hedging, and distributing the ARNs. |

| § | A trading market is not expected to develop for the ARNs. MLPF&S is not obligated to make a market for, or to repurchase, the ARNs. |

| § | The Redemption Amount will not be affected by all developments relating to the Brent Crude Oil Futures Contract. |

| § | Ownership of the ARNs will not entitle you to any rights with respect to the Brent Crude Oil Futures Contract or any related futures contracts. |

| § | If you attempt to sell the ARNs prior to maturity, their market value, if any, will be affected by various factors that interrelate in complex ways, and their market value may be less than the Original Offering Price. |

| § | Payments on the ARNs are subject to our credit risk, and changes in our credit ratings are expected to affect the value of the ARNs. |

| § | The price of the Brent Crude Oil Futures Contract may change unpredictably, affecting the value of the ARNs in unforeseeable ways. |

| § | Suspensions or disruptions of trading in the Brent Crude Oil Futures Contract and related futures markets may adversely affect the value of the ARNs. |

| § | The ARNs will not be regulated by the U.S. Commodity Futures Trading Commission. |

| § | Trading by us and our affiliates in related futures and options contracts may affect your return. |

| § | Our trading and hedging activities may create conflicts of interest with you. |

| § | Our hedging activities may affect your return on the ARNs and their market value. |

| § | There may be potential conflicts of interest involving the calculation agent. We have the right to appoint and remove the calculation agent. |

| § | The U.S. federal income tax consequences of the ARNs are uncertain, and may be adverse to a holder of ARNs. See “Summary Tax Consequences” and “Certain U.S. Federal Income Taxation Considerations” below and “U.S. Federal Income Tax Summary” beginning on page S-43 of product supplement ARN-3. |

Additional Risk Factors

The price movements in the Brent Crude Oil Futures Contract may not correlate with changes in Brent crude oil’s spot price

The Brent Crude Oil Futures Contract is a futures contract for Brent blend crude oil that trades on the ICE. Unlike equities, which typically entitle the holder to a continuing stake in a corporation, a commodity futures contract is typically an agreement to buy a set amount of an underlying physical commodity at a predetermined price during a stated delivery period. A futures contract reflects the expected value of the underlying physical commodity upon delivery in the future. In contrast, the underlying physical commodity’s current or “spot” price reflects the immediate delivery value of the commodity.

The ARNs are linked to the Brent Crude Oil Futures Contract and not to the spot price of Brent crude oil, and an investment in the ARNs is not the same as buying and holding Brent crude oil. While price movements in the Brent Crude Oil Futures Contract may correlate with changes in Brent crude oil’s spot price, the correlation will not be perfect and price movements in the spot market for Brent crude oil may not be reflected in the futures market (and vice versa). Accordingly, an increase in the spot price of Brent crude oil may not result in an increase in the price of the Brent Crude Oil Futures Contract. The value of the Brent Crude Oil Futures Contract may decrease while the spot price for Brent crude oil remains stable or increases, or does not decrease to the same extent.

The market value of the ARNs may be affected by price movements in distant-delivery futures contracts associated with the Brent Crude Oil Futures Contract.

The price movements in the Brent Crude Oil Futures Contract may not be reflected in the market value of the ARNs. If you are able to sell your ARNs, the price you receive could be affected by changes in the values of futures contracts for Brent crude oil that have more distant delivery dates than the Brent Crude Oil Futures Contract. The prices for these distant-delivery futures contracts may not increase to the same extent as the prices of the Brent Crude Oil Futures Contract, or may decrease to a greater extent, which may adversely affect the value of the ARNs.

The ARNs include the risk of a concentrated position in a single commodity.

The ARNs are linked to a single exchange-traded physical commodity underlying the Brent Crude Oil Futures Contract, Brent crude oil. An investment in the ARNs may therefore carry risks similar to a concentrated investment in a single commodity. Accordingly, a decline in the value of Brent crude oil may adversely affect the price of the Brent Crude Oil Futures Contract and the value of the ARNs. Technological advances or the discovery of new oil reserves could lead to increases in worldwide production of oil and corresponding decreases in the price of Brent crude oil. In addition, further development and commercial exploitation of alternative energy sources and technologies, including solar, wind, or geothermal energy and hybrid and electric automobiles, could reduce the demand for Brent crude oil and result in lower prices. As a result of any of these events, the value of the ARNs could decrease.

|

Accelerated Return Notes® |

TS-5 |

Crude oil prices can be volatile as a result of various factors that we cannot control, and this volatility may reduce the value of the ARNs.

Historically, oil prices have been highly volatile. They are affected by numerous factors, including oil supply and demand, the level of global industrial activity, the driving habits of consumers, political events and policies, regulations, weather, fiscal, monetary and exchange control programs, and, especially, direct government intervention such as embargoes, and supply disruptions in major producing or consuming regions such as the Middle East, the United States, Latin America, and Russia. The outcome of meetings of the Organization of Petroleum Exporting Countries also can affect liquidity and world oil supply and, consequently, the value of the Brent Crude Oil Futures Contract. Market expectations about these events and speculative activity also may cause oil prices to fluctuate unpredictably. If the volatility of Brent crude oil and the Brent Crude Oil Futures Contract increases or decreases, the value of the ARNs may be adversely affected.

Furthermore, a significant proportion of world oil production capacity is controlled by a small number of producers. These producers have, in certain recent periods, implemented curtailments of output and trade. These efforts at supply curtailment, or the cessation of supply, could affect the value of the Brent Crude Oil Futures Contract. Additionally, the development of substitute products for oil could adversely affect the value of the Brent Crude Oil Futures Contract and the value of the ARNs.

The policies of the ICE are subject to change, in a manner which may reduce the value of the ARNs.

The policies of the ICE concerning the manner in which the price of Brent crude oil is calculated may change in the future. The ICE is not our affiliate, and we have no ability to control or predict the actions of the ICE. The ICE may also from time to time change its rules or bylaws or take emergency action under its rules. The ICE may discontinue or suspend calculation or dissemination of information relating to the Brent Crude Oil Futures Contract. Any such actions could affect the price of the Brent Crude Oil Futures Contract, and therefore, the value of the ARNs.

|

Accelerated Return Notes® |

TS-6 |

Other Terms of the ARNs

The following definition shall supersede and replace the definition of “Market Disruption Event” set forth on page S-30 of product supplement ARN-3.

A “Market Disruption Event” means any of the following events as determined by the calculation agent:

| (A) | the suspension of, or material limitation on, trading in Brent crude oil, or futures contracts or options related to Brent crude oil, on the Relevant Market (as defined below); |

| (B) | the failure of trading to commence, permanent discontinuance of trading, or a discontinuance of trading at or within 15 minutes of the close, in Brent crude oil, or futures contracts or options related to Brent crude oil, on the Relevant Market; |

| (C) | the failure of the ICE to calculate or publish the official settlement price of Brent crude oil for that day (or the information necessary for determining the official settlement prices); or |

| (D) | any other event which the calculation agent determines, in its sole discretion, materially interferes with its ability or the ability of any of its affiliates to unwind all or a material portion of a hedge that the calculation agent or its affiliates have effected or may effect in connection with the ARNs. |

For the purpose of determining whether a Market Disruption Event has occurred:

| (A) | a limitation on the hours in a trading day and/or number of days of trading will not constitute a Market Disruption Event if it results from an announced change in the regular trading hours of the Relevant Market; and |

| (B) | a suspension of or material limitation on trading in the Relevant Market will not include any time when trading is not conducted or prices are not quoted by the ICE in the Relevant Market under ordinary circumstances. |

“Relevant Market” means the market on which members of the ICE, or any successor thereto, quote prices for the buying and selling of Brent crude oil, or if such market is no longer the principal trading market for Brent crude oil or options or futures contracts for Brent crude oil, such other exchange or principal trading market for Brent crude oil, as determined in good faith by the calculation agent, which serves as the source of prices for Brent crude oil, and any principal exchanges where options or futures contracts on Brent crude oil are traded.

|

Accelerated Return Notes® |

TS-7 |

Investor Considerations

Other Provisions

We may deliver the ARNs against payment therefor in New York, New York on a date that is greater than three business days following the pricing date. Under Rule 15c6-1 of the Securities Exchange Act of 1934, trades in the secondary market generally are required to settle in three business days, unless the parties to any such trade expressly agree otherwise. Accordingly, if the initial settlement of the ARNs occurs more than three business days from the pricing date, purchasers who wish to trade the ARNs more than three business days prior to the original issue date will be required to specify alternative settlement arrangements to prevent a failed settlement.

If you place an order to purchase the ARNs, you are consenting to MLPF&S acting as a principal in effecting the transaction for your account.

Supplement to the Plan of Distribution; Conflicts of Interest

MLPF&S, a broker-dealer subsidiary of BAC, is a member of the Financial Industry Regulatory Authority, Inc. (“FINRA”) and will participate as selling agent in the distribution of the ARNs. Accordingly, offerings of the ARNs will conform to the requirements of FINRA Rule 5121. Under our distribution agreement with MLPF&S, MLPF&S will purchase the ARNs from us on the issue date as principal at the purchase price indicated on the cover of this term sheet, less the indicated underwriting discount. MLPF&S will not receive an underwriting discount for ARNs sold to certain fee-based trusts and fee-based discretionary accounts managed by U.S. Trust operating through Bank of America, N.A. In the original offering of the ARNs, the ARNs will be sold in minimum investment amounts of 100 units.

MLPF&S may use this Note Prospectus for offers and sales in secondary market transactions and market-making transactions in the ARNs but is not obligated to engage in such secondary market transactions and/or market-making transactions. MLPF&S may act as principal or agent in these transactions, and any such sales will be made at prices related to prevailing market prices at the time of the sale.

|

Accelerated Return Notes® |

TS-8 |

The Brent Crude Oil Futures Contract

We have derived all information regarding the Brent Crude Oil Futures Contract and the ICE from publicly available sources. Such information reflects the policies of, and is subject to change without notice by, the ICE. The consequences of ICE discontinuing trading in the Brent Crude Oil Futures Contract are discussed in the section of product supplement ARN-3 beginning on page S-36 entitled “Description of ARNs—Discontinuance of a Market Measure.” None of us, the calculation agent, or the selling agent accepts any responsibility for the calculation or dissemination of information relating to the Brent Crude Oil Futures Contract.

The Futures Market

An exchange-traded futures contract, such as the Brent Crude Oil Futures Contract, provides for the future purchase and sale of a specified type and quantity of a commodity, at a particular price and on a specific date. Futures contracts are standardized so that each investor trades contracts with the same requirements as to quality, quantity, and delivery terms. Rather than settlement by physical delivery of the commodity, futures contracts may be settled for the cash value of the right to receive or sell the specified commodity on the specified date. Exchange-traded futures contracts are traded on organized exchanges such as ICE, known as “contract markets,” through the facilities of a centralized clearing house and a brokerage firm which is a member of the clearing house.

The ICE Futures Europe

IntercontinentalExchange, Inc. was established in May 2000. Its founding shareholders represented some of the world’s largest energy traders. In June 2001, IntercontinentalExchange, Inc expanded its business into futures trading by acquiring the International Petroleum Exchange (the “IPE”), now ICE Futures, which operated Europe’s leading open-outcry energy futures exchange. Since 2003, ICE has partnered with the Chicago Climate Exchange to host its electronic marketplace. In April 2005, the entire ICE portfolio of energy futures became fully electronic.

IPE, the predecessor of ICE Futures was established in London in 1980 as a traditional open-cry auction market by a group of energy and trading companies. The IPE launched the gas oil futures contracts in 1981, followed by the brent crude oil futures contract in 1988 and the natural gas futures contract in 1997.

ICE Futures is a “Recognized Investment Exchange” in the United Kingdom and is regulated by the U.K. Financial Services Authority. Trading in futures and options is offered exclusively electronically, and access to the trading platform is offered directly via the Internet, through private telecommunications lines, through an independent software vendor, or through an ICE Futures exchange member’s own system.

The Brent Crude Oil Futures Contract

The “Brent Crude Oil Futures Contract” is the first nearby Brent crude oil futures contract traded on the ICE. Brent crude oil has served as a global benchmark for Atlantic Basin crude oils in general, and low-sulfur (“sweet”) crude oils in particular, since the 1970’s. The Brent Crude Oil Futures Contract is a deliverable contract based on an Exchange of Futures for Physical Delivery, or “EFP”, with an option to cash settle. This mechanism enables companies to take delivery of physical crude supplies through EFP or, alternatively and more commonly, open positions that can be cash settled at expiration.

Trading in each first nearby futures contract ceases on the business day (a trading day which is not a public holiday in England and Wales) immediately preceding:

| § | either the 15th day before the first day of the delivery month, if that 15th day is a business day; or |

| § | if that 15th day is not a trading day, the next preceding business day. |

Trading hours for the Brent Crude Oil Futures Contract are from 01:00 London local time (23:00 on Sundays) to 23:00 London local time. The contract price is in U.S. dollars and cents per barrel. The Brent Crude Oil Futures Contract trades in a contract size of 1,000 barrels (42,000 U.S. gallons). The minimum price fluctuation for the Brent Crude Oil Futures Contract is one cent per barrel, and the ICE does not set forth a standard permitted maximum price fluctuation for the Brent Crude Oil Futures Contract. The settlement price on each trading day is the weighted average price of trades during a three minute settlement period from 19:27:00, London time.

The Closing Price of the Brent Crude Oil Futures Contract will be the official settlement price for the first nearby Brent crude oil futures contract.

|

Accelerated Return Notes® |

TS-9 |

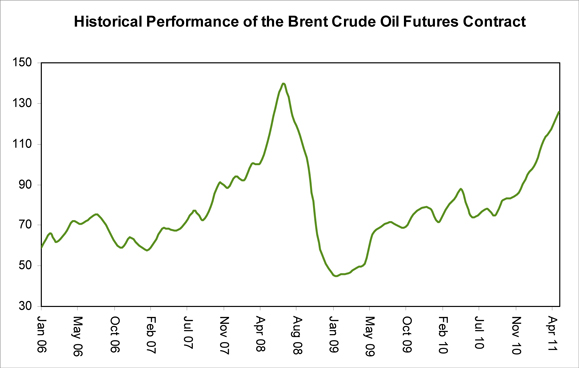

Historical Data on the Brent Crude Oil Futures Contract

The following graph sets forth the monthly historical prices of the Brent Crude Oil Futures Contract in the period from January 2006 through April 2011. This historical data is not necessarily indicative of the future price of the Brent Crude Oil Futures Contract or what the value of the ARNs may be. On May 19, 2011, the official settlement price of the Brent Crude Oil Futures Contract was 111.42.

Before investing in the ARNs, you should consult publicly available sources for the levels and trading pattern of the Brent Crude Oil Future Contract. The generally unsettled international environment and related uncertainties, including the risk of terrorism, may result in the Brent Crude Oil Future Contract and financial markets generally exhibiting greater volatility than in earlier periods.

|

Accelerated Return Notes® |

TS-10 |

Summary Tax Consequences

You should consider the U.S. federal income tax consequences of an investment in the ARNs, including the following

| § | You agree with us (in the absence of an administrative determination, or judicial ruling to the contrary) to characterize and treat the ARNs for all tax purposes as a single financial contract with respect to the Brent Crude Oil Futures Contract that requires you to pay us at inception an amount equal to the purchase price of the ARNs and that entitles you to receive at maturity an amount in cash based upon the price of the Brent Crude Oil Futures Contract. |

| § | Under this characterization and tax treatment of the ARNs, upon receipt of a cash payment at maturity or upon a sale or exchange of the ARNs prior to maturity, you generally will recognize capital gain or loss. This capital gain or loss generally will be long-term capital gain or loss if you held the ARNs for more than one year. |

Certain U.S. Federal Income Taxation Considerations

Set forth below is a summary of certain U.S. federal income tax considerations relating to an investment in the ARNs. The following summary is not complete and is qualified in its entirety by the discussion under the section entitled “U.S. Federal Income Tax Summary” beginning on page S-43 of product supplement ARN-3, which you should carefully review prior to investing in the ARNs.

General. Although there is no statutory, judicial, or administrative authority directly addressing the characterization of the ARNs, we intend to treat the ARNs for all tax purposes as a single financial contract with respect to the Brent Crude Oil Futures Contract that requires the investor to pay us at inception an amount equal to the purchase price of the ARNs and that entitles the investor to receive at maturity an amount in cash based upon the price of the Brent Crude Oil Futures Contract. Under the terms of the ARNs, we and every investor in the ARNs agree, in the absence of an administrative determination or judicial ruling to the contrary, to treat the ARNs as described in the preceding sentence. This discussion assumes that the ARNs constitute a single financial contract with respect to the Brent Crude Oil Futures Contract for U.S. federal income tax purposes. If the ARNs did not constitute a single financial contract, the tax consequences described below would be materially different. The discussion in this section also assumes that there is a significant possibility of a significant loss of principal on an investment in the ARNs.

This characterization of the ARNs is not binding on the Internal Revenue Service (“IRS”) or the courts. No statutory, judicial, or administrative authority directly addresses the characterization of the ARNs or any similar instruments for U.S. federal income tax purposes, and no ruling is being requested from the IRS with respect to their proper characterization and treatment. Due to the absence of authorities on point, significant aspects of the U.S. federal income tax consequences of an investment in the ARNs are not certain, and no assurance can be given that the IRS or any court will agree with the characterization and tax treatment described in product supplement ARN-3. Accordingly, you are urged to consult your tax advisor regarding all aspects of the U.S. federal income tax consequences of an investment in the ARNs, including possible alternative characterizations.

Settlement at Maturity or Sale or Exchange Prior to Maturity. Assuming that the ARNs are properly characterized and treated as single financial contracts with respect to the Brent Crude Oil Futures Contract for U.S. federal income tax purposes, upon receipt of a cash payment at maturity or upon a sale or exchange of the ARNs prior to maturity, a U.S. Holder (as defined on page S-44 of product supplement ARN-3) generally will recognize capital gain or loss equal to the difference between the amount realized and the U.S. Holder’s basis in the ARNs. This capital gain or loss generally will be long-term capital gain or loss if the U.S. Holder held the ARNs for more than one year. The deductibility of capital losses is subject to limitations.

Possible Future Tax Law Changes. From time to time, there may be legislative proposals or interpretive guidance addressing the tax treatment of financial instruments such as the ARNs. We cannot predict the likelihood of any such legislation or guidance being adopted, or the ultimate impact on the ARNs. For example, on December 7, 2007, the IRS released Notice 2008-2 (“Notice”) seeking comments from the public on the taxation of financial instruments currently taxed as “prepaid forward contracts.” This Notice addresses instruments such as the ARNs. According to the Notice, the IRS and Treasury are considering whether a holder of an instrument such as the ARNs should be required to accrue ordinary income on a current basis, regardless of whether any payments are made prior to maturity. It is not possible to determine what guidance the IRS and Treasury will ultimately issue, if any. Any such future guidance may affect the amount, timing, and character of income, gain, or loss in respect of the ARNs, possibly with retroactive effect. The IRS and Treasury are also considering additional issues, including whether additional gain or loss from such instruments should be treated as ordinary or capital, whether foreign holders of such instruments should be subject to withholding tax on any deemed income accruals, whether Section 1260 of the Internal Revenue Code of 1986, as amended, concerning certain “constructive ownership transactions,” generally applies or should generally apply to such instruments, and whether any of these determinations depend on the nature of the underlying asset. We urge you to consult your own tax advisors concerning the impact and the significance of the above considerations. We intend to continue treating the ARNs for U.S. federal income tax purposes in the manner described herein unless and until such time as we determine, or the IRS or Treasury determines, that some other treatment is more appropriate.

You should consult your own tax advisor concerning the U.S. federal income tax consequences to you of acquiring, owning, and disposing of the ARNs, as well as any tax consequences arising under the laws of any state, local, foreign, or other tax jurisdiction and the possible effects of changes in U.S. federal or other tax laws. See the discussion under the section entitled “U.S. Federal Income Tax Summary” beginning on page S-43 of product supplement ARN-3.

|

Accelerated Return Notes® |

TS-11 |

Additional Terms

You should read this term sheet, together with the documents listed below, which together contain the terms of the ARNs and supersede all prior or contemporaneous oral statements as well as any other written materials. You should carefully consider, among other things, the matters set forth under “Risk Factors” and “Additional Risk Factors” in the sections indicated on the cover of this term sheet. The ARNs involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting, and other advisors before you invest in the ARNs.

You may access the following documents on the SEC Website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC Website):

| § | Product supplement ARN-3 dated April 1, 2010: |

http://www.sec.gov/Archives/edgar/data/70858/000119312510075888/d424b5.htm

| § | Series L MTN prospectus supplement dated April 21, 2009 and prospectus dated April 20, 2009: |

http://www.sec.gov/Archives/edgar/data/70858/000095014409003387/g18667b5e424b5.htm

Our Central Index Key, or CIK, on the SEC Website is 70858.

We have filed a registration statement (including a product supplement, a prospectus supplement, and a prospectus) with the SEC for the offering to which this term sheet relates. Before you invest, you should read the product supplement, the prospectus supplement, and the prospectus in that registration statement, and the other documents relating to this offering that we have filed with the SEC for more complete information about us and this offering. You may get these documents without cost by visiting EDGAR on the SEC Website at www.sec.gov. Alternatively, we, any agent, or any dealer participating in this offering will arrange to send you the Note Prospectus if you so request by calling MLPF&S toll-free at 1-866-500-5408.

Market-Linked Investments Classification

Market-Linked Investments come in four basic categories, each designed to meet a different set of investor risk profiles, time horizons, income requirements, and market views (bullish, bearish, moderate outlook, etc.). The following descriptions of these categories are meant solely for informational purposes and are not intended to represent any particular Market-Linked Investment or guarantee performance. Certain Market-Linked Investments may have overlapping characteristics.

Market Downside Protection Market-Linked Investments combine some of the capital preservation features of traditional bonds with the growth potential of equities and other asset classes. They offer full or partial market downside protection at maturity, while offering market exposure that may provide better returns than comparable fixed-income securities. It is important to note that the market downside protection feature provides investors with protection only at maturity, subject to issuer credit risk. In addition, in exchange for full or partial protection, you forfeit dividends and full exposure to the linked asset’s upside. In some circumstances, this could result in a lower return than with a direct investment in the asset.

These short- to medium-term market-linked notes offer you a way to enhance your income stream, either through variable or fixed-interest coupons, an added payout at maturity based on the performance of the linked asset, or both. In exchange for receiving current income, you will generally forfeit upside potential on the linked asset. Even so, the prospect of higher interest payments and/or an additional payout may equate to a higher return potential than you may be able to find through other fixed-income securities. Enhanced Income Market-Linked Investments generally do not include market downside protection. The degree to which your principal is repaid at maturity is generally determined by the performance of the linked asset. Although enhanced income streams may help offset potential declines in the asset, you can still lose part or all of your original investment.

Market Access notes may offer exposure to certain market sectors, asset classes, and/or strategies that may not even be available through the other three categories of Market-Linked Investments. Subject to certain fees, the returns on Market Access Market-Linked Investments will generally correspond on a one-to-one basis with any increases or decreases in the value of the linked asset, similar to a direct investment. In some instances, they may also provide interim coupon payments. These investments do not include the market downside protection feature and, therefore, your principal remains at risk.

These short- to medium-term investments offer you a way to enhance exposure to a particular market view without taking on a similarly enhanced level of market downside risk. They can be especially effective in a flat to moderately positive market (or, in the case of bearish investments, a flat to moderately negative market). In exchange for the potential to receive better-than market returns on the linked asset, you must generally accept a degree of market downside risk and capped upside potential. As these investments are not market downside protected, and do not assure full repayment of principal at maturity, you need to be prepared for the possibility that you may lose all or part of your investment.

“Accelerated Return Notes®” and “ARNs®” are our registered service marks.

|

Accelerated Return Notes® |

TS-12 |