Filed Pursuant to Rule 433

Registration No. 333-158663

Subject to Completion

Preliminary Term Sheet dated June 23, 2011

The notes are being offered by Bank of America Corporation (“BAC”). The notes will have the terms specified in this term sheet as supplemented by the documents indicated below under “Additional Terms” (together, the “Note Prospectus”). Investing in the notes involves a number of risks. There are important differences between the notes and a conventional debt security, including different investment risks. See “Risk Factors” on page TS-6 of this term sheet and beginning on page S-10 of product supplement STR-2. The notes:

|

Are Not FDIC Insured

|

Are Not Bank Guaranteed

|

May Lose Value

|

In connection with this offering, Merrill Lynch, Pierce, Fenner & Smith Incorporated (“MLPF&S”) is acting in its capacity as principal for your account.

None of the Securities and Exchange Commission (the “SEC”), any state securities commission, or any other regulatory body has approved or disapproved of these securities or determined if this Note Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Unit |

Total |

|||||||||

| Public offering price (1) |

$ | 10.000 | $ | |||||||

| Underwriting discount (1) |

$ | 0.125 | $ | |||||||

| Proceeds, before expenses, to Bank of America Corporation |

$ | 9.875 | $ | |||||||

| (1) | The public offering price and underwriting discount for any purchase of 500,000 or more units in a single transaction by an individual investor will be $9.975 per unit and $0.10 per unit, respectively. The public offering price and underwriting discount for any purchase by certain fee-based trusts and fee-based discretionary accounts managed by U.S. Trust operating through Bank of America, N.A. will be $9.875 per unit and $0.00 per unit, respectively. |

*Depending on the date the notes are priced for initial sale to the public (the “pricing date”), any reference in this term sheet to the month in which the pricing date, the settlement date, or any Observation Date, or the maturity date will occur is subject to change.

| Merrill Lynch & Co.

|

| |||

| July , 2011 |

Units

Strategic Accelerated Redemption Securities®

Linked to the iShares® S&P Latin America 40 Index Fund,

due August , 2012

$10 principal amount per unit

Term Sheet No.

Pricing Date* July , 2011 Settlement Date* August , 2011 Maturity Date* August , 2012 CUSIP No.

Strategic Accelerated Redemption Securities®

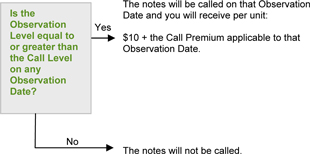

¡ The notes have a maturity of approximately one year, and are callable at approximately 6, 9 and 12 months after issuance

¡ The notes will be called at $10 per unit plus a Call Premium if the closing value per share of the iShares® S&P Latin America 40 Index Fund (the “Index Fund”) on any Observation Date is equal to or greater than 100% of its Starting Value

¡ The Call Premium will be between 7% and 11% per annum (equivalent to between 3.50% and 5.50% if the notes are called on the first Observation Date, or between 5.25% and 8.25% if the notes are called on the second Observation Date)

¡ 1-to-1 downside loss if the notes are not called and the Closing Value of the Index Fund on the final Observation Date decreases below the Threshold Value, with up to 95% of the principal amount at risk

¡ Payments on the notes are subject to the credit risk of Bank of America Corporation

¡ No periodic interest payments

¡ No listing on any securities exchange

Market Downside Protection

Enhanced Income

Market Access

Enhanced Return

Summary

The Strategic Accelerated Redemption Securities® Linked to the iShares® S&P Latin America 40 Index Fund, due August , 2012 (the “notes”), are our senior unsecured debt securities. The notes are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The notes will rank equally with all of our other unsecured and unsubordinated debt, and any payments due on the notes, including any repayment of principal, will be subject to the credit risk of BAC.

The notes provide for an automatic call if the Observation Level of the iShares® S&P Latin America 40 Index Fund (the “Index Fund”) on any Observation Date is equal to or greater than the Call Level. If the notes are called, you will receive the Original Offering Price of the notes plus the applicable Call Premium. If your notes are not called, the amount you receive on the maturity date will not be greater than the Original Offering Price per unit and will be based on the percentage decrease in the price per share of the Index Fund from the Starting Value to the Ending Value. Investors must be willing to forgo interest payments on the notes and be willing to accept a repayment that may be less, and potentially significantly less, than the Original Offering Price of the notes. Investors also must be prepared to have us call their notes on any Observation Date. Investors’ gain or loss generally will be long-term capital gain or loss if the notes are held for more than one year, and otherwise will be short-term capital gain or loss. Accordingly, if the notes are called on the first or second Observation Date, any capital gain or loss generally will be short-term capital gain or loss. Any such gain or loss is subject to certain tax implications, set forth under “Summary Tax Consequences” and “Certain U.S. Federal Income Taxation Considerations.”

Capitalized terms used but not defined in this term sheet have the meanings set forth in product supplement STR-2. Unless otherwise indicated or unless the context requires otherwise, all references in this term sheet to “we,” “us,” “our,” or similar references are to BAC.

|

Strategic Accelerated Redemption Securities® |

TS-2 |

Hypothetical Payments

Set forth below are five hypothetical examples of payment calculations (rounded to three decimal places). These examples have been prepared for purposes of illustration only. Your actual return will depend on the actual Starting Value, Threshold Value, Call Level, Observation Level, and term of your investment. The following examples do not take into account any tax consequences from investing in the notes. These examples are based on:

1) the hypothetical Starting Value of 100.00;

2) the hypothetical Threshold Value of 95.00, or 95% of the hypothetical Starting Value;

3) the hypothetical Call Level of 100.00, or 100% of the hypothetical Starting Value;

4) a term of the notes from June 24, 2011 to July 3, 2012, a term expected to be similar to that of the notes;

5) a hypothetical Call Premium of 9% of the Original Offering Price per unit per annum, the midpoint of the Call Premium range of 7% to 11% of the Original Offering Price per annum; and

6) hypothetical Observation Dates occurring December 23, 2011, March 22, 2012, and June 26, 2012.

The hypothetical Starting Value of 100 used in these examples has been chosen for illustrative purposes only, and does not represent a likely actual Starting Value for the Index Fund. For recent actual values of the Index Fund, see the “The Index Fund” section below, beginning on page TS-9.

The Notes Are Called on One of the Observation Dates

The notes have not been previously called and the Observation Level on the relevant Observation Date is equal to or greater than the Call Level. Consequently, the notes will be called at $10.000 plus the applicable Call Premium.

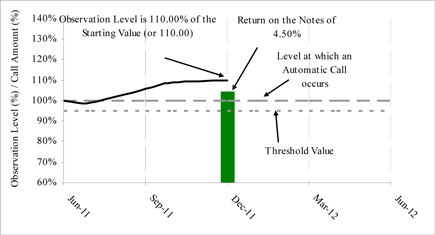

Example 1

If the call is related to the Observation Date that falls on December 23, 2011, the Call Amount per unit will be:

$10.000 plus the Call Premium of $0.450 = $10.450 per unit.

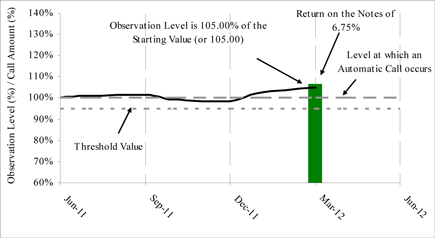

Example 2

If the call is related to the Observation Date that falls on March 22, 2012, the Call Amount per unit will be:

$10.000 plus the Call Premium of $0.675= $10.675 per unit.

|

Strategic Accelerated Redemption Securities® |

TS-3 |

Example 3

If the call is related to the Observation Date that falls on June 26, 2012, the Call Amount per unit will be:

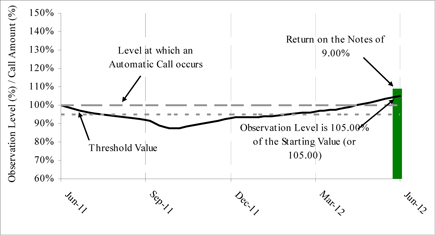

$10.000 plus the Call Premium of $0.900 = $10.900 per unit.

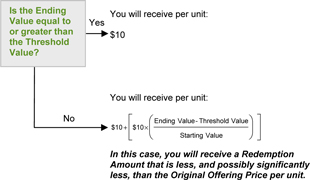

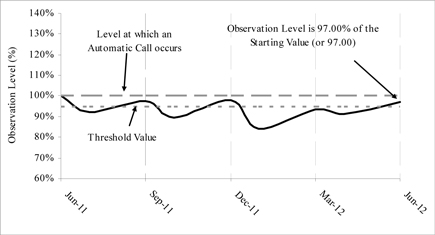

The Notes Are Not Called on Any of the Observation Dates

Example 4

The notes are not called on any of the Observation Dates and the Ending Value of the Index Fund on the final Observation Date is not less than 95.00,

the Threshold Value. The Redemption Amount per unit will therefore be $10.000.

|

Strategic Accelerated Redemption Securities® |

TS-4 |

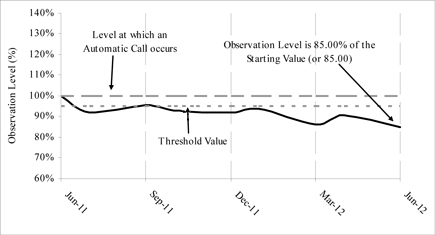

Example 5

The notes are not called on any of the Observation Dates and the Ending Value of the Index Fund on the final Observation Date is less than 95.00, the Threshold Value. The Redemption Amount will be less, and possibly significantly less, than the Original Offering Price per unit.

If the Ending Value is 85.00, or 85% of the Starting Value, the Redemption Amount will be:

| $10 + |

[ | $10 × | ( | 85.00 – 95.00 | ) | ] | = $9.000 per unit | |||||||||||||

| 100.00 |

These examples have been prepared for purposes of illustration only. Your actual return will depend on the actual Observation Level on the applicable Observation Date, the Ending Value, if applicable, the Call Premium, and the term of your investment.

| Summary of the Hypothetical Examples | Hypothetical Observation Date on December 23, 2011 |

Hypothetical Observation Date on March 22, 2012 |

Hypothetical Observation Date on June 26, 2012 | |||

|

Notes Are Called on an Observation Date |

||||||

| Starting Value |

100.00 | 100.00 | 100.00 | |||

| Call Level |

100.00 | 100.00 | 100.00 | |||

| Observation Level on the Observation Date |

110.00 | 105.00 | 105.00 | |||

| Return of the Index Fund (excluding any dividends) |

10.00% | 5.00% | 5.00% | |||

| Return of the Notes |

4.50% | 6.75% | 9.00% | |||

| Call Amount per Unit |

$10.450 | $10.675 | $10.900 | |||

| Notes Are Not Called on Any Observation Date | Hypothetical Ending Value Is Greater than the Hypothetical Threshold Value |

Hypothetical Ending Value Is Less than the Hypothetical Threshold Value | ||||||

| Starting Value |

100.00 | 100.00 | ||||||

| Ending Value |

97.00 | 85.00 | ||||||

| Threshold Value |

95.00 | 95.00 | ||||||

| Return of the Index Fund (excluding any dividends) |

-3.00% | -15.00% | ||||||

| Return of the Notes |

0.00% | -10.00% | ||||||

| Redemption Amount per Unit |

$10.000 | $9.000 | ||||||

|

Strategic Accelerated Redemption Securities® |

TS-5 |

Risk Factors

There are important differences between the notes and a conventional debt security. An investment in the notes involves significant risks, including those listed below. The following is a list of certain of the risks involved in investing in the notes. You should carefully review the more detailed explanation of risks relating to the notes in the “Risk Factors” sections beginning on page S-10 of product supplement STR-2 and page S-4 of the MTN prospectus supplement identified below under “Additional Terms.” We also urge you to consult your investment, legal, tax, accounting, and other advisors before you invest in the notes.

| § | If the notes are not called prior to maturity, your investment may result in a loss; there is no guaranteed return of principal. |

| § | Your return, if any, is limited to the return represented by the Call Premium. |

| § | Your yield may be less than the yield on a conventional debt security of comparable maturity. |

| § | Your investment return may be less than the return on a comparable investment directly in the Index Fund. |

| § | You must rely on your own evaluation of the merits of an investment linked to the Index Fund. |

| § | In seeking to provide you with what we believe to be competitive terms for the notes while providing MLPF&S with compensation for its services, we have considered the costs of developing, hedging, and distributing the notes. The price at which you may sell the notes in any secondary market may be lower than the public offering price due to, among other things, the inclusion of these costs. |

| § | A trading market is not expected to develop for the notes. MLPF&S is not obligated to make a market for, or to repurchase, the notes. |

| § | The amount that you receive at maturity or upon a call will not be affected by all developments relating to the Index Fund. |

| § | The sponsor of the Underlying Index, Standard & Poor’s Financial Services LLC (“S&P”), may adjust the Underlying Index in a way that affects its level, and S&P has no obligation to consider your interests. |

| § | We cannot control actions by the sponsor of the Index Fund, BlackRock Institutional Trust Company, N.A. (“BTC”), or the Index Fund’s investment advisor, BlackRock Fund Advisors, which may adjust the Index Fund in a way that could adversely affect the value of the notes and the amount payable on the notes, and these entities have no obligation to consider your interests. |

| § | You will have no rights of a holder of the securities held by the Index Fund, and you will not be entitled to receive securities or dividends or other distributions by the issuers of those securities. |

| § | While we or our affiliates may from time to time own shares of companies held by the Index Fund or included in the Underlying Index, we do not control any company held by the Index Fund or included in the Underlying Index, and are not responsible for any disclosure made by any other company. |

| § | There are liquidity and management risks associated with the Index Fund. |

| § | The performance of the Index Fund and the performance of the Underlying Index may vary. |

| § | Risks associated with the Underlying Index or the underlying assets of the Index Fund will affect the share price of the Index Fund and hence, the value of the notes. |

| § | Your return on the notes may be affected by factors affecting the international securities markets. |

| § | Exchange rate movements may impact the value of the notes. |

| § | If you attempt to sell the notes prior to maturity, their market value, if any, will be affected by various factors that interrelate in complex ways, and their market value may be less than the Original Offering Price. |

| § | Payments on the notes are subject to our credit risk, and changes in our credit ratings are expected to affect the value of the notes. |

| § | Purchases and sales by us and our affiliates of shares of companies held by the Index Fund or included in the Underlying Index may affect your return. |

| § | Our trading and hedging activities may create conflicts of interest with you. |

| § | Our hedging activities may affect your return on the notes and their market value. |

| § | Our business activities relating to the companies held by the Index Fund or included in the Underlying Index may create conflicts of interest with you. |

| § | There may be potential conflicts of interest involving the calculation agent. We have the right to appoint and remove the calculation agent. |

| § | The U.S. federal income tax consequences of the notes are uncertain, and may be adverse to a holder of the notes. See “Summary Tax Consequences” and “Certain U.S. Federal Income Taxation Considerations” below and “U.S. Federal Income Tax Summary” beginning on page S-43 of product supplement STR-2. |

|

Strategic Accelerated Redemption Securities® |

TS-6 |

Investor Considerations

Other Terms of the Notes

Closing Market Price

The provisions of this section supersede and replace the definition of “Closing Market Price” set forth in product supplement STR-2.

The “Closing Market Price” means:

| (A) | If the Index Fund is listed or admitted to trading on a national securities exchange in the United States that is registered under the Securities Exchange Act of 1934 (“registered national securities exchange”), is included in the OTC Bulletin Board Service (the “OTC Bulletin Board”) operated by the Financial Industry Regulatory Authority, Inc. (“FINRA”), or is quoted on a United States quotation medium or inter-dealer quotation system (e.g., the Pink-Sheets), then the Closing Market Price for any trading day means for one share of the Index Fund (or any other security underlying the Index Fund for which a Closing Market Price must be determined for purposes of the notes): |

| i. | the last reported sale price, regular way, on that day on the principal registered national securities exchange on which that security is listed or admitted to trading (without taking into account any extended or after-hours trading session); |

| ii. | if the last reported sale price is not obtainable on a registered national securities exchange, then the last reported sale price on the over-the-counter-market as reported on the OTC Bulletin Board or, if not available on the OTC Bulletin Board, then the last reported sale price on any other United States quotation medium or inter-dealer quotation system on that day (without taking into account any extended or after-hours trading session); or |

| iii. | if the last reported sale price is not available for any reason on a registered national securities exchange, on the OTC Bulletin Board, or on any other United States quotation medium or inter-dealer quotation system, then the Closing Market Price shall be the arithmetic mean of the bid prices on that day from as many dealers in that security, but not exceeding three, as have made bid prices available to the calculation agent after 3:00 p.m., local time in the principal market of the shares of the Index Fund (or any other security underlying the Index Fund for which a Closing Market Price must be determined for purposes of the notes) on that date (without taking into account any extended or after-hours trading session), or if there are no such bids available to the calculation agent, then the Closing Market Price shall be determined by the calculation agent in its sole discretion and reasonable judgment. |

| (B) | If the Index Fund is not listed on a registered national securities exchange, is not included in the OTC Bulletin Board, or is not quoted on any other United States quotation medium or inter-dealer system, then the Closing Market Price for any trading day means for one share of the Index Fund, the U.S. dollar equivalent of the last reported sale price (as determined by the calculation agent in its sole discretion and reasonable judgment) on that day on a foreign securities exchange on which that security is listed or admitted to trading with the greatest volume of trading for the calendar month preceding that trading day as determined by the calculation agent; provided that if the last reported sale price is for a transaction which occurred more than four hours prior to the close of that foreign exchange, then the Closing Market Price will mean the U.S. dollar equivalent (as determined by the calculation |

|

Strategic Accelerated Redemption Securities® |

TS-7 |

| agent in its sole discretion and reasonable judgment) of the average of the last available bid and offer price on that foreign exchange. |

| (C) | If the Index Fund is not listed on a registered national securities exchange, is not included in the OTC Bulletin Board, is not quoted on any other United States quotation medium or inter-dealer quotation system, is not listed or admitted to trading on any foreign securities exchange, or if the last reported sale price or bid and offer are not obtainable, then the Closing Market Price will mean the average of the U.S. dollar value (as determined by the calculation agent in its sole discretion) of the last available purchase and sale prices in the market of the three dealers which have the highest volume of transactions in that security in the immediately preceding calendar month as determined by the calculation agent based on information that is reasonably available to it. |

Supplement to the Plan of Distribution; Role of MLPF&S and Conflicts of Interest

We may deliver the notes against payment therefor in New York, New York on a date that is greater than three business days following the pricing date. Under Rule 15c6-1 of the Securities Exchange Act of 1934, trades in the secondary market generally are required to settle in three business days, unless the parties to any such trade expressly agree otherwise. Accordingly, if the initial settlement of the notes occurs more than three business days from the pricing date, purchasers who wish to trade the notes more than three business days prior to the original issue date will be required to specify alternative settlement arrangements to prevent a failed settlement.

The notes will not be listed on any securities exchange. In the original offering, the notes will be sold in minimum investment amounts of 100 units.

MLPF&S, a broker-dealer subsidiary of BAC, is a member of the FINRA and will participate as selling agent in the distribution of the notes. Accordingly, offerings of the notes will conform to the requirements of Rule 5121 applicable to FINRA members. MLPF&S may not make sales in this offering to any of its discretionary accounts without the prior written approval of the account holder.

Under our distribution agreement with MLPF&S, MLPF&S will purchase the notes from us as principal at the public offering price indicated on the cover of this term sheet, less the indicated underwriting discount. The public offering price includes, in addition to the underwriting discount, a charge of approximately $0.05 per unit. This charge reflects an estimated profit earned by MLPF&S from transactions through which the notes are structured and resulting obligations hedged. The fees charged reduce the economic terms of the notes. Actual profits or losses from these hedging transactions may be more or less than this amount. In entering into the hedging arrangements for the notes, we seek competitive terms and may enter into hedging transactions with a division of MLPF&S or one of our subsidiaries or affiliates. For further information regarding these charges, our trading and hedging activities and conflicts of interest, see “General Risks Relating to the Notes,” beginning on page S-9 and “Use of Proceeds” on page S-18 in product supplement STR-2.

MLPF&S will not receive an underwriting discount for notes sold to certain fee-based trusts and fee-based discretionary accounts managed by U.S. Trust operating through Bank of America, N.A.

If you place an order to purchase the notes, you are consenting to MLPF&S acting as a principal in effecting the transaction for your account.

MLPF&S may repurchase and resell the notes, with repurchases and resales being made at prices related to then-prevailing market prices or at negotiated prices. MLPF&S may act as principal or agent in these market-making transactions; however it is not obligated to engage in any such transactions.

|

Strategic Accelerated Redemption Securities® |

TS-8 |

The Index Fund

We have derived the following information from publicly available documents published by iShares, Inc., a registered investment company. We make no representation or warranty as to the accuracy or completeness of the following information. We are not affiliated with the Index Fund, and the Index Fund does not have any obligations with respect to the notes. This term sheet relates only to the notes and does not relate to the shares of the Index Fund or securities included in the Underlying Index described below. Neither we nor MLPF&S has or will participate in the preparation of the publicly available documents described below. Neither we nor MLPF&S has made any due diligence inquiry with respect to the Index Fund in connection with the offering of the notes. There can be no assurance that all events occurring prior to the date of this term sheet, including events that would affect the accuracy or completeness of the publicly available documents described below, that would affect the trading price of the shares of the Index Fund have been or will be publicly disclosed. Subsequent disclosure of any events or the disclosure of or failure to disclose material future events concerning the Index Fund could affect the value of the shares of the Index Fund on each Observation Date and therefore could affect your return on the notes.

iShares, Inc. consists of numerous separate investment portfolios, including the Index Fund. The Index Fund typically earns dividend income from securities included in the Underlying Index. These amounts, net of expenses and taxes (if applicable), are passed along to the Index Fund’s shareholders as “ordinary income.” In addition, the Index Fund realizes capital gains or losses whenever it sells securities. Net long-term capital gains are distributed to shareholders as “capital gain distributions.” However, because your notes are linked only to the share price of the Index Fund, you will not be entitled to receive income, dividend, or capital gain distributions from the Index Fund or any equivalent payments.

Information provided to or filed with the SEC by iShares, Inc. under the Investment Company Act of 1940 can be located at the SEC’s facilities or through the SEC’s website by reference to SEC file number 811-09102. We make no representation or warranty as to the accuracy or completeness of the information or reports.

The Index Fund seeks investment results that correspond generally to the price and yield performance, before fees and expenses, of companies in the Mexican and South American equity markets as represented by the S&P Latin America 40 Index (the “Underlying Index”). The Underlying Index is comprised of selected equities trading on the exchanges of four Latin American countries and includes highly liquid securities from major economic sectors of the Mexican and South American equity markets. In order to improve its portfolio liquidity and its ability to track the Underlying Index, the Index Fund may invest up to 10% of its assets in futures contracts, options on futures contracts, other types of options, and swaps related to the Underlying Index, as well as cash and cash equivalents, including shares of money market funds advised by BFA or its affiliates. The Index Fund currently has an expense ratio of approximately 0.50% per year. As of June 22, 2011, the five largest company weights were Vale SA ADR (11.27%), America Movil Sab de CV-SER L (9.92%), Banco Itau Holding Financeira SA ADR (9.80%), Petroleo Brasileiro S.A. ADR (6.99%), and Banco Bradesco-Sponsored ADR (5.65%), and the five largest sector weights were Materials (23.31%), Financials (22.04%), Consumer Staples (15.52%), Energy (11.91%), and Telecommunications Services (11.90%).

The Index Fund pursues a “representative sampling” strategy in attempting to track the performance of the Underlying Index, and does not necessarily hold at any time all of the equity securities included in the Underlying Index. The Index Fund invests in a representative sample of securities in the Underlying Index, which have a similar investment profile. Securities selected have aggregate investment characteristics (based on market capitalization and industry weightings), fundamental characteristics (such as return variability and yield) and liquidity measures similar to those of the Underlying Index.

S&P Latin America 40 Index

We have derived all information contained in this underlying supplement regarding the Underlying Index including, without limitation, its make-up, method of calculation and changes in its components, from publicly available information, and we have not participated in the preparation of, or verified, such publicly available information. This information reflects the policies of, and is subject to change by S&P. The Underlying Index was developed by, and is calculated, maintained and published by S&P.

The Underlying Index includes the stocks that are among the largest in terms of market capitalization from companies located in Mexico, Brazil, Peru and Chile (the “Component Stocks”). A stock’s domicile is determined based on criteria that include headquarters of the company, registration, listing of the stock, place of operations, and residence of the senior officers. Prior to September 2009, Argentinean stocks were included in the Underlying Index.

A stock’s weight in the Underlying Index is determined by the float-adjusted market capitalization of the stock, which excludes holdings by certain types of shareholders, such as governments and strategic partners. A minimum float turnover is required for companies to be included in the Underlying Index. The Underlying Index is designed to mirror the sector weights and country weights of the broader universe of stocks from the relevant four markets.

|

Strategic Accelerated Redemption Securities® |

TS-9 |

Index Fund Historical Data

The following table sets forth the high and low closing prices of the shares of the Index Fund for the calendar quarters from the first quarter of 2006 through June 22, 2011. The closing prices listed below were obtained from publicly available information at Bloomberg Financial Markets, rounded to two decimal places. The historical closing prices of shares of the Index Fund should not be taken as an indication of future performance, and we cannot assure you that the price per share of the Index Fund will not decrease. In addition, we cannot assure you that the price per share of the Index Fund will increase.

| High | Low | |||||||

| 2006 |

||||||||

| First Quarter |

29.40 | 25.54 | ||||||

| Second Quarter |

32.39 | 22.65 | ||||||

| Third Quarter |

28.93 | 25.70 | ||||||

| Fourth Quarter |

34.15 | 28.04 | ||||||

| 2007 |

||||||||

| First Quarter |

36.17 | 31.57 | ||||||

| Second Quarter |

44.25 | 36.17 | ||||||

| Third Quarter |

48.25 | 36.32 | ||||||

| Fourth Quarter |

53.40 | 45.50 | ||||||

| 2008 |

||||||||

| First Quarter |

54.36 | 43.38 | ||||||

| Second Quarter |

61.04 | 52.41 | ||||||

| Third Quarter |

53.78 | 34.86 | ||||||

| Fourth Quarter |

38.33 | 19.65 | ||||||

| 2009 |

||||||||

| First Quarter |

28.90 | 21.65 | ||||||

| Second Quarter |

37.39 | 26.56 | ||||||

| Third Quarter |

42.91 | 32.28 | ||||||

| Fourth Quarter |

49.50 | 41.79 | ||||||

| 2010 |

||||||||

| First Quarter |

49.82 | 41.43 | ||||||

| Second Quarter |

49.79 | 40.27 | ||||||

| Third Quarter |

50.54 | 41.86 | ||||||

| Fourth Quarter |

54.63 | 50.68 | ||||||

| 2011 |

||||||||

| First Quarter |

54.34 | 49.84 | ||||||

| Second Quarter (ending June 22, 2011) |

54.94 | 49.20 | ||||||

Before investing in the notes, you should consult publicly available sources for the prices and trading pattern of the Index Fund.

License Agreement

BTC and MLPF&S have entered into a non-exclusive license agreement under which BTC has licensed to MLPF&S and certain of its affiliates the right to use the iShares® mark in connection with the Index Fund. The license agreement provides that the following language must be set forth in this term sheet:

iShares® is a registered mark of BTC. BTC has licensed certain trademarks and trade names of BlackRock to MLPF&S. The notes are not sponsored, endorsed, sold, or promoted by BTC or any of its affiliates (collectively “BlackRock”). BlackRock makes no representations or warranties to the owners of the notes or any member of the public regarding the advisability of investing in the notes. BlackRock has no obligation or liability in connection with the operation, marketing, trading or sale of the notes.

|

Strategic Accelerated Redemption Securities® |

TS-10 |

Summary Tax Consequences

You should consider the U.S. federal income tax consequences of an investment in the notes, including the following:

| • | You agree with us (in the absence of an administrative determination, or judicial ruling to the contrary) to characterize and treat the notes for all tax purposes as a callable single financial contract linked to the Index Fund that requires you to pay us at inception an amount equal to the purchase price of the notes and that entitles you to receive at maturity or upon earlier redemption an amount in cash linked to the value of the Index Fund. |

| • | Under this characterization and tax treatment of the notes, subject to the discussion below concerning the potential application of the “constructive ownership” rules under Section 1260 of the Internal Revenue Code of 1986, as amended (the “Code”), upon receipt of a cash payment at maturity or upon a sale, exchange, or redemption of the notes prior to maturity, you generally will recognize capital gain or loss. This capital gain or loss generally will be long-term capital gain or loss if you hold the notes for more than one year and otherwise will be short-term capital gain or loss. Accordingly, if the notes are called on the first or second Observation Date, your capital gain or loss generally will be short-term capital gain or loss. |

Certain U.S. Federal Income Taxation Considerations

Set forth below is a summary of certain U.S. federal income tax considerations relating to an investment in the notes. The following summary is not complete and is qualified in its entirety by the discussion under the section entitled “U.S. Federal Income Tax Summary” beginning on page S-43 of product supplement STR-2, which you should carefully review prior to investing in the notes.

General. Although there is no statutory, judicial, or administrative authority directly addressing the characterization of the notes, we intend to treat the notes for all tax purposes as a callable single financial contract linked to the Index Fund that requires you to pay us at inception an amount equal to the purchase price of the notes and that entitles you to receive at maturity or upon earlier redemption an amount in cash linked to the value of the Index Fund. Under the terms of the notes, we and every investor in the notes agree, in the absence of an administrative determination or judicial ruling to the contrary, to treat the notes as described in the preceding sentence. This discussion assumes that the notes constitute a callable single financial contract linked to the Index Fund for U.S. federal income tax purposes. If the notes did not constitute a callable single financial contract, the tax consequences described below would be materially different.

This characterization of the notes is not binding on the Internal Revenue Service (“IRS”) or the courts. No statutory, judicial, or administrative authority directly addresses the characterization of the notes or any similar instruments for U.S. federal income tax purposes, and no ruling is being requested from the IRS with respect to their proper characterization and treatment. Due to the absence of authorities on point, significant aspects of the U.S. federal income tax consequences of an investment in the notes are not certain, and no assurance can be given that the IRS or any court will agree with the characterization and tax treatment described in product supplement STR-2. Accordingly, you are urged to consult your tax advisor regarding all aspects of the U.S. federal income tax consequences of an investment in the notes, including possible alternative characterizations. The discussion in this section and in the section entitled “U.S. Federal Income Tax Summary” in product supplement STR-2 assume that there is a significant possibility of a significant loss of principal on an investment in the notes.

Settlement at Maturity or Sale, Exchange, or Redemption Prior to Maturity. Assuming that the notes are properly characterized and treated as callable single financial contracts linked to the Index Fund for U.S. federal income tax purposes, subject to the discussion below concerning the potential application of the “constructive ownership” rules under Section 1260 of the Code, upon receipt of a cash payment at maturity or upon a sale, exchange, or redemption of the notes prior to maturity, a U.S. Holder (as defined on page S-44 of product supplement STR-2) generally will recognize capital gain or loss equal to the difference between the amount realized and the U.S. Holder’s basis in the notes. This capital gain or loss generally will be long-term capital gain or loss if the U.S. Holder holds the notes for more than one year and otherwise will be short-term capital gain or loss. Accordingly, if the notes are called on the first or second Observation Date, a U.S. Holder’s capital gain or loss generally will be short-term capital gain or loss. The deductibility of capital losses is subject to limitations.

Possible Application of Section 1260 of the Code. Because the Index Fund is a type of financial assets described under Section 1260 of the Code, while the matter is not entirely clear, there may exist a risk that an investment in the notes will be treated as a “constructive ownership transaction” to which Section 1260 of the Code applies. If Section 1260 of the Code applies, all or a portion of any long-term capital gain recognized by a U.S. Holder in respect of the notes will be recharacterized as ordinary income (the “Excess Gain”). Although not clear, the Excess Gain may equal the excess of (i) any long-term capital gain recognized by the U.S. Holder in respect of the notes, over (ii) the “net underlying long-term capital gain” (as defined in Section 1260 of the Code) such U.S. Holder would have had if such U.S. Holder had acquired an amount of the Index Fund at fair market value on the original issue date for an amount equal to the issue price of the notes and sold such amount of the Index Fund upon the date of sale, exchange, redemption, or settlement of the notes at fair market value. In addition, an interest charge will also apply to any deemed underpayment of tax in respect of any Excess Gain to the extent such gain would have resulted in gross income inclusion for the U.S. Holder in taxable years prior to the taxable year of sale, exchange, redemption, or settlement (assuming such income accrued at a constant rate equal to the applicable federal rate as of the date of sale, exchange, redemption, or settlement). U.S. Holders should consult their tax advisor regarding the potential application of Section 1260 of the Code to an investment in the notes.

Possible Future Tax Law Changes. From time to time, there may be legislative proposals or interpretive guidance addressing the tax treatment of financial instruments such as the notes. We cannot predict the likelihood of any such legislation or guidance being adopted, or the ultimate impact on the notes. For example, on December 7, 2007, the IRS released Notice 2008-2 (“Notice”) seeking comments from the public on the taxation of financial instruments currently taxed as “prepaid forward contracts.” This Notice addresses instruments such as the notes. According to the Notice, the IRS and Treasury are considering whether a holder of an instrument such as the notes should be required to accrue ordinary income on a current basis, regardless of whether any payments are made prior to maturity. It is not possible to determine what guidance the IRS and Treasury will ultimately issue, if any. Any such future guidance may affect the amount, timing, and character of income, gain, or loss in respect of the notes, possibly with retroactive effect. The IRS and Treasury are also considering additional issues, including whether additional gain or loss from such instruments should be treated as ordinary or capital, whether foreign holders of such instruments should be subject to withholding tax on any deemed income accruals, whether the Code concerning certain “constructive ownership transactions,” generally applies or should generally apply to such instruments, and whether any of these determinations depend on the nature of the underlying asset. We urge you to consult your own tax advisors concerning the impact and the significance of the above considerations. We intend to continue treating the notes for U.S. federal income tax purposes in the manner described herein unless and until such time as we determine, or the IRS or Treasury determines, that some other treatment is more appropriate.

|

Strategic Accelerated Redemption Securities® |

TS-11 |

You should consult your own tax advisor concerning the U.S. federal income tax consequences to you of acquiring, owning, and disposing of the notes, as well as any tax consequences arising under the laws of any state, local, foreign, or other tax jurisdiction and the possible effects of changes in U.S. federal or other tax laws. See the discussion under the section entitled “U.S. Federal Income Tax Summary” beginning on page S-43 of product supplement STR-2.

|

Strategic Accelerated Redemption Securities® |

TS-12 |

Additional Terms

You should read this term sheet, together with the documents listed below, which together contain the terms of the notes and supersede all prior or contemporaneous oral statements as well as any other written materials. You should carefully consider, among other things, the matters set forth under “Risk Factors” in the sections indicated on the cover of this term sheet. The notes involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting, and other advisors before you invest in the notes.

You may access the following documents on the SEC Website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC Website):

| § | Product supplement STR-2 dated April 21, 2009: |

http://www.sec.gov/Archives/edgar/data/70858/000095014409003417/g18702p5e424b5.htm

| § | Series L MTN prospectus supplement dated April 21, 2009 and prospectus dated April 20, 2009: |

http://www.sec.gov/Archives/edgar/data/70858/000095014409003387/g18667b5e424b5.htm

Our Central Index Key, or CIK, on the SEC Website is 70858.

We have filed a registration statement (including a product supplement, a prospectus supplement, and a prospectus) with the SEC for the offering to which this term sheet relates. Before you invest, you should read the product supplement, the prospectus supplement, and the prospectus in that registration statement, and the other documents relating to this offering that we have filed with the SEC for more complete information about us and this offering. You may get these documents without cost by visiting EDGAR on the SEC Website at www.sec.gov. Alternatively, we, any agent or any dealer participating in this offering will arrange to send you the Note Prospectus if you so request by calling MLPF&S toll-free at 1-866-500-5408.

Market-Linked Investments Classification

Market-Linked Investments come in four basic categories, each designed to meet a different set of investor risk profiles, time horizons, income requirements, and market views (bullish, bearish, moderate outlook, etc.). The following descriptions of these categories are meant solely for informational purposes and are not intended to represent any particular Market-Linked Investment or guarantee performance. Certain Market-Linked Investments may have overlapping characteristics.

Market Downside Protection Market-Linked Investments combine some of the capital preservation features of traditional bonds with the growth potential of equities and other asset classes. They offer full or partial market downside protection at maturity, while offering market exposure that may provide better returns than comparable fixed-income securities. It is important to note that the market downside protection feature provides investors with protection only at maturity, subject to issuer credit risk. In addition, in exchange for full or partial protection, you forfeit dividends and full exposure to the linked asset’s upside. In some circumstances, this could result in a lower return than with a direct investment in the asset.

These short- to medium-term market-linked notes offer you a way to enhance your income stream, either through variable or fixed-interest coupons, an added payout at maturity based on the performance of the linked asset, or both. In exchange for receiving current income, you will generally forfeit upside potential on the linked asset. Even so, the prospect of higher interest payments and/or an additional payout may equate to a higher return potential than you may be able to find through other fixed-income securities. Enhanced Income Market-Linked Investments generally do not include market downside protection. The degree to which your principal is repaid at maturity is generally determined by the performance of the linked asset. Although enhanced income streams may help offset potential declines in the asset, you can still lose part or all of your original investment.

Market Access notes may offer exposure to certain market sectors, asset classes and/or strategies that may not even be available through the other three categories of Market-Linked Investments. Subject to certain fees, the returns on Market Access Market-Linked Investments will generally correspond on a one-to-one basis with any increases or decreases in the value of the linked asset, similar to a direct investment. In some instances, they may also provide interim coupon payments. These investments do not include the market downside protection feature and, therefore, your principal remains at risk.

These short- to medium-term investments offer you a way to enhance exposure to a particular market view without taking on a similarly enhanced level of market downside risk. They can be especially effective in a flat to moderately positive market (or, in the case of bearish investments, a flat to moderately negative market). In exchange for the potential to receive better-than market returns on the linked asset, you must generally accept a degree of market downside risk and capped upside potential. As these investments are not market downside protected, and do not assure full repayment of principal at maturity, you need to be prepared for the possibility that you may lose all or part of your investment.

“Strategic Accelerated Redemption Securities®” is our registered service mark.

|

Strategic Accelerated Redemption Securities® |

TS-13 |