Addressing Legacy Mortgage Issues

June 29, 2011

Exhibit 99.4 |

| Addressing Legacy Mortgage Issues

June 29, 2011

Exhibit 99.4 |

Key Takeaways

•

Today we are announcing a settlement agreement, a related institutional investor

agreement and several 2Q11 mortgage actions that represent important

steps in putting representations

and warranties (“R & W”) risk behind us

•

Following today's agreements (which include an $8.5B cash payment after final

court approval)

and

other

mortgage-related

actions

in

2Q11

we

will

have

recorded

reserves¹

in

our

financial statements for a substantial portion of our R & W exposure measured

by original UPB and we have estimated a range of possible loss for the

remainder •

Expect to report a 2Q11 net loss of $8.6B to $9.1B on July 19; EPS loss of $0.88

to $0.93 (includes $0.26 per share goodwill impairment charge)

•

Excluding mortgage-related items and gains from asset sales and other

non-operating items, net income expected in the $3.2B -

$3.7B range

•

Including the impact of these settlements and related actions, BAC's Tier 1 Common

Equity ratio is expected to remain above 8% at June 30, 2011 and tangible

book value per share to be above $12.50 (and

book value per share to be above $20.00) 1

Settlement

Agreement

and Other

2Q11

Actions

Executing on

Long-Term

Strategy

•

We have best-in-class businesses

•

We are executing on a strategy for growth and relationship deepening with strong

early signs of success

•

All of our businesses, ex Consumer Real Estate Services, are performing well

•

We are focused on a shareholder-value model to deliver consistent, sustainable

returns •

Our reported capital ratios are expected to be well above minimum Basel III

requirements 1

2

Represents a non-GAAP financial measure, please refer to the end of this

presentation material for a reconciliation. 2

2

Reserves are subject to adjustment in future periods based on a number of factors including home

prices and counterparty behavior – also refer to Footnote 3 of this document. |

Summary Review of Today’s Agreements

Announced

Agreements:

•

Settlement with Bank of New York Mellon (“BNY”), as Trustee, regarding

repurchase and servicing claims for 530 legacy Countrywide

private-label residential mortgage-backed securities trusts

–

BNY, as Trustee, will release the claims on behalf of the covered trusts and all

associated investors

•

Agreement with a group of large institutional asset managers being represented by

the law firm Gibbs & Bruns to support the settlement

•

Settlement agreement is subject to final court approval and certain other

matters Claims

Covered

by

Agreement:

•

The settlement agreement will provide for the release of claims related to:

–

All R

&

W

in

the

covered

Countrywide

RMBS

trusts

which

represent

nearly

all of

Countrywide first-lien private-label exposure;

–

Substantially all past servicing of loans;

–

Future servicing of loans, to the extent that future servicing complies with newly

agreed- to standards; and

–

Successor liability claims against BAC for Countrywide acts related to released

claims 2 |

Scope of Private-Label Settlement Agreement

Scope of Settlement:

•

Covers 530 Countrywide residential mortgage-backed private-label

trusts

–

$424B of Original Unpaid Principal Balance

•

Does not address R & W exposure from:

–

Loans sold by other BAC entities into private-label trusts

–

Loans sold to third parties and subsequently sold in private

RMBS trusts

–

Investors’

securities and fraud claims and certain other claims

Settlement Amount / Other:

•

$8.5B cash payment upon final court approval plus related

fees/expenses of $100M

•

Payment allocated

directly

to

the

trusts

by

the

Trustee

based

on

a

collateral loss formula

•

BAC has agreed to implement certain servicing standards and

address documentation deficiencies as part of the settlement, with

certain of the obligations starting now

–

The estimated cost to implement servicing and documentation

obligations is approximately $400M and will contribute to a

negative valuation charge

on the MSR asset in 2Q11

3

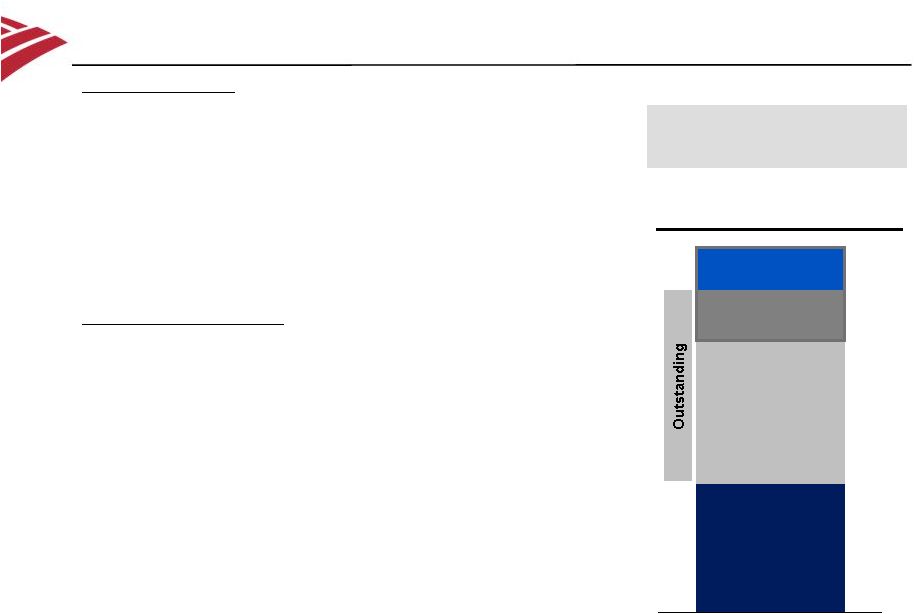

Original Unpaid Principal Balance

of 530 Countrywide Private Label

Mortgage Trusts in Settlement

$47B

$59B

$115B

$203B

Defaulted

Severely

Delinquent

Outstanding

Excluding

Severely

Delinquent

Paid Off

$424B

Total Original Unpaid

Principal Balance |

Rationale for Settlement

4

•

Continued and substantial progress in addressing R & W exposure

–

January 3, 2011 -

Settlements with Fannie Mae and Freddie Mac for certain Countrywide exposure

–

April 15, 2011 -

Assured Guaranty Settlement

–

June 28, 2011 -

Countrywide-issued Private-Label Settlement

–

Total R & W expense of

approximately $22.0B over the last six quarters, including expected 2Q11

actions •

Reduces uncertainty –

based on original principal balance, and including the impact of pay-downs,

prior settlements and 2Q11 actions we have settled or have provided reserves

for a substantial portion of the original UPB and have provided a range

of possible loss for the remainder

–

Reserves are subject to adjustment in future periods depending on a number of

factors including home prices and behavior of our counterparties

–

Unreserved reasonably possible and estimable exposure is reflected in the

non-GSE Range of Possible Loss disclosure

•

Today’s settlement reduces exposure to variability of future losses on

loans through liquidation

•

Attractive trust-based structure addresses all historical R & W exposure of

the covered trusts –

Trustee will release repurchase and certain servicing and loan documentation

claims on behalf of all private- label investors in 530 legacy

Countrywide trusts |

Preliminary Financial Impact of Today’s Announcements

5

•

$8.5B

settlement

payment

will

be

accrued

for

in

2Q11,

but

is

not

payable

until

after

final

court approval of settlement agreement

•

Expect to record additional 2Q11 mortgage items:

–

Additional $5.5B provision for R & W liability for non-GSE exposure and,

to a lesser extent, GSE exposure

–

$2.6B goodwill impairment in Consumer Real Estate Services, reducing its goodwill

to $0 –

Other mortgage-related charges of approximately $4.0B including litigation

costs, MSR valuation charge and compensatory fees and assessments related

to foreclosure delays •

Remaining Range of Possible Loss on non-GSE R & W exposure currently

estimated to be up

to

$5B

above

accruals

3

After giving effect to the settlement and the additional representations and

warranties charges expected to be recorded in the second quarter of 2011, the

company currently estimates that the range of possible loss with

respect to non-GSE investor representations and warranties expense could be up

to $5 billion over expected accruals. After giving effect to the additional

GSE representations and warranties charges expected to be taken in the

second quarter of 2011, based on its past experience with the GSEs, the

company believes that its remaining exposure to repurchase obligations for

first-lien residential mortgage loans sold directly to the GSEs will be

accounted for in the recorded liability for representations and warranties for these loans. The company is not currently

able to reasonably estimate the possible loss with respect to any such potential

impact in excess of current reserves on future GSE provisions if the GSE

behaviors change from past experience. In addition, future provisions associated

with representations and warranties for both non-GSE and GSE exposures

may be materially impacted if actual results are different from our assumptions

regarding economic conditions, home prices and other matters, including

counterparty behavior and estimated repurchase rates.

3 |

•

Expect to report a net loss of $8.6B to $9.1B on July 19; EPS loss of $0.88 to

$0.93 –

$0.26 EPS impact of $2.6B goodwill impairment charge

•

Earnings ex goodwill impairment expected to include the following

mortgage-related pre-tax charges:

–

R & W expense $14.0B

–

Additional mortgage costs of approximately $4.0B, including:

•

Litigation costs

•

MSR valuation charge

•

Compensatory fees and other assessments related to foreclosure delays

•

Earnings also expected to include several non mortgage-related items totaling

approximately $2.5B pre-tax:

–

Gains on the sales of Balboa, BlackRock stock

–

Other notable items will include debt securities gains, dividends from strategic

investments •

Results expected to show the following trends:

–

Net interest income hitting expected lows

–

Sales

and

trading

results

ahead

of

last

year

second

quarter,

but

below

seasonally

strong

1Q11

–

Provision expense declining from 1Q11, asset quality continues to improve

6

4

Results are estimates and could change based on information obtained in the process

of finalizing results. 2Q11 Preliminary Results

4 |

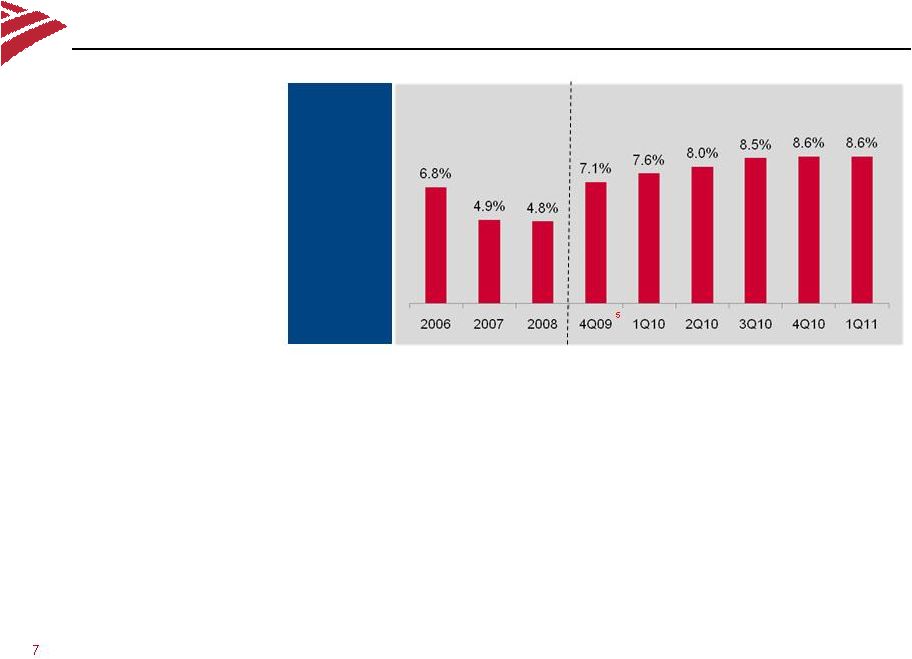

7

Estimated Regulatory Capital Impact

•

Tier 1 Common Ratio

(under Basel I)

expected to be above

8% at 6/30/11

5

Reflects the 12/31/09 information adjusted to include 1/1/10 adoption of FAS

166/167 as reported in our SEC filings. 5

BAC

Tier 1

Common

Ratio

(Basel I) |

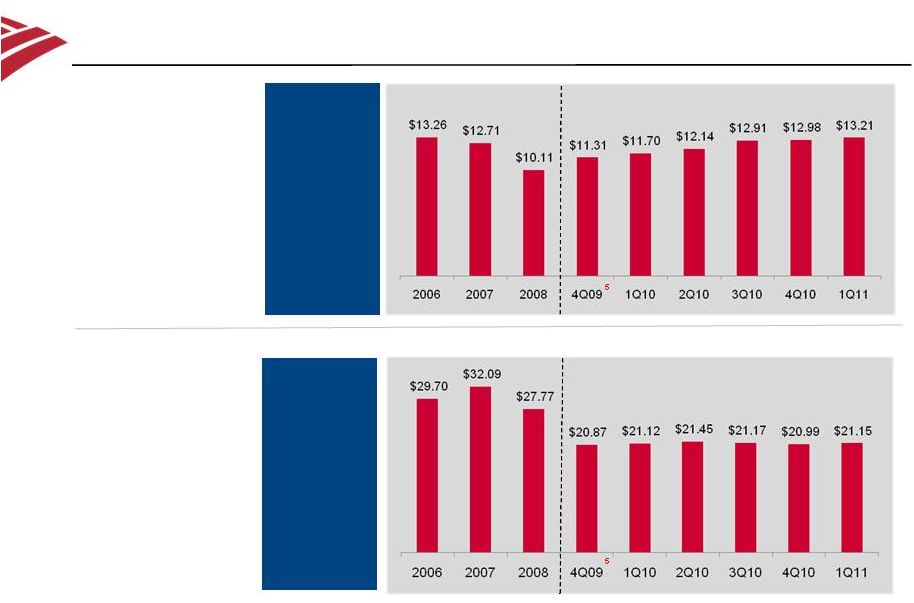

8

•

Tangible Book Value

Per Share expected

to be above $12.50

at 6/30/11

6

5

Reflects the 12/31/09 information adjusted to include 1/1/10 adoption of FAS

166/167 as reported in our SEC filings. 6

Represents a non-GAAP financial measure, refer to the end of the presentation

material for a reconciliation. Estimated Impact on Capital

Metrics •

Book Value Per

Share expected to

be above $20.00 at

6/30/11

Tangible

Book Value

Per Share

Book Value

Per Share |

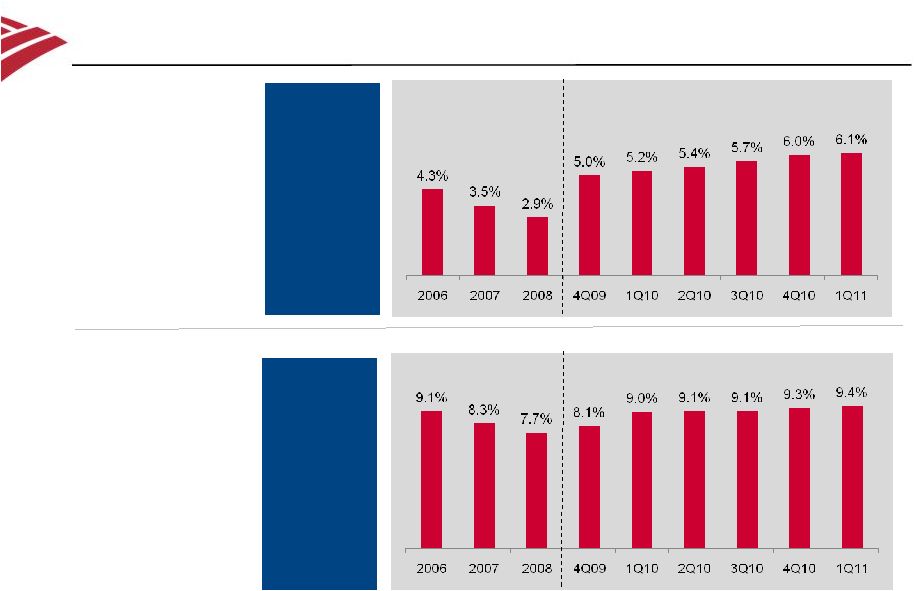

9

Estimated Impact on Capital Metrics (cont’d)

•

Tangible Common

Equity Ratio

expected to be above

5.7% at 6/30/11

6

Tangible

Common

Equity Ratio

Common

Equity Ratio

•

Common Equity

Ratio expected to be

above roughly 9.0%

at 6/30/11

5

5

5

Reflects the 12/31/09 information adjusted to include 1/1/10 adoption of FAS

166/167 as reported in our SEC filings. 6

Represents a non-GAAP financial measure, refer to the end of the presentation

material for a reconciliation. |

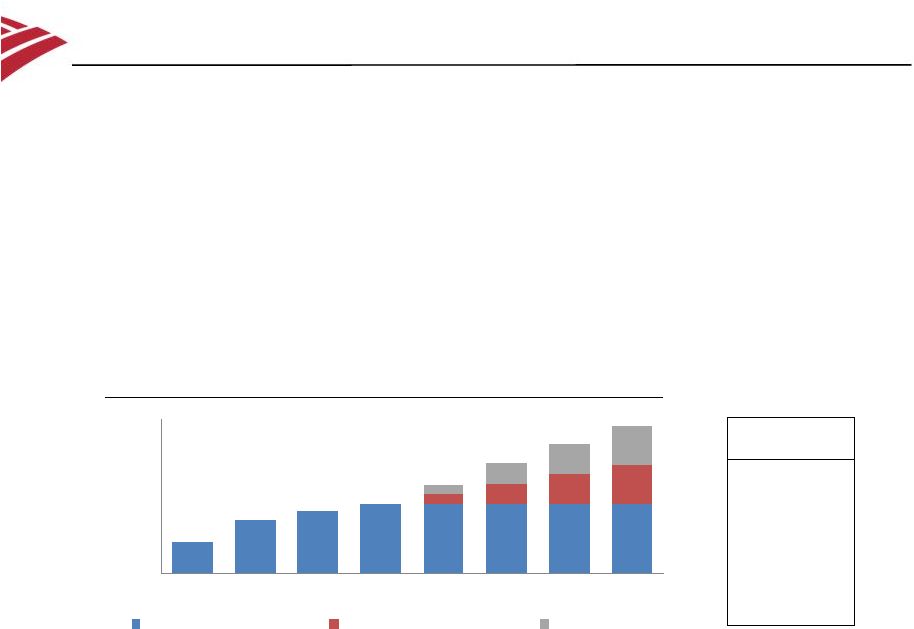

Capital and Basel III

2.0%

3.5%

4.0%

4.5%

4.5%

4.5%

4.5%

4.5%

0.6%

1.3%

1.9%

2.5%

0.6%

1.3%

1.9%

2.5%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Capital Deduction

Phase-In

1/1/2012

0%

1/1/2013

0%

1/1/2014

20%

1/1/2015

40%

1/1/2016

60%

1/1/2017

80%

1/1/2018

100%

1/1/2019

100%

•

Including currently identified RWA mitigation, 12/31/12 RWA is estimated at ~$1.8T;

mitigation efforts will continue after 12/31/12

•

Also actively mitigating against Basel III capital numerator deductions which

phase in starting in 2014 •

Expect our ratios to be in excess of all required minimums

•

Assuming no benefit for the Basel III capital deduction phase-in (i.e., fully

front-loaded basis), our goal is to achieve a 6.75% -

7% Tier 1 Common Ratio by 1/1/13 assuming no phase-in for capital

deductions

•

That said, given the phase-in period provided for by the Basel rules, we will

protect shareholder value when decisioning

mitigation

efforts

that

allow

for

earlier

fully

phased-in

compliance

Basel III Capital Requirements *

Tier 1 Common Minimum

Capital Conservation Buffer

SIFI @ 250bps

2012

2013

2014

2015

2016

2017

2018

2019

10

* Per Basel |

Key Takeaways

•

Making substantial progress in addressing legacy issues

•

Today’s announcement addresses significant exposure on potential

representations and warranties losses

•

2Q11 results include other mortgage-related costs

•

Although results include a significant cost to shareholders, we believe the

capital impact is recoverable over two quarters

•

Outside of Consumer Real Estate Services, businesses operating well

11 |

Forward-Looking Statements

12

Certain statements in this Presentation represent the current expectations, plans or forecasts of Bank

of America and are forward-looking statements within the meaning of the Private Securities

Litigation Reform Act of 1995. Forward-looking statements can be identified by the fact that they do not relate strictly to

historical or current facts. These statements often use words like “expects,” “anticipates,”

“believes,” “estimates,” “targets,” “intends,”

“plans,” “predict,” “goal” and other similar expressions or future or conditional verbs such as “will,” “may,” “might,” “should,” “would” and

“could.” The forward-looking statements made in this Presentation include, without

limitation, statements concerning: the preliminary information about Bank of America’s results of

operations and financial condition for the quarter ending June 30, 2011 and related trends, including

Bank of America’s expected net loss and including Bank of America’s expected net

income if the settlement, other mortgage-related charges, and proceeds from asset-sales are excluded, the expected amount and sufficiency of the charges to be recorded in the

quarter ending June 30, 2011 related to the settlement agreement, the related expected increase in the

reserve for representations and warranties expense and the estimated costs associated with the

additional servicing and documentation obligations undertaken in connection with the settlement and the corresponding expected write-down of the valuation of the

mortgage servicing rights (MSR), the expected amount and sufficiency of the additional charge for

representation and warranty expense in the quarter ending June 30, 2011 for both GSE and

non-GSE-exposures, the expected other mortgage-related costs to be recorded in the quarter ending June 30, 2011, including the expected elimination in the quarter ending

June 30, 2011 of the balance of the goodwill in the Consumer Real Estate Services business segment and

the amount of the goodwill impairment charge expected to be recorded, Bank of America’s

expected tangible book value per share, book value per share, tangible common equity ratio, common equity ratio, Tier 1 common ratio (Basel I) for the quarter

ending June 30, 2011 and the estimated capital recovery period, estimated RWA, ratio goals and

expectations, and the expected trends outside of the mortgage area, including Bank of

America’s expectations regarding net interest income, sales and trading results, core expenses, provision expense, gains from the sale of Balboa and BlackRock, debt securities

gains, dividends from strategic investment and fair value option gains on certain structured

liabilities; the portion of Bank of America’s repurchase obligations for residential mortgage

obligations sold by Bank of America and its affiliates to investors that has been paid or reserved

after giving effect to the settlement agreement and the expected charges in the quarter ending

June 30, 2011; the estimated range of possible loss over existing accruals related to non-GSE representation and warranty exposure; the expected impact of the settlement

agreement and the institutional investor agreement; expected support of the institutional investors;

whether and to what extent challenges will be made to the settlement and the timing of the

court approval process; whether the conditions to the settlement will be satisfied, including the receipt of final court approval and tax opinions; and the potential assertion and

impact of claims not addressed by the settlement agreement. Forward-looking statements speak

only as of the date they are made, and Bank of America undertakes no obligation to update any

forward-looking statement to reflect the impact of circumstances or events that arise after the date the forward-looking statement was made.

These statements are not guarantees of future results or performance and involve certain risks,

uncertainties and assumptions that are difficult to predict and are often beyond Bank of

America’s control. Actual outcomes and results may differ materially from those expressed

in, or implied by, any of these forward-looking statements. You should not place undue

reliance on any forward-looking statement and should consider all of the following uncertainties

and risks, as well as those more fully discussed under Item 1A. “Risk Factors” of Bank

of America’s 2010 Annual Report on Form 10-K and in any of Bank of America’s other

subsequent Securities and Exchange (SEC) filings: the accuracy and variability of estimates

and assumptions in determining the expected total cost of the settlement to Bank of America; the

adequacy of the liability reserves for the representations and warranties exposures to the

GSEs, monolines and private-label and other investors; the accuracy and variability of estimates and assumptions in determining the estimated range of possible loss over existing

accruals related to non-GSE representation and warranty exposure; the accuracy and variability of

estimates and assumptions in determining the portion of Bank of America’s repurchase

obligations for residential mortgage obligations sold by Bank of America and its affiliates to investors that has been paid or reserved after giving effect to the settlement

agreement and the expected charges in the quarter ending June 30, 2011; whether and to what extent

challenges will be made to the settlement and the timing of the court approval process,

including the nature and timing of any appeals that may follow an initial court decision; whether the conditions to the settlement will be satisfied, including the receipt of final

court approval and a private letter rulings from the IRS and other tax opinions; whether conditions in

the settlement agreement that would permit Bank of America and legacy Countrywide to withdraw

from the settlement will occur and whether Bank of America and legacy Countrywide will determine to withdraw from the settlement if such conditions occur;

the impact of performance and enforcement of obligations under, and provisions contained in, the

settlement agreement and the institutional investor Agreement, including performance of

obligations under the settlement agreement by Bank of America (and certain of its affiliates) and the Trustee and the performance of obligations under the institutional

investor agreement by Bank of America (and certain of it affiliates) and the investor group; Bank of

America’s and certain of its affiliates’ ability to comply with the servicing and

documentation obligations under the settlement agreement; the potential assertion and impact of

additional claims not addressed by the settlement agreement or any of the prior agreements

entered into between Bank of America (and/or certain of its affiliates) and the GSEs, monoline insurers and other investors; Bank of America’s mortgage modification

policies, loss mitigation strategies and related results; the foreclosure review and assessment

process, the effectiveness of Bank of America’s response to such process, and any

governmental or private third-party claims asserted in connection with these foreclosure matters;

and any measures or steps taken by federal regulators or other governmental authorities with

regard to mortgage loans, servicing agreements and standards, or other matters. |

Note Relating to Non-GAAP Financial Disclosures

This presentation contains non-GAAP financial information. We believe the use

of these non-GAAP measures provides additional clarity in

assessing the

results

of

the

Corporation.

Other

companies

may

define

or

calculate

these

measures

and

ratios

differently.

The

reconciliations of those measures to GAAP measures are provided herein, in our

Form 10-K for the year ended December 31, 2010 or in our Form 10-Q

for the three months ended March 31, 2011, available through the Bank of America Investor Relations web site at:

http://investor.bankofamerica.com.

13

1

Reflects the 12/31/09 information adjusted to include 1/1/10 adoption of FAS

166/167 as reported in our SEC filings. $ in billions

As Reported

2006

2007

2008

4Q09

4Q09

Tangible common shareholder's equity

59.1

$

56.4

$

50.7

$

112.5

$

118.6

$

Tangible assets

1,386.5

1,629.8

1,729.3

2,235.8

2,135.4

Ratio

4.3%

3.5%

2.9%

5.0%

5.6%

Common shareholder's equity

132.4

$

142.4

$

139.4

$

188.1

$

194.2

$

Assets

1,459.7

1,715.7

1,817.9

2,330.7

2,230.2

Ratio

9.1%

8.3%

7.7%

8.1%

8.7%

Tangible book value per share

13.26

$

12.71

$

10.11

$

11.31

$

11.94

$

Book value per share

29.70

$

32.09

$

27.77

$

20.87

$

21.48

$

Reconciling items from GAAP measures to

non-GAAP measures are:

Common equlivalent securities

-

$

-

$

-

$

19.2

$

19.2

$

Goodwill

(65.7)

(77.5)

(81.9)

(86.3)

(86.3)

Intangible assets (excluding MSRs)

(9.4)

(10.3)

(8.5)

(12.0)

(12.0)

Related deferred tax liabilities

1.8

1.9

1.9

3.5

3.5

$ in billions

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

estimate

Tangible common shareholder's equity

117.4

$

121.8

$

129.5

$

130.9

$

133.8

$

126.8

$

Tangible assets

2,250.2

2,275.0

2,256.8

2,184.2

2,194.0

2,196.5

Ratio

5.2%

5.4%

5.7%

6.0%

6.1%

5.8%

Common shareholder's equity

211.9

$

215.2

$

212.4

$

211.7

$

214.3

$

204.7

$

Assets

2,344.6

2,368.4

2,339.7

2,264.9

2,274.5

2,274.5

Ratio

9.0%

9.1%

9.1%

9.3%

9.4%

9.0%

Tangible book value per share

11.70

$

12.14

$

12.91

$

12.98

$

13.21

$

12.52

$

Book value per share

21.12

$

21.45

$

21.17

$

20.99

$

21.15

$

20.21

$

Reconciling items from GAAP measures to

non-GAAP measures are:

Goodwill

(86.3)

$

(85.8)

$

(75.6)

$

(73.9)

$

(73.9)

$

(71.3)

$

Intangible assets (excluding MSRs)

(11.5)

(10.8)

(10.4)

(9.9)

(9.6)

(9.6)

Related deferred tax liabilities

3.4

3.2

3.1

3.0

2.9

2.9

1 |

Note Relating to Non-GAAP Financial Disclosures

This page presents a reconciliation of estimated earnings adjusted for large items

expected to be recorded during the second quarter of 2011. The

after-tax amounts shown on large items assumes a 37% tax rate which could be different as actual results are finalized.

14

$ in billions

Estimated loss

(12.5)

$

to

(13.2)

$

(8.6)

$

to

(9.1)

$

Adjustments for large estimated items

Plus mortgage-related costs

Representations & warranties expense

14.0

14.0

8.8

8.8

Other mortgage-related costs

4.0

4.0

2.5

2.5

Goodwill impairment charge

2.6

2.6

2.6

2.6

Less gains

Gains from non-operating items

(2.5)

(2.5)

(1.6)

(1.6)

Adjusted estimated earnings

5.6

$

to

4.9

$

3.7

$

to

3.2

$

Pre-tax

After-tax |

|