CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of Each Class of Securities to be Registered |

Amount to be Registered |

Proposed Maximum Offering Price Per Unit |

Proposed Maximum Offering Price |

Amount of Fee(1) | ||||

| Currency-Linked Step Up Notes Linked to a Basket of Asian Currencies, due July 25, 2014 |

2,246,558 | $10.00 | $22,465,580 | $2,608.25 | ||||

|

| ||||||||

|

| ||||||||

| (1) | Calculated in accordance with Rule 457(r) of the Securities Act of 1933. |

Filed Pursuant to Rule 424(b)(2)

Registration No. 333-158663

The notes are being offered by Bank of America Corporation (“BAC”). The notes will have the terms specified in this term sheet as supplemented by the documents indicated below under “Additional Terms” (together, the “Note Prospectus”). Investing in the notes involves a number of risks. There are important differences between the notes and a conventional debt security, including different investment risks. See “Risk Factors” and “Additional Risk Factor” beginning on page TS-5 of this term sheet and “Risk Factors” beginning on page S-9 of product supplement STEP UP-2. The notes:

|

Are Not FDIC Insured |

Are Not Bank Guaranteed

|

May Lose Value

|

In connection with this offering, Merrill Lynch, Pierce, Fenner & Smith Incorporated (“MLPF&S”) is acting in its capacity as principal for your account.

None of the Securities and Exchange Commission (the “SEC”), any state securities commission, or any other regulatory body has approved or disapproved of these securities or determined if this Note Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Unit |

Total |

|||||||||

| Public offering price (1) |

$10.00 | $22,465.580.00 | ||||||||

| Underwriting discount (1) |

$0.20 | $449,311.60 | ||||||||

| Proceeds, before expenses, to Bank of America Corporation |

$9.80 | $22,016,268.40 | ||||||||

| (1) | The public offering price and underwriting discount for any purchase of 500,000 units or more in a single transaction by an individual investor will be $9.95 per unit and $0.15 per unit, respectively. |

| Merrill Lynch & Co.

|

| |||

| July 28, 2011 |

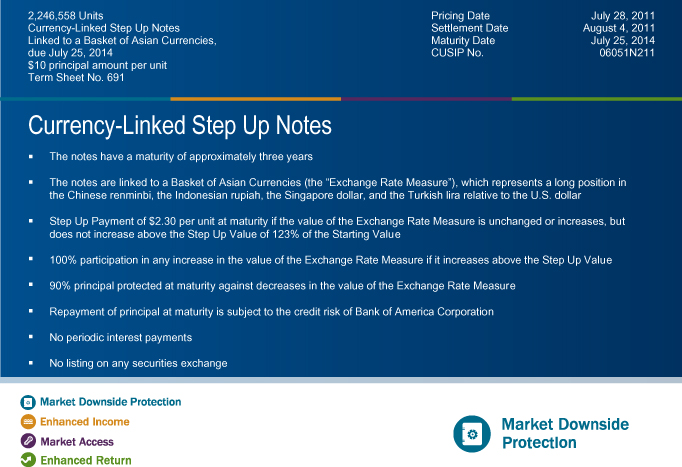

2,246,558 Units Pricing Date July 28, 2011

Currency-Linked Step Up Notes Settlement Date August 4, 2011

Linked to a Basket of Asian Currencies, Maturity Date July 25, 2014

due July 25, 2014 CUSIP No. 06051N211

$10 principal amount per unit

Term Sheet No. 691

Currency-Linked Step Up Notes

The notes have a maturity of approximately three years

The notes are linked to a Basket of Asian Currencies (the “Exchange Rate Measure”), which represents a long position in the Chinese renminbi, the Indonesian rupiah, the Singapore dollar, and the Turkish lira relative to the U.S. dollar

Step Up Payment of $2.30 per unit at maturity if the value of the Exchange Rate Measure is unchanged or increases, but does not increase above the Step Up Value of 123% of the Starting Value

100% participation in any increase in the value of the Exchange Rate Measure if it increases above the Step Up Value

90% principal protected at maturity against decreases in the value of the Exchange Rate Measure

Repayment of principal at maturity is subject to the credit risk of Bank of America Corporation

No periodic interest payments

No listing on any securities exchange

Summary

The Currency-Linked Step Up Notes Linked to a Basket of Asian Currencies, due July 25, 2014 (the “notes”) are our senior unsecured debt securities. The notes are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The notes will rank equally with all of our other unsecured and unsubordinated debt, and any payments due on the notes, including any repayment of principal, will be subject to the credit risk of BAC.

The notes are linked to a Basket of Asian Currencies (the “Exchange Rate Measure”), which tracks the value of an equally weighted investment in the Chinese renminbi, the Indonesian rupiah, the Singapore dollar, and the Turkish lira (each, an “underlying currency”), based on the exchange rate for each underlying currency relative to the U.S. dollar.

The notes provide investors with a Step Up Payment if the value of the Exchange Rate Measure is unchanged or increases from the Starting Value to the Ending Value, but does not increase above the Step Up Value. If the value of the Exchange Rate Measure increases (that is, the underlying currencies strengthen relative to the U.S. dollar) over the term of the notes from the Starting Value to an Ending Value that is above the Step Up Value, investors will participate on a 1-for-1 basis in the increase above the Starting Value. Investors must be willing to forgo interest payments on the notes and be willing to accept a repayment at maturity that is up to 10% less than the Original Offering Price.

Capitalized terms used but not defined in this term sheet have the meanings set forth in product supplement STEP UP-2. Unless otherwise indicated or unless the context requires otherwise, all references in this document to “we,” “us,” “our,” or similar references are to BAC.

|

Currency-Linked Step Up Notes |

TS-2 |

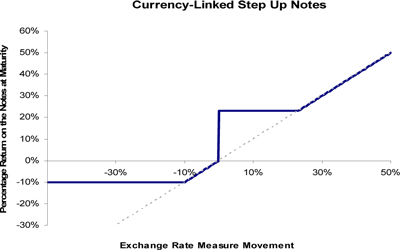

Hypothetical Payout Profile

|

This graph reflects the hypothetical returns on the notes at maturity, based on the Step Up Payment of $2.30, the Step Up Value of 123.00, and the Minimum Redemption Amount of $9.00. The blue line reflects the hypothetical returns on the notes, while the dotted gray line reflects the hypothetical returns of a direct investment in the Exchange Rate Measure.

This graph has been prepared for purposes of illustration only. Your actual return will depend on the actual Ending Value and the term of your investment. |

Hypothetical Redemption Amounts

The below table and examples are for purposes of illustration only. They are based on hypothetical values and show a hypothetical return on the notes. The actual amount you receive and the resulting total rate of return will depend on the actual Ending Value and the term of your investment.

The following table illustrates, for the Starting Value of 100 and a range of Ending Values:

| § | the percentage change from the Starting Value to the Ending Value; |

| § | the Redemption Amount per unit of the notes; and |

| § | the total rate of return to holders of the notes. |

The table and examples are based on the Step Up Payment of $2.30, the Step Up Value of 123.00, and the Minimum Redemption Amount of $9.00 per unit.

| Ending Value |

Percentage Change to the Ending Value |

Redemption Amount per Unit |

Total Rate of Return on the Notes | |||||||||||||||

| 50.00 | -50.00 | % | $9.00 | -10.00 | % | |||||||||||||

| 60.00 | -40.00 | % | $9.00 | -10.00 | % | |||||||||||||

| 70.00 | -30.00 | % | $9.00 | -10.00 | % | |||||||||||||

| 80.00 | -20.00 | % | $9.00 | -10.00 | % | |||||||||||||

| 90.00 | -10.00 | % | $9.00 | (1) | -10.00 | % | ||||||||||||

| 95.00 | -5.00 | % | $9.50 | -5.00 | % | |||||||||||||

| 97.00 | -3.00 | % | $9.70 | -3.00 | % | |||||||||||||

| 99.00 | -1.00 | % | $9.90 | -1.00 | % | |||||||||||||

| 100.00 | (2) | 0.00 | % | $12.30 | (3) | 23.00 | % | |||||||||||

| 101.00 | 1.00 | % | $12.30 | 23.00 | % | |||||||||||||

| 102.00 | 2.00 | % | $12.30 | 23.00 | % | |||||||||||||

| 103.00 | 3.00 | % | $12.30 | 23.00 | % | |||||||||||||

| 105.00 | 5.00 | % | $12.30 | 23.00 | % | |||||||||||||

| 110.00 | 10.00 | % | $12.30 | 23.00 | % | |||||||||||||

| 115.00 | 15.00 | % | $12.30 | 23.00 | % | |||||||||||||

| 120.00 | 20.00 | % | $12.30 | 23.00 | % | |||||||||||||

| 123.00 | (4) | 23.00 | % | $12.30 | 23.00 | % | ||||||||||||

| 130.00 | 30.00 | % | $13.00 | 30.00 | % | |||||||||||||

| 140.00 | 40.00 | % | $14.00 | 40.00 | % | |||||||||||||

| 150.00 | 50.00 | % | $15.00 | 50.00 | % | |||||||||||||

| (1) | The Redemption Amount will not be less than the Minimum Redemption Amount. |

| (2) | This is the Starting Value. |

| (3) | This amount represents the sum of the Original Offering Price and the Step Up Payment. |

| (4) | This is the Step Up Value. |

|

Currency-Linked Step Up Notes |

TS-3 |

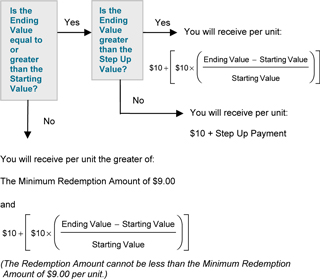

Example 1— The Ending Value is equal to 50.00:

| Redemption Amount (per unit) = the greater of (a) $10 + | [ | $10 × | ( | 50.00 – 100.00 | ) | ] | = $5.00 and (b) $9.00 | |||||||

| 100.00 |

Redemption Amount (per unit) = $9.00 (The Redemption Amount cannot be less than the Minimum Redemption Amount.)

Example 2— The Ending Value is equal to 97.00:

| Redemption Amount (per unit) |

= $10 + |

[ | $10 × | ( | 97.00 – 100.00 | ) | ] | = $9.70 | ||||||||||

| 100.00 |

Example 3— The Ending Value is equal to 102.00:

Redemption Amount (per unit) = $10.00 + $2.30 = $12.30

In this case, because the Ending Value is greater than the Starting Value but less than or equal to the Step Up Value, the Redemption Amount (per unit) will equal $12.30, which is the sum of the Original Offering Price of $10.00 and the Step Up Payment of $2.30.

Example 4—The Ending Value is equal to 130.00:

| Redemption Amount (per unit) |

= $10 + |

[ | $10 × | ( | 130.00 – 100.00 | ) | ] | = $13.00 | ||||||||||

| 100.00 |

In this case, because the Ending Value is greater than the Step Up Value, the Redemption Amount (per unit) will equal $13.00.

|

Currency-Linked Step Up Notes |

TS-4 |

Risk Factors

There are important differences between the notes and a conventional debt security. An investment in the notes involves significant risks, including those listed below. You should carefully review the more detailed explanation of risks relating to the notes in the “Risk Factors” sections beginning on page S-9 of product supplement STEP UP-2 and page S-4 of the MTN prospectus supplement identified below under “Additional Terms.” We also urge you to consult your investment, legal, tax, accounting, and other advisors before you invest in the notes.

| § | Your investment may result in a loss; there is no guaranteed return of principal. |

| § | Your yield may be less than the yield on a conventional debt security of comparable maturity. |

| § | Changes in the exchange rates of the underlying currencies may offset each other. |

| § | You must rely on your own evaluation of the merits of an investment linked to the Exchange Rate Measure. |

| § | In seeking to provide you with what we believe to be competitive terms for the notes while providing MLPF&S with compensation for its services, we have considered the costs of developing, hedging, and distributing the notes described on page TS-7. The price at which you may sell the notes in any secondary market may be lower than the public offering price due to, among other things, the inclusion of these costs. |

| § | A trading market is not expected to develop for the notes. MLPF&S is not obligated to make a market for, or to repurchase, the notes. |

| § | Payments on the notes are subject to our credit risk, and changes in our credit ratings are expected to affect the value of the notes. |

| § | The Redemption Amount will not be affected by all developments relating to the Exchange Rate Measure. |

| § | If you attempt to sell the notes prior to maturity, their market value, if any, will be affected by various factors that interrelate in complex ways, and their market value may be less than their Original Offering Price. |

| § | Purchases and sales by us and our affiliates of the underlying currencies may affect your return. |

| § | Our trading and hedging activities may create conflicts of interest with you. |

| § | Our hedging activities may affect your return at maturity and the market value of the notes. |

| § | There may be potential conflicts of interest involving the calculation agent. We have the right to appoint and remove the calculation agent. |

| § | The return on the notes depends on the exchange rates of the underlying currencies, which are affected by many complex factors outside of our control. |

| § | The exchange rates could be affected by the actions of the governments of China, Indonesia, Singapore, Turkey, and the United States. |

| § | Even though currencies trade around-the-clock, the notes will not trade around-the-clock, and the prevailing market prices for the notes may not reflect the current exchange rates. |

| § | Suspensions or disruptions of market trading in the underlying currencies and the U.S. dollar may adversely affect the value of the notes. |

| § | The notes are payable only in U.S. dollars and you will have no right to receive any payments in any underlying currency. |

| § | The U.S. federal income tax consequences of the notes are uncertain and may be adverse to a holder of the notes. See “Summary Tax Consequences” and “Certain U.S. Federal Income Taxation Considerations” below and “U.S. Federal Income Tax Summary” beginning on page S-23 of product supplement STEP UP-2. |

Additional Risk Factor

The exchange rate of the Chinese renminbi is currently managed by the Chinese government.

On July 21, 2005, the People’s Bank of China, with the authorization of the State Council of the People’s Republic of China, announced that the Chinese renminbi exchange rate would no longer be pegged to the U.S. dollar and would float within managed bands, which the People’s Bank of China resets daily. After the closing of the market on each business day, the People’s Bank of China announces the closing price of a foreign currency, such as the U.S. dollar, traded against the Chinese renminbi in the interbank foreign exchange market.

The initial adjustment of the Chinese renminbi exchange rate occurred on July 21, 2005 and resulted in an approximate 2% revaluation from an exchange rate of 8.28 renminbi per U.S. dollar to 8.11 renminbi per U.S. dollar. As of the pricing date, the exchange rate was 6.4438 renminbi per U.S. dollar. The People’s Bank of China has also announced that the daily trading price of the U.S. dollar against the renminbi in the interbank foreign exchange market will continue to be allowed to float within a band of 0.50 percent around the central parity published by the People’s Bank of China, while the trading prices of the non-U.S. dollar currencies against the renminbi will be allowed to move within a certain band announced by the People’s Bank of China. The People’s Bank of China will announce the closing price of a foreign currency such as the U.S. dollar traded against the renminbi in the interbank foreign

|

Currency-Linked Step Up Notes |

TS-5 |

exchange market after the closing of the market on each working day, and will make it the central parity for trading against the renminbi on the following working day. The People’s Bank of China has stated that it will make adjustments to the renminbi exchange rate band when necessary according to market, economic, and financial developments.

The People’s Bank of China has indicated that an upward revaluation in the value of the Chinese renminbi against the U.S. dollar may be allowed; however, no assurances can be given that this will occur. Despite the change in its exchange rate regime, the Chinese government continues to manage the valuation of the renminbi and, as currently managed, its price movements may not contribute significantly to either an increase or decrease in the value of the Exchange Rate Measure. However, further changes in the Chinese government’s management of the renminbi could result in a significant movement in the U.S. dollar/renminbi exchange rate. Assuming the value of the other underlying currencies in the Exchange Rate Measure remain constant, a decrease in the value of the renminbi relative to the U.S. dollar, whether as a result of a change in the Chinese government’s management of the renminbi or for other reasons, would result in a decrease in the value of the Exchange Rate Measure.

Investor Considerations

|

Currency-Linked Step Up Notes |

TS-6 |

Supplement to the Plan of Distribution; Role of MLPF&S and Conflicts of Interest

We will deliver the notes against payment therefor in New York, New York on a date that is greater than three business days following the pricing date. Under Rule 15c6-1 of the Securities Exchange Act of 1934, trades in the secondary market generally are required to settle in three business days, unless the parties to any such trade expressly agree otherwise. Accordingly, purchasers who wish to trade the notes more than three business days prior to the original issue date will be required to specify alternative settlement arrangements to prevent a failed settlement.

The notes will not be listed on any securities exchange. In the original offering, the notes will be sold in minimum investment amounts of 100 units.

MLPF&S, a broker-dealer subsidiary of BAC, is a member of the Financial Industry Regulatory Authority, Inc. (“FINRA”) and will participate as selling agent in the distribution of the notes. Accordingly, offerings of the notes will conform to the requirements of FINRA Rule 5121 applicable to FINRA members. MLPF&S may not make sales in this offering to any of its discretionary accounts without the prior written approval of the account holder.

Under our distribution agreement with MLPF&S, MLPF&S will purchase the notes from us as principal at the public offering price indicated on the cover of this term sheet, less the indicated underwriting discount. The public offering price includes, in addition to the underwriting discount, a charge of approximately $0.075 per unit. This charge reflects an estimated profit earned by MLPF&S from transactions through which the notes are structured and resulting obligations hedged. The fees charged reduce the economic terms of the notes. Actual profits or losses from these hedging transactions may be more or less than this amount. In entering into the hedging arrangements for the notes, we seek competitive terms and may enter into hedging transactions with a division of MLPF&S or one of our subsidiaries or affiliates. For further information regarding these charges, our trading and hedging activities and conflicts of interest, see “Risks Factors,” beginning on page S-9 and “Use of Proceeds” on page S-16 in Product Supplement STEP UP-2.

If you place an order to purchase the notes, you are consenting to MLPF&S acting as a principal in effecting the transaction for your account.

MLPF&S may repurchase and resell the notes, with repurchases and resales being made at prices related to then-prevailing market prices or at negotiated prices. MLPF&S may act as principal or agent in these market-making transactions; however, it is not obligated to engage in any such transactions.

|

Currency-Linked Step Up Notes |

TS-7 |

The Basket of Asian Currencies

The notes are designed to allow investors to participate in the movements of the Exchange Rate Measure over the term of the notes. The Exchange Rate Measure is designed to track the value of an equally weighted investment in the Chinese renminbi, the Indonesian rupiah, the Singapore dollar, and the Turkish lira, based on the exchange rate of each underlying currency relative to the U.S. dollar. The notes provide upside participation at maturity if the value of the Exchange Rate Measure increases (that is, the underlying currencies strengthen relative to the U.S. dollar) over the term of the notes.

The exchange rate for each underlying currency is expressed as the number of units of the applicable underlying currency for which one U.S. dollar can be exchanged. Accordingly, an increase in the applicable exchange rate means that the value of the relevant underlying currency has weakened against the U.S. dollar, and a decrease in the applicable exchange rate means that the value of the relevant underlying currency has strengthened against the U.S. dollar. If investing in the notes, investors should be of the view that the value of the Exchange Rate Measure will increase over the term of the notes (that is, the underlying currencies will strengthen relative to the U.S. dollar from the Initial Exchange Rate, determined on the pricing date, to the Final Exchange Rate, determined on a calculation day shortly before the maturity date).

For each underlying currency, the Initial Exchange Rate (which was rounded to four decimal places) was determined, and the Final Exchange Rate (which will be rounded to four decimal places) will be determined, as follows:

| § | Chinese renminbi: the number of Chinese renminbi for which one U.S. dollar can be exchanged as reported by Reuters on page SAEC, or any substitute page thereto, at approximately 9:15 a.m. in Beijing, China. |

| § | Indonesian rupiah: the number of Indonesian rupiahs for which one U.S. dollar can be exchanged as reported by Reuters on page ABSIRFIX01, or any substitute page thereto, under USD, at approximately 11:00 a.m. in Singapore. |

| § | Singapore dollar: the number of Singapore dollars for which one U.S. dollar can be exchanged as reported by Reuters on page ABSIRFIX01, or any substitute page thereto, under USD, at approximately 11:00 a.m. in Singapore. |

| § | Turkish lira: the number of Turkish lira for which one U.S. dollar can be exchanged as reported by Reuters on page WMRSPOT, or any substitute page thereto, under USD, at approximately 4:00 p.m. in London. |

If the calculation agent determines that the scheduled calculation day is not a business day by reason of an extraordinary event, occurrence, declaration, or otherwise, or if the exchange rate for an underlying currency is not so quoted on the applicable page indicated above on the scheduled calculation day (each, a “Non-Publication Event”), then the calculation agent will determine the Final Exchange Rate for that underlying currency on the next applicable business day on which the exchange rate is so quoted. However, in no event will the determination of the Final Exchange Rate for any underlying currency be postponed to a date (the “final determination date”) that is later than the close of business in New York, New York on the second scheduled business day prior to the maturity date.

If, following a Non-Publication Event and postponement as described above, the exchange rate for any underlying currency remains not quoted on the final determination date, the Final Exchange Rate for that currency will nevertheless be determined on the final determination date. The calculation agent, in its sole discretion, will determine the Final Exchange Rate for that underlying currency, the applicable Weighted Return and the Ending Value of the Exchange Rate Measure in a manner which the calculation agent considers commercially reasonable under the circumstances. In making its determination, the calculation agent may take into account spot quotations for the applicable underlying currency and any other information that it deems relevant.

The Final Exchange Rate for each underlying currency that is not affected by a Non-Publication Event will be determined on the scheduled calculation day.

The Starting Value was set to 100 on the pricing date.

The Ending Value will equal the value of the Exchange Rate Measure on the calculation day.

The value of the Exchange Rate Measure on the calculation day will equal: 100 + 100 × (the sum of the Weighted Return for each exchange rate), rounded to two decimal places.

|

Currency-Linked Step Up Notes |

TS-8 |

The Weighted Return for each exchange rate will be determined by the calculation agent as follows:

| § Chinese renminbi: |

Exchange Rate Weighting × | ( | Initial Exchange Rate - Final Exchange Rate | ) | ||||||

| Final Exchange Rate | ||||||||||

| § Indonesian rupiah: |

Exchange Rate Weighting × | ( | Initial Exchange Rate - Final Exchange Rate | ) | ||||||

| Final Exchange Rate | ||||||||||

| § Singapore dollar: |

Exchange Rate Weighting × | ( | Initial Exchange Rate - Final Exchange Rate | ) | ||||||

| Final Exchange Rate | ||||||||||

| § Turkish lira: |

Exchange Rate Weighting × | ( | Initial Exchange Rate - Final Exchange Rate | ) | ||||||

| Final Exchange Rate | ||||||||||

The formulas above will result in the Weighted Return for an exchange rate being positive when the underlying currency strengthens relative to the U.S. dollar and being negative when that underlying currency weakens relative to the U.S. dollar. Assuming the Final Exchange Rate for the other underlying currencies remain the same, any strengthening of an underlying currency relative to the U.S. dollar will result in an increase in the Ending Value while any weakening of an underlying currency relative to the U.S. dollar will result in a decrease in the Ending Value.

The strengthening of an underlying currency relative to the U.S. dollar will result in a decrease in the applicable exchange rate, while the weakening of an underlying currency relative to the U.S. dollar will result in an increase in the applicable exchange rate.

The “Exchange Rate Weighting” with respect to each exchange rate equals 25%, reflecting an equal weighting for each underlying currency in the Exchange Rate Measure.

The “Initial Exchange Rate” for each underlying currency was determined on the pricing date.

The “Final Exchange Rate” for each underlying currency will be determined on the calculation day, subject to postponement as described above.

|

Currency-Linked Step Up Notes |

TS-9 |

Hypothetical Calculations of the Weighted Returns and the Ending Value

Set forth below are two examples of hypothetical Weighted Return and hypothetical Ending Value calculations (rounded to two decimal places) based on the Initial Exchange Rates and assuming hypothetical Final Exchange Rates for each exchange rate as follows.

Example 1:

| Underlying Currency |

Exchange Rate Weighting |

Initial Exchange Rate |

Hypothetical Final |

Hypothetical | ||||

| Chinese renminbi |

25.00% | 6.4438 | 12.8876 | -12.50% | ||||

| Indonesian rupiah |

25.00% | 8,509.0000 | 6,892.2900 | 5.86% | ||||

| Singapore dollar |

25.00% | 1.2033 | 1.8050 | -8.33% | ||||

| Turkish lira |

25.00% | 1.6718 | 2.5077 | -8.33% |

The hypothetical Weighted Return for each exchange rate is determined as follows:

| § Chinese renminbi: |

25% × | ( | 6.4438 - 12.8876 | ) | = -12.50% | |||||

| 12.8876 | ||||||||||

| § Indonesian rupiah: |

25% × | ( | 8,509.0000 - 6,892.2900 | ) | = 5.86% | |||||

| 6,892.2900 | ||||||||||

| § Singapore dollar: |

25% × | ( | 1.2033 - 1.8050 | ) | = -8.33% | |||||

| 1.85050 | ||||||||||

| § Turkish lira: |

25% × | ( | 1.6718 - 2.5077 | ) | = -8.33% | |||||

| 2.5077 | ||||||||||

The hypothetical Ending Value would be 76.70, determined as follows:

100 + 100 x (sum of the Weighted Return for each exchange rate), rounded to two decimal places

100 + 100 x (–12.50 + 5.86 – 8.33 – 8.33)%

100 + 100 x (–23.30%) = 76.70

Example 2:

| Underlying Currency |

Exchange Rate Weighting |

Initial Exchange Rate |

Hypothetical Final |

Hypothetical | ||||

| Chinese renminbi |

25.00% | 6.4438 | 5.7994 | 2.78% | ||||

| Indonesian rupiah |

25.00% | 8,509.0000 | 10,210.8000 | -4.17% | ||||

| Singapore dollar |

25.00% | 1.2033 | 1.2153 | -0.25% | ||||

| Turkish lira |

25.00% | 1.6718 | 1.2539 | 8.33% |

The hypothetical Weighted Return for each exchange rate is determined as follows:

| § Chinese renminbi: |

25% × | ( | 6.4438 - 5.7994 | ) | = 2.78% | |||||

| 5.7994 | ||||||||||

| § Indonesian rupiah: |

25% × | ( | 8,509.0000 - 10,210.8000 | ) | = -4.17% | |||||

| 10,210.8000 | ||||||||||

| § Singapore dollar: |

25% × | ( | 1.2033 - 1.2153 | ) | = -0.25% | |||||

| 1.2153 | ||||||||||

| § Turkish lira: |

25% × | ( | 1.6718 - 1.2539 | ) | = 8.33% | |||||

| 1.2539 | ||||||||||

The hypothetical Ending Value would be 106.69, determined as follows:

100 + 100 x (sum of the Weighted Return for each exchange rate), rounded to two decimal places

100 + 100 x (2.78 – 4.17– 0.25 + 8.33)%

100 + 100 x (6.69%) = 106.69

|

Currency-Linked Step Up Notes |

TS-10 |

Historical Data on the Exchange Rates

The following tables set forth the high and low daily exchange rates for each underlying currency from the first quarter of 2006 through the pricing date. These exchange rates were obtained from publicly available information on Bloomberg, L.P. These exchange rates should not be taken as an indication of the future performance of any of the underlying currencies or the Exchange Rate Measure, or as an indication of whether, or to what extent, the Ending Value will be greater than the Starting Value.

As described above, the exchange rate for each underlying currency is expressed as the number of units of the applicable underlying currency for which one U.S. dollar can be exchanged. As a result, the “High” values represent the weakest that currency was relative to the U.S. dollar for the given quarter, while the “Low” values represent the strongest that currency was relative to the U.S. dollar for the given quarter.

Chinese renminbi

The following table sets forth the high and low daily exchange rates for the Chinese renminbi for the calendar quarters from the first quarter of 2006 through the pricing date. The Initial Exchange Rate for the Chinese renminbi was 6.4438 Chinese renminbi per U.S. dollar.

| High | Low | |||

| 2006 |

||||

| First Quarter | 8.0702 | 8.0172 | ||

| Second Quarter | 8.0265 | 7.9943 | ||

| Third Quarter | 8.0048 | 7.8965 | ||

| Fourth Quarter | 7.9149 | 7.8045 | ||

| 2007 |

||||

| First Quarter | 7.8160 | 7.7269 | ||

| Second Quarter | 7.7350 | 7.6151 | ||

| Third Quarter | 7.6059 | 7.5036 | ||

| Fourth Quarter | 7.5276 | 7.3037 | ||

| 2008 |

||||

| First Quarter | 7.3041 | 7.0116 | ||

| Second Quarter | 7.0185 | 6.8544 | ||

| Third Quarter | 6.8792 | 6.8113 | ||

| Fourth Quarter | 6.8872 | 6.8171 | ||

| 2009 |

||||

| First Quarter | 6.8519 | 6.8270 | ||

| Second Quarter | 6.8373 | 6.8192 | ||

| Third Quarter | 6.8362 | 6.8259 | ||

| Fourth Quarter | 6.8311 | 6.8233 | ||

| 2010 |

||||

| First Quarter | 6.8339 | 6.8256 | ||

| Second Quarter | 6.8333 | 6.7818 | ||

| Third Quarter | 6.8108 | 6.6873 | ||

| Fourth Quarter | 6.6917 | 6.6070 | ||

| 2011 |

||||

| First Quarter | 6.6350 | 6.5483 | ||

| Second Quarter | 6.5477 | 6.4634 | ||

| Third Quarter (through the pricing date) | 6.4721 | 6.4419 | ||

|

Currency-Linked Step Up Notes |

TS-11 |

Indonesian rupiah

The following table sets forth the high and low daily exchange rates for the Indonesian rupiah for the calendar quarters from the first quarter of 2006 through the pricing date. The Initial Exchange Rate for the Indonesian rupiah was 8,509.0000 Indonesian rupiahs per U.S. dollar.

| High | Low | |||

| 2006 | ||||

| First Quarter | 9,815.0000 | 9,045.0000 | ||

| Second Quarter | 9,495.0000 | 8,703.0000 | ||

| Third Quarter | 9,295.0000 | 9,045.0000 | ||

| Fourth Quarter | 9,228.0000 | 8,995.0000 | ||

| 2007 | ||||

| First Quarter | 9,255.0000 | 8,973.0000 | ||

| Second Quarter | 9,125.0000 | 8,675.0000 | ||

| Third Quarter | 9,480.0000 | 9,000.0000 | ||

| Fourth Quarter | 9,433.0000 | 9,053.0000 | ||

| 2008 | ||||

| First Quarter | 9,458.0000 | 9,060.0000 | ||

| Second Quarter | 9,355.0000 | 9,189.0000 | ||

| Third Quarter | 9,506.0000 | 9,073.0000 | ||

| Fourth Quarter | 12,650.0000 | 9,478.0000 | ||

| 2009 | ||||

| First Quarter | 12,100.0000 | 10,805.0000 | ||

| Second Quarter | 11,595.0000 | 9,930.0000 | ||

| Third Quarter | 10,293.0000 | 9,658.0000 | ||

| Fourth Quarter | 9,665.0000 | 9,340.0000 | ||

| 2010 | ||||

| First Quarter | 9,428.0000 | 9,090.0000 | ||

| Second Quarter | 9,378.0000 | 9,008.0000 | ||

| Third Quarter | 9,071.0000 | 8,908.0000 | ||

| Fourth Quarter | 9,048.0000 | 8,890.0000 | ||

| 2011 | ||||

| First Quarter | 9,073.0000 | 8,708.0000 | ||

| Second Quarter | 8,696.0000 | 8,513.0000 | ||

| Third Quarter (through the pricing date) | 8,578.0000 | 8,487.0000 | ||

|

Currency-Linked Step Up Notes |

TS-12 |

Singapore dollar

The following table sets forth the high and low daily exchange rates for the Singapore dollar for the calendar quarters from the first quarter of 2006 through the pricing date. The Initial Exchange Rate for the Singapore dollar was 1.2033 Singapore dollars per U.S. dollar.

| High | Low | |||

| 2006 |

||||

| First Quarter | 1.6605 | 1.6140 | ||

| Second Quarter | 1.6157 | 1.5608 | ||

| Third Quarter | 1.5953 | 1.5673 | ||

| Fourth Quarter | 1.5906 | 1.5344 | ||

| 2007 |

||||

| First Quarter | 1.5450 | 1.5159 | ||

| Second Quarter | 1.5428 | 1.5102 | ||

| Third Quarter | 1.5342 | 1.4852 | ||

| Fourth Quarter | 1.4821 | 1.4393 | ||

| 2008 |

||||

| First Quarter | 1.4478 | 1.3756 | ||

| Second Quarter | 1.3841 | 1.3501 | ||

| Third Quarter | 1.4393 | 1.3482 | ||

| Fourth Quarter | 1.5302 | 1.4301 | ||

| 2009 |

||||

| First Quarter | 1.5549 | 1.4349 | ||

| Second Quarter | 1.5189 | 1.4367 | ||

| Third Quarter | 1.4640 | 1.4097 | ||

| Fourth Quarter | 1.4161 | 1.3795 | ||

| 2010 |

||||

| First Quarter | 1.4241 | 1.3875 | ||

| Second Quarter | 1.4179 | 1.3671 | ||

| Third Quarter | 1.3940 | 1.3164 | ||

| Fourth Quarter | 1.3202 | 1.2822 | ||

| 2011 |

||||

| First Quarter | 1.2977 | 1.2605 | ||

| Second Quarter | 1.2606 | 1.2232 | ||

| Third Quarter (through the pricing date) | 1.2280 | 1.2021 | ||

|

Currency-Linked Step Up Notes |

TS-13 |

Turkish lira

The following table sets forth the high and low daily exchange rates for the Turkish lira for the calendar quarters from the first quarter of 2006 through the pricing date. The Initial Exchange Rate for the Turkish lira was 1.6718 Turkish lira per U.S. dollar.

| High | Low | |||

| 2006 |

||||

| First Quarter | 1.3590 | 1.3028 | ||

| Second Quarter | 1.7077 | 1.3175 | ||

| Third Quarter | 1.5988 | 1.4400 | ||

| Fourth Quarter | 1.5155 | 1.4134 | ||

| 2007 |

||||

| First Quarter | 1.4535 | 1.3813 | ||

| Second Quarter | 1.3884 | 1.3019 | ||

| Third Quarter | 1.3926 | 1.2072 | ||

| Fourth Quarter | 1.2307 | 1.1685 | ||

| 2008 |

||||

| First Quarter | 1.3241 | 1.1508 | ||

| Second Quarter | 1.3303 | 1.2163 | ||

| Third Quarter | 1.2883 | 1.1535 | ||

| Fourth Quarter | 1.7320 | 1.2720 | ||

| 2009 |

||||

| First Quarter | 1.8080 | 1.5120 | ||

| Second Quarter | 1.6545 | 1.5218 | ||

| Third Quarter | 1.5620 | 1.4530 | ||

| Fourth Quarter | 1.5289 | 1.4425 | ||

| 2010 |

||||

| First Quarter | 1.5517 | 1.4493 | ||

| Second Quarter | 1.6128 | 1.4708 | ||

| Third Quarter | 1.5799 | 1.4456 | ||

| Fourth Quarter | 1.5624 | 1.3950 | ||

| 2011 |

||||

| First Quarter | 1.6191 | 1.5403 | ||

| Second Quarter | 1.6426 | 1.5106 | ||

| Third Quarter (through the pricing date) | 1.7154 | 1.6069 | ||

|

Currency-Linked Step Up Notes |

TS-14 |

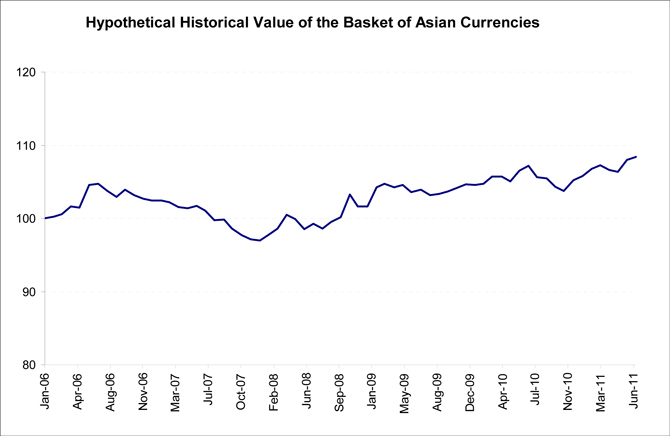

While historical information on the Exchange Rate Measure did not exist before the pricing date, the following graph sets forth hypothetical monthly historical values of the Exchange Rate Measure from January 1, 2006 through June 30, 2011 based upon historical exchange rates for the underlying currencies as of the end of each month. For purposes of this graph, the value of the Exchange Rate Measure was set to 100 as of December 31, 2005 and the value of the Exchange Rate Measure as of the end of each month is based upon the hypothetical Ending Value as of the end of that month, calculated as described in the section “The Basket of Asian Currencies” above. This historical data on the exchange rates as reported by Bloomberg is not necessarily indicative of the future performance of the underlying currencies or the Exchange Rate Measure or what the value of the notes may be. Any historical upward or downward trend in the value of the Exchange Rate Measure during any period set forth below is not an indication that the Ending Value will be greater than the Starting Value.

|

Currency-Linked Step Up Notes |

TS-15 |

Summary Tax Consequences

You should consider the U.S. federal income tax consequences of an investment in the notes, including the following:

| • | Although there are no statutory provisions, regulations, published rulings, or judicial decisions addressing the characterization, for U.S. federal income tax purposes, of the notes, we intend to treat the notes as debt instruments for U.S. federal income tax purposes and, where required, intend to file information returns with the IRS in accordance with such treatment. |

| • | A U.S. Holder will be required to report original issue discount (“OID”) or interest income based on a “comparable yield” with respect to a note without regard to cash, if any, received on the notes. |

| • | Upon a sale, exchange, or retirement of a note prior to maturity, a U.S. Holder generally will recognize taxable gain or loss equal to the difference between the amount realized on the sale, exchange, or retirement and the holder’s tax basis in the notes. A U.S. Holder generally will treat any gain as ordinary interest income, and any loss as ordinary up to the amount of previously accrued OID and then as capital loss. At maturity, (i) if the actual Redemption Amount exceeds the projected Redemption Amount, a U.S. Holder must include such excess as interest income, or (ii) if the projected Redemption Amount exceeds the actual Redemption Amount, a U.S. Holder will generally treat such excess first as an offset to previously accrued OID for the taxable year, then as an ordinary loss to the extent of all prior OID inclusions, and thereafter as a capital loss. |

Certain U.S. Federal Income Taxation Considerations

Set forth below is a summary of certain U.S. federal income tax considerations relating to an investment in the notes. The following summary is not complete and is qualified in its entirety by the discussion under the section entitled “U.S. Federal Income Tax Summary” beginning on page S-23 of product supplement STEP UP-2, which you should carefully review prior to investing in the notes. Capitalized terms used and not defined herein have the meanings ascribed to them in product supplement STEP UP-2.

General. There are no statutory provisions, regulations, published rulings, or judicial decisions addressing the characterization, for U.S. federal income tax purposes, of the notes or other instruments with terms substantially the same as the notes. However, although the matter is not free from doubt, under current law, each note should be treated as a debt instrument for U.S. federal income tax purposes. We currently intend to treat the notes as debt instruments for U.S. federal income tax purposes and, where required, intend to file information returns with the IRS in accordance with such treatment, in the absence of any change or clarification in the law, by regulation or otherwise, requiring a different characterization of the notes. You should be aware, however, that the IRS is not bound by our characterization of the notes as indebtedness and the IRS could possibly take a different position as to the proper characterization of the notes for U.S. federal income tax purposes. If the notes are not in fact treated as debt instruments for U.S. federal income tax purposes, then the U.S. federal income tax treatment of the purchase, ownership, and disposition of the notes could differ materially from the treatment discussed below, with the result that the timing and character of income, gain, or loss recognized in respect of a note could differ materially from the timing and character of income, gain, or loss recognized in respect of a note had the notes in fact been treated as debt instruments for U.S. federal income tax purposes. Accordingly, prospective purchasers are urged to consult their own tax advisors regarding the tax consequences of investing in the notes. The following summary assumes that the notes will be treated as debt instruments of BAC for U.S. federal income tax purposes.

Interest Accruals. The amount payable on the notes at maturity will depend on the performance of the Exchange Rate Measure. We intend to take the position that the “denomination currency” (as defined in the applicable Treasury regulations) of the notes is the U.S. dollar and, accordingly, we intend to take the position that the notes will be treated as “contingent payment debt instruments” for U.S. federal income tax purposes, subject to taxation under the “noncontingent bond method,” and the balance of this discussion assumes that this characterization is proper and will be respected. Under this characterization, the notes generally will be subject to the Treasury regulations governing contingent payment debt instruments. Under those regulations, a U.S. Holder will be required to report OID or interest income based on a “comparable yield” and a “projected payment schedule,” established by us for determining interest accruals and adjustments with respect to a note. A U.S. Holder who does not use the “comparable yield” and follow the “projected payment schedule” to calculate its OID and interest income on a note must timely disclose and justify the use of other estimates to the IRS.

Sale, Exchange, or Retirement of the Notes. Upon a sale, exchange, or retirement of a note prior to maturity, a U.S. Holder generally will recognize taxable gain or loss equal to the difference between the amount realized on the sale, exchange, or retirement and the holder’s tax basis in the notes. A U.S. Holder’s tax basis in a note generally will equal the cost of that note, increased by the amount of OID previously accrued by the holder for that note (without regard to any positive or negative adjustments under the contingent payment debt regulations). A U.S. Holder generally will treat any gain as interest income, and will treat any loss as ordinary loss to the extent of the excess of previous interest inclusions over the total negative adjustments previously taken into account as ordinary losses, and the balance as long-term or short-term capital loss depending upon the U.S. Holder’s holding period for the notes. At maturity, (i) if the actual Redemption Amount exceeds the projected Redemption Amount, a U.S. Holder must include such excess as interest income, or (ii) if the projected Redemption Amount exceeds the actual Redemption Amount, a U.S. Holder will generally treat such excess first as an offset to previously accrued OID for the taxable year, then as an ordinary loss to the extent of all prior OID inclusions, and thereafter as a capital loss. The deductibility of capital losses by a U.S. Holder is subject to limitations.

|

Currency-Linked Step Up Notes |

TS-16 |

Tax Accrual Table. The following table is based upon a projected payment schedule (including a projection for tax purposes of the Redemption Amount) and a comparable yield equal to 2.2508% per annum (compounded semi-annually) that we established for the notes. The table reflects the expected issuance of the notes on August 4, 2011 and the scheduled maturity date of July 25, 2014. This tax accrual table is based upon a projected payment schedule per $10 principal amount of the notes, which would consist of a single payment of $10.6885 at maturity. This information is provided solely for tax purposes, and we make no representations or predictions as to what the actual Redemption Amount will be.

|

Accrual Period |

Interest Deemed to Accrue on the Notes During Accrual Period (per Unit of the Notes) |

Total Interest Deemed to Have Accrued on the Notes as of End of Accrual Period (per Unit of the Notes) | ||

| August 4, 2011 to December 31, 2011 | $0.0919 | $0.0919 | ||

| January 1, 2012 to December 31, 2012 | $0.2285 | $0.3204 | ||

| January 1, 2013 to December 31, 2013 | $0.2336 | $0.5540 | ||

| January 1, 2014 to July 25, 2014 | $0.1345 | $0.6885 |

Projected Redemption Amount = $10.6885 per unit of the notes.

Additional Medicare Tax on Unearned Income. With respect to taxable years beginning after December 31, 2012, certain U.S. Holders, including individuals and estates and trusts, will be subject to an additional 3.8% Medicare tax on unearned income. For individual U.S. Holders, the additional Medicare tax applies to the lesser of (i) “net investment income,” or (ii) the excess of “modified adjusted gross income” over $200,000 ($250,000 if married and filing jointly or $125,000 if married and filing separately). “Net investment income” generally equals the taxpayer’s gross investment income reduced by the deductions that are allocable to such income. Investment income generally includes passive income such as interest, dividends, annuities, royalties, rents, and capital gains. U.S. Holders are urged to consult their own tax advisors regarding the implications of the additional Medicare tax resulting from an investment in the notes.

You should consult your own tax advisor concerning the U.S. federal income tax consequences to you of acquiring, owning, and disposing of the notes, as well as any tax consequences arising under the laws of any state, local, foreign, or other tax jurisdiction and the possible effects of changes in U.S. federal or other tax laws. See the discussion under the section entitled “U.S. Federal Income Tax Summary” beginning on page S-23 of product supplement STEP UP-2.

Validity of the Notes

In the opinion of McGuireWoods LLP, as counsel to BAC, when the notes offered by this Note Prospectus have been completed and executed by BAC, and authenticated by the trustee in accordance with the provisions of the Senior Indenture, and delivered against payment therefor as contemplated by this Note Prospectus, such notes will be legal, valid and binding obligations of BAC, subject to applicable bankruptcy, reorganization, insolvency, moratorium, fraudulent conveyance or other similar laws affecting the rights of creditors now or hereafter in effect, and to equitable principles that may limit the right to specific enforcement of remedies, and further subject to 12 U.S.C. §1818(b)(6)(D) (or any successor statute) and any bank regulatory powers now or hereafter in effect and to the application of principles of public policy. This opinion is given as of the date hereof and is limited to the Federal laws of the United States, the laws of the State of New York and the Delaware General Corporation Law (including the statutory provisions, all applicable provisions of the Delaware Constitution and reported judicial decisions interpreting the foregoing). In addition, this opinion is subject to customary assumptions about the trustee’s authorization, execution and delivery of the Senior Indenture, the validity, binding nature and enforceability of the Senior Indenture with respect to the trustee, the legal capacity of natural persons, the genuineness of signatures, the authenticity of all documents submitted to McGuireWoods LLP as originals, the conformity to original documents of all documents submitted to McGuireWoods LLP as photocopies, the authenticity of the originals of such copies and certain factual matters, all as stated in the letter of McGuireWoods LLP dated April 28, 2011, which has been filed as an exhibit to our Current Report on Form 8-K dated April 28, 2011.

|

Currency-Linked Step Up Notes |

TS-17 |

Additional Terms

You should read this term sheet, together with the documents listed below, which together contain the terms of the notes and supersede all prior or contemporaneous oral statements as well as any other written materials. You should carefully consider, among other things, the matters set forth under “Risk Factors” and “Additional Risk Factor” in the sections indicated on the cover of this term sheet. The notes involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting, and other advisors before you invest in the notes.

You may access the following documents on the SEC Website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC Website):

| § | Product supplement STEP UP-2 dated September 22, 2009: |

http://www.sec.gov/Archives/edgar/data/70858/000119312509195722/d424b5.htm

| § | Series L MTN prospectus supplement dated April 21, 2009 and prospectus dated April 20, 2009: |

http://www.sec.gov/Archives/edgar/data/70858/000095014409003387/g18667b5e424b5.htm

Our Central Index Key, or CIK, on the SEC Website is 70858.

We have filed a registration statement (including a product supplement, a prospectus supplement, and a prospectus) with the SEC for the offering to which this term sheet relates. Before you invest, you should read the product supplement, the prospectus supplement, and the prospectus in that registration statement, and the other documents relating to this offering that we have filed with the SEC for more complete information about us and this offering. You may get these documents without cost by visiting EDGAR on the SEC Website at www.sec.gov. Alternatively, we, any agent, or any dealer participating in this offering will arrange to send you the Note Prospectus if you so request by calling MLPF&S toll-free at 1-866-500-5408.

Market-Linked Investments Classification

Market-Linked Investments come in four basic categories, each designed to meet a different set of investor risk profiles, time horizons, income requirements and market views (bullish, bearish, moderate outlook, etc.). The following descriptions of these categories are meant solely for informational purposes and are not intended to represent any particular Market-Linked Investment or guarantee performance. Certain Market-Linked Investments may have overlapping characteristics.

Market Downside Protection Market-Linked Investments combine some of the capital preservation features of traditional bonds with the growth potential of equities and other asset classes. They offer full or partial market downside protection at maturity, while offering market exposure that may provide better returns than comparable fixed income securities. It is important to note that the market downside protection feature provides investors with protection only at maturity, subject to issuer credit risk. In addition, in exchange for full or partial protection, you forfeit dividends and full exposure to the linked asset’s upside. In some circumstances, this could result in a lower return than with a direct investment in the asset.

These short- to medium-term market-linked notes offer you a way to enhance your income stream, either through variable or fixed-interest coupons, an added payout at maturity based on the performance of the linked asset, or both. In exchange for receiving current income, you will generally forfeit upside potential on the linked asset. Even so, the prospect of higher interest payments and/or an additional payout may equate to a higher return potential than you may be able to find through other fixed-income securities. Enhanced Income Market-Linked Investments generally do not include market downside protection. The degree to which your principal is repaid at maturity is generally determined by the performance of the linked asset. Although enhanced income streams may help offset potential declines in the asset, you can still lose part or all of your original investment.

Market Access notes may offer exposure to certain market sectors, asset classes and/or strategies that may not even be available through the other three categories of Market-Linked Investments. Subject to certain fees, the returns on Market Access Market-Linked Investments will generally correspond on a one-to-one basis with any increases or decreases in the value of the linked asset, similar to a direct investment. In some instances, they may also provide interim coupon payments. These investments do not include the market downside protection feature and, therefore, your principal remains at risk.

These short- to medium-term investments offer you a way to enhance exposure to a particular market view without taking on a similarly enhanced level of market downside risk. They can be especially effective in a flat to moderately positive market (or, in the case of bearish investments, a flat to moderately negative market). In exchange for the potential to receive better-than market returns on the linked asset, you must generally accept a degree of market downside risk and capped upside potential. As these investments are not market downside protected, and do not assure full repayment of principal at maturity, you need to be prepared for the possibility that you may lose all or part of your investment.

|

Currency-Linked Step Up Notes |

TS-18 |