Filed Pursuant to Rule 433

Registration No. 333-180488

Subject to Completion

Preliminary Term Sheet dated June 22, 2012

The notes are being issued by Bank of America Corporation (“BAC”). There are important differences between the notes and a conventional debt security, including different investment risks. See “Risk Factors” on page TS-5 and “Additional Risk Factors” beginning on page TS-6 of this term sheet and “Risk Factors” beginning on page S-10 of product supplement ARN-4.

None of the Securities and Exchange Commission (the “SEC”), any state securities commission, or any other regulatory body has approved or disapproved of these securities or determined if this Note Prospectus (as defined below) is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Unit |

Total |

|||||||||

| Public offering price (1) (2) |

$10.00 | $ | ||||||||

| Underwriting discount (1) (2) |

$0.20 | $ | ||||||||

| Proceeds, before expenses, to BAC |

$9.80 | $ | ||||||||

| (1) | For any purchase of 500,000 units or more in a single transaction by an individual investor, the public offering price and the underwriting discount will be $9.95 per unit and $0.15 per unit, respectively. |

| (2) | For any purchase by certain fee-based trusts and discretionary accounts managed by U.S. Trust operating through Bank of America, N.A., the public offering price and underwriting discount will be $9.80 per unit and $0.00 per unit, respectively. |

The notes:

| Are Not FDIC Insured | Are Not Bank Guaranteed | May Lose Value |

Merrill Lynch & Co.

June , 2012

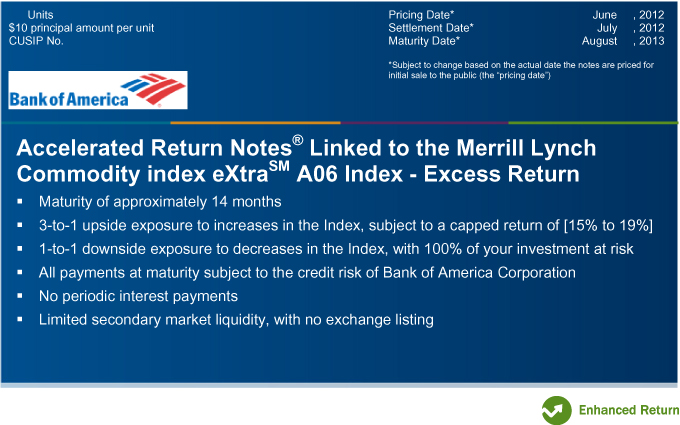

Units

$10 principal amount per unit

CUSIP No.

Pricing Date* June , 2012

Settlement Date* July , 2012

Maturity Date* August , 2013

*Subject to change based on the actual date the notes are priced for initial sale to the public (the “pricing date”)

Accelerated Return Notes® Linked to the Merrill Lynch Commodity index eXtraSM A06 Index—Excess Return

¡Maturity of approximately 14 months

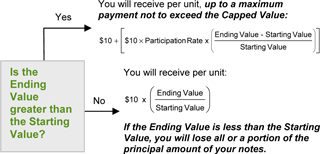

¡3-to-1 upside exposure to increases in the Index, subject to a capped return of [15% to 19%]

¡1-to-1 downside exposure to decreases in the Index, with 100% of your investment at risk

¡All payments at maturity subject to the credit risk of Bank of America Corporation

¡No periodic interest payments

¡Limited secondary market liquidity, with no exchange listing

| Accelerated Return Notes® Linked to the Merrill Lynch Commodity index eXtraSM A06 Index - Excess Return, due August , 2013 |

|

Summary

The Accelerated Return Notes® Linked to the Merrill Lynch Commodity index eXtraSM A06 Index — Excess Return due August , 2013 (the “notes”) are our senior unsecured debt securities. The notes are not guaranteed or insured by the Federal Deposit Insurance Corporation or secured by collateral. The notes will rank equally with all of our other unsecured and unsubordinated debt. Any payments due on the notes, including any repayment of principal, will be subject to the credit risk of BAC. The notes provide you a leveraged return, subject to a cap, if the Ending Value (as determined below) of the Merrill Lynch Commodity index eXtraSM A06 Index — Excess Return (the “Index”) is greater than the Starting Value. If the Ending Value is less than the Starting Value, you will lose all or a portion of the principal amount of your notes.

The terms and risks of the notes are contained in this term sheet and the documents listed below (together, the “Note Prospectus”). The documents have been filed as part of a registration statement with the SEC, which may, without cost, be accessed on the SEC website as indicated below or obtained from MLPF&S by calling 1-866-500-5408:

| § | Product supplement ARN-4 dated April 2, 2012: |

http://www.sec.gov/Archives/edgar/data/70858/000119312512146655/d326526d424b5.htm

| § | Series L MTN prospectus supplement dated March 30, 2012 and prospectus dated March 30, 2012: |

http://www.sec.gov/Archives/edgar/data/70858/000119312512143855/d323958d424b5.htm

Before you invest, you should read the Note Prospectus, including this term sheet, for information about us and this offering. Any prior or contemporaneous oral statements and any other written materials you may have received are superseded by the Note Prospectus. Capitalized terms used but not defined in this term sheet have the meanings set forth in product supplement ARN-4. Unless otherwise indicated or unless the context requires otherwise, all references in this document to “we,” “us,” “our,” or similar references are to BAC.

| Accelerated Return Notes® | TS-2 |

| Accelerated Return Notes® Linked to the Merrill Lynch Commodity index eXtraSM A06 Index - Excess Return, due August , 2013 |

|

Investor Considerations

We urge you to consult your investment, legal, tax, accounting, and other advisors before you invest in the notes.

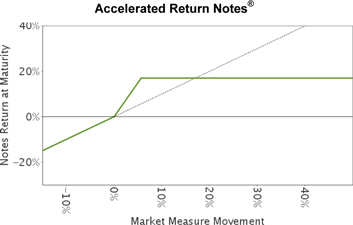

Hypothetical Payout Profile

The below graph is based on hypothetical numbers and values.

|

This graph reflects the returns on the notes, based on the Participation Rate of 300% and a Capped Value of $11.70, the midpoint of the Capped Value range of [$11.50 to $11.90]. The green line reflects the returns on the notes, while the dotted gray line reflects the returns of a direct investment in the components of the Index.

This graph has been prepared for purposes of illustration only. |

| Accelerated Return Notes® | TS-3 |

| Accelerated Return Notes® Linked to the Merrill Lynch Commodity index eXtraSM A06 Index - Excess Return, due August , 2013 |

|

Hypothetical Payments at Maturity

The following table and examples are for purposes of illustration only. They are based on hypothetical values and show hypothetical returns on the notes. The actual amount you receive and the resulting total rate of return will depend on the actual Starting Value, Ending Value, Capped Value, and the term of your investment.

The following table is based on a Starting Value of 100, the Participation Rate of 300% and a Capped Value of $11.70 per unit. It illustrates the effect of a range of Ending Values on the Redemption Amount per unit of the notes and the total rate of return to holders of the notes. The following examples do not take into account any tax consequences from investing in the notes.

| Ending Value |

Percentage Change from Value to the Ending Value |

Redemption |

Total Rate | |||||||||||||||

| 50.00 | -50.00 | % | $5.00 | -50.00 | % | |||||||||||||

| 60.00 | -40.00 | % | $6.00 | -40.00 | % | |||||||||||||

| 70.00 | -30.00 | % | $7.00 | -30.00 | % | |||||||||||||

| 80.00 | -20.00 | % | $8.00 | -20.00 | % | |||||||||||||

| 90.00 | -10.00 | % | $9.00 | -10.00 | % | |||||||||||||

| 92.00 | -8.00 | % | $9.20 | -8.00 | % | |||||||||||||

| 94.00 | -6.00 | % | $9.40 | -6.00 | % | |||||||||||||

| 96.00 | -4.00 | % | $9.60 | -4.00 | % | |||||||||||||

| 98.00 | -2.00 | % | $9.80 | -2.00 | % | |||||||||||||

| 100.00 | (1) | 0.00 | % | $10.00 | 0.00 | % | ||||||||||||

| 102.00 | 2.00 | % | $10.60 | 6.00 | % | |||||||||||||

| 104.00 | 4.00 | % | $11.20 | 12.00 | % | |||||||||||||

| 106.00 | 6.00 | % | $11.70 | (2) | 17.00 | % | ||||||||||||

| 108.00 | 8.00 | % | $11.70 | 17.00 | % | |||||||||||||

| 110.00 | 10.00 | % | $11.70 | 17.00 | % | |||||||||||||

| 117.00 | 17.00 | % | $11.70 | 17.00 | % | |||||||||||||

| 120.00 | 20.00 | % | $11.70 | 17.00 | % | |||||||||||||

| 130.00 | 30.00 | % | $11.70 | 17.00 | % | |||||||||||||

| 140.00 | 40.00 | % | $11.70 | 17.00 | % | |||||||||||||

| 150.00 | 50.00 | % | $11.70 | 17.00 | % | |||||||||||||

| (1) | The hypothetical Starting Value of 100 used in these examples has been chosen for illustrative purposes only, and does not represent a likely actual Starting Value for the Market Measure. |

| (2) | The Redemption Amount per unit cannot exceed the hypothetical Capped Value. |

For recent actual levels of the Market Measure, see “The Index” section below. In addition, all payments on the notes are subject to issuer credit risk.

Redemption Amount Calculation Examples

Example 1

The Ending Value is 80.00, or 80.00% of the Starting Value:

| Starting Value: | 100.00 | |||

| Ending Value: | 80.00 |

| $10 × |

( | 80 | ) | = $8.00 Redemption Amount per unit | ||||||||||||

| 100 | ||||||||||||||||

Example 2

The Ending Value is 103.00, or 103.00% of the Starting Value:

| Starting Value: | 100.00 | |||

| Ending Value: | 103.00 |

| $10 + |

[ | $10 × 300% × | ( | 103 – 100 | ) | ] | = $10.90 Redemption Amount per unit | |||||||||||

| 100 | ||||||||||||||||||

Example 3

The Ending Value is 130.00, or 130.00% of the Starting Value:

| Starting Value: | 100.00 | |||

| Ending Value: | 130.00 |

| $10 + |

[ | $10 × 300% × | ( | 130 – 100 | ) | ] | = $19.00, however, because the Redemption Amount for the notes cannot exceed the Capped Value, the Redemption Amount will be $11.70 per unit | |||||||||||

| 100 | ||||||||||||||||||

| Accelerated Return Notes® | TS-4 |

| Accelerated Return Notes® Linked to the Merrill Lynch Commodity index eXtraSM A06 Index - Excess Return, due August , 2013 |

|

Risk Factors

There are important differences between the notes and a conventional debt security. An investment in the notes involves significant risks, including those listed below. You should carefully review the more detailed explanation of risks relating to the notes in the “Risk Factors” sections beginning on page S-10 of product supplement ARN-4, page S-5 of the MTN prospectus supplement, and page 8 of the prospectus identified above under “Summary.” We also urge you to consult your investment, legal, tax, accounting, and other advisors before you invest in the notes.

| § | Depending on the performance of the Index measured shortly before the maturity date, your investment may result in a loss; there is no guaranteed return of principal. |

| § | Your yield may be less than the yield you could earn by owning a conventional debt security of comparable maturity. |

| § | Payments on the notes are subject to our credit risk, and actual or perceived changes in our creditworthiness are expected to affect the value of the notes. If we become insolvent or are unable to pay our obligations, you may lose your entire investment. |

| § | Your investment return, if any, is limited to the return represented by the Capped Value and may be less than a comparable investment directly in the components of the Index. |

| § | If you attempt to sell the notes prior to maturity, their market value may be lower than the price you paid for the notes due to, among other things, the inclusion of fees charged for developing, hedging and distributing the notes, as described on page TS-13 and various credit, market and economic factors that interrelate in complex and unpredictable ways. |

| § | A trading market is not expected to develop for the notes. MLPF&S is not obligated to make a market for, or to repurchase, the notes. |

| § | Our business activities as a full service financial institution, including our commercial and investment banking activities, our hedging and trading activities (including trades in components included in the Index) and any hedging and trading activities we engage in for our clients’ accounts, may affect the market value and return of the notes and may create conflicts of interest with you. |

| § | Ownership of the notes will not entitle you to any rights with respect to the commodities or futures contracts included in, or tracked by, the Index. |

| § | The notes will not be regulated by the U.S. Commodity Futures Trading Commission. |

| § | The Index includes futures contracts traded on foreign exchanges that may be less regulated than U.S. markets. |

| § | Suspensions or disruptions of market trading in the commodities or futures contracts included in, or tracked by, the Index may adversely affect the value of the notes. |

| § | There may be potential conflicts of interest involving the calculation agent. We have the right to appoint and remove the calculation agent. |

| § | The U.S. federal income tax consequences of the notes are uncertain, and may be adverse to a holder of the notes. See “Summary Tax Consequences” below and “U.S. Federal Income Tax Summary” beginning on page S-45 of product supplement ARN-4. |

| Accelerated Return Notes® | TS-5 |

| Accelerated Return Notes® Linked to the Merrill Lynch Commodity index eXtraSM A06 Index - Excess Return, due August , 2013 |

|

Additional Risk Factors

There is no assurance that the methodology of the Index will result in the Index accurately reflecting commodity market performance.

The methodology and criteria used to determine the composition of the Index, the weights of the Index Components, and the calculation of the level of the Index are designed to enable the Index to serve as a measure of the performance of the commodity market. However, the Index has only recently been introduced and has a limited history. It is possible that the methodology and criteria of the Index will not accurately reflect the performance of the commodity market and that the trading of or investments in products based on or related to the Index, such as the notes, will not correlate with that performance.

The Index tracks commodity futures contracts and does not track the spot prices of the Index Commodities.

The Index is composed of exchange-traded futures contracts (the “Index Components”) on physical commodities (the “Index Commodities”). Unlike equities, which typically entitle the holder to a continuing stake in a corporation, a commodity futures contract is typically an agreement to buy a set amount of an underlying physical commodity at a predetermined price during a stated delivery period. A futures contract reflects the expected value of the underlying physical commodity upon delivery in the future. In contrast, the underlying physical commodity’s current or “spot” price reflects the immediate delivery value of the commodity.

The notes are linked to the Index and not to the spot prices of the Index Commodities. An investment in the notes is not the same as buying and holding the Index Commodities. While price movements in the Index Components may correlate with changes in the spot prices of the Index Commodities, the correlation will not be perfect and price movements in the spot markets for the Index Commodities may not be reflected in the futures market (and vice versa). Accordingly, an increase in the spot prices of the Index Commodities may not result in an increase in the prices of the Index Components or the level of the Index. The Index Component prices and the level of the Index may decrease while the spot prices for the Index Commodities remain stable or increase, or do not decrease to the same extent.

Higher future prices of the Index Components relative to their current prices may have a negative effect on the level of the Index, and therefore the value of the notes.

Commodity indices generally reflect movements in commodity prices by measuring the value of futures contracts for the applicable commodities. To maintain the Index, as futures contracts approach expiration, they are replaced by similar contracts that have a later expiration. This process is referred to as “rolling.” The level of the Index is calculated as if the expiring futures contracts are sold and the proceeds from those sales are used to purchase longer-dated futures contracts. The difference in the price between the contracts that are sold and the new contracts for more distant delivery that are purchased is called “roll yield.”

If the expiring futures contract included in the Index is “rolled” into a less expensive futures contract with a more distant delivery date, the market for that futures contract is trading in “backwardation.” In this case, the effect of the roll yield on the level of the Index will be positive because it costs less to replace the expiring futures contract. However, if the expiring futures contract included in the Index is “rolled” into a more expensive futures contract with a more distant delivery date, the market for that futures contract is trading in “contango.” In this case, the effect of the roll yield on the level of the Index will be negative because it will cost more to replace the expiring futures contract.

There is no indication that the markets for the Index Components will consistently be in backwardation or that there will be a positive roll yield that increases the level of the Index. If all other factors remain constant, the presence of contango in the market for an Index Component could result in negative roll yield, which could decrease the level of the Index and the value of the notes.

The value of the Index Components may change unpredictably, affecting the value of the notes in unforeseeable ways.

Trading in commodities and related futures contracts may be speculative and can be extremely volatile. The value of the Index Components may fluctuate rapidly based on numerous factors, including: changes in supply and demand relationships; weather; agriculture; trade; fiscal, monetary, and exchange control programs; domestic and foreign political and economic events and policies; disease; technological developments; and changes in interest rates. The same factors may cause the value of the Index Components to move in different directions at different rates. These factors may affect the level of the Index and the value of the notes in varying ways.

Changes in the methodology for determining the composition and calculation of the Index or changes in laws or regulations may affect the value of the notes.

Merrill Lynch Commodities, Inc. (the “Index Manager”), which is one of our subsidiaries, retains the discretion to modify the methodology for determining the composition and calculation of the level of the Index at any time. The Index Manager reserves the right to modify the methodology and calculation of the Index from time to time if it believes that modifications are necessary or appropriate. It is possible that certain of these modifications will adversely affect the level of the Index. This may decrease the market value of the notes and the Redemption Amount.

In addition, the values of the Index Components or Index Commodities could be adversely affected by the promulgation of new laws or regulations or by the reinterpretation of existing laws or regulations (including, without limitation, those relating to taxes and duties on commodities or commodity components) by one or more governments, governmental agencies, courts, or other official bodies. Any event of this kind could adversely affect the level of the Index and, as a result, could adversely affect the value of the notes.

| Accelerated Return Notes® | TS-6 |

| Accelerated Return Notes® Linked to the Merrill Lynch Commodity index eXtraSM A06 Index - Excess Return, due August , 2013 |

|

The notes are linked to the Merrill Lynch Commodity index eXtraSM A06 Index—Excess Return (Bloomberg symbol “MLCXA06E”), not the Merrill Lynch Commodity index eXtraSM A06 Index—Total Return (Bloomberg symbol “MLCXA06T”).

The notes are linked to the Merrill Lynch Commodity index eXtraSM A06 Index—Excess Return (Bloomberg symbol “MLCXA06E”), which we refer to in this term sheet as the “Index”. The Index reflects both price movements as well as roll yields. By comparison, the Merrill Lynch Commodity index eXtraSM A06 Index—Total Return includes commodity price movements, a roll-return component, and a U.S. Treasury-bill return component to measure fully collateralized commodity futures investment. Because the notes are linked to the Index and not the Merrill Lynch Commodity index eXtraSM A06 Index—Total Return, the Redemption Amount will not reflect the total return feature.

Additional conflicts of interest may exist.

One of our subsidiaries, Merrill Lynch, Pierce, Fenner & Smith Limited, is the Index Publisher, and another of our subsidiaries, Merrill Lynch Commodities, Inc., is the Index Manager. In certain circumstances, the Index Publisher’s and the Index Manager’s roles as our subsidiaries and their responsibilities with respect to the Index could give rise to conflicts of interest. Even though the Index will be calculated in accordance with certain principles, its calculation and maintenance require that certain judgments and decisions be made. The Index Publisher and the Index Manager will be responsible for these judgments and decisions. As a result, the determinations made by the Index Publisher and/or the Index Manager could adversely affect the level of the Index and, accordingly, decrease the Redemption Amount. In making any determination with respect to the Index, neither the Index Publisher nor the Index Manager is required to consider your interests as a holder of the notes.

Further, Merrill Lynch Commodities, Inc. faces a potential conflict of interest between its role as the Index Manager and its active role in trading commodities and derivatives instruments based upon the Index Components.

The Index has limited actual historical information.

The Index was created in April 2010. The Index Manager has published limited actual information about how the Index would have performed had it been calculated in the past. Because the Index is of recent origin and limited actual historical performance data exists with respect to it, your investment in the notes may involve a greater risk than investing in securities linked to one or more indices with a more established record of performance.

| Accelerated Return Notes® | TS-7 |

| Accelerated Return Notes® Linked to the Merrill Lynch Commodity index eXtraSM A06 Index - Excess Return, due August , 2013 |

|

The Index

All disclosures contained in this term sheet regarding the Index, including, without limitation, its make up, method of calculation, and changes in its components, have been derived from publicly available sources or from information made available to us by the Index Manager or the Index Publisher. The information reflects the policies of, and is subject to change by, the Index Manager and the Index Publisher. The Index Manager and the Index Publisher have no obligation to continue to publish, and may discontinue publication of, the Index. The consequences of the Index Manager and the Index Publisher discontinuing publication of the Index are discussed in the section of product supplement ARN-4 beginning on page S-38 entitled “Description of ARNs — Discontinuance of a Market Measure. None of us, the calculation agent, or MLPF&S accepts any responsibility for the calculation, maintenance, or publication of the Index or any successor index.

The Index (Bloomberg symbol “MLCXA06E”) was launched in April 2010, and is a modified version of the Merrill Lynch Commodity index eXtra (the “MLCX”), as further described below. The Index differs from the MLCX in that it uses a different roll schedule, consists of a different set of commodities, and has different weightings for each of the six Market Sectors (as defined below) and does not use as an exchange the New York Board of Trade Division (NYBOT). The target weightings for the commodities included in the Index are set in January of each year, and the weightings of the commodities are rebalanced monthly based on the price of futures contracts for the commodity on the first business day preceding the start of the roll period for that month. The nineteen commodities, with their respective approximate percentage weights (rounded to two decimal places), as of June 19, 2012, are listed below:

| Market Sector |

Commodity |

Weight |

Exchange/Trading Facility | |||

| Energy |

Crude Oil (WTI) | 8.52% | New York Mercantile Exchange (NYMEX) | |||

| Natural Gas | 9.45% | New York Mercantile Exchange (NYMEX) | ||||

| Gasoline | 3.20% | New York Mercantile Exchange (NYMEX) | ||||

| Heating Oil | 3.15% | New York Mercantile Exchange (NYMEX) | ||||

| Brent | 4.81% | New York Mercantile Exchange (NYMEX) | ||||

| Grains & Oil Seeds |

Soybean | 9.18% | Chicago Board of Trade (CBOT) | |||

| Corn | 6.79% | Chicago Board of Trade (CBOT) | ||||

| Wheat | 5.63% | Chicago Board of Trade (CBOT) | ||||

| Soybean Oil | 3.53% | Chicago Board of Trade (CBOT) | ||||

| Base Metals |

Copper | 7.53% | London Metals Exchange (LME) | |||

| Aluminum | 5.77% | London Metals Exchange (LME) | ||||

| Zinc | 3.39% | London Metals Exchange (LME) | ||||

| Nickel | 2.49% | London Metals Exchange (LME) | ||||

| Soft Commodities & Others |

Sugar | 3.42% | ICE Futures (ICE) | |||

| Coffee | 1.96% | ICE Futures (ICE) | ||||

| Cotton | 1.70% | ICE Futures (ICE) | ||||

| Precious Metals |

Gold | 10.42% | New York Mercantile Exchange (COMEX) | |||

| Silver | 2.91% | New York Mercantile Exchange (COMEX) | ||||

| Livestock |

Live Cattle | 3.77% | Chicago Mercantile Exchange (CME) | |||

| Lean Hogs | 2.38% | Chicago Mercantile Exchange (CME) |

| Accelerated Return Notes® | TS-8 |

| Accelerated Return Notes® Linked to the Merrill Lynch Commodity index eXtraSM A06 Index - Excess Return, due August , 2013 |

|

The Index Roll Mechanism

The following table sets forth the futures contracts constituting the Index held during each month of the year, and their corresponding delivery months. The letters designating the delivery month for each contract held at the start of that month are set forth below. For example, based on the table below, a gold contract held in April would specify a delivery date in August of the same year, while a sugar contract held in August would specify a delivery date in May of the following year.

During the first 15 business days of each month, certain contracts constituting the Index are rolled from the contract then held at the start of the month to a contract with a future delivery month. There may be no roll for a given contract for a given month. For example, a wheat futures contract included in the Index at the beginning of January would have a delivery date in July of the same year, and a nickel contract included in the Index at the beginning of January would have a delivery date in April of the same year. There would be no roll of the wheat contract from January to February, while the nickel contract would be rolled during a 15-business day period in January from a contract with a delivery date in April to a contract with a delivery date in May of the same year.

| Contract |

Jan |

Feb |

Mar |

Apr |

May |

Jun |

Jul |

Aug |

Sep |

Oct |

Nov |

Dec | ||||||||||||

| Crude Oil (WTI) |

J | K | M | N | Q | U | V | X | Z | F+ | G+ | H+ | ||||||||||||

| Heating Oil |

J | K | M | N | Q | U | V | X | Z | F+ | G+ | H+ | ||||||||||||

| Wheat |

N | N | U | U | Z | Z | H+ | H+ | H+ | K+ | K+ | K+ | ||||||||||||

| Corn |

N | N | U | U | Z | Z | H+ | H+ | H+ | K+ | K+ | K+ | ||||||||||||

| Aluminum |

J | K | M | N | Q | U | V | X | Z | F+ | G+ | H+ | ||||||||||||

| Gold |

J | M | M | Q | Q | Z | Z | Z | Z | G+ | G+ | J+ | ||||||||||||

| Natural Gas |

J | K | M | N | Q | U | V | X | Z | F+ | G+ | H+ | ||||||||||||

| Live Cattle |

M | Q | Q | V | V | Z | Z | G+ | G+ | J+ | J+ | M+ | ||||||||||||

| Soybean |

N | N | X | X | F+ | F+ | F+ | F+ | H+ | H+ | K+ | K+ | ||||||||||||

| Coffee |

N | N | U | U | Z | Z | H+ | H+ | H+ | K+ | K+ | K+ | ||||||||||||

| Nickel |

J | K | M | N | Q | U | V | X | Z | F+ | G+ | H+ | ||||||||||||

| Zinc |

J | K | M | N | Q | U | V | X | Z | F+ | G+ | H+ | ||||||||||||

| Sugar |

N | N | V | V | H+ | H+ | H+ | K+ | K+ | K+ | K+ | K+ | ||||||||||||

| Silver |

K | K | N | N | U | U | Z | Z | Z | H+ | H+ | H+ | ||||||||||||

| Gasoline (RBOB) |

J | K | M | N | Q | U | V | X | Z | F+ | G+ | H+ | ||||||||||||

| Lean Hogs |

M | N | N | Q | V | Z | Z | G+ | G+ | J+ | J+ | M+ | ||||||||||||

| Soybean Oil |

N | N | Q | Q | U | Z | F+ | F+ | F+ | H+ | K+ | K+ | ||||||||||||

| Cotton |

K | N | N | Z | Z | Z | H+ | H+ | H+ | H+ | K+ | K+ | ||||||||||||

| Copper (LME) |

J | K | M | N | Q | U | V | X | Z | F+ | G+ | H+ | ||||||||||||

| Brent |

K | M | N | Q | U | V | X | Z | F+ | G+ | H+ | J+ |

Month Letter Code: January F, February G, March H, April J, May K, June M, July N, August Q, September U, October V, November X, and December Z. A “+” following the contract indicates a contract of the following year.

The Index is calculated by the Index Publisher based on the official settlement or similar prices for the applicable contracts. The Index Manager applies the daily percentage change in the prices of the futures contracts included in the Index to the prior trading day’s level of the Index in order to calculate the current level of the Index. The Index is calculated in the manner described in the MLCX Handbook, which is available at http://gmi.ml.com/mlcx/downloads/MLCX_Handbook.pdf, as modified to reflect the commodities and weightings that the Index measures. The MLCX Handbook is not part of, and is not incorporated by reference in, this term sheet.

“Merrill Lynch Commodity index eXtraSM” is a registered service mark and trademark of our subsidiary, Merrill Lynch & Co., Inc.

The MLCX

The MLCX was created by the Index Manager and the Index Publisher in 2006 and is designed to provide a benchmark for the performance of the commodity market and for investment in commodities as an asset class. The MLCX is comprised of futures contracts on physical commodities. As the exchange traded futures contracts that comprise the MLCX approach the month before expiration, they are replaced by contracts that have later expiration dates. This process is referred to as “rolling.” The MLCX rolls over a 15-index business day period each month.

The Index Manager constructed the MLCX based primarily on the liquidity of the futures contracts that comprise the MLCX and the value of the global production of each related commodity. The Index Manager believes that these criteria allow the MLCX to reflect the general significance of the commodities (the “MLCX Commodities”) in the global economy, differentiating between “upstream” and “downstream” commodities, with a particular emphasis on downstream commodities (i.e., those that are derived from other commodities represented by the MLCX). The MLCX composition and weights are typically determined once a year and applied once at the start of

| Accelerated Return Notes® | TS-9 |

| Accelerated Return Notes® Linked to the Merrill Lynch Commodity index eXtraSM A06 Index - Excess Return, due August , 2013 |

|

each year in January. The methodology for determining the composition, weighting, or value of the MLCX and for calculating its level is subject to modification by the Index Manager and the Index Publisher, respectively, at any time. The Index Manager reserves the right to modify the methodology and calculation of the MLCX from time to time, if it believes that modifications are necessary or appropriate.

Construction

The MLCX was created using the following four main principles:

1. Liquidity – The futures contracts included in the MLCX should be sufficiently liquid to accommodate the level of trading needed to support the MLCX. The selection mechanism is therefore based primarily on liquidity.

2. Weighting – The weight of each futures contract in the MLCX should reflect the value of the global production of the related commodity, as a measure of the significance of the commodity in the global economy, with appropriate adjustments to avoid “double counting.”

3. Market Sectors – Each Market Sector should be adequately represented in the MLCX and the weights should be adjusted to maintain the integrity of the Market Sectors.

4. Rolling – Futures contracts that comprise the MLCX are rolled during a fifteen day period to limit the market impact that such contract rolls could have.

The MLCX contains six market sectors identified by the Index Manager: (1) energy; (2) base metals; (3) precious metals; (4) grains & oil seeds; (5) livestock; and (6) soft commodities & others (each a “Market Sector”). Each Market Sector is represented in the MLCX by a minimum of two and a maximum of four futures contracts, selected based on liquidity.

Exchange Selection

The Index Manager has selected a set of exchanges, on the basis of liquidity, geographical location, and commodity type (the “Selected Exchanges”), from which the contracts included in the MLCX will be selected. To be considered for selection, an exchange must be located in a country that is a member of the Organization for Economic Co-Operation and Development. The exchange must also be a principal trading forum, based on relative liquidity, for U.S. dollar-denominated futures contracts on major physical commodities. The four exchanges currently are: (1) the New York Mercantile Exchange (the “NYMEX”) (NYMEX and COMEX Divisions); (2) the Chicago Mercantile Exchange (the “CME”) (CME and Chicago Board of Trade (CBOT) Divisions); (3) the London Metals Exchange (the “LME”); and (4) the ICE Futures exchange (the “ICE”) (ICE and New York Board of trade (NYBOT) Divisions).

Contract Selection

Eligibility

To be an “Eligible Contract,” a commodity futures contract must satisfy all of the following requirements:

| § | it must be denominated in U.S. dollars; |

| § | it must be based on a physical commodity (or the price of a physical commodity) and provide for cash settlement or physical delivery at a specified time, or during a specified period, in the future; |

| § | detailed trading volume data regarding the contract must be available for at least two years prior to the initial inclusion of the contract in the MLCX, provided that the Index Manager may determine to include a contract with less than two years of data; |

| § | the contract must have a Total Trading Volume, or TTV (as defined below), of at least 500,000 contracts for each twelve-month period beginning on July 1 and ending on June 30; and |

| § | Reference Prices must be publicly available on a daily basis either directly from the Selected Exchange or, if available through an external data vendor, on any day on which the relevant exchange is open for business. “Reference Prices” are the official settlement or similar prices posted by the relevant Selected Exchange (or its clearinghouse) with respect to a contract and against which positions in such contract are margined or settled. |

An Eligible Contract is selected for inclusion in the MLCX only after application of the requirements for a minimum and maximum number of contracts from each Market Sector. A contract that does not otherwise satisfy all of the foregoing requirements may nevertheless be included in the MLCX if the inclusion of the contract is, in the judgment of the Index Manager, necessary or appropriate to maintain the integrity of the MLCX and/or to realize the objectives of the MLCX. Every year, the Index Manager compiles a list of all commodity futures contracts traded on the Selected Exchanges and a list of the Eligible Contracts that satisfy the foregoing criteria. This list will be used to determine the commodities futures contracts which will be included in the MLCX.

Liquidity

The Index Manager distinguishes the Eligible Contracts by their liquidity. Liquidity is measured by a contract’s “Total Trading Volume” (“TTV”) and the value of that trading volume. The “Total Trading Volume” with respect to each contract traded on a Selected Exchange is equal to the sum of the daily trading volumes in all expiration months of the contract on each day during the most recent twelve-month period beginning on July 1 and ending on June 30. The “Contract Size” (“CS”) is the number of standard physical units of the underlying commodity represented by one contract. For example, the Contract Size of a crude oil futures contract is 1,000 barrels. The “Average Reference Price” (“ARP”), which is used to determine the value of the Total Trading Volume, is the average of the Reference Prices of the Front-Month Contract (as defined below) for an MLCX contract on each Trading Day (as defined below) during the twelve-month

| Accelerated Return Notes® | TS-10 |

| Accelerated Return Notes® Linked to the Merrill Lynch Commodity index eXtraSM A06 Index - Excess Return, due August , 2013 |

|

period beginning on July 1 and ending on June 30 of each year. A “Front-Month Contract” on any given day is the futures contract expiring on the first available contract expiration month after the date on which the determination is made. A “Trading Day” means any day on which the relevant Selected Exchange is open for trading. “Liquidity” (“LIQ”) is therefore equal to the Total Trading Volume, multiplied by the Contract Size with respect to each contract, multiplied by the Average Reference Price for that contract: LIQ = TTV × CS × ARP.

Once the LIQ is determined, the Eligible Contracts are listed in order of their LIQ, from highest to lowest. Each MLCX Market Sector must be represented by a minimum of two and a maximum of four Eligible Contracts. The MLCX will only include the Eligible Contracts with the greater LIQs. The “Redundant Contracts,” which are less liquid Eligible Contracts representing the same MLCX commodity, are excluded. For instance, the list of futures contracts that comprise the MLCX includes an Eligible Contract on WTI crude oil but excludes a contract on Brent crude oil as a Redundant Contract.

The selection of Eligible Contracts and determination of the futures contracts that comprise the MLCX occur once a year. The results for the following calendar year will be announced before the first NYMEX Business Day (as defined below) of November. “NYMEX Business Day” is any day that the NYMEX rules define as a trading day.

Based on this selection process, the MLCX may include from 12 to 22 commodity futures contracts.

Weighting

The Index Manager determines the weight of each contract on the basis of the global production value of the related commodity, provided that the contract reflects global prices for that commodity. In some cases, however, the futures contracts that comprise the MLCX only have pricing links to a limited number of markets around the world. For instance, the NYMEX natural gas contract primarily represents the U.S. market and the surrounding North American markets in Canada and Mexico. In addition, some European gas markets, such as the U.K., are developing an increasing link to U.S. natural gas prices through the liquefied natural gas market. As a result, rather than using production of natural gas in the world or in the U.S. to assign a weight to the natural gas contract in the MLCX, the Index Manager has aggregated U.S., Canadian, Mexican, and U.K. natural gas production. Similarly, the Index Manager found that U.S. livestock prices can be affected by local issues such as disease and trade restrictions, so it limited the livestock component of the MLCX to production of cattle and hogs in the United States, instead of using global production weights. Also, certain commodities are derived from other commodities in various forms. For example, gasoline and heating oil are produced from crude oil, and, because livestock feed on corn and other grains, they are to an extent derived from agricultural commodities. To avoid “double counting” of commodities such as crude oil or grains used as livestock feed, the Index Manager differentiates between “upstream” and “downstream” commodities and adjusts the global production quantity of the MLCX Commodities accordingly.

Rolling

Each MLCX contract is rolled into the next available contract month in advance of the month in which expiration of the contract occurs. The rolling process takes place over a 15-day period during each month prior to the relevant expiration month of each contract. The rolling process is spread out to limit the effect it might have on the market through the purchase and sale of contracts by investors who might attempt to replicate the performance of the MLCX. The rolling of contracts is effected on the same days for all MLCX contracts, regardless of exchange holiday schedules, emergency closures, or other events that could prevent trading in such contracts, although the Index Manager reserves the right to delay the rolling of a particular contract under extraordinary circumstances. If an MLCX contract is rolled on a day on which the relevant contract is not available for trading, the roll will be effected on the basis of the most recent available settlement price.

Market Sectors

The weight of any given Market Sector in the MLCX is capped at 60% of the overall MLCX. A minimum weight of 3% is applicable to each Market Sector. Although the MLCX is designed to reflect the significance of the underlying commodities in the global economy, each Market Sector maintains these limits in an attempt to control volatility.

The weights of the Market Sectors for 2012, as of February 2012, were:

| Market Sector |

Weight | |||

| Energy |

60.0 | % | ||

| Grains & Oil Seeds |

15.8 | % | ||

| Base Metals |

10.3 | % | ||

| Soft Commodities & Others |

6.7 | % | ||

| Precious Metals |

4.2 | % | ||

| Livestock |

3.0 | % | ||

MLCX Oversight

The Merrill Lynch Commodity Index Advisory Committee (the “Advisory Committee”), comprised of individuals internal and external to Merrill Lynch, assists the Index Manager and the Index Publisher in connection with the application of the MLCX principles, advises the Index Manager and the Index Publisher on the administration and operation of the MLCX, and makes recommendations to the Index Manager and the Index Publisher as to any modifications to the MLCX methodology that may be necessary or appropriate. The

| Accelerated Return Notes® | TS-11 |

| Accelerated Return Notes® Linked to the Merrill Lynch Commodity index eXtraSM A06 Index - Excess Return, due August , 2013 |

|

Advisory Committee meets once a year and may meet more often at the request of the Index Manager and the Index Publisher. The Advisory Committee advises the Index Manager and the Index Publisher with respect to the inclusion or exclusion of any of the exchanges and contracts in the MLCX, any changes to the composition of the MLCX or in the weights of the futures contracts that comprise the MLCX, and any changes to the calculation procedures applicable to the MLCX. The Advisory Committee acts solely in an advisory and consulting capacity. All decisions relating to the composition, weighting or value of the MLCX are made by the Index Manager and the Index Publisher. The Index Manager and the Index Publisher expect that, to the extent any changes are made as to the MLCX, corresponding changes will be made to the Index.

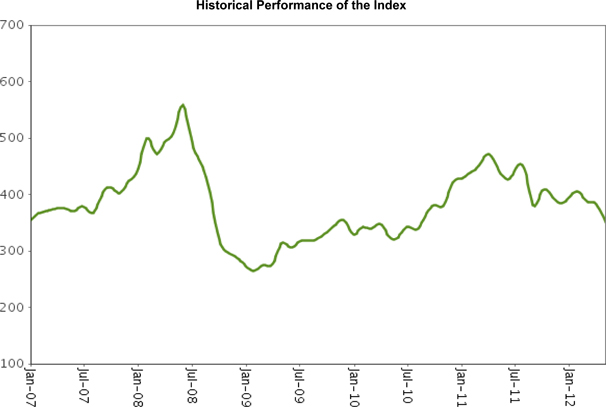

The Index was launched in April 2010 and, accordingly, there is no actual historical data on the Index prior to April 2010. The following graph sets forth the hypothetical monthly historical performance of the Index in the period from January 2006 to April 2010 and the actual monthly historical performance of the Index in the period from April 2010 through May 2012. The hypothetical historical information has been prepared based on certain assumptions, including the pro-forma composition of the Index and the weights of the Index Components, and has otherwise been produced according to the current MLCX methodology described above. There can therefore be no assurance that the hypothetical historical information accurately reflects the performance of the Index had the Index been actually published and calculated during the relevant period. We obtained historical data from Bloomberg L.P. We have not independently verified the accuracy or completeness of the information obtained from Bloomberg L.P. On June 19, 2012, the closing level of the Index was 357.044.

This historical data on the Index is not necessarily indicative of the future performance of the Index or what the value of the notes may be. Any historical upward or downward trend in the level of the Index during any period set forth above is not an indication that the level of the Index is more or less likely to increase or decrease at any time over the term of the notes.

Before investing in the notes, you should consult publicly available sources for the levels and trading pattern of the Index.

| Accelerated Return Notes® | TS-12 |

| Accelerated Return Notes® Linked to the Merrill Lynch Commodity index eXtraSM A06 Index - Excess Return, due August , 2013 |

|

Supplement to the Plan of Distribution

We may deliver the notes against payment therefor in New York, New York on a date that is greater than three business days following the pricing date. Under Rule 15c6-1 of the Securities Exchange Act of 1934, trades in the secondary market generally are required to settle in three business days, unless the parties to any such trade expressly agree otherwise. Accordingly, if the initial settlement of the notes occurs more than three business days from the pricing date, purchasers who wish to trade the notes more than three business days prior to the original issue date will be required to specify alternative settlement arrangements to prevent a failed settlement.

The notes will not be listed on any securities exchange. In the original offering of the notes, the notes will be sold in minimum investment amounts of 100 units.

MLPF&S will not receive an underwriting discount for notes sold to certain fee-based trusts and fee-based discretionary accounts managed by U.S. Trust operating through Bank of America, N.A.

If you place an order to purchase the notes, you are consenting to MLPF&S acting as a principal in effecting the transaction for your account.

MLPF&S may repurchase and resell the notes, with repurchases and resales being made at prices related to then-prevailing market prices or at negotiated prices. MLPF&S may act as principal or agent in these market-making transactions; however it is not obligated to engage in any such transactions.

Role of MLPF&S and Conflicts of Interest

MLPF&S, a broker-dealer subsidiary of BAC, is a member of the Financial Industry Regulatory Authority, Inc. (“FINRA”) and will participate as selling agent in the distribution of the notes. Accordingly, offerings of the notes will conform to the requirements of Rule 5121 applicable to FINRA members. MLPF&S may not make sales in this offering to any of its discretionary accounts without the prior written approval of the account holder.

Under our distribution agreement with MLPF&S, MLPF&S will purchase the notes from us as principal at the public offering price indicated on the cover of this term sheet, less the indicated underwriting discount. The public offering price includes, in addition to the underwriting discount, a charge of approximately $0.075 per unit, reflecting an estimated profit earned by MLPF&S from transactions through which the notes are structured and resulting obligations hedged. Actual profits or losses from these hedging transactions may be more or less than this amount. In entering into the hedging arrangements for the notes, we seek competitive terms and may enter into hedging transactions with MLPF&S or another of our affiliates.

All charges related to the notes, including the underwriting discount and the hedging related costs and charges, reduce the economic terms of the notes. For further information regarding these charges, our trading and hedging activities and conflicts of interest, see “Risk Factors—General Risks Relating to ARNs” beginning on page S-10 and “Use of Proceeds” on page S-22 of product supplement ARN-4.

| Accelerated Return Notes® | TS-13 |

| Accelerated Return Notes® Linked to the Merrill Lynch Commodity index eXtraSM A06 Index - Excess Return, due August , 2013 |

|

Summary Tax Consequences

You should consider the U.S. federal income tax consequences of an investment in the notes, including the following:

| • | There is no statutory, judicial, or administrative authority directly addressing the characterization of the notes. |

| • | You agree with us (in the absence of an administrative determination, or judicial ruling to the contrary) to characterize and treat the notes for all tax purposes as a single financial contract with respect to the Index. |

| • | Under this characterization and tax treatment of the notes, a U.S. Holder (as defined on page 62 of the prospectus) generally will recognize capital gain or loss upon maturity or upon a sale or exchange of the notes prior to maturity. This capital gain or loss generally will be long-term capital gain or loss if you held the notes for more than one year. |

| • | No assurance can be given that the IRS or any court will agree with this characterization and tax treatment. |

You should consult your own tax advisor concerning the U.S. federal income tax consequences to you of acquiring, owning, and disposing of the notes, as well as any tax consequences arising under the laws of any state, local, foreign, or other tax jurisdiction and the possible effects of changes in U.S. federal or other tax laws. You should review carefully the discussion under the section entitled “U.S. Federal Income Tax Summary” beginning on page S-45 of product supplement ARN-4.

Where You Can Find More Information

We have filed a registration statement (including a product supplement, a prospectus supplement, and a prospectus) with the SEC for the offering to which this term sheet relates. Before you invest, you should read the Note Prospectus, including this term sheet, and the other documents that we have filed with the SEC, for more complete information about us and this offering. You may get these documents without cost by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, we, any agent, or any dealer participating in this offering will arrange to send you these documents if you so request by calling MLPF&S toll-free at 1-866-500-5408.

Market-Linked Investments Classification

MLPF&S classifies certain market-linked investments (the “Market-Linked Investments”) into categories, each with different investment characteristics. The following description is meant solely for informational purposes and is not intended to represent any particular Enhanced Return Market-Linked Investment or guarantee any performance.

Enhanced Return Market-Linked Investments are short- to medium-term investments that offer you a way to enhance exposure to a particular market view without taking on a similarly enhanced level of market downside risk. They can be especially effective in a flat to moderately positive market (or, in the case of bearish investments, a flat to moderately negative market). In exchange for the potential to receive better-than market returns on the linked asset, you must generally accept market downside risk and capped upside potential. As these investments are not market downside protected, and do not assure full repayment of principal at maturity, you need to be prepared for the possibility that you may lose all or part of your investment.

“Accelerated Return Notes®” and “ARNs®” are our registered service marks.

| Accelerated Return Notes® | TS-14 |