Filed Pursuant to Rule 424(b)(5)

Registration Statement No. 333-268718 and

333-268718-01

Product Supplement No. STOCK LIRN-1

March 20, 2025

BofA Finance LLC

Leveraged Index Return Notes® “LIRNs®” Linked to One or More Equity Securities

Fully and Unconditionally Guaranteed by Bank of America Corporation

| • | The LIRNs are unsecured senior notes issued by BofA Finance LLC, a consolidated finance subsidiary of Bank of America Corporation (the “Guarantor”). Any payment due on the LIRNs is fully and unconditionally guaranteed by the Guarantor. Any payments due on the LIRNs, including any repayment of principal, will be subject to the credit risk of BofA Finance LLC, as issuer of the LIRNs, and the credit risk of Bank of America Corporation, as guarantor of the LIRNs. |

| • | The LIRNs do not guarantee the return of principal at maturity, and we will not pay interest on the LIRNs. Instead, the return on the LIRNs will be based on the performance of an underlying “Market Measure,” which will be either the common equity securities or American Depositary Receipts (“ADRs”) of a company other than us and our affiliates (the “Underlying Stock”). The Market Measure may also consist of a “Basket” of two or more Underlying Stocks. |

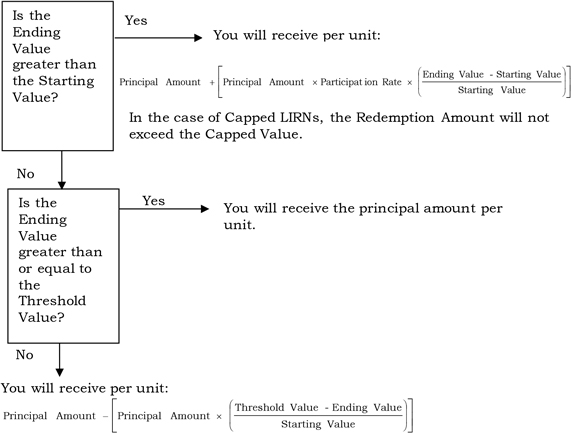

| • | The LIRNs provide an opportunity to earn a multiple of the positive performance of the Market Measure, and may provide limited protection against the risk of losses. You will be exposed to any negative performance of the Market Measure below the Threshold Value (as defined in “Summary” below) on a 1-to-1 basis. If specified in the applicable term sheet, your LIRNs may be “Capped LIRNs.” In the case of Capped LIRNs, the amount payable at maturity will not exceed a specified cap (the “Capped Value”). Additionally, if specified in in the applicable term sheet, your LIRNs may be subject to an automatic call, which will limit your return to a fixed amount if the LIRNs are called. |

| • | If the LIRNs are not automatically called prior to maturity, if applicable, and the value of the Market Measure increases from its Starting Value to its Ending Value (each as defined in “Summary” below), you will receive at maturity a cash payment per unit (the “Redemption Amount”) that equals the principal amount of your LIRNs plus a multiple of that increase, and in the case of Capped LIRNs, up to the Capped Value. If the LIRNs are not automatically called prior to maturity, if applicable, and the value of the Market Measure does not change or decreases from its Starting Value to its Ending Value but not below the Threshold Value, then unless otherwise provided in the applicable term sheet the Redemption Amount will equal the principal amount. However, if the Ending Value is less than the Threshold Value, you will be subject to 1-to-1 downside exposure to the decrease of the Market Measure below the Threshold Value. In such a case, you may lose all or a significant portion of the principal amount of your LIRNs. |

| • | If specified in the applicable term sheet, your LIRNs may be subject to an automatic call. In that case, the LIRNs will be automatically called if the Observation Level on any Observation Date is greater than or equal to the Call Level (each as defined in “Summary” below). If called, you will receive a cash payment per unit that equals the principal amount plus the applicable Call Premium (as defined in “Summary” below). |

| • | This product supplement describes the general terms of the LIRNs, the risk factors to consider before investing, the general manner in which the LIRNs may be offered and sold, and other relevant information. |

| • | For each offering of the LIRNs, we will provide you with a pricing supplement (which we refer to as a “term sheet”) that will describe the specific terms of that offering, including the specific Market Measure, the Capped Value if applicable, the Threshold Value, the Participation Rate (as defined in “Summary” below) and, if the LIRNs are subject to an automatic call, the Call Level, the Call Amount and the Call Premium for each Observation Date, the Observation Dates and the Call Settlement Dates, and certain risk factors. The applicable term sheet will identify, if applicable, any additions or changes to the terms specified in this product supplement. |

| • | The LIRNs will be issued in denominations of whole units. Unless otherwise set forth in the applicable term sheet, each unit will have a principal amount of $10. The applicable term sheet may also set forth a minimum number of units that you must purchase. |

| • | Unless otherwise specified in the applicable term sheet, the LIRNs will not be listed on a securities exchange or quotation system. |

| • | One or more of our affiliates, including BofA Securities, Inc. (“BofAS”), may act as our selling agents to offer the LIRNs and will act in a principal capacity in such role. |

The LIRNs are unsecured and unsubordinated obligations of BofA Finance LLC and the related guarantee of the LIRNs is an unsecured and unsubordinated obligation of Bank of America Corporation. The LIRNs and the related guarantee are not savings accounts, deposits, or other obligation of a bank. The LIRNs are not guaranteed by Bank of America, N.A. or any other bank, and are not insured by the Federal Deposit Insurance Corporation (the “FDIC”) or any other governmental agency and may involve investment risks, including possible loss of principal. Potential purchasers of the LIRNs should consider the information in “Risk Factors” beginning on page PS-8 of this product supplement, page S-6 of the accompanying Series A MTN prospectus supplement, and page 7 of the accompanying prospectus. You may lose all or a significant portion of your investment in the LIRNs.

None of the Securities and Exchange Commission (the “SEC”), any state securities commission, or any other regulatory body has approved or disapproved of these securities or passed upon the adequacy or accuracy of this product supplement or the accompanying prospectus supplement or prospectus. Any representation to the contrary is a criminal offense.

BofA Securities