BofA Finance LLC

Fully and Unconditionally Guaranteed by Bank of America Corporation

Market Linked Securities

|

BofA Finance LLC

Fully and Unconditionally Guaranteed by Bank of America Corporation

Market Linked Securities

|

|

Summary of Terms

| Issuer: | BofA Finance LLC (“BofA Finance”) |

| Guarantor: | Bank of America Corporation (“BAC” or the “Guarantor”) |

| Term: | Approximately 4 years (unless earlier called) |

| Underlying: | Russell 2000® Index (the “Underlying”) |

| Pricing Date: | October 29, 2021 |

| Issue Date: | November 3, 2021 |

| Denominations: | $1,000 and any integral multiple of $1,000. References in the pricing supplement to a “Security” are to a Security with a principal amount of $1,000. |

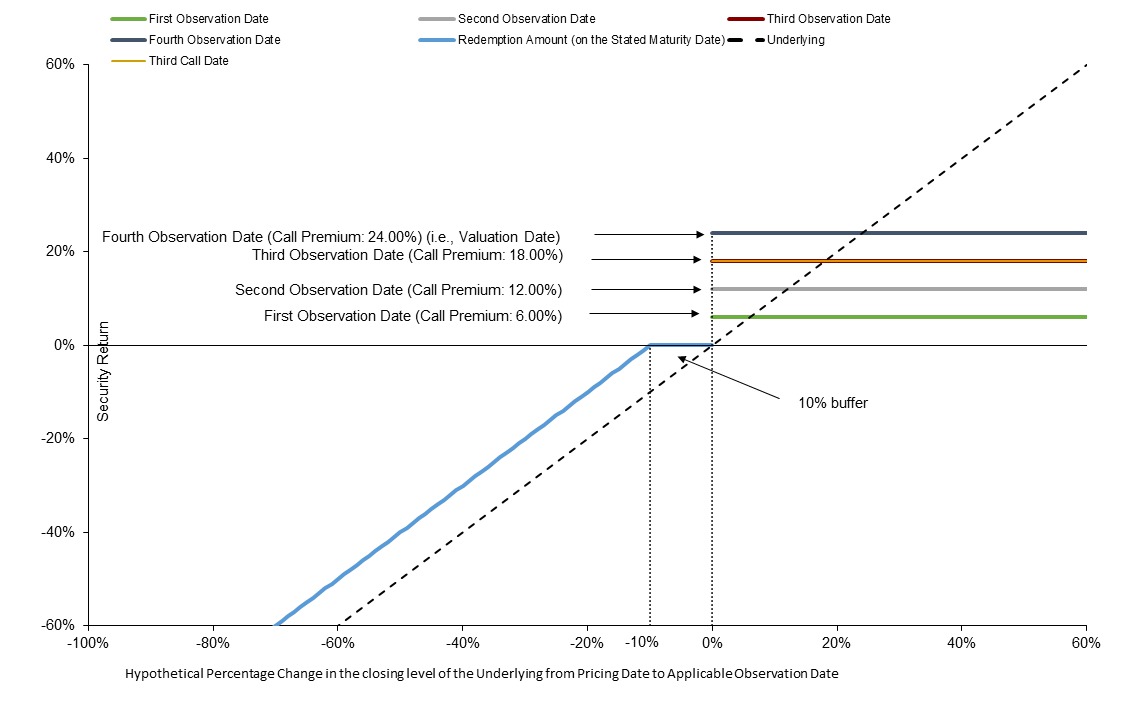

| Automatic Call: | If the closing level of the Underlying on any Observation Date is greater than or equal to the Starting Value, the Securities will be automatically called for the principal amount plus the Call Premium applicable to that Observation Date. See “Observation Dates and Call Premiums” on page 3 |

| Observation Dates: | November 3, 2022; November 3, 2023; November 4, 2024; and October 27, 2025 |

| Call Settlement Date: | Five business days after the applicable Observation Date (if the Securities are called on the last Observation Date, the Call Settlement Date will be the Maturity Date) |

| Redemption Amount: | See “How the Redemption Amount is calculated” on page 3 |

| Maturity Date: | November 3, 2025 |

| Starting Value: | 2,297.191, which is the closing level of the Underlying on the pricing date |

| Ending Value: | The closing level of the Underlying on the Valuation Date |

| Threshold Value: | 2,067.4719, which is 90% of the Starting Value |

| Calculation Agent: | BofA Securities, Inc. (“BofAS”), an affiliate of BofA Finance |

| Underwriting Discount: | 2.825%; dealers, including those using the trade name Wells Fargo Advisors (WFA), may receive a selling concession of 1.75% and WFA will receive a distribution expense fee of 0.075%. In addition, in respect of certain Securities sold in this offering, BofAS or one of its affiliates may pay a fee of up to $1.00 per Security to selected securities dealers in consideration for marketing and other services in connection with the distribution of the Securities to other securities dealers. |

| CUSIP: | 09709USN9 |

Description of Terms

| · | Linked to the Russell 2000® Index |

| · | Unlike ordinary debt Securities, the Securities do not pay interest, do not repay a fixed amount of principal at maturity and are subject to potential automatic call upon the terms described below. Any return you receive on the Securities and whether they are automatically called will depend on the performance of the Underlying |

| · | Automatic Call. If the closing level of the Underlying on any Observation Date is greater than or equal to the Starting Value, the Securities will be automatically called, and on the related Call Settlement Date, you will receive the principal amount plus the Call Premium applicable to that Observation Date. The Call Premium applicable to each Observation Date will be a percentage of the principal amount that increases for each Observation Date based on a simple (non-compounding) return of 6.00% per annum |

| Observation Date | Call Premium |

| November 3, 2022 | 6.00% of the principal amount |

| November 3, 2023 | 12.00% of the principal amount |

| November 4, 2024 | 18.00% of the principal amount |

| October 27, 2025 (the “Valuation Date”) | 24.00% of the principal amount |

| · | Redemption Amount. If the Securities are not automatically called, you will receive a Redemption Amount that could be equal to or less than the principal amount per Security depending on the closing level of the Underlying on the Valuation Date as follows: |

| o | If the level of the Underlying decreases but the decrease is not more than 10%: |

You will receive the principal amount of your Securities at maturity

| o | If the level of the Underlying decreases by more than 10%: |

You will receive less than the principal amount and have 1-to-1 downside exposure to the decrease in the level of the Underlying in excess of 10%

| · | Investors may lose up to 90% of the principal amount |

| · | Any positive return on the Securities will be limited to the applicable Call Premium |

| · | All payments on the Securities are subject to the credit risk of BofA Finance LLC, as issuer, and Bank of America Corporation, as guarantor, and you will have no ability to pursue any securities included in any Underlying for payment; if BofA Finance LLC, as issuer, and Bank of America Corporation, as guarantor, default on their respective obligations, you could lose some or all of your investment |

| · | No exchange listing; designed to be held to maturity |

The initial estimated value of the Securities as of the pricing date is $955.20 per Security, which is less than the public offering price. The actual value of your Securities at any time will reflect many factors and cannot be predicted with accuracy. See “Risk Factors” beginning on page PS-8 of the accompanying pricing supplement and “Structuring the Securities” on page PS-22 of the accompanying pricing supplement for additional information.

The Securities have complex features and investing in the Securities involves risks not associated with an investment in conventional debt securities. Potential purchasers of the Securities should consider the information in “Risk Factors” beginning on page PS-8 of the accompanying pricing supplement, page PS-5 of the accompanying product supplement, page S-5 of the accompanying prospectus supplement, and page 7 of the accompanying prospectus.

This final term sheet should be read in conjunction with the accompanying pricing supplement, product supplement, prospectus supplement and prospectus before making a decision to invest in the Securities.

NOT A BANK DEPOSIT AND NOT INSURED OR GUARANTEED BY THE FDIC OR ANY OTHER GOVERNMENTAL AGENCY

|

Hypothetical Observation Date on which Securities are automatically called

|

Payment per Security on related Call Settlement Date

|

Pre-tax total rate of return

|

|

1st Observation Date

|

$1,060.00

|

6.00%

|

|

2nd Observation Date

|

$1,120.00

|

12.00 %

|

|

3rd Observation Date

|

$1,180.00

|

18.00%

|

|

4th Observation Date

|

$1,240.00

|

24.00%

|

|

Hypothetical Ending Value

|

Hypothetical percentage change from the hypothetical Starting Value to the hypothetical Ending Value

|

Hypothetical Redemption Amount per Security

|

Hypothetical pre-tax total rate of return

|

|

95.00

|

-5.00%

|

$1,000.00

|

0.00%

|

|

90.00

|

-10.00%

|

$1,000.00

|

0.00%

|

|

89.00

|

-11.00%

|

$990.00

|

-1.00%

|

|

80.00

|

-20.00%

|

$900.00

|

-10.00%

|

|

75.00

|

-25.00%

|

$850.00

|

-15.00%

|

|

50.00

|

-50.00%

|

$600.00

|

-40.00%

|

|

25.00

|

-75.00%

|

$350.00

|

-65.00%

|

|

0.00

|

-100.00%

|

$100.00

|

-90.00%

|

|

Observation Date

|

Call Premium

|

Payment per Security upon an Automatic Call

|

|

November 3, 2022

|

6.00% of the principal amount

|

$1,060.00

|

|

November 3, 2023

|

12.00% of the principal amount

|

$1,120.00

|

|

November 4, 2024

|

18.00% of the principal amount

|

$1,180.00

|

|

October 27, 2025 (the “Valuation Date”)

|

24.00% of the principal amount

|

$1,240.00

|

|

●

|

If the Ending Value is less than the Starting Value but greater than or equal to the Threshold Value: $1,000; or

|

|

●

|

If the Ending Value is less than the Threshold Value: $1,000 minus

|

|

●

|

Your investment may result in a loss; there is no guaranteed return of principal.

|

|

●

|

Any positive investment return on the Securities is limited.

|

|

●

|

The Securities do not bear interest.

|

|

●

|

The Call Premium or Redemption Amount, as applicable, will not reflect the levels of the Underlying other than on the Observation Dates.

|

|

●

|

The Securities are subject to a potential Automatic Call, which would limit your ability to receive further payment on the Securities.

|

|

●

|

Your return on the Securities may be less than the yield on a conventional debt security of comparable maturity.

|

|

●

|

Any payment on the Securities is subject to the credit risk of BofA Finance, as issuer, and BAC, as Guarantor, and actual or perceived changes in BofA Finance’s or the Guarantor’s creditworthiness are expected to affect the value of the Securities.

|

|

●

|

We are a finance subsidiary and, as such, have no independent assets, operations or revenues.

|

|

●

|

The public offering price you are paying for the Securities exceeds their initial estimated value.

|

|

●

|

The initial estimated value does not represent a minimum or maximum price at which BofA Finance, BAC, BofAS or any of our other affiliates or WFS or its affiliates would be willing to purchase your Securities in any secondary market (if any exists) at any time.

|

|

●

|

BofA Finance cannot assure you that a trading market for your Securities will ever develop or be maintained.

|

|

●

|

The Securities are not designed to be short-term trading instruments, and if you attempt to sell the Securities prior to maturity, their market value, if any, will be affected by various factors that interrelate in complex ways, and their market value may be less than the principal amount.

|

|

●

|

Trading and hedging activities by BofA Finance, the Guarantor and any of our other affiliates, including BofAS, and WFS and its affiliates, may create conflicts of interest with you and may affect your return on the Securities and their market value.

|

|

●

|

There may be potential conflicts of interest involving the calculation agent, which is an affiliate of ours.

|

|

●

|

The publisher of the Underlying may adjust the Underlying in a way that affects its levels, and the publisher has no obligation to consider your interests.

|

|

●

|

The Securities are subject to risks associated with small-size capitalization companies.

|

|

●

|

The U.S. federal income tax consequences of an investment in the Securities are uncertain, and may be adverse to a holder of the Securities.

|