PS-28

|

|

|

|

Market Linked Securities—Auto-Callable with Fixed Percentage Buffered Downside

Principal at Risk Securities Linked to the KraneShares CSI China Internet ETF due December 3, 2025

|

The material included in this Appendix was prepared by Wells Fargo Securities, LLC and will be distributed to investors in connection with the offering of the Securities described in this pricing supplement. This material does not constitute terms of the Securities. Instead, the Securities will have the terms specified in the prospectus dated December 31, 2019, the prospectus supplement dated December 31, 2019 and the product supplement no. EQUITY-1 dated January 3, 2020, as supplemented or superseded by this pricing supplement.

PS-29

Market Linked Securities

Auto-Callable with Fixed Percentage Buffered Downside

This material was prepared by Wells Fargo Securities, LLC, a registered broker -

dealer and separate non-bank affiliate of Wells Fargo & Company. This material

is not a product of Wells Fargo & Company research departments. Please see the

relevant offering materials for complete product descriptions, including related risk

and tax disclosure.

MARKET LINKED SECURITIES — AUTO-CALLABLE WITH FIXED PERCENTAGE BUFFERED DOWN SIDE ARE NOT DEPOSITS OR OTHER OBLIGATIONS OF A DEPOSITORY INSTITUTION AND ARE NOT INSURED BY THE FEDERAL DEPOSIT INSURANCE CORPORATION, THE DEPOSIT INSURANCE FUND OR ANY OTHER GOVERNMENTAL AGENCY OF THE UNITED STATES OR ANY OTHER JURISDICTION .

Market Linked Securities — Auto-Callable with Fixed Percentage Buffered Downside have complex features and are not appropriate for all investors. Before deciding to make an investment, you should read and understand the applicable preliminary pricing supplement and other related offering documents provided by the applicable issuer.

Market Linked Securities — Auto-Callable with Fixed Percentage Downside

Market Linked Securities — Auto-Callable with Fixed Percentage Buffered Downside (“these Market Linked Securities”) offer a return linked to the performance of a market measure, such as an index, exchange-traded fund or a basket of indices or exchange-traded funds (the “underlying”). In contrast to a direct investment in the underlying, these Market Linked Securities offer the potential for a positive return in the form of a fixed call premium upon automatic call, which will be triggered if the closing level of the underlying is greater than or equal to its starting level on any specified call date. These Market Linked Securities also offer a buffer against a moderate decline of the underlying. However, if these Market Linked Securities are not automatically called and the underlying has declined by more than the buffer as of the final call date, you could incur a substantial loss on your investment. If the issuer defaults on its payment obligations, you could lose your entire investment.

These Market Linked Securities are designed for investors who seek the potential fora fixed return if the underlying is flat or appreciates at all, and a measure of market risk reduction if the underlying declines. In exchange for these features, you must be willing to forgo interest payments, dividends (in the case of equity underlyings) and participation in any appreciation of the underlying beyond the fixed call premium. You must also be willing to accept the possibility of a shorter maturity upon automatic call and downside exposure to any decline in the underlying beyond the buffer. The potential to receive a call premium upon automatic call applies only on the applicable call settlement date, and the buffer applies only if you hold these Market Linked Securities at maturity.

These Market Linked Securities are unsecured debt obligations of the issuer. You will have no ability to pursue the underlying or any assets included in the underlying for payment.

A -2 | Market Linked Securities — Auto-Callable with Fixed Percentage Buffered Downside

| The charts in this section do not reflect forgone dividend payments. |

|

|

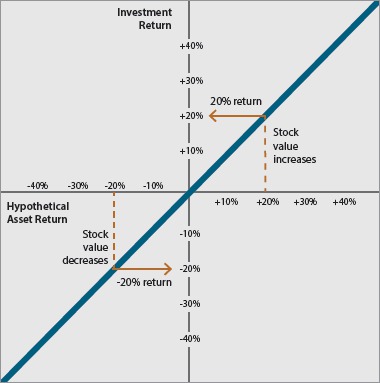

Direct investment payoff

For traditional assets, such as stocks, there is a direct relationship between the change in the level of the asset and the return on the investment. For example, as the graph indicates, suppose you bought shares of a common stock at $100 per share. If you sold the shares at $120 each, the return on the investment (excluding any dividend payments) would be $20 per share, or 20%. Similarly, if you sold the shares after the price decreased to $80 (i.e., a decline of 20%), this would result in a 20% investment loss (excluding dividends). |

Market Linked Securities — Auto-Callable with Fixed Percentage Buffered Downside

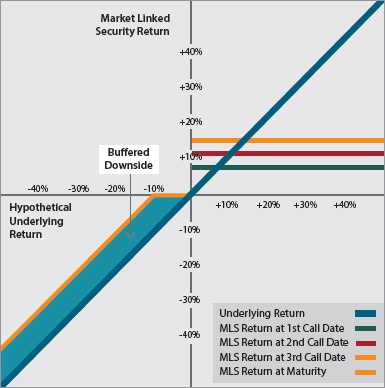

These Market Linked Securities offer a return that is linked to the performance of an underlying but that differs from the return that would be achieved on a direct investment in the underlying. If the closing level of the underlying is greater than or equal to its starting level on any one of the specified call dates, these Market Linked Securities will be automatically called and you would receive the original offering price of these Market Linked Securities plus a fixed c all premium. If these Market Linked Securities are not automatically called on one of the call dates, the payment at maturity will be based on the performance of the underlying, as measured from its starting level to its closing level on the final call date (the ending level). Under these circumstances, if the underlying has declined by more than a specified buffer, you could incur a substantial loss on your investment.

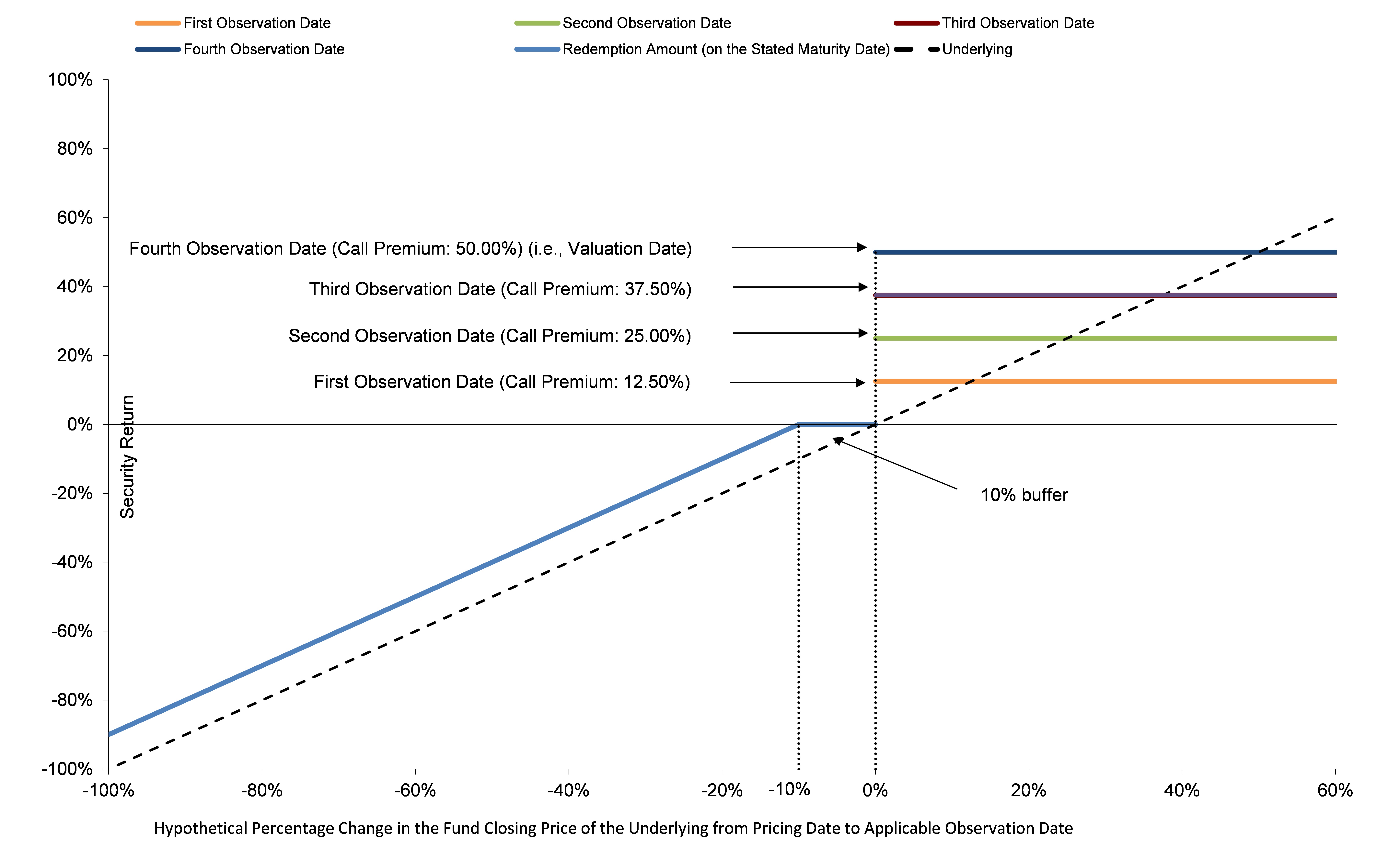

To understand how these Market Linked Securities would perform under varying market conditions, consider a hypothetical Market Linked Security with the following terms:

|

●

|

Call Dates: 1 year, 1 .5 years and 2 years. If the closing level of the underlying on any of the three call dates (occurring approximately 1 year, 1 .5 years and 2 years after issuance) is greater than or equal to the starting level, these Market Linked Securities will be automatically called, and on the related call settlement date (typically 3 to 5 business days after the call date) you will receive a cash payment equal to the original offering price plus the call premium applicable to that call date. If these Market Linked Securities are automatically called on one of the call dates prior to maturity, the term of these Market Linked Securities will be limited (to as little as o ne year in the case of the first call date in this hypothetical example) and you might not be able to reinvest your funds in an investment with a similar return profile.

|

A -3 | Market Linked Securities — Auto-Callable with Fixed Percentage Buffered Downside

|

●

|

Call Premium: 7 % per year. If these Market Linked Securities are automatically called on a call date, you will receive a payment on the applicable call settlement date equal to the $1,000 original offering price per Market Linked Security plus the applicable call premium, as set forth below:

|

|

Call Date

|

Call Premium

|

Payment per $1,000 Market Linked Security

|

|

1st call date (at 1 year)

|

7 .00% of the original offering price

|

$1 ,070.00

|

|

2nd call date (at 1 .5 years)

|

10.50% of the original offering price

|

$1 ,105.00

|

|

3rd call date (at 2 years)

|

14.00% of the original offering price

|

$1 ,140.00

|

Any return on these Market Linked Securities will be limited to the applicable call premium, even if the closing level of the underlying greatly exceeds the starting level on the applicable call date. You will not participate in any appreciation of the underlying beyond the fixed call premium. If the issuer defaults on its payment obligations, you could lose your entire

investment.

|

●

|

Buffer: 10%. If these Market Linked Securities are not automatically called, the buffer offers a measure of downside market risk reduction at maturity as compared to a direct investment in the underlying. A 10% fixed buffer means that you will be repaid the original offering price at maturity if the underlying declines by 10% or less from the starting level to the ending level — in other words, if the ending level is greater than or equal to a threshold level that is equal to 90% of the starting level. However, if these Market Linked Securities are not automatically called and the underlying declines by more than 10%, so that the ending level is less than the threshold level, you will incur a loss equal to the percentage decline of the underlying in excess of 10%. For example, if the underlying declines by 25%, the percentage decline of 25% would exceed the 10% buffer by 15% and you would incur a 15% loss at maturity.

|

| This information, including the graph to the right, is hypothetical and is provided for informational purposes only. It is not intended to represent any specific return, yield, or investment, nor is it indicative of future results. The graph illustrates the payoff on the hypothetical Market Linked Securities — Auto-Callable with Fixed Percentage Buffered Downside described above for a range of percentage changes in the closing level of the underlying from the starting level to the closing level on the applicable call date. |

|

A -4 | Market Linked Securities — Auto-Callable with Fixed Percentage Buffered Downside

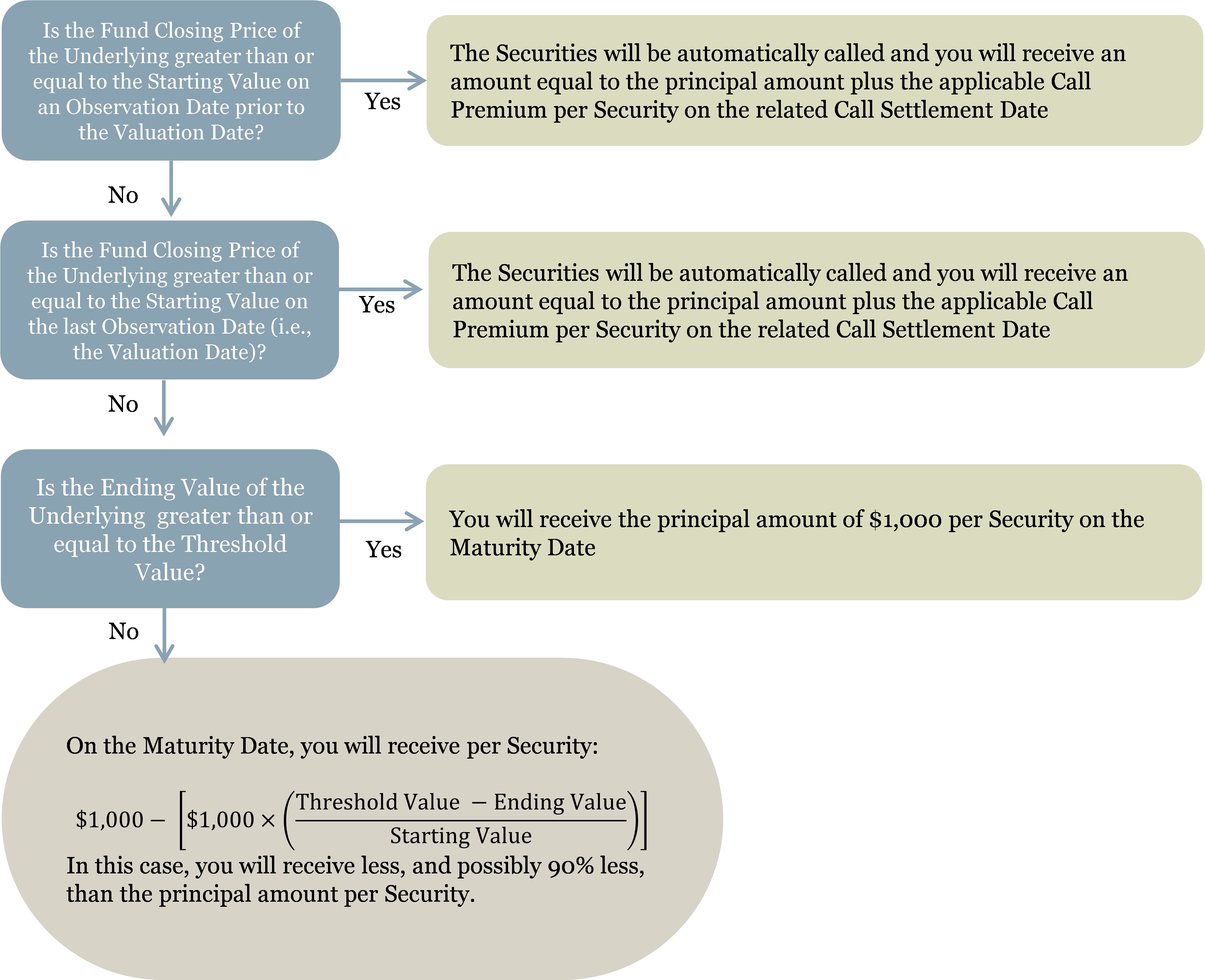

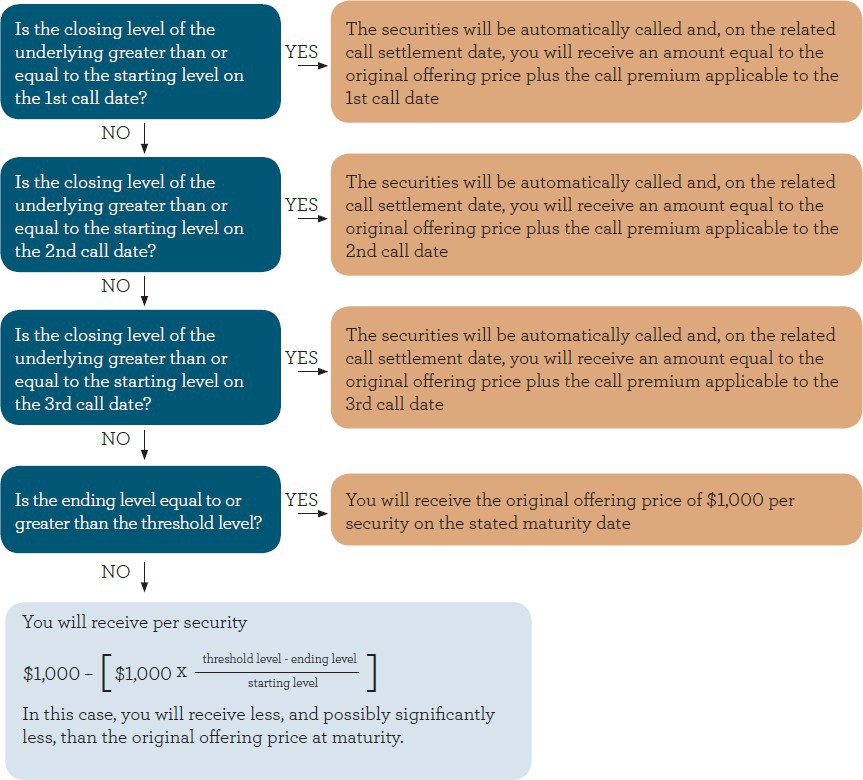

Determining payment upon automatic call or at maturity

The diagram below illustrates how to determine whether these Market Linked Securities are automatically called on a call date and, if these Market Linked Securities are not automatically called, how to determine the payment at maturity. The diagram below assumes three call dates. The ending level is the closing level of the underlying on the third call date.

A -5 | Market Linked Securities — Auto-Callable with Fixed Percentage Buffered Downside

Hypothetical Examples

The examples below are hypothetical and are provided for informational purposes only. They are not intended to represent any specific return, yield, or investment, nor are they indicative of future results. The examples illustrate the automatic call feature and, if an automatic call does not occur, the payment at maturity of these Market Linked Securities assuming the following terms:

Term: 2 years, unless earlier automatically called

Buffer: 10%

Original Offering Price: $1 ,000 per Market Linked Security

Call Date/Call Premium:

| Call Date |

Call Premium |

| 1st call date (at 1 year) |

7 .00% of the original offering price |

| 2nd call date (at 1 .5 years) |

10.50% of the original offering price |

| 3rd call date (at 2 years) |

14.00% of the original offering price |

Starting Level: 1 ,000

Threshold Level: 900, which is equal to 90% of the starting level

The first hypothetical example below illustrates a scenario in which these Market Linked Securities are automatically called on a call date for the original offering price plus the call premium applicable to that call date. The second and third hypothetical examples below illustrate scenarios in which the Market Linked Securities are not automatically called and the payment at maturity is based on the performance of the underlying from the starting level to the ending level.

Example 1:

Closing Level on 1st Call Date: 1 ,200

Because the closing level of the underlying on the 1st call date is greater than or equal to the starting level, these Market Linked Securities would be automatically called on the 1st call date and, on the related call settlement date, you would receive the original offering price of $1,000 per Market Linked Security plus a call premium of 7 .00% of the original offering price. In this example, the total payment upon automatic call would be $1,070 per Market Linked Security.

Even though the underlying appreciated by 20% from its starting level to its closing level on the 1st call date in this example, your return is limited to the call premium of 7 .00% that is applicable to the 1st call date.

Example 2:

Closing Level on 1st Call Date: 975

Closing Level on 2nd Call Date: 950

Closing Level on 3rd Call Date: 925 (ending level)

Because the hypothetical closing level of the underlying is less than the starting level on each call date, these Market Linked Securities would not be automatically called and you would not receive a call premium. However, because the ending level is greater than the threshold level (i.e., it has not declined from the starting level by more than the 10% buffer), you would be repaid the original offering price of $1 ,000 per Market Linked Security at maturity.

A -6 | Market Linked Securities — Auto-Callable with Fixed Percentage Buffered Downside

Example 3:

Closing Level on 1st Call Date: 850

Closing Level on 2nd Call Date: 7 00

Closing Level on 3rd Call Date: 500 (ending level)

Because the hypothetical closing level of the underlying is less than the starting level on each call date, these Market Linked Securities would not be automatically called and you would not receive a call premium. Furthermore, because the ending level is less than the threshold level (i.e., it has declined from the starting level by more than the 10% buffer), you would incur a loss on your investment equal to the decline of the underlying beyond the buffer. Your payment at maturity in this example would be calculated as follows:

On the stated maturity date, you would receive $600.00 per Market Linked Security, resulting in a loss of 40%.

All payments on these Market Linked Securities are subject to the ability of the issuer to make such payments to you when they are due, and you will have no ability to pursue the underlying or any asset included in the underlying for payment. If the issuer defaults on its payment obligations, you could lose your entire investment.

Estimated value of Market Linked Securities — Auto-Callable with Fixed Percentage Buffered Downside

The original offering price of these Market Linked Securities will include certain costs that are borne by you. Because of these costs, the estimated value of these Market Linked Securities on the pricing date will be less than the original offering price. If specified in the applicable pricing supplement, these costs may include the underwriting discount or commission, the hedging profits of the issuer’s hedging counterparty (which may be an affiliate of the issuer), hedging and other costs associated with the offering and costs relating to the issuer’s funding considerations for debt of this type. See “General risks and investment considerations” herein and the applicable pricing supplement for more information.

The issuer will disclose the estimated value of these Market Linked Securities in the applicable pricing supplement. The estimated value of these Market Linked Securities will be determined by estimating the value of the combination of hypothetical financial instruments that would replicate the payout on these Market Linked Securities, which combination consists of a non-interest bearing, fixed-income bond and one or more derivative instruments underlying the economic terms of these Market Linked Securities. You should read the applicable pricing supplement for more information about the estimated value of these Market Linked Securities and how it is determined.

A -7 | Market Linked Securities — Auto-Callable with Fixed Percentage Buffered Downside

Which investments are right

for you?

It is important to read and understand the applicable preliminary pricing supplement and other related offering documents and consider several factors before making an investment decision.

An investment in these Market Linked Securities may help you modify your portfolio’s risk-return profile to more closely reflect your market views. However, at maturity you may incur a loss on your investment, and you will forgo interest payments, dividend payments (in the case of equity underlyings) and any return in excess of the applicable call premium.

These Market Linked Securities are not appropriate for all investors, but may be appropriate for investors aiming to :

|

●

|

Gain or increase exposure to different asset classes and who believe that the closing level of the underlying will be greater than or equal to the starting level on one of the call dates

|

|

●

|

Receive a fixed return if the underlying is flat or appreciates at all and a buffer against a moderate decline in the underlying in lieu of participation in any potential market appreciation beyond a fixed call premium

|

|

●

|

Supplement their existing investments with new return profiles

|

|

●

|

Obtain exposure to an underlying with a different risk/return profile than a direct investment in that underlying

|

|

●

|

Seek the potential to outperform the underlying in a declining or a low to moderately appreciating market

|

you can find a discussion of risks and investment considerations on the next page and in the preliminary pricing supplement and other related offering documents for these Market Linked Securities. The following questions, which you should review with your financial advisor, are intended to initiate a conversation about whether these Market Linked Securities are right for you.

|

●

|

Are you comfortable with the potential loss of a significant portion of your initial investment as a result of a percentage decline of the underlying that exceeds the buffer?

|

|

●

|

What is your time horizon? Do you foresee liquidity needs? Will you be able to hold these investments until maturity or earlier automatic call?

|

|

●

|

Does protection against moderate market declines take precedence for you over participation in any appreciation of the underlying beyond the fixed call premium and dividend payments?

|

|

●

|

What is your outlook on the market? How confident are you in your portfolio’s ability to weather a market decline?

|

|

●

|

What is your sensitivity to the tax treatment for your investments?

|

|

●

|

Are you dependent on your investments for current income?

|

|

●

|

Are you willing to accept the credit risk of the applicable issuer in order to obtain the exposure to the underlying that these Market Linked Securities provide?

|

Before making an investment decision, please work with your financial advisor to determine which investment products may be appropriate given your financial situation, investment goals, and risk profile.

A -8 | Market Linked Securities — Auto-Callable with Fixed Percentage Buffered Downside

General risks and investment

considerations

These Market Linked Securities have complex features and are not appropriate for all investors. They involve a variety of risks and may be linked to a variety of different underlyings. Each of these Market Linked Securities and each underlying will have its own unique set of risks and investment considerations. Before you invest in these Market Linked Securities, you should thoroughly review the relevant preliminary pricing supplement and other related offering documents for a comprehensive discussion of the risks associated with the investment. The following are general risks and investment considerations applicable to these Market Linked Securities:

|

●

|

Principal and performance risk. These Market Linked Securities are not structured to repay your full original offering price on the stated maturity date. If these Market Linked Securities are not automatically called and the ending level has declined from the starting level by more than the buffer, the payment you receive at maturity will be less than the original offering price of the Market Linked Securities and you may incur a substantial loss on y our investment.

|

|

●

|

Limited upside. The potential return on these Marked Linked Securities is limited to the applicable call premium, regardless of the performance of the underlying. The underlying may appreciate by significantly more than the percentage represented by the applicable call premium from the starting level to the closing level on the applicable call date, in which case an investment in these Market Linked Securities will underperform a hypothetical alternative investment providing a 1 -to-1 return based on the performance of the underlying. Furthermore, if these Market Linked Securities are automatically called on an earlier call date, you will receive a lower call premium than if these Market Linked Securities were automatically called on a later call date.

|

|

●

|

Reinvestment risk. If these Market Linked Securities are automatically called prior to the final call date, the term of these Market Linked Securities will be less than the full term to maturity. There is no guarantee that you would be able to reinvest the proceeds from an investment in these Market Linked Securities at a comparable return for a similar level of risk in the event these Market Linked Securities are automatically called prior to maturity.

|

|

●

|

Liquidity risk. These Market Linked Securities are not appropriate for investors who may have liquidity needs prior to maturity. These Market Linked Securities are not listed on any securities exchange and are generally illiquid instruments. Neither Wells Fargo Securities nor any other person is required to maintain a secondary market for these Market Linked Securities. Accordingly, you may be unable to sell your Market Linked Securities prior to their maturity date. If you choose to sell these Market Linked Securities prior to maturity, assuming a buyer is available, you may receive less in sale proceeds than the original offering price.

|

|

●

|

Market value uncertain. These Market Linked Securities are not appropriate for investors who need their investments to maintain a stable value during their term. The value of your Market Linked Securities prior to maturity or automatic call will be affected by numerous factors, such as performance, volatility and dividend rate, if applicable, of the underlying; interest rates; the time remaining to maturity; the correlation among basket components, if applicable; and the applicable issuer’s creditworthiness. Wells Fargo Securities anticipates that the value of these Market Linked Securities will always be at a discount to the original offering price plus the call premium applicable to the next call date.

|

|

●

|

Costs to investors. The original offering price of these Market Linked Securities will include certain costs that are borne by you. These costs will adversely affect the economic terms of these Market Linked Securities and will cause their estimated value on the pricing date to be less than the original offering price. If specified in the applicable pricing supplement, these costs may include the underwriting discount or commission, the hedging profits of the issuer’s hedging counterparty (which may be an affiliate of the issuer), hedging and other costs associated with the offering, and costs relating to the issuer’s funding considerations for debt of this type. These costs will adversely affect any secondary market price for these Market Linked Securities, which may be further reduced by a bid-offer spread. As a result, unless market conditions and other relevant factors change significantly in your favor following the pricing date, any secondary market price for these Market Linked Securities is likely to be less than the original offering price.

|

|

●

|

Credit risk. Any investment in these Market Linked Securities is subject to the ability of the applicable issuer to make payments to you w hen they are due, and you will have no ability to pursue the underlying or any assets included in the underlying for payment. If the issuer defaults on its payment obligations, you could lose your entire investment. In addition, the actual or perceived creditworthiness of the issuer may affect the value of these Market Linked Securities prior to maturity.

|

|

●

|

No periodic interest or dividend payments. These Market Linked Securities do not typically provide periodic interest. These Market Linked Securities linked to equity underlyings do not provide for a pass through of any dividend paid on the equity underlyings.

|

A -9 | Market Linked Securities — Auto-Callable with Fixed Percentage Buffered Downside

|

●

|

Estimated value considerations. The estimated value of these Market Linked Securities that is disclosed in the applicable pricing supplement will be determined by the issuer or an underwriter of the offering, which underwriter may be an affiliate of the issuer and may be Wells Fargo Securities. The estimated value will be based on the issuer’s or the underwriter’s proprietary pricing models and assumptions and certain inputs that may be determined by the issuer or underwriter in its discretion. Because other dealers may have different views on these inputs, the estimated value that is disclosed in the applicable pricing supplement may be higher, and perhaps materially higher, than the estimated value that would be determined by other dealers in the market. Moreover, you should understand that the estimated value that is disclosed in the applicable pricing supplement will not be an indication of the price, if any, at which Wells Fargo Securities or any other person may be willing to buy these Market Linked Securities from you at any time after issuance.

|

|

●

|

Conflicts of interest. Potential conflicts of interest may exist between you and the applicable issuer and/or Wells Fargo Securities. For example, the applicable issuer, Wells Fargo Securities, or one of their respective affiliates may engage in business with companies whose securities are included in the underlying, or may publish research on such companies or the underlying. In addition, the applicable issuer, Wells Fargo Securities, or one of their respective affiliates may be the calculation agent for the purposes of making important determinations that affect the payments on these Market Linked Securities. Finally, the estimated value of these Market Linked Securities may be determined by the issuer or an underwriter of the offering, which underwriter may be an affiliate of the issuer and may be Wells Fargo Securities.

|

|

●

|

Effects of trading and other transactions. Trading and other transactions by the applicable issuer, Wells Fargo Securities or one of their respective affiliates could affect the underlying or the value of these Market Linked Securities.

|

|

●

|

Basket risk. If the underlying is a basket, the basket components may offset each other. Any appreciation of one or more basket components may be moderated, wholly offset, or more than offset, by depreciation of one or more other basket components.

|

|

●

|

ETF risk. If the underlying is an exchange-traded fund (ETF), it may underperform the index it is designed to track as a result of costs and fees of the ETF and differences between the constituents of the index and the actual assets held by the ETF. In addition, an investment in these Market Linked Securities linked to an ETF involves risks related to the index underlying the ETF, as discussed in the next risk consideration.

|

|

●

|

Index risk. If the underlying is an index, or an ETF that tracks an index, your return on these Market Linked Securities may be adversely affected by changes that the index publisher may make to the manner in which the index is constituted or calculated. Furthermore, if the index represents foreign securities markets, you should understand that foreign securities markets tend to be less liquid and more volatile than U.S. markets and that there is generally less information available about foreign companies than about companies that file reports with the U.S. Securities and Exchange Commission. Moreover, if the index represents emerging foreign securities markets, these Market Linked Securities will be subject to the heightened political and economic risks associated with emerging markets. If the index includes foreign securities and the level of the index is based on the U.S. dollar value of those foreign securities, these Market Linked Securities will be subject to currency exchange rate risk in addition to the other risks described above, as the level of the index will be adversely affected if the currencies in which the foreign securities trade depreciate against the U.S. dollar.

|

|

●

|

Commodity risk. These Market Linked Securities linked to commodities will be subject to a number of significant risks associated with commodities. Commodity prices tend to be volatile and may fluctuate in ways that are unpredictable and adverse to you. Commodity markets are frequently subject to disruptions, distortions, and changes due to various factors, including the lack of liquidity in the markets, the participation of speculators, and government regulation and intervention. Moreover, commodity indices may be adversely affected by a phenomenon known as “negative roll yield,” which occurs when future prices of the commodity futures contracts underlying the index are higher than current prices. Negative roll yield can have a significant negative effect on the performance of a commodity index. Furthermore, for commodities that are traded in U.S. dollars but for which market prices are driven by global demand, any strengthening of the U.S. dollar against relevant other currencies may adversely affect the demand for, and therefore the price of, those commodities.

|

|

●

|

Currency risk. These Market Linked Securities linked to currencies will be subject to a number of significant risks associated with currencies. Currency exchange rates are frequently subject to intervention by governments, which can be difficult to predict and can have a significant impact on exchange rates. Moreover, currency exchange rates are driven by complex factors relating to the economies of the relevant countries that can be difficult to understand and predict. Currencies issued by emerging market governments may be particularly volatile and will be subject to heightened risks.

|

|

●

|

Bond risk. These Market Linked Securities linked to bond indices or exchange-traded funds that are comprised of specific types of bonds with different maturities and qualities will be subject to a number of significant risks associated with bonds. In general, if market interest rates rise, the value of bonds will decline. In addition, if the market perception of the creditworthiness of the relevant bond issuers falls, the value of bonds will generally decline.

|

|

●

|

Tax considerations. You should review carefully the relevant preliminary pricing supplement and other related offering documents and consult your tax advisors regarding the application of the U.S. federal tax laws to your particular circumstances, as well as any tax consequences arising under the laws of any state, local, or non-U.S. jurisdiction.

|

A -10 | Market Linked Securities — Auto-Callable with Fixed Percentage Buffered Downside

Always read the preliminary pricing supplement and other related offering documents.

These Market Linked Securities are offered with the attached preliminary pricing supplement and other related offering documents. Investors should read and consider these documents carefully before investing. Prior to investing, always consult your financial advisor to understand the investment structure in detail.

For more information about these Market Linked Securities and the structures currently available for investment, contact your financial advisor, who can advise you of whether or not a particular offering may meet your individual needs and investment requirements.

Wells Fargo Securities is the trade name for the capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including Wells Fargo Securities, LLC, a member of FINRA, NYSE, and SIPC, and Wells Fargo Bank, N.A.

Wells Fargo Advisors is a trade name used by Wells Fargo Clearing services, LLC and Wells Fargo Advisors Financial Network, LLC, members SIPC, separate registered broker-dealers and non-bank affiliates of Wells Fargo & Company .

© 2021 Wells Fargo Securities, LLC. All rights reserved.