This pricing supplement, which is not complete and may be changed, relates to an effective Registration Statement under the Securities Act of 1933. This pricing supplement and the accompanying product supplement, prospectus supplement and prospectus are not an offer to sell these notes in any country or jurisdiction where such an offer would not be permitted.

SUBJECT TO COMPLETION, DATED April 6, 2022

|

Preliminary Pricing Supplement - Subject to Completion

(To Prospectus dated December 31, 2019,

Prospectus Supplement dated December 31, 2019 and

Product Supplement COMM-1 dated June 1, 2021)

Dated April , 2022

|

Filed Pursuant to Rule 424(b)(2)

Series A Registration Statement No. 333-234425

|

|

|

|

BofA Finance LLC $---- Market Linked Notes

|

|

Linked to an Equally Weighted Basket of Commodities and Commodity Futures Contracts Due

Fully and Unconditionally Guaranteed by Bank of America Corporation

|

|

Investment Description

|

|

The Market Linked Notes (the “Notes”) linked to an equally weighted basket of commodities and commodity futures contracts due are senior unsecured obligations issued by BofA Finance LLC (“BofA Finance”), a direct, wholly-owned subsidiary of Bank of America Corporation (“BAC” or the “Guarantor”), which are fully and unconditionally guaranteed by the Guarantor. The return on the Notes is linked to the performance of an equally weighted basket (the “Basket” or “Market Measure”) comprised of the commodities and commodity futures contracts specified below (each, a “Basket Component”).If the Basket Return is positive, BofA Finance will repay the Stated Principal Amount of the Notes at maturity plus a return equal to the Basket Return. If the Basket Return is zero or negative, BofA Finance will repay the Stated Principal Amount of the Notes at maturity but you will not receive any return on your investment.

Investing in the Notes involves significant risks. You will not receive coupon payments during the term of the Notes.The repayment of the Stated Principal Amount applies only if you hold the Notes to maturity. Any payment on the Notes, including any repayment of the Stated Principal Amount, is subject to the creditworthiness of BofA Finance and the Guarantor and is not, either directly or indirectly, an obligation of any third party.

|

|

Features

|

|

Key Dates1

|

|

❑ Growth Potential— If the Basket Return is positive, BofA Finance will repay the Stated Principal Amount of the Notes at maturity plus a return equal to the Basket Return.

❑ Repayment of Principal at Maturity— If the Basket Return is zero or negative, you will receive the Stated Principal Amount at maturity but will not receive any return on your investment.

Any payment on the Notes is subject to the creditworthiness of BofA Finance and the Guarantor.

|

|

Trade Date

Issue Date

Valuation Date2

Maturity Date

|

April 11, 2022

April 13, 2022

Expected to be between October 11, 2024 and January 13, 2025

Expected to be between October 17, 2024 and January 16, 2025

|

|

1 Subject to change and will be set forth in the final pricing supplement relating to the Notes.

2 See page PS-4 for additional details.

|

|

NOTICE TO INVESTORS: THE NOTES ARE SIGNIFICANTLY RISKIER THAN CONVENTIONAL DEBT INSTRUMENTS. THE NOTES ARE SUBJECT TO THE CREDIT RISK INHERENT IN PURCHASING A DEBT OBLIGATION OF BOFA FINANCE THAT IS GUARANTEED BY BAC. YOU SHOULD NOT PURCHASE THE NOTES IF YOU DO NOT UNDERSTAND OR ARE NOT COMFORTABLE WITH THE SIGNIFICANT RISKS INVOLVED IN INVESTING IN THE NOTES.

YOU SHOULD CAREFULLY CONSIDER THE RISKS DESCRIBED UNDER “RISK FACTORS’’ BEGINNING ON PAGE PS-6 OF THIS PRICING SUPPLEMENT, PAGE PS-6 OF THE ACCOMPANYING PRODUCT SUPPLEMENT, PAGE S-5 OF THE ACCOMPANYING PROSPECTUS SUPPLEMENT AND PAGE 7 OF THE ACCOMPANYING PROSPECTUS BEFORE PURCHASING ANY NOTES. EVENTS RELATING TO ANY OF THOSE RISKS, OR OTHER RISKS AND UNCERTAINTIES, COULD ADVERSELY AFFECT THE MARKET VALUE OF, AND THE RETURN ON, YOUR NOTES. YOU MAY NOT RECEIVE ANY RETURN ON YOUR INVESTMENT IN THE NOTES. THE NOTES WILL NOT BE LISTED ON ANY SECURITIES EXCHANGE AND MAY HAVE LIMITED OR NO LIQUIDITY.

|

|

Notes Offering

|

|

We are offering Market Linked Notes linked to an equally weighted basket of commodities and commodity futures contracts due . The Basket Components are listed below and described in more detail beginning on page PS-13 of this pricing supplement. Any payment on the Notes will be based on the performance of the Basket. The Initial Commodity Price of each Basket Component will be determined on the Trade Date. The Notes are our senior unsecured obligations, guaranteed by BAC, and are offered at the Public Offering Price described below.

West Texas Intermediate (“WTI”) light sweet crude oil futures (Bloomberg ticker* “CLK2”)

Brent crude oil futures (Bloomberg ticker* “COM2”)

Natural gas futures (Bloomberg ticker* “NGK2”)

Corn futures (Bloomberg ticker* “C K2”)

Soybeans futures (Bloomberg ticker* “S K2”)

Wheat futures (Bloomberg ticker* “W K2”)

Grade A copper spot price (Bloomberg ticker “LOCADY”)

Special high-grade zinc spot price (Bloomberg ticker “LOZSDY”)

*Bloomberg ticker symbols are being provided for reference purposes only and represent the specific futures contract which will be used to determine the Initial Commodity Price by application of the methodology as described under “Additional Terms of the Notes— Determining the Commodity Price of a Basket Component” in this pricing supplement.

|

See “Summary” in this pricing supplement. The Notes will have the terms specified in the accompanying product supplement, prospectus supplement and prospectus, as supplemented by this pricing supplement.

None of the Securities and Exchange Commission (the “SEC”), any state securities commission, or any other regulatory body has approved or disapproved of these Notes or the guarantee, or passed upon the adequacy or accuracy of this pricing supplement, or the accompanying product supplement, prospectus supplement or prospectus. Any representation to the contrary is a criminal offense. The Notes and the related guarantee of the Notes by the Guarantor are unsecured and are not savings accounts, deposits, or other obligations of a bank. The Notes are not guaranteed by Bank of America, N.A. or any other bank, are not insured by the Federal Deposit Insurance Corporation or any other governmental agency and involve investment risks.

|

|

Public Offering Price

|

Underwriting Discount(1)

|

Proceeds (before expenses) to BofA Finance

|

|

Per Note

|

$1,000.00

|

$15.00

|

$985.00

|

|

Total

|

$

|

$

|

$

|

(1) The underwriting discount is $15.00 per Note. BofA Securities, Inc. (“BofAS”), acting as principal, expects to purchase from BofA Finance, and BofA Finance expects to sell to BofAS, the aggregate principal amount of the Notes set forth above for $985.00 per Note. UBS Financial Services Inc. (“UBS”), acting as a selling agent for sales of the Notes, expects to purchase from BofAS, and BofAS expects to sell to UBS, all of the Notes for $985.00 per Note. UBS will receive an underwriting discount of $15.00 per Note for each Note it sells in this offering. UBS proposes to offer the Notes to the public at a price of $1,000.00 per Note. For additional information on the distribution of the Notes, see “Supplement to the Plan of Distribution; Role of BofAS and Conflicts of Interest” in this pricing supplement.

The initial estimated value of the Notes will be less than the public offering price. The initial estimated value of the Notes as of the Trade Date is expected to be between $920 and $940 per $1,000 in Stated Principal Amount. See “Summary” on page PS-4 of this pricing supplement, “Risk Factors” beginning on page PS-6 of this pricing supplement and “Structuring the Notes” on page PS-24 of this pricing supplement for additional information. The actual value of your Notes at any time will reflect many factors and cannot be predicted with accuracy.

UBS Financial Services Inc. |

BofA Securities

|

|

Additional Information about BofA Finance LLC, Bank of America Corporation and the Notes

|

|

You should read carefully this entire pricing supplement and the accompanying product supplement, prospectus supplement and prospectus to understand fully the terms of the Notes, as well as the tax and other considerations important to you in making a decision about whether to invest in the Notes. In particular, you should review carefully the section in this pricing supplement entitled “Risk Factors,” which highlights a number of risks of an investment in the Notes, to determine whether an investment in the Notes is appropriate for you. If information in this pricing supplement is inconsistent with the product supplement, prospectus supplement or prospectus, this pricing supplement will supersede those documents. You are urged to consult with your own attorneys and business and tax advisors before making a decision to purchase any of the Notes.

The information in the “Summary” section is qualified in its entirety by the more detailed explanation set forth elsewhere in this pricing supplement and the accompanying product supplement, prospectus supplement and prospectus. You should rely only on the information contained in this pricing supplement and the accompanying product supplement, prospectus supplement and prospectus. We have not authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. None of us, the Guarantor, BofAS or UBS is making an offer to sell these Notes in any jurisdiction where the offer or sale is not permitted. You should assume that the information in this pricing supplement and the accompanying product supplement, prospectus supplement, and prospectus is accurate only as of the date on their respective front covers.

Certain terms used but not defined in this pricing supplement have the meanings set forth in the accompanying product supplement, prospectus supplement and prospectus. Unless otherwise indicated or unless the context requires otherwise, all references in this pricing supplement to “we,” “us,” “our,” or similar references are to BofA Finance, and not to BAC (or any other affiliate of BofA Finance).

The above-referenced accompanying documents may be accessed at the following links:

♦

Product supplement COMM-1 dated June 1, 2021:

♦

Series A MTN prospectus supplement dated December 31, 2019 and prospectus dated December 31, 2019:

The Notes are our senior debt securities. Any payments on the Notes are fully and unconditionally guaranteed by BAC. The Notes and the related guarantee are not insured by the Federal Deposit Insurance Corporation or secured by collateral. The Notes will rank equally in right of payment with all of our other unsecured and unsubordinated obligations, and the related guarantee will rank equally in right of payment with all of BAC’s other unsecured and unsubordinated obligations, in each case, except obligations that are subject to any priorities or preferences by law. Any payments due on the Notes, including any repayment of the principal amount, will be subject to the credit risk of BofA Finance, as Issuer, and BAC, as Guarantor.

|

PS-2

|

The Notes may be suitable for you if, among other considerations:

♦

You fully understand the risks inherent in an investment in the Notes.

♦

You do not seek current income from your investment

♦

You understand and accept the risks associated with the Basket Components.

♦

You believe that the value of the Basket will increase over the term of the Notes and that the Final Basket Value is likely to close above the Initial Basket Value.

♦

You can tolerate fluctuations in the value of the Notes prior to maturity that may be similar to or exceed the downside fluctuations in the value of the Basket.

♦

You are willing and able to hold the Notes to maturity, and accept that there may be little or no secondary market for the Notes.

♦

You are willing to assume the credit risk of BofA Finance and BAC for all payments under the Notes, and understand that if BofA Finance and BAC default on their obligations, you might not receive any amounts due to you, including any repayment of the Stated Principal Amount.

|

The Notes may not be suitable for you if, among other considerations:

♦

You do not fully understand the risks inherent in an investment in the Notes.

♦

You seek current income from this investment.

♦

You do not understand or are not willing to accept the risks associated with the Basket Components.

♦

You believe that the value of the Basket will decline during the term of the Notes and the Final Basket Value is likely to close below the Initial Basket Value on the Valuation Date, in which case you will not receive any return on your investment.

♦

You cannot tolerate fluctuations in the value of the Notes prior to maturity that may be similar to or exceed the downside fluctuations in the value of the Basket.

♦

You seek an investment for which there will be an active secondary market.

♦

You prefer the lower risk of conventional fixed income investments with comparable maturities and credit ratings.

♦

You are not willing to assume the credit risk of BofA Finance and BAC for all payments under the Notes, including any repayment of the Stated Principal Amount.

|

|

The suitability considerations identified above are not exhaustive. Whether or not the Notes are a suitable investment for you will depend on your individual circumstances and you should reach an investment decision only after you and your investment, legal, tax, accounting and other advisors have carefully considered the suitability of an investment in the Notes in light of your particular circumstances. You should review “The Basket and the Basket Components” herein for more information on the Basket Components. You should also review carefully the “Risk Factors” section herein for risks related to an investment in the Notes.

|

PS-3

|

Summary

|

|

Issuer

|

BofA Finance

|

|

Guarantor

|

BAC

|

|

Public Offering Price

|

100% of the Stated Principal Amount

|

|

Stated Principal Amount

|

$1,000.00 per Note

|

|

Term

|

Approximately 30-33 months

|

|

Trade Date1

|

April 11, 2022

|

|

Issue Date1

|

April 13, 2022

|

|

Valuation Date1

|

Expected to be between October 11, 2024 and January 13, 2025, subject to postponement as set forth in “Description of the Notes—Basket Market Measures—Observation Values or Ending Values of the Basket” on page PS-25 of the accompanying product supplement (with references to "closing value of the Basket Component" deemed to be references to "Final Commodity Price" and references to "Ending Value" deemed to be references to "Final Basket Value").

|

|

Maturity Date1

|

Expected to be between October 17, 2024 and January 16, 2025

|

|

Basket/Market Measure

|

The Notes are linked to an equally weighted basket consisting of the following commodities and commodity futures contracts and their respective weightings:

|

|

West Texas Intermediate (“WTI”) light sweet crude oil futures (Bloomberg ticker* “CLK2”)

|

12.50%

|

|

Brent crude oil futures (Bloomberg ticker* “COM2”)

|

12.50%

|

|

Natural gas futures (Bloomberg ticker* “NGK2”)

|

12.50%

|

|

Corn futures (Bloomberg ticker* “C K2”)

|

12.50%

|

|

Soybeans futures (Bloomberg ticker* “S K2”)

|

12.50%

|

|

Wheat futures (Bloomberg ticker* “W K2”)

|

12.50%

|

|

Grade A copper spot price (Bloomberg ticker “LOCADY”)

|

12.50%

|

|

Special high-grade zinc spot price (Bloomberg ticker “LOZSDY”)

|

12.50%

|

*Bloomberg ticker symbols are being provided for reference purposes only and represent the specific futures contract which will be used to determine the Initial Commodity Price by application of the methodology as described under “Additional Terms of the Notes— Determining the Commodity Price of a Basket Component” in this pricing supplement.

|

|

Payment At Maturity (per $1,000.00 Stated Principal Amount)

|

If the Basket Return is positive, we will repay the Stated Principal Amount of the Notes at maturity plus a return equal to the Basket Return, calculated as follows:

$1,000.00 × (1 + Basket Return)

If the Basket Return is zero or negative, we will repay the Stated Principal Amount of the Notes at maturity.

In this scenario, you will not receive any return on your investment.

|

|

Basket Return

|

Final Basket Value — Initial Basket Value

Initial Basket Value

|

|

Initial Basket Value

|

100.00

|

|

Final Basket Value

|

100.00 × (1 + the sum of the Weighted Basket Component Returns)

|

|

Weighted Basket Component Return

|

For each Basket Component, its weighting multiplied by its Basket Component Return

|

|

Basket Component Return

|

For each Basket Component,

Final Commodity Price — Initial Commodity Price

Initial Commodity Price

|

|

Initial Commodity Price

|

For each Basket Component, the Commodity Price of that Basket Component on the Trade Date, as specified on the cover page of this pricing supplement.

|

|

Final Commodity Price

|

For each Basket Component, the Commodity Price of that Basket Component on the Valuation Date.

|

|

Commodity Price

|

See “Additional Terms of the Notes—Determining the Commodity Price of a Basket Commodity” in this pricing supplement.

|

|

Calculation Agent

|

BofAS, an affiliate of BofA Finance.

|

|

Selling Agents

|

BofAS and UBS.

|

|

Events of Default and Acceleration

|

If an Event of Default, as defined in the senior indenture relating to the Notes and in the section entitled “Description of Debt Securities — Events of Default and Rights of Acceleration” beginning on page 22 of the accompanying prospectus, with respect to the Notes occurs and is continuing, the amount payable to a holder of the Notes upon any acceleration permitted under the senior indenture will be equal to the amount described under the caption “—Payment at Maturity” above, calculated as though the date of acceleration were the Maturity Date of the Notes and as though the Valuation Date were the third Market Measure Business Day prior to the date of acceleration. In case of a default in the payment of the Notes, whether at their maturity or upon acceleration, the Notes will not bear a default interest rate.

|

1 Subject to change and will be set forth in the final pricing supplement relating to the Notes.

PS-4

|

Investment Timeline

|

|

|

|

|

|

|

|

Trade Date

|

|

The Initial Commodity Price of each Basket Component is observed.

|

|

|

|

|

|

|

|

Maturity Date

|

|

The Final Basket Value is determined on the Valuation Date and the Basket Return is calculated.

If the Basket Return is positive, we will repay the Stated Principal Amount of the Notes at maturity plus a return equal to the Basket Return, calculated as follows:

$1,000.00 × (1 + Basket Return)

If the Basket Return is zero or negative, we will repay the Stated Principal Amount of the Notes at maturity.

In this scenario, you will not receive any return on your investment.

|

INVESTING IN THE NOTES INVOLVES SIGNIFICANT RISKS. YOU WILL BE EXPOSED TO THE MARKET RISK OF THE BASKET COMPONENTS. THE REPAYMENT OF THE STATED PRINCIPAL AMOUNT APPLIES ONLY IF YOU HOLD THE NOTES TO MATURITY. ANY PAYMENT ON THE NOTES IS SUBJECT TO THE CREDITWORTHINESS OF BOFA FINANCE AND THE GUARANTOR.

PS-5

Your investment in the Notes entails significant risks, many of which differ from those of a conventional debt security. Your decision to purchase the Notes should be made only after carefully considering the risks of an investment in the Notes, including those discussed below, with your advisors in light of your particular circumstances. The Notes are not an appropriate investment for you if you are not knowledgeable about significant elements of the Notes or financial matters in general. You should carefully review the more detailed explanation of risks relating to the Notes in the “Risk Factors” sections beginning on page PS-6 of the accompanying product supplement, page S-5 of the accompanying prospectus supplement and page 7 of the accompanying prospectus identified on page PS-2 above.

Structure-related Risks

|

♦

|

You may not receive a return on your investment. If the Final Basket Value is equal to or less than the Initial Basket Value, at maturity, you will receive the Stated Principal Amount. In that case, you will not receive any return on your investment.

|

|

♦

|

Although the Notes provide for the repayment of the Stated Principal Amount at maturity, you may nevertheless suffer a loss on your investment in real value terms if the Basket declines or does not appreciate sufficiently from the Initial Basket Value to the Final Basket Value. This is because inflation may cause the real value of the Stated Principal Amount to be less at maturity than it is at the time you invest, and because an investment in the Notes represents a forgone opportunity to invest in an alternative asset that does generate a positive real return. This potential loss in real value terms is significant given the approximately 30- to 33-month term of the Notes. You should carefully consider whether an investment that may not provide for any return on your investment, or may provide a return that is lower than the return on alternative investments, is appropriate for you.

|

|

♦

|

The Valuation Date and the Maturity Date are pricing terms of the Notes and will be set by us on the Trade Date. We will not set the Valuation Date or the Maturity Date until the Trade Date. Therefore, the term of the Notes could be as short as approximately 30 months or as long as approximately 33 months. You should be willing to hold the Notes for up to approximately 33 months. The Valuation Date and the Maturity Date selected by us could have an impact on the value of the Notes.

|

|

♦

|

The Notes do not bear interest. Unlike a conventional debt security, no interest payments will be paid over the term of the Notes, regardless of the extent to which the Final Basket Value exceeds the Initial Basket Value.

|

|

♦

|

The Payment at Maturity will not reflect the value of the Basket other than on the Valuation Date. The value of the Basket during the term of the Notes other than on the Valuation Date will not affect payment on the Notes. Notwithstanding the foregoing, investors should generally be aware of the performance of the Basket and the Basket Components while holding the Notes, as the performance of the Basket and the Basket Components may influence the market value of the Notes. The calculation agent will calculate the Payment at Maturity by comparing only the Initial Basket Value to the Final Basket Value for the Basket. No other value of the Basket will be taken into account. As a result, if the Final Basket Value is equal to or less than the Initial Basket Value, you will receive the Stated Principal Amount at maturity, even if the value of the Basket was always above the Initial Basket Value prior to the Valuation Date.

|

|

♦

|

Your return on the Notes may be less than the yield on a conventional debt security of comparable maturity. Any return that you receive on the Notes may be less than the return you would earn if you purchased a conventional debt security with the same Maturity Date. As a result, your investment in the Notes may not reflect the full opportunity cost to you when you consider factors, such as inflation, that affect the time value of money.

|

|

♦

|

Changes in the price of one of the Basket Components may be offset by changes in the price of the other Basket Components. The Notes are linked to a Basket. Changes in the prices of one or more of the Basket Components may not correlate with changes in the prices of one or more of the other Basket Components. The prices of one or more Basket Components may increase, while the prices of one or more of the other Basket Components may decrease or not increase as much. Therefore, in calculating the value of the Basket, increases in the price of one Basket Component may be moderated or wholly offset by decreases or lesser increases in the price of one or more of the other Basket Components.

|

|

♦

|

Any payment on the Notes is subject to our credit risk and the credit risk of the Guarantor, and actual or perceived changes in our or the Guarantor’s creditworthiness are expected to affect the value of the Notes. The Notes are our senior unsecured debt securities. Any payment on the Notes will be fully and unconditionally guaranteed by the Guarantor. The Notes are not guaranteed by any entity other than the Guarantor. As a result, your receipt of any payment on the Notes will be dependent upon our ability and the ability of the Guarantor to repay our respective obligations under the Notes on the Maturity Date, regardless of the Final Basket Value as compared to the Initial Basket Value. No assurance can be given as to what our financial condition or the financial condition of the Guarantor will be on the Maturity Date. If we and the Guarantor become unable to meet our respective financial obligations as they become due, you may not receive the amount payable under the terms of the Notes and you could lose all of your initial investment.

|

In addition, our credit ratings and the credit ratings of the Guarantor are assessments by ratings agencies of our respective abilities to pay our obligations. Consequently, our or the Guarantor’s perceived creditworthiness and actual or anticipated decreases in our or the Guarantor’s credit ratings or increases in the spread between the yield on our respective securities and the yield on U.S. Treasury securities (the “credit spread”) prior to the Maturity Date may adversely affect the market value of the Notes. However, because your return on the Notes depends upon factors in addition to our ability and the ability of the Guarantor to pay our respective obligations, such as the prices of the Basket Components, an improvement in our or the Guarantor’s credit ratings will not reduce the other investment risks related to the Notes.

|

♦

|

We are a finance subsidiary and, as such, have no independent assets, operations or revenues. We are a finance subsidiary of BAC, have no operations other than those related to the issuance, administration and repayment of our debt securities that are guaranteed by the Guarantor,

|

PS-6

|

|

and are dependent upon the Guarantor and/or its other subsidiaries to meet our obligations under the Notes in the ordinary course. Therefore, our ability to make payments on the Notes may be limited.

|

Valuation and Market-related Risks

|

♦

|

The public offering price you pay for the Notes will exceed their initial estimated value. The range of initial estimated values of the Notes that is provided on the cover page of this preliminary pricing supplement, and the initial estimated value as of the Trade Date that will be provided in the final pricing supplement, are each estimates only, determined as of a particular point in time by reference to our and our affiliates' pricing models. These pricing models consider certain assumptions and variables, including our credit spreads and those of the Guarantor, the Guarantor’s internal funding rate, mid-market terms on hedging transactions, expectations on interest rates, dividends and volatility, price-sensitivity analysis, and the expected term of the Notes. These pricing models rely in part on certain forecasts about future events, which may prove to be incorrect. If you attempt to sell the Notes prior to maturity, their market value may be lower than the price you paid for them and lower than their initial estimated value. This is due to, among other things, changes in the prices of the Basket Components, changes in the Guarantor’s internal funding rate, and the inclusion in the public offering price of the underwriting discount and the hedging related charges, all as further described in "Structuring the Notes" below. These factors, together with various credit, market and economic factors over the term of the Notes, are expected to reduce the price at which you may be able to sell the Notes in any secondary market and will affect the value of the Notes in complex and unpredictable ways.

|

|

♦

|

The initial estimated value does not represent a minimum or maximum price at which we, BAC, BofAS or any of our other affiliates would be willing to purchase your Notes in any secondary market (if any exists) at any time. The value of your Notes at any time after issuance will vary based on many factors that cannot be predicted with accuracy, including the performance of the Basket Components, our and BAC’s creditworthiness and changes in market conditions.

|

|

♦

|

The price of the Notes that may be paid by BofAS in any secondary market (if BofAS makes a market, which it is not required to do), as well asthe price which may be reflected on customer account statements, will be higher than the then-current estimated value of the Notes for a limited time period after the Trade Date. As agreed by BofAS and UBS, for approximately a four-month period after the Trade Date, to the extent BofAS offers to buy the Notes in the secondary market, it will do so at a price that will exceed the estimated value of the Notes at that time. The amount of this excess, which represents a portion of the hedging-related charges expected to be realized by BofAS and UBS over the term of the Notes, will decline to zero on a straight line basis over that four-month period. Accordingly, the estimated value of your Notes during this initial four-month period may be lower than the value shown on your customer account statements. Thereafter, if BofAS buys or sells your Notes, it will do so at prices that reflect the estimated value determined by reference to its pricing models at that time. Any price at any time after the Trade Date will be based on then-prevailing market conditions and other considerations, including the performances of the Basket Components and the remaining term of the Notes. However, none of us, the Guarantor, BofAS or any other party is obligated to purchase your Notes at any price or at any time, and we cannot assure you that any party will purchase your Notes at a price that equals or exceeds the initial estimated value of the Notes.

|

|

♦

|

We cannot assure you that a trading market for your Notes will ever develop or be maintained. We will not list the Notes on any securities exchange. We cannot predict how the Notes will trade in any secondary market or whether that market will be liquid or illiquid.

|

The development of a trading market for the Notes will depend on the Guarantor’s financial performance and other factors, including changes in the prices of the Basket Components. The number of potential buyers of your Notes in any secondary market may be limited. We anticipate that BofAS will act as a market-maker for the Notes, but none of us, the Guarantor or BofAS is required to do so. There is no assurance that any party will be willing to purchase your Notes at any price in any secondary market. BofAS may discontinue its market-making activities as to the Notes at any time. To the extent that BofAS engages in any market-making activities, it may bid for or offer the Notes. Any price at which BofAS may bid for, offer, purchase, or sell any Notes may differ from the values determined by pricing models that it may use, whether as a result of dealer discounts, mark-ups, or other transaction costs. These bids, offers, or completed transactions may affect the prices, if any, at which the Notes might otherwise trade in the market. In addition, if at any time BofAS were to cease acting as a market-maker as to the Notes, it is likely that there would be significantly less liquidity in the secondary market. In such a case, the price at which the Notes could be sold likely would be lower than if an active market existed.

|

♦

|

Economic and market factors have affected the terms of the Notes and may affect the market value of the Notes prior to maturity. Because market-linked notes, including the Notes, can be thought of as having a debt component and a derivative component, factors that influence the values of debt instruments and options and other derivatives will also affect the terms and features of the Notes at issuance and the market price of the Notes prior to maturity. These factors include the prices of the Basket Components; the volatility of the Basket Components; the time remaining to the maturity of the Notes; interest rates in the markets; geopolitical conditions and economic, financial, political, force majeure and regulatory or judicial events; whether the value of the Basket is currently or has been less than the Initial Basket Value; the availability of comparable instruments; the creditworthiness of BofA Finance, as issuer, and BAC, as guarantor; and the then current bid-ask spread for the Notes and the factors discussed under “— Trading and hedging activities by us, the Guarantor and any of our other affiliates, including BofAS, and UBS and its affiliates, may create conflicts of interest with you and may affect your return on the Notes and their market value” below. These factors are unpredictable and interrelated and may offset or magnify each other.

|

|

♦

|

Sale of the Notes prior to maturity may result in a loss of principal. You will be entitled to receive at least the full Stated Principal Amount of your Notes, subject to the credit risk of BofA Finance and BAC, only if you hold the Notes to maturity. The value of the Notes may fluctuate during the term of the Notes, and if you are able to sell your Notes prior to maturity, you may receive less than the full Stated Principal Amount of your Notes.

|

PS-7

Conflict-related Risks

|

♦

|

Trading and hedging activities by us, including BofAS,the Guarantor and any of our other affiliates, and UBS and its affiliates, may create conflicts of interest with you and may affect your return on the Notes and their market value.We, the Guarantor or one or more of our other affiliates, including BofAS, and UBS and its affiliates, may buy or sell the Basket Components or the assets represented by the Basket Components, or futures or options contracts on the Basket Components or those assets, or other listed or over-the-counter derivative instruments linked to the Basket Components or those assets. We, the Guarantor or one or more of our other affiliates, including BofAS, and UBS and its affiliates also may issue or underwrite other financial instruments with returns based upon the Basket Components and the assets represented by the Basket Components. We expect to enter into arrangements or adjust or close out existing transactions to hedge our obligations under the Notes. We, the Guarantor or our other affiliates, including BofAS, and UBS and its affiliates also may enter into hedging transactions relating to other notes or instruments, some of which may have returns calculated in a manner related to that of the Notes offered hereby. We or UBS may enter into such hedging arrangements with one of our or their affiliates. Our affiliates or their affiliates may enter into additional hedging transactions with other parties relating to the Notes and the Basket Components. This hedging activity is expected to result in a profit to those engaging in the hedging activity, which could be more or less than initially expected, or the hedging activity could also result in a loss. We and our affiliates and UBS and its affiliates will price these hedging transactions with the intent to realize a profit, regardless of whether the value of the Notes increases or decreases. Any profit in connection with such hedging activities will be in addition to any other compensation that we, the Guarantor and our other affiliates, including BofAS, and UBS and its affiliates receive for the sale of the Notes, which creates an additional incentive to sell the Notes to you. We, the Guarantor or one or more of our other affiliates, including BofAS, and UBS and its affiliates may execute such purchases or sales for our own or their own accounts, for business reasons, or in connection with hedging our obligations under the Notes. The transactions described above may present a conflict of interest between your interest in the Notes and the interests we, the Guarantor and our other affiliates, including BofAS, and UBS and its affiliates may have in our or their proprietary accounts, in facilitating transactions, including block trades, for our or their other customers, and in accounts under our or their management.

|

The transactions described above may adversely affect the value of the Basket Components in a manner that could be adverse to your investment in the Notes. On or before the Trade Date, any purchases or sales by us, the Guarantor or our other affiliates, including BofAS or others on its behalf, and UBS and its affiliates (including for the purpose of hedging some or all of our anticipated exposure in connection with the Notes) may affect the price of the Basket Components. Consequently, the price of the Basket Components may change subsequent to the Trade Date, which may adversely affect the market value of the Notes. In addition, these activities may decrease the market value of your Notes prior to maturity, and may affect the amounts to be paid on the Notes. We, the Guarantor or one or more of our other affiliates, including BofAS, and UBS and its affiliates may purchase or otherwise acquire a long or short position in the Notes and may hold or resell the Notes. For example, BofAS may enter into these transactions in connection with any market making activities in which it engages. We cannot assure you that these activities will not adversely affect the price of the Basket Components, the market value of your Notes prior to maturity or the amounts payable on the Notes.

|

♦

|

There may be potential conflicts of interest involving the calculation agent, which is an affiliate of ours. We have the right to appoint and remove the calculation agent. One of our affiliates will be the calculation agent for the Notes and, as such, will make a variety of determinations relating to the Notes, including the amounts that will be paid on the Notes. Under some circumstances, these duties could result in a conflict of interest between its status as our affiliate and its responsibilities as calculation agent.

|

Basket-related Risks

|

♦

|

The Notes are subject to the market risk of the Basket Components. The return on the Notes, which may be negative, is directly linked to the performance of the Basket Components. The prices of the Basket Components can rise or fall sharply due to factors specific to the Basket Components, such as industry and regulatory developments and other events, as well as general market factors, such as general commodity market volatility and prices, interest rates and economic and political conditions.

|

|

♦

|

Ownership of the Notes will not entitle you to any rights with respect to the Basket Components or any related futures contracts. You will not own or have any beneficial or other legal interest in any of the commodities or futures contracts represented by the Basket Components. We will not invest in any of the commodities or futures contracts represented by or included in the Basket Components for your benefit.

|

|

♦

|

Suspensions or disruptions of trading in the Basket Components and any related futures contracts may adversely affect the value of the Notes. The commodity markets are subject to temporary distortions or other disruptions due to various factors, including the lack of liquidity in the markets, the participation of speculators and government regulation and intervention. Any such distortion, disruption, or any other force majeure (such as an act of God, fire, flood, severe weather conditions, act of governmental authority, labor difficulty, etc.), may adversely affect the prices of or trading in the Basket Components or the manner in which they are calculated, and therefore, the value of the Notes.

|

|

♦

|

Investments linked to commodities are subject to sharp fluctuations in commodity prices. Investments, such as the Notes, linked to the prices of commodities are subject to sharp fluctuations in the prices of commodities and commodity futures over short periods of time for a variety of reasons, including changes in supply and demand relationships; weather; climatic events; the occurrence of natural disasters; wars; political and civil upheavals; acts of terrorism; trade, fiscal, monetary, and exchange control programs; domestic and foreign political and economic events and policies; disease; pestilence; technological developments; changes in interest rates; and trading activities in commodities and commodity futures. These factors may affect the Commodity Prices of the Basket Components and the value of the Notes in varying and potentially inconsistent ways. As a result of these or other factors, the Commodity Prices of the Basket Components may be, and recently have been, highly volatile.

|

|

♦

|

Changes in exchange methodology related to the Basket Components may adversely affect the value of the Notes prior to maturity.The prices of the Basket Components will be determined by reference to fixing prices, spot prices, or related futures contracts of the commodities represented by or

|

PS-8

|

|

included in the Basket Components, as determined by the applicable exchange. An exchange may from time to time change its rules or take extraordinary actions under its rules, which could adversely affect the prices of the applicable commodities or futures contracts, which could reduce the prices of the Basket Components and the value of the Notes.

|

|

♦

|

Legal and regulatory changes could adversely affect the return on and value of your Notes.The prices of the Basket Components could be adversely affected by new laws or regulations or by the reinterpretation of existing laws or regulations (including, without limitation, those related to taxes and duties on commodities and futures contracts) by one or more governments, courts, or other official bodies. Any such regulatory action could have an adverse effect on the prices of the Basket Components and your Notes.

|

|

♦

|

The Notes will not be regulated by the U.S. Commodity Futures Trading Commission (“CFTC”). Unlike an investment in the Notes, an investment in a collective investment vehicle that invests in futures contracts on behalf of its participants may be regulated as a commodity pool and its operator may be required to be registered with and regulated by the CFTC as a “commodity pool operator” (a “CPO”). Because the Notes will not be interests in a commodity pool, the Notes will not be regulated by the CFTC as a commodity pool, neither we nor the Guarantor will be registered with the CFTC as a CPO, and you will not benefit from the CFTC’s or any non-U.S. regulatory authority’s regulatory protections afforded to persons who trade in futures contracts or who invest in regulated commodity pools.

|

|

♦

|

The Notes provide exposure to futures contracts on corn, Brent crude oil, natural gas, soybeans, wheat and WTI light sweet crude oil and not direct exposure to such commodities. The price of a futures contract reflects the expected value of the underlying commodity upon delivery in the future, whereas the spot price of the commodity reflects the immediate delivery value of that commodity. A variety of factors can lead to a disparity between the expected future price of a commodity and its spot price at a given point in time, such as the cost of storing the commodity for the term of the futures contract, interest charges incurred to finance the purchase of the commodity and expectations concerning supply and demand for the commodity. The price movement of a futures contract is typically correlated with the movements of the spot price of the reference commodity, but the correlation is generally imperfect and price movements of the spot price may not be reflected in the futures market (and vice versa).

|

In addition, the difference between a futures price and a spot price is typically greater the longer the remaining term of the futures contract (in other words, futures prices converge toward spot prices as the expiration of the futures contract nears). As a result, the price of each of the futures contracts on corn, Brent crude oil, natural gas, soybeans, wheat and WTI light sweet crude oil on the Valuation Date will be influenced in part by how much time remains to expiration of the futures on the Valuation Date. Had the Valuation Date occurred with a different length of time remaining to expiration of the futures, your return on the Notes might have been more favorable.

|

♦

|

Futures contracts on Brent crude oil are the benchmark crude oil contracts in European and Asian markets and may be affected by economic conditions in Europe and Asia. Because futures contracts on Brent crude oil are the benchmark crude oil contracts in European and Asian markets, they will be affected by economic conditions in Europe and Asia. A decline in economic activity in Europe or Asia could result in decreased demand for Brent crude oil and for futures contracts on Brent crude oil, which could adversely affect the commodity price of Brent crude oil futures and, therefore, the value of the Notes.

|

|

♦

|

There are risks relating to the commodity price of Brent crude oil futures being determined by ICE Futures Europe. The price of Brent crude oil futures will be determined by reference to the official settlement price per barrel on ICE Futures Europe of the first nearby month futures contract for Brent crude oil (or, in some circumstances, the second nearby month futures contract for Brent crude oil), stated in U.S. dollars, as made public by ICE Futures Europe and displayed on the applicable Bloomberg page. Investments in Notes linked to the value of commodity futures contracts that are traded on non-U.S. exchanges, such as ICE Futures Europe, involve risks associated with the markets in foreign countries, including risks of volatility in those markets and governmental intervention in those markets.

|

|

♦

|

A decision by ICE Futures Europe to increase margin requirements for Brent crude oil futures contracts may affect the commodity price of such basket commodity. If ICE Futures Europe increases the amount of collateral required to be posted to hold positions in the futures contracts on Brent crude oil (i.e., the margin requirements), market participants who are unwilling or unable to post additional collateral may liquidate their positions, which may cause the price to decline significantly.

|

|

♦

|

On the Valuation Date, the price of each of special high-grade zinc and Grade A copper will be determined by reference to its official cash settlement price as determined by the London Metal Exchange (“LME”), and there are certain risks relating to the commodity price being determined by the LME. The price of each of special high-grade zinc and Grade A copper will be determined by reference to its official cash settlement price as determined by the LME. The LME is a principals’ market that operates in a manner more closely analogous to the over-the-counter physical commodity markets than regulated futures markets. In a declining market, therefore, it is possible that prices would continue to decline without limitation within a trading day or over a period of trading days. In addition, investments in notes linked to the value of commodities that are traded on non-U.S. exchanges, such as LME, involve risks associated with the markets in foreign countries, including risks of volatility in those markets and governmental intervention in those markets.

|

|

♦

|

If a Commodity Hedging Disruption Event occurs during the term of the Notes, we may redeem the notes early. See “Additional Terms of the Notes—Commodity Hedging Disruption Event” in this pricing supplement for information about the events that may constitute a Commodity Hedging Disruption Event. If a Commodity Hedging Disruption Event occurs, we may redeem the Notes prior to the Maturity Date for an amount equal to the Early Redemption Amount determined as of the Early Redemption Notice Date. If we redeem the Notes early, the amount you receive may be less than the amount you would have received if you had been able to hold the notes to maturity

|

|

♦

|

The market price of each Basket Component will affect the value of the Notes — The value of the Notes will depend on the price of each Basket Component. Specific factors related to each Basket Component that may affect its price are:

|

PS-9

|

♦

|

Corn. The price of corn futures is primarily affected by the global demand for, and supply of, corn. The demand for corn is in part linked to the development of industrial and energy uses for corn. This includes the use of corn in the production of ethanol. The demand for corn is also affected by the production and profitability of the pork and poultry sectors, which use corn for feed. Negative developments in those industries may lessen the demand for corn. For example, if avian flu were to have a negative effect on world poultry markets, the demand for corn might decrease. The supply of corn is dependent on many factors including weather patterns, government regulation, the price of fuel and fertilizers and the current and previous price of corn. The United States is the world’s largest supplier of corn, followed by China and Brazil. The supply of corn is particularly sensitive to weather patterns in the United States and China. In addition, technological advances could lead to increases in worldwide production of corn and corresponding decreases in the price of corn. Furthermore, any changes in the policies or regulations of the Chicago Board of Trade (the “CBOT”) or other regulators could also affect the price of corn.

|

|

♦

|

Brent crude oil & WTI light sweet crude oil. Brent crude oil futures and WTI light sweet crude oil futures are referred to for purposes of this paragraph as “crude oil futures.” The price of crude oil futures is primarily affected by the demand for and supply of crude oil, but is also influenced significantly from time to time by speculative actions and by currency exchange rates. Crude oil prices are generally highly volatile and subject to dislocation. Demand for refined petroleum products by consumers, as well as the agricultural, manufacturing and transportation industries, affects the price of crude oil. Crude oil’s end-use as a refined product is often as transport fuel, industrial fuel and in-home heating fuel. Potential for substitution in most areas exists. Because the precursors of demand for petroleum products are linked to economic activity, demand will tend to reflect economic conditions. Demand is also influenced by government regulations, such as environmental or consumption policies. In addition to general economic activity and demand, prices for crude oil are affected by political events, labor activity and, in particular, direct government intervention (such as embargos) or supply disruptions in major oil-producing regions of the world. Such events tend to affect oil prices worldwide, regardless of the location of the event. Supply for crude oil may increase or decrease depending on many factors. These include production decisions by OPEC and other crude oil producers. Crude oil prices are determined with significant influence by OPEC. OPEC has the potential to influence oil prices worldwide because its members possess a significant portion of the world’s oil supply. In the event of sudden disruptions in the supplies of oil, such as those caused by war, natural events, accidents or acts of terrorism, prices of oil futures contracts could become extremely volatile and unpredictable. Also, sudden and dramatic changes in the futures market may occur, for example, upon a cessation of hostilities that may exist in countries producing oil, the introduction of new or previously withheld supplies into the market or the introduction of substitute products or commodities. Crude oil prices may also be affected by short-term changes in supply and demand because of trading activities in the oil market and seasonality (e.g., weather conditions such as hurricanes).

|

|

♦

|

Special high-grade zinc. The spot price of zinc is primarily affected by the global demand for and supply of special high-grade zinc, but is also influenced significantly from time to time by speculative actions and by currency exchange rates. Demand for zinc is significantly influenced by the level of global industrial economic activity. The galvanized steel industrial sector is particularly important to demand for zinc given that the use of zinc in the manufacture of galvanized steel accounts for a significant percentage of worldwide zinc demand. The galvanized steel sector is in turn heavily dependent on the automobile and construction sectors. Growth in the production of galvanized steel will drive zinc demand. An additional, but highly volatile, component of demand is adjustments to inventory in response to changes in economic activity and/or pricing levels. The supply of zinc concentrate (the raw material) is dominated by Australia, North America and Latin America. The supply of zinc is also affected by current and previous price levels, which will influence investment decisions in new mines and smelters.

|

|

♦

|

Natural gas. The price of natural gas futures is primarily affected by the global demand for, and supply of, natural gas. Natural gas is used primarily for residential and commercial heating and in the production of electricity. Natural gas has also become an increasingly popular source of energy in the United States, both for consumers and industry. However, because natural gas can be used as a substitute for coal and oil in certain circumstances, the price of coal and oil influence the price of natural gas. The level of global industrial activity influences the demand for natural gas. The demand for natural gas has traditionally been cyclical, with higher demand during the winter months and lower demand during relatively warmer summer months. Seasonal temperatures in countries throughout the world can also heavily influence the demand for natural gas. The world’s supply of natural gas is concentrated in the former Soviet Union, the Middle East, Europe and Africa. In general, the supply of natural gas is based on competitive market forces. Inadequate supply at any one time leads to price increases, which signal to production companies the need to increase the supply of natural gas to the market. The ability of production companies to supply natural gas, however, is dependent on a number of factors. Factors that affect the short term supply of natural gas include the availability of skilled workers and equipment, permitting and well development, as well as weather and delivery disruptions (e.g., hurricanes, labor strikes and wars). In addition, production companies face more general barriers to their ability to increase the supply of natural gas, including access to land, the expansion of pipelines and the financial environment. These factors, which are not exhaustive, are interrelated and can have complex and unpredictable effects on the supply for, and the price of, natural gas.

|

|

♦

|

Soybeans. The price of soybeans futures is primarily affected by the global demand for, and supply of, soybeans, but is also influenced significantly from time to time by speculative actions and by currency exchange rates. The demand for soybeans is in part linked to the development of industrial and energy uses for soybeans. This includes the use of soybeans in the production of biodiesels. The supply of soybeans is dependent on many factors including weather patterns, government regulation, the price of fuel and fertilizers and the current and previous price of soybeans. The United States is the world’s largest supplier of soybeans, followed by Brazil. The supply of soybeans is particularly sensitive to weather patterns in the United States and Brazil. In addition, technological advances could lead to increases in worldwide production of soybeans and corresponding decreases in the price of

|

PS-10

|

|

soybeans. Furthermore, any changes in the policies or regulations of the CBOT or other regulators could also affect the price of soybeans futures.

|

|

♦

|

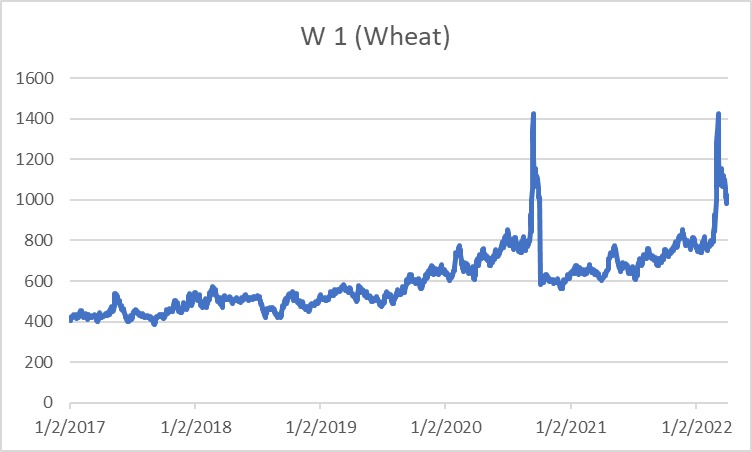

Wheat. The price of wheat futures is primarily affected by the global demand for and supply of wheat, but is also influenced significantly from time to time by speculative actions and by currency exchange rates. Wheat prices are primarily affected by weather and crop growing conditions generally and the global demand for and supply of grain, which are driven by global grain production, population growth and economic activity. Demand for wheat is in part linked to the development of agricultural, industrial and energy uses for wheat including the use of wheat for the production of animal feed and bioethanol, which may have a major impact on worldwide demand for wheat. In addition, prices for wheat are affected by governmental and intergovernmental programs and policies regarding trade, agriculture, and energy and, more generally, regarding fiscal and monetary issues. Wheat prices may also be influenced by or dependent on retail prices, social trends, lifestyle changes and market power. Substitution of other commodities for wheat could also impact the price of wheat. The supply of wheat is particularly sensitive to weather patterns such as floods, drought and freezing conditions, planting decisions, the price of fuel, seeds and fertilizers and the current and previous price of wheat. In addition, technological advances and scientific developments could lead to increases in worldwide production of wheat and corresponding decreases in the price of wheat. Extrinsic factors affecting wheat prices include natural disasters, pestilence, wars and political and civil upheavals. China, India and the United States are the three largest suppliers of wheat crops.

|

|

♦

|

Grade A Copper. The spot price of copper is primarily affected by the global demand for and supply of copper, but is also influenced significantly from time to time by speculative actions and by currency exchange rates. Demand for copper is significantly influenced by the level of global industrial economic activity. Industrial sectors which are particularly important to demand for copper include the electrical and construction sectors. There are substitutes for copper in various applications. Their availability and price will also affect demand for copper. Apart from the United States, Canada and Australia, the majority of copper concentrate supply (the raw material) comes from outside the Organization for Economic Cooperation and Development countries. The supply of copper is also affected by current and previous price prices, which will influence investment decisions in new smelters.

|

It is not possible to predict the aggregate effect of all or any combination of these factors on the prices of the Basket Components and, therefore, the value of the Notes.

Tax-related Risks

|

♦

|

The U.S. federal income tax consequences of an investment in the Notes are uncertain, and may be adverse to a holder of the Notes. No statutory, judicial, or administrative authority directly addresses the characterization of the Notes or securities similar to the Notes for U.S. federal income tax purposes. As a result, significant aspects of the U.S. federal income tax consequences of an investment in the Notes are not certain. We intend to treat the Notes as debt instruments for U.S. federal income tax purposes. Accordingly, you should consider the tax consequences of investing in the Notes, aspects of which are uncertain. See the section entitled “U.S. Federal Income Tax Summary.”

|

|

♦

|

You may be required to include income on the Notes over their term, even though you will not receive any payments until maturity. The Notes will be considered to be issued with original issue discount. You will be required to include income on the Notes over their term based upon a comparable yield, even though you will not receive any payments until maturity. You are urged to review the section entitled “U.S. Federal Income Tax Summary” and consult your own tax advisor.

|

You are urged to consult with your own tax advisor regarding all aspects of the U.S. federal income tax consequences of investing in the Notes.

PS-11

Hypothetical terms only. Actual terms may vary. See the cover page for actual offering terms.

The examples below illustrate the hypothetical Payment at Maturity for a $1,000.00 Stated Principal Amount Note for a hypothetical range of Basket Returns for the Basket with the following assumptions* (the actual terms of the Notes will be determined on the Trade Date; amounts may have been rounded for ease of reference and do not take into account any tax consequences from investing in the Notes):

|

♦

|

Stated Principal Amount: $1,000

|

|

♦

|

Initial Basket Value: 100.00

|

* Any payment on the Notes is subject to issuer and guarantor credit risk.

|

Final Basket Value

|

Basket Return

|

Payment at Maturity

|

Return on the Notes

|

|

160.00

|

60.00%

|

$1,600.00

|

60.00%

|

|

150.00

|

50.00%

|

$1,500.00

|

50.00%

|

|

140.00

|

40.00%

|

$1,400.00

|

40.00%

|

|

130.00

|

30.00%

|

$1,300.00

|

30.00%

|

|

120.00

|

20.00%

|

$1,200.00

|

20.00%

|

|

105.00

|

5.00%

|

$1,050.00

|

5.00%

|

|

102.00

|

2.00%

|

$1,020.00

|

2.00%

|

|

100.00(1)

|

0.00%

|

$1,000.00

|

0.00%

|

|

90.00

|

-10.00%

|

$1,000.00

|

0.00%

|

|

80.00

|

-20.00%

|

$1,000.00

|

0.00%

|

|

75.00

|

-25.00%

|

$1,000.00

|

0.00%

|

|

60.00

|

-40.00%

|

$1,000.00

|

0.00%

|

|

50.00

|

-50.00%

|

$1,000.00

|

0.00%

|

|

0.00

|

-100.00%

|

$1,000.00

|

0.00%

|

(1)

This is the Initial Basket Value.

|

Example 1 —The Final Basket Value of 150.00 is greater than the Initial Basket Value of 100.00, resulting in aBasket Return of 50.00%.

Since the Basket Return is positive,we will repay the Stated Principal Amount of the Notes at maturity plus a return equal to the Basket Return, calculated as follows:

$1,000.00 × (1 + 50.00%) = $1,500.00

Example 2 — The Final Basket Value of 90.00 is less than the Initial Basket Value of 100.00.

Since the Basket Return is negative, we will repay the Stated Principal Amount of the Notes at maturity.

PS-12

|

The Basket and the Basket Components

|

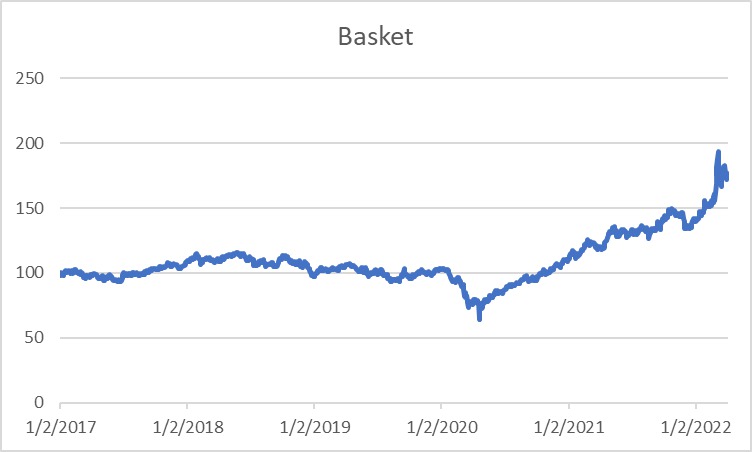

Because the Basket exists solely for purposes of these Notes, historical information on the performance of the Basket does not exist for dates prior to the Trade Date for these Notes. The graph below sets forth the hypothetical historical daily levels of the Basket for the period from January 2, 2017 to April 4, 2022, assuming that the Basket was created on January 2, 2017 with the same Basket Components and corresponding weights in the Basket and with an Initial Basket Value of 100 on that date. The hypothetical performance of the Basket is based on the actual Commodity Prices of the Basket Components on the applicable dates. We obtained these Commodity Prices from Bloomberg L.P., without independent verification. Any historical trend in the value of the Basket during the period shown below is not an indication of the performance of the Basket during the term of the Notes.

All disclosures contained in this pricing supplement regarding the Basket Components, including, without limitation, their make-up, method of calculation, and changes in their components, have been derived from publicly available sources. The information reflects the policies of, and is subject to change by, the relevant exchanges. The consequences of any relevant exchange discontinuing publication of any Basket Component are discussed in “Description of the Notes — Discontinuance of a Market Measure” in the accompanying product supplement. None of us, the Guarantor, the calculation agent, or BofAS accepts any responsibility for the calculation, maintenance or publication of the Basket Components or any successor basket component.

None of us, the Guarantor, the Selling Agents or any of our or their respective affiliates makes any representation to you as to the future performance of any Basket Component.

You should make your own investigation into the Basket Components.

Corn Futures

Corn futures contracts trade on the Chicago Board of Trade (“CBOT”). The Commodity Price of corn futures on any day is the settlement price per bushel of deliverable grade corn on the CBOT of the first nearby futures contract, stated in U.S. cents, as made public by the CBOT and displayed on Bloomberg Page “C 1 <CMDTY>” on that day; provided that such day is two business days prior to both the first notice date and the last trade date (all as specified by the CBOT); after any of these dates, the settlement price of the second nearby futures contract is referenced.

A corn futures contract trades on the CBOT in 5,000 bushel increments, and delivery is on the No. 2 yellow corn at par with substitutions deliverable at various differentials established by the exchange. Contract months are March, May, July, September and December. The CBOT determines an official settlement price for corn futures contracts on each trading day as of 2:15 p.m., New York time. The daily settlement price of the nearest-to-expiration corn futures contract is the volume-weighted average price of all trades in that contract that are executed between 2:14:00 and 2:15:00 p.m., New York City time. The daily settlement price of the next expiring corn futures contract is the price implied from the volume-weighted average price of all trades executed in the spread between the nearest-to-expiration contract and the next expiring contract between 2:14:00 and 2:15:00 p.m., New York City time, using the daily settlement price of the nearest-to-expiration contract as the anchor price and adding to it the spread.

Historical Performance of Corn Futures

The following graph sets forth the daily historical performance of corn futures in the period from January 2, 2017 through April 4, 2022. We obtained this historical data from Bloomberg L.P. We have not independently verified the accuracy or completeness of the information obtained from Bloomberg L.P. On April 4, 2022 the Commodity Price of corn futures was $750.50.

PS-13

This historical data on corn futures is not necessarily indicative of the future performance of corn futures or what the value of the Notes may be. Any historical upward or downward trend in the price of corn futures during any period set forth above is not an indication that the price of corn futures is more or less likely to increase or decrease at any time over the term of the Notes.

Before investing in the Notes, you should consult publicly available sources for the prices of corn futures.

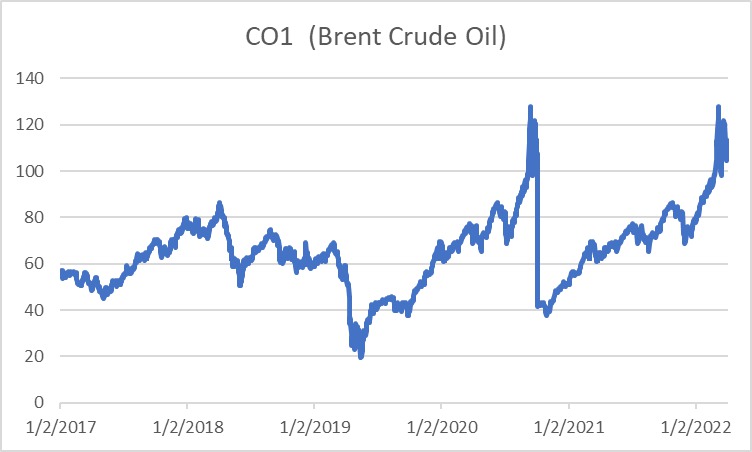

Brent Crude Oil Futures

Brent crude oil futures contracts trade on ICE Futures Europe (the “ICE”). The Commodity Price of Brent crude oil futures on any day is the settlement price of per metric barrel of deliverable grade Brent blend crude oil on the ICE of the first nearby futures contract stated in U.S. Dollars as made public by the ICE and displayed on Bloomberg Page “CO1 <CMDTY>” on that day.

The Brent crude oil futures contract represents the right to receive a future delivery of 1,000 net barrels of Brent blend crude oil per unit and is quoted at a price that represents one barrel of Brent blend crude oil. The delivery point of crude oil underlying the contract is Sullom Voe, Scotland. The Brent crude oil futures contract is a deliverable contract based on an Exchange of Futures for Physical (“EFP”) delivery mechanism with an option to cash settle. This mechanism enables companies to take delivery of physical crude supplies through EFP or, alternatively and more commonly, open positions that can be cash settled at expiration against a physical price index. Trading in a given futures contract will cease at the end of the designated settlement period on the last business day of the second month preceding the relevant contract month (e.g., the futures contract that is settled in March will cease trading on the last business day of January). The official settlement price is determined by the ICE based on the weighted average price of trades during a two minute settlement period from 19:28:00, London time.

Historical Performance of Brent crude oil futures

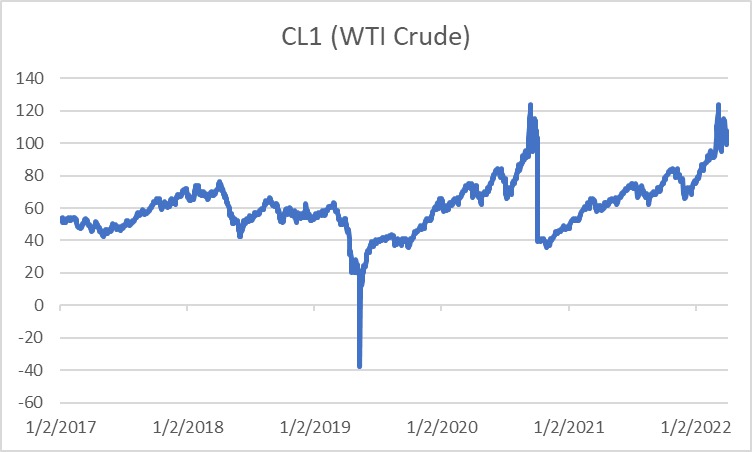

The following graph sets forth the daily historical performance of Brent crude oil futures in the period from January 2, 2017 through April 4, 2022. We obtained this historical data from Bloomberg L.P. We have not independently verified the accuracy or completeness of the information obtained from Bloomberg L.P. On April 4, 2022 the Commodity Price of Brent crude oil futures was $107.53.

PS-14

This historical data on Brent crude oil futures is not necessarily indicative of the future performance of Brent crude oil futures or what the value of the Notes may be. Any historical upward or downward trend in the price of Brent crude oil futures during any period set forth above is not an indication that the price of Brent crude oil futures is more or less likely to increase or decrease at any time over the term of the Notes.

Before investing in the Notes, you should consult publicly available sources for the prices of Brent crude oil futures.

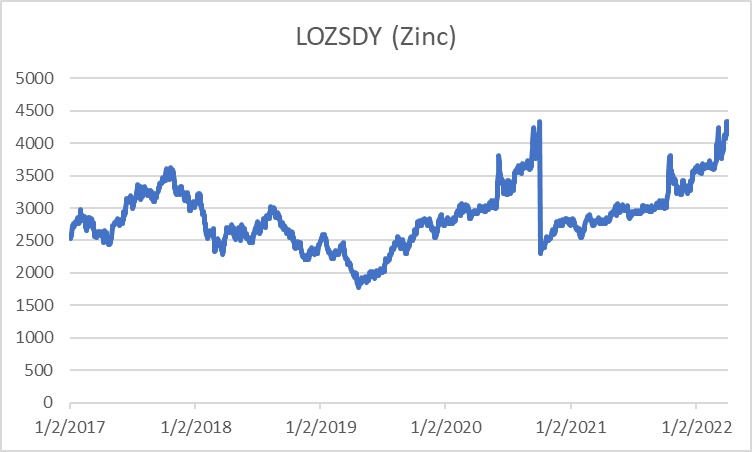

Special High-Grade Zinc

Special high-grade zinc trades on the London Metal Exchange (the “LME”). The Commodity Price of special high-grade zinc on any day is the settlement price of per tonne of special high grade zinc on the LME deliverable in two days, stated in U.S. dollars, as determined by the LME and displayed on Bloomberg Page “LOZSDY <CMDTY>” on that day.

Historical Performance of special high grade zinc

The following graph sets forth the daily historical performance of special high grade zinc in the period from January 2, 2017 through April 4, 2022. We obtained this historical data from Bloomberg L.P. We have not independently verified the accuracy or completeness of the information obtained from Bloomberg L.P. On April 4, 2022 the Commodity Price of special high grade zinc was $4,332.00.

This historical data on special high grade zinc is not necessarily indicative of the future performance of special high grade zinc or what the value of the Notes may be. Any historical upward or downward trend in the price of special high grade zinc during any period set forth above is not an indication that the price of special high grade zinc is more or less likely to increase or decrease at any time over the term of the Notes.

Before investing in the Notes, you should consult publicly available sources for the prices of special high grade zinc.

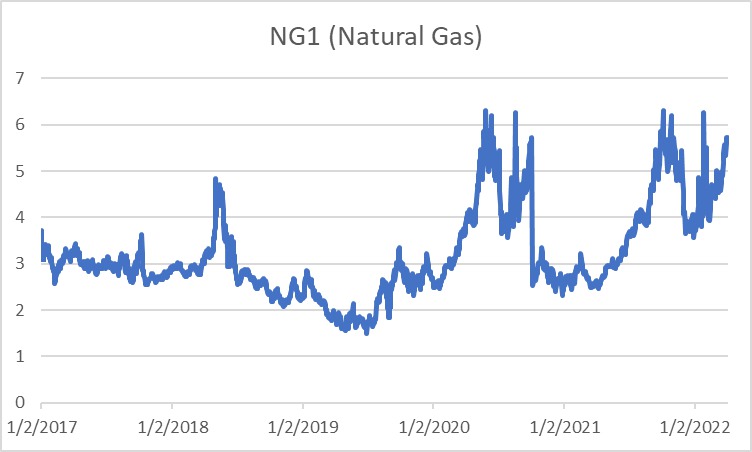

Natural Gas Futures

Natural gas futures contracts trade on the New York Mercantile Exchange (the “NYMEX”). The Commodity Price of natural gas futures on any day is the settlement price of per MMBTU of deliverable grade natural gas on the NYMEX of the first nearby futures contract stated in U.S. dollars as made public by the NYMEX and displayed on Bloomberg Page “NG1 <CMDTY>” on that day.

A natural gas futures contract traded on the NYMEX is an agreement to buy or sell 10,000 million British thermal units (as defined under the NYMEX’s rules) within a specified expiration month in the future at a price specified at the time of entering into the contract. The price of the natural gas contract is based on delivery at the Henry Hub, which refers to piping and related facilities owned and/or leased by Sabine Pipe Line LLC near Erath, Louisiana. Natural gas trades in contracts for 10,000 million British thermal units and must meet the specifications set forth in the FERC-approved tariff of Sabine Pipe Line LLC as then in effect at the time of delivery.

The NYMEX determines an official settlement price for natural gas futures contracts on each trading day as of 2:30 p.m., New York City time. The daily settlement price of the nearest-to-expiration NYMEX natural gas futures contract is the volume-weighted average price of all trades in that contract that are executed between 2:28:00 and 2:30:00 p.m., New York City time. The daily settlement price of the next expiring NYMEX natural gas futures contract is the price implied from the volume-weighted average price of all trades executed in the spread between the nearest-to-expiration contract and the next expiring contract between 2:28:00 and 2:30:00 p.m., New York City time, using the daily settlement price of the nearest-to-expiration contract as the anchor price and adding to it the spread.

Historical Performance of natural gas futures

The following graph sets forth the daily historical performance of natural gas futures in the period from January 2, 2017 through April 4, 2022. We obtained this historical data from Bloomberg L.P. We have not independently verified the accuracy or completeness of the information obtained from Bloomberg L.P. On April 4, 2022 the Commodity Price of natural gas futures was $5.712.

PS-15

This historical data on natural gas futures is not necessarily indicative of the future performance of natural gas futures or what the value of the Notes may be. Any historical upward or downward trend in the price of natural gas futures during any period set forth above is not an indication that the price of natural gas futures is more or less likely to increase or decrease at any time over the term of the Notes.

Before investing in the Notes, you should consult publicly available sources for the prices of natural gas futures.

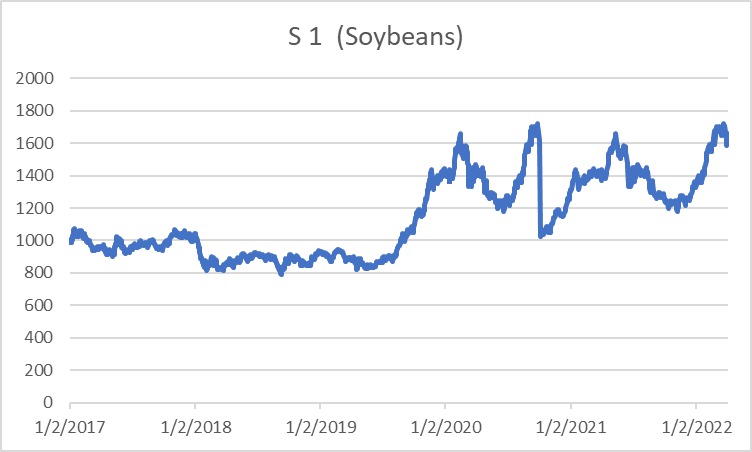

Soybeans Futures

Soybeans futures contracts trade on the CBOT. The Commodity Price of soybeans futures on any day is the settlement price per bushel of deliverable grade soybeans on the CBOT of the first nearby futures contract, stated in U.S. cents, as made public by the CBOT and displayed on Bloomberg Page “S 1 <CMDTY> CT” on that day; provided that such day is two business days prior to both the first notice date and the last trade date (all as specified by the CBOT); after any of these dates, the settlement price of the second nearby futures contract is referenced.

A soybean futures contract trades on the CBOT in 5,000 bushel increments, and delivery is on the No. 2 yellow soybean at par with substitutions deliverable at various differentials established by the exchange. Contract months are January, March, May, July, August, September and November. The CBOT determines an official settlement price for soybean futures contracts on each trading day as of 2:15 p.m., New York time. The daily settlement price of the nearest-to-expiration soybean futures contract is the volume-weighted average price of all trades in that contract that are executed between 2:14:00 and 2:15:00 p.m., New York City time. The daily settlement price of the next expiring soybeans futures contract is the price implied from the volume-weighted average price of all trades executed in the spread between the nearest-to-expiration contract and the next expiring contract between 2:14:00 and 2:15:00 p.m., New York City time, using the daily settlement price of the nearest-to-expiration contract as the anchor price and adding to it the spread.

Historical Performance of soybeans futures