Preliminary Pricing Supplement

Subject To Completion, dated September 23, 2022

(To Prospectus dated December 31, 2019,

Series A Prospectus Supplement dated December 31, 2019 and

Product Supplement No. WF-1 dated September 9, 2022)

|

Filed Pursuant to Rule 424(b)(2) Registration Nos. 333-234425 and 333-234425 -01 This pricing supplement, which is not complete and may be changed, relates to an effective Registration Statement under the Securities Act of 1933. This pricing supplement and the accompanying product supplement, prospectus supplement and prospectus are not an offer to sell these Securities in any country or jurisdiction where such an offer would not be permitted. |

|

Preliminary Pricing Supplement Subject To Completion, dated September 23, 2022 (To Prospectus dated December 31, 2019, Series A Prospectus Supplement dated December 31, 2019 and Product Supplement No. WF-1 dated September 9, 2022) |

|

|

BofA Finance LLC Medium-Term Notes, Series A Fully and Unconditionally Guaranteed by Bank of America Corporation |

||||

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025 |

||||

|

■ Linked to the Lowest Performing of the S&P 500® Linked to the Lowest Performing of the SPDR® S&P® Regional Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® (each referred to as an “Underlying”) ■ Unlike ordinary debt securities, the Securities do not provide for fixed payments of interest, do not repay a fixed amount of principal on the Maturity Date and are subject to potential automatic call prior to the Maturity Date upon the terms described below. Whether the Securities pay a Contingent Coupon, whether the Securities are automatically called prior to the Maturity Date and, if they are not automatically called, whether you receive the principal amount of your Securities on the Maturity Date will depend, in each case, on the closing value of the Lowest Performing Underlying on the relevant Calculation Day. The Lowest Performing Underlying on any Calculation Day is the Underlying that has the lowest closing value on that Calculation Day as a percentage of its Starting Value ■ Contingent Coupon. The Securities will pay a Contingent Coupon on a quarterly basis until the earlier of the Maturity Date or automatic call if, and only if, the closing value of the Lowest Performing Underlying on the Calculation Day for that quarter is greater than or equal to its Coupon Barrier. However, if the closing value of the Lowest Performing Underlying on a Calculation Day is less than its Coupon Barrier, you will not receive any Contingent Coupon for the relevant quarter. If the closing value of the Lowest Performing Underlying is less than its Coupon Barrier on every Calculation Day, you will not receive any Contingent Coupons throughout the entire term of the Securities. The Coupon Barrier for each Underlying is equal to 70% of its Starting Value. The Contingent Coupon Rate will be determined on the Pricing Date and will be at least 11.25% per annum ■ Automatic Call. If the closing value of the Lowest Performing Underlying on any of the quarterly Calculation Days from March 2023 to June 2025, inclusive, is greater than or equal to its Starting Value, the Securities will be automatically called for the principal amount plus a final Contingent Coupon Payment ■ Potential Loss of Principal. If the Securities are not automatically called prior to the Maturity Date, you will receive the principal amount on the Maturity Date if, and only if, the closing value of the Lowest Performing Underlying on the Final Calculation Day is greater than or equal to its Threshold Value. If the closing value of the Lowest Performing Underlying on the Final Calculation Day is less than its Threshold Value, you will lose more than 30%, and possibly all, of the principal amount of your Securities. The Threshold Value for each Underlying is equal to 70% of its Starting Value ■ If the Securities are not automatically called prior to the Maturity Date, you will have full downside exposure to the Lowest Performing Underlying from its Starting Value if its closing value on the Final Calculation Day is less than its Threshold Value, but you will not participate in any appreciation of any Underlying and will not receive any dividends on shares of the Fund or the securities held by or included in any Underlying ■ Your return on the Securities will depend solely on the performance of the Underlying that is the Lowest Performing Underlying on each Calculation Day. You will not benefit in any way from the performance of the better performing Underlyings. Therefore, you will be adversely affected if any Underlying performs poorly, even if the other Underlyings perform favorably ■ All payments on the Securities are subject to the credit risk of BofA Finance LLC (“BofA Finance”), as issuer of the Securities, and Bank of America Corporation (“BAC” or the “Guarantor”), as guarantor of the Securities ■ Securities will not be listed on any securities exchange |

||||

|

|

Public offering price

|

Underwriting Discount(1)(2)

|

Proceeds, before expenses, to BofA Finance

|

|

Per Security

|

$1,000.00

|

$21.25

|

$978.75

|

|

Total

|

|

|

|

|

(1)

|

Wells Fargo Securities, LLC and BofA Securities, Inc. are the selling agents for the distribution of the Securities and are acting as principal. See “Terms of the Securities—Selling Agents” in this pricing supplement for further information.

|

|

(2)

|

In addition, in respect of certain Securities sold in this offering, BofA Securities, Inc. or its affiliates may pay a fee of up to $1.00 per Security to selected securities dealers in consideration for marketing and other services in connection with the distribution of the Securities to other securities dealers.

|

|

Wells Fargo Securities

|

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

| Terms of the Securities |

| Issuer: |

BofA Finance LLC.

|

|||||||||

|

Guarantor:

|

BAC.

|

|||||||||

|

Underlyings:

|

The SPDR® S&P® Regional Banking ETF (Bloomberg symbol: “KRE”), the Russell 2000® Index (Bloomberg symbol: “RTY”) and the Nasdaq-100 Index® (Bloomberg symbol: “NDX”), each a price return index. The SPDR® S&P® Regional Banking ETF is sometimes referred to herein as the “Fund.”

The Russell 2000® Index and the Nasdaq-100 Index® are sometimes collectively referred to herein as

the “Indices” and individually as an “Index.”

|

|||||||||

|

Pricing Date*:

|

September 29, 2022.

|

|||||||||

|

Issue Date*:

|

October 4, 2022.

|

|||||||||

|

Maturity Date*:

|

September 29, 2025, subject to postponement as described below in “—Market Disruption Events and Postponement Provisions”. The Securities are not subject to repayment at the option of any holder of the Securities prior to the Maturity Date.

|

|||||||||

|

Denominations:

|

$1,000 and any integral multiple of $1,000. References in this pricing supplement to a “Security” are to a Security with a principal amount of $1,000.

|

|||||||||

|

Contingent Coupon Payment:

|

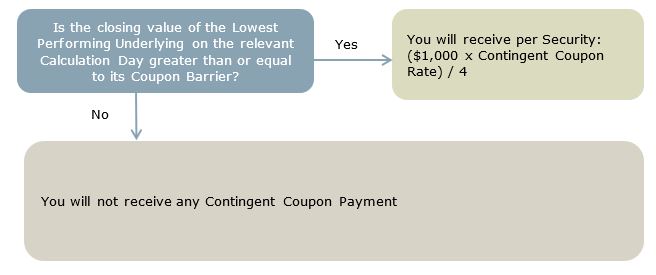

On each Contingent Coupon Payment Date, you will receive a Contingent Coupon Payment at a per annum rate equal to the Contingent Coupon Rate if, and only if, the closing value of the Lowest Performing Underlying on the related Calculation Day is greater than or equal to its Coupon Barrier. Each “Contingent Coupon Payment,” if any, will be calculated per Security as follows: ($1,000 × Contingent Coupon Rate)/4. Any Contingent Coupon Payment will be rounded to the nearest cent, with one-half cent rounded upward.

If the closing value of the Lowest Performing Underlying on any Calculation Day is less than its Coupon Barrier, you will not receive any Contingent Coupon Payment on the related Contingent Coupon Payment Date. If the closing value of the Lowest Performing Underlying is less than its Coupon Barrier on all Calculation Days, you will not receive any Contingent Coupon Payments over the term of the Securities.

|

|||||||||

|

Contingent Coupon Payment Dates:

|

Quarterly, on the third business day following each Calculation Day (as each such Calculation Day may be postponed pursuant to “—Market Disruption Events and Postponement Provisions” below, if applicable); provided that the Contingent Coupon Payment Date with respect to the Final Calculation Day will be the Maturity Date.

|

|||||||||

|

Contingent Coupon Rate:

|

The “Contingent Coupon Rate” will be determined on the Pricing Date and will be at least 11.25% per annum (equal to at least 2.8125% per quarter).

|

|||||||||

|

Automatic Call:

|

If the closing value of the Lowest Performing Underlying on any of the Calculation Days from March 2023 to June 2025, inclusive, is greater than or equal to its Starting Value, the Securities will be automatically called, and on the related Call Settlement Date you will be entitled to receive a cash payment per Security in U.S. dollars equal to the principal amount per Security plus a final Contingent Coupon Payment. The Securities will not be subject to automatic call until the second Calculation Day, which is approximately six months after the issue date.

If the Securities are automatically called, they will cease to be outstanding on the related Call Settlement Date and you will have no further rights under the Securities after such Call Settlement Date. You will not receive any notice from us if the Securities are automatically called.

|

|||||||||

|

Calculation Days*:

|

Quarterly, on the 24th day of each March, June, September and December, commencing December 2022 and ending June 2025, and the Final Calculation Day, each subject to postponement as described below under “—Market Disruption Events and Postponement Provisions.” We refer to September 24, 2025 as the “Final Calculation Day.”

|

|||||||||

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

| Call Settlement Date: |

Three business days after the applicable Calculation Day (as each such Calculation Day may be postponed pursuant to “—Market Disruption Events and Postponement Provisions” below, if applicable).

|

|||||||

|

Maturity Payment Amount:

|

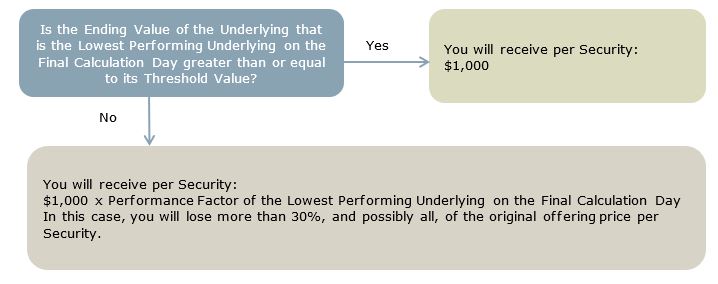

If the Securities are not automatically called prior to the Maturity Date, you will be entitled to receive on the Maturity Date a cash payment per Security in U.S. dollars equal to the Maturity Payment Amount (in addition to the final Contingent Coupon Payment, if any). The “Maturity Payment Amount” per Security will equal:

• if the Ending Value of the Lowest Performing Underlying on the Final Calculation Day is greater than or equal to its Threshold Value:

$1,000; or • if the Ending Value of the Lowest Performing Underlying on the Final Calculation Day is less than its Threshold Value:

|

|||||||

| $1,000 × Performance Factor of the Lowest Performing Underlying on the Final Calculation Day | ||||||||

|

If the Securities are not automatically called prior to the Maturity Date and the Ending Value of the Lowest Performing Underlying on the Final Calculation Day is less than its Threshold Value, you will lose more than 30%, and possibly all, of the principal amount of your Securities on the Maturity Date.

Any return on the Securities will be limited to the sum of your Contingent Coupon Payments, if any. You will not participate in any appreciation of any Underlying, but you will have full downside exposure to decreases in the value of the Lowest Performing Underlying on the Final Calculation Day if the Ending Value of that Underlying is less than its Threshold Value.

|

||||||||

|

Lowest Performing Underlying:

|

For any Calculation Day, the “Lowest Performing Underlying” will be the Underlying with the lowest Performance Factor on that Calculation Day.

|

|||||||

|

Performance Factor:

|

With respect to an Underlying on any Calculation Day, its closing value on such Calculation Day divided by its Starting Value (expressed as a percentage).

|

|||||||

|

Closing Value:

|

With respect to each Underlying, closing value

has the meaning set forth under “Summary” in the accompanying product supplement.

|

|||||||

|

Starting Value:

|

With respect to the SPDR® S&P® Regional Banking ETF: $ , its closing value on the Pricing Date.

With respect to the Russell 2000® Index: , its closing value on the Pricing Date.

With respect to the Nasdaq-100 Index®: , its closing value on the Pricing Date.

|

|||||||

|

Ending Value:

|

With respect to each Underlying, its closing value on the Final Calculation Day.

|

|||||||

|

Coupon Barrier:

|

With respect to the SPDR® S&P® Regional Banking ETF: $ , which is equal to 70% of its Starting Value.

With respect to the Russell 2000® Index: , which is equal to 70% of its Starting Value.

With respect to the Nasdaq-100 Index®: , which is equal to 70% of its Starting Value.

|

|||||||

| Threshold Value: |

With respect to the SPDR® S&P® Regional Banking ETF: $ , which is equal to 70% of its Starting Value.

With respect to the Russell 2000® Index: , which is equal to 70% of its Starting Value.

With respect to the Nasdaq-100 Index®: , which is equal to 70% of its Starting Value.

|

|||||||

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

Market Disruption Events and Postponement Provisions:

|

Each Calculation Day is subject to postponement due to non-trading days and the occurrence of a market disruption event. In addition, the Maturity Date will be postponed if the Final Calculation Day is postponed and will be adjusted for non-business days. For more information regarding adjustments to the Calculation Days and the Maturity Date, see “General Terms of the Securities—Consequences of a Market Disruption Event; Postponement of a Calculation Day—Securities Linked to Multiple Market Measures” and “—Payment Dates” in the accompanying product supplement. For purposes of the accompanying product supplement, each Contingent Coupon Payment Date, each Call Settlement Date and the Maturity Date is a “payment date.” In addition, for information regarding the circumstances that may result in a market disruption event, see “General Terms of the Securities—Certain Terms for Securities Linked to an Index—Market Disruption Events” in the accompanying product supplement.

|

|||||||

|

Calculation Agent:

|

BofA Securities, Inc. (“BofAS”), an affiliate of BofA Finance.

|

|||||||

|

Selling Agents:

|

BofAS and Wells Fargo Securities, LLC (“WFS”).

Under our distribution agreement with BofAS, BofAS will purchase the Securities from us as principal at the public offering price indicated on the cover of this pricing supplement, less the indicated underwriting discount. BofAS will sell the Securities to WFS at the public offering price of the Securities less a concession of up to $21.25 per Security. WFS will provide dealers, which may include Wells Fargo Advisors (“WFA”) (the trade name of the retail brokerage business of WFS’s affiliates, Wells Fargo Clearing Services, LLC and Wells Fargo Advisors Financial Network, LLC), with a selling concession of up to $15.00 per Security. In addition to the concession allowed to WFA, WFS may pay up to $0.75 per Security to WFA as a distribution expense fee for each Security sold by WFA.

In addition, in respect of certain Securities sold in this offering, BofAS or its affiliates may pay a fee of up to $1.00 per Security to selected securities dealers in consideration for marketing and other services in connection with the distribution of the Securities to other securities dealers.

WFS has advised us that if it, WFA or any of their affiliates makes a secondary market in the Securities at any time up to the Issue Date or during the three-month period following the Issue Date, the secondary market price offered by it, WFA or any of their affiliates will be increased by an amount reflecting a portion of the costs associated with selling, structuring and hedging the Securities that are included in the public offering price of the Securities. Because this portion of the costs is not fully deducted upon issuance, WFS has advised us that any secondary market price it, WFA or any of their affiliates offers during this period will be higher than it otherwise would be outside of this period, as any secondary market price offered outside of this period will reflect the full deduction of the costs as described above. WFS has advised us that the amount of this increase in the secondary market price will decline steadily to zero over this three-month period. If you hold the Securities through an account at WFS, WFA or any of their affiliates, WFS has advised us that it expects that this increase will also be reflected in the value indicated for the Securities on your brokerage account statement. If you hold your Securities through an account at a broker-dealer other than WFS, WFA or any of their affiliates, the value of the Securities on your brokerage account statement may be different than if you held your Securities at WFS, WFA or any of their affiliates.

|

|||||||

|

Material Tax

Consequences:

|

For a discussion of the material U.S. federal income and estate tax consequences of the ownership and disposition of the Securities, see “U.S. Federal Income Tax Summary.”

|

|||||||

|

CUSIP:

|

09709V3Q7

|

|||||||

|

|

||||||||

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

Additional Information about BofA Finance, the Guarantor and the Securities

|

| • | Product Supplement No. WF-1 dated September 9, 2022: https://www.sec.gov/Archives/edgar/data/70858/000119312522241727/d401279d424b5.htm |

| • | Series A MTN prospectus supplement dated December 31, 2019 and prospectus dated December 31, 2019: https://www.sec.gov/Archives/edgar/data/70858/000119312519326462/d859470d424b3.htm |

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

Investor Considerations

|

| ■ | seek an investment with contingent quarterly coupon payments at a rate of 9.75% to 10.75% per annum (to be determined on the Pricing Date) until the earlier of the Maturity Date or automatic call, if, and only if, the closing level of the Lowest Performing Underlying on the applicable quarterly Observation Date is greater than or equal to 75% of its Starting Value; |

| ■ | understand that if the Ending Value of the Lowest Performing Underlying on the Final Calculation Day has declined by more than 30% from its Starting Value, they will be fully exposed to the decline in the Lowest Performing Underlying from its Starting Value and will lose more than 30%, and possibly all, of the principal amount of their Securities at maturity; |

| ■ | are willing to accept the risk that they may receive few or no Contingent Coupon Payments over the term of the Securities; |

| ■ | understand that the Securities may be automatically called prior to the Maturity Date and that the term of the Securities may be as short as approximately six months; |

| ■ | understand that the return on the Securities will depend solely on the performance of the Underlying that is the Lowest Performing Underlying on each Calculation Day and that they will not benefit in any way from the performance of the better performing Underlyings; |

| ■ | understand that the Securities are riskier than alternative investments linked to only one of the Underlyings or linked to a basket composed of each Underlying; |

| ■ | understand and are willing to accept the full downside risks of each Underlying; |

| ■ | are willing to forgo participation in any appreciation of any Underlying and dividends on shares of the Fund and on the securities held by or included in the Underlyings; and |

| ■ | are willing to hold the Securities until maturity. |

| ■ | seek a liquid investment or are unable or unwilling to hold the Securities to maturity; |

| ■ | require full payment of the principal amount of the Securities at maturity; |

| ■ | seek a security with a fixed term; |

| ■ | are unwilling to purchase Securities with an estimated value as of the Pricing Date that is lower than the public offering price and that may be as low as the lower estimated value set forth on the cover page; |

| ■ | are unwilling to accept the risk that the closing value of the Lowest Performing Underlying on the Final Calculation Day may decline by more than 30% from its Starting Value; |

| ■ | seek certainty of current income over the term of the Securities; |

| ■ | seek exposure to the upside performance of any or each Underlying; |

| ■ | seek exposure to a basket composed of each Underlying or a similar investment in which the overall return is based on a blend of the performances of the Underlyings, rather than solely on the Lowest Performing Underlying; |

| ■ | are unwilling to accept the risk of exposure to the Underlyings; |

| ■ | are unwilling to accept the credit risk of BofA Finance, as issuer, and BAC, as guarantor, to obtain exposure to the Underlyings generally, or to obtain exposure to the Underlyings that the Securities provide specifically; or |

| ■ | prefer the lower risk of conventional fixed income investments with comparable maturities issued by companies with comparable credit ratings. |

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

|

|

Determining Payment On A Contingent Coupon Payment Date and at Maturity

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

|

|

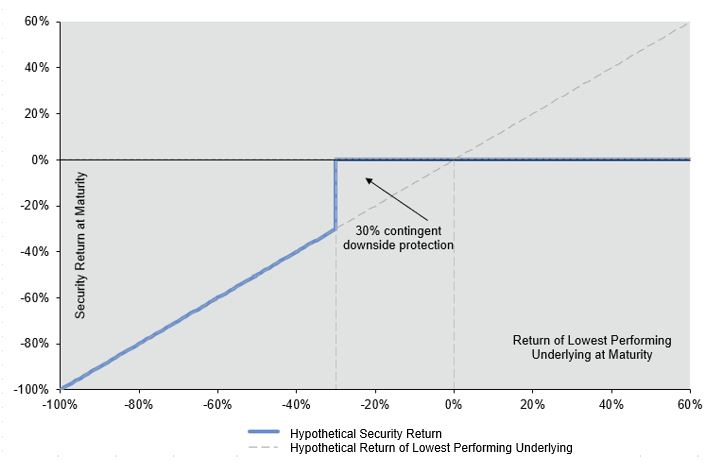

Hypothetical Payout Profile

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

|

|

Selected Risk Considerations

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

●

|

Changes that affect the Indices may adversely affect the value of the Securities and any payments on the Securities.

|

|

●

|

We and our affiliates have no affiliation with any index sponsor, fund sponsor or fund underlying index sponsor and have not independently verified their public disclosure of information.

|

|

●

|

Risks associated with the applicable fund underlying index, or underlying assets of a fund, will affect the value of that fund and hence the value of the Securities.

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

|

|

Hypothetical Returns

|

|

|

||

|

Hypothetical Performance Factor of Lowest Performing Underlying on Final Calculation Day

|

Hypothetical Maturity Payment Amount per Security

|

|

|

175.00%

|

$1,000.00

|

|

|

160.00%

|

$1,000.00

|

|

|

150.00%

|

$1,000.00

|

|

|

140.00%

|

$1,000.00

|

|

|

130.00%

|

$1,000.00

|

|

|

120.00%

|

$1,000.00

|

|

|

110.00%

|

$1,000.00

|

|

|

100.00%

|

$1,000.00

|

|

|

90.00%

|

$1,000.00

|

|

|

80.00%

|

$1,000.00

|

|

|

70.00%

|

$1,000.00

|

|

|

69.00%

|

$690.00

|

|

|

60.00%

|

$600.00

|

|

|

50.00%

|

$500.00

|

|

|

40.00%

|

$400.00

|

|

|

30.00%

|

$300.00

|

|

|

25.00%

|

$250.00

|

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

|

|

Hypothetical Contingent Coupon Payments

|

|

|

SPDR® S&P® Regional Banking ETF

|

Russell 2000® Index

|

Nasdaq-100 Index®

|

|

Hypothetical Starting Value:

|

100.00

|

100.00

|

100.00

|

|

Hypothetical closing value on relevant Calculation Day:

|

90.00

|

95.00

|

80.00

|

|

Hypothetical Coupon Barrier:

|

70.00

|

70.00

|

70.00

|

|

Performance Factor (closing value on Calculation Day divided by Starting Value):

|

90.00%

|

95.00%

|

80.00%

|

|

|

SPDR® S&P® Regional Banking ETF

|

Russell 2000® Index

|

Nasdaq-100 Index®

|

|

Hypothetical Starting Value:

|

100.00

|

100.00

|

100.00

|

|

Hypothetical closing value on relevant Calculation Day:

|

69.00

|

125.00

|

105.00

|

|

Hypothetical Coupon Barrier:

|

70.00

|

70.00

|

70.00

|

|

Performance Factor (closing value on Calculation Day divided by Starting Value):

|

69.00%

|

125.00%

|

105.00%

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

|

SPDR® S&P® Regional Banking ETF

|

Russell 2000® Index

|

Nasdaq-100 Index®

|

|

Hypothetical Starting Value:

|

100.00

|

100.00

|

100.00

|

|

Hypothetical closing value on relevant Calculation Day:

|

115.00

|

105.00

|

130.00

|

|

Hypothetical Coupon Barrier:

|

70.00

|

70.00

|

70.00

|

|

Performance Factor (closing value on Calculation Day divided by Starting Value):

|

115.00%

|

105.00%

|

130.00%

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

|

|

Hypothetical Payment at the Maturity Date

|

|

|

SPDR® S&P® Regional Banking ETF

|

Russell 2000® Index

|

Nasdaq-100 Index®

|

|

Hypothetical Starting Value:

|

100.00

|

100.00

|

100.00

|

|

Hypothetical Ending Value:

|

145.00

|

135.00

|

125.00

|

|

Hypothetical Coupon Barrier:

|

70.00

|

70.00

|

70.00

|

|

Hypothetical Threshold Value:

|

70.00

|

70.00

|

70.00

|

|

Performance Factor (Ending Value divided by Starting Value):

|

145.00%

|

135.00%

|

125.00%

|

|

|

SPDR® S&P® Regional Banking ETF

|

Russell 2000® Index

|

Nasdaq-100 Index®

|

|

Hypothetical Starting Value:

|

100.00

|

100.00

|

100.00

|

|

Hypothetical Ending Value:

|

80.00

|

115.00

|

110.00

|

|

Hypothetical Coupon Barrier:

|

70.00

|

70.00

|

70.00

|

|

Hypothetical Threshold Value:

|

70.00

|

70.00

|

70.00

|

|

Performance Factor (Ending Value divided by Starting Value):

|

80.00%

|

115.00%

|

110.00%

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

|

SPDR® S&P® Regional Banking ETF

|

Russell 2000® Index

|

Nasdaq-100 Index®

|

|

Hypothetical Starting Value:

|

100.00

|

100.00

|

100.00

|

|

Hypothetical Ending Value:

|

120.00

|

45.00

|

90.00

|

|

Hypothetical Coupon Barrier:

|

70.00

|

70.00

|

70.00

|

|

Hypothetical Threshold Value:

|

70.00

|

70.00

|

70.00

|

|

Performance Factor (Ending Value divided by Starting Value):

|

120.00%

|

45.00%

|

90.00%

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

All disclosures contained in this pricing supplement regarding the Underlyings, including, without limitation, their make-up, method of calculation, and changes in their components, have been derived from publicly available sources. The information reflects the policies of, and is subject to change by, each of SSGA Funds Management, Inc. (“SSGA”), the investment advisor to the KRE, FTSE Russell, the sponsor of the RTY, and Nasdaq, Inc., the sponsor of the NDX. We refer to SSGA as the “Investment Advisor” and FTSE Russell and Nasdaq, Inc. as the “Underlying Sponsors”. The Investment Advisor and the Underlying Sponsors, which license the copyright and all other rights to the respective Underlyings, have no obligation to continue to publish, and may discontinue publication of, the Underlyings. The consequences of any Investment Advisor or Underlying Sponsor discontinuing publication of the applicable Underlying are discussed in “General Terms of the Securities — Discontinuance of an Index” and “—Anti-dilution Adjustments Relating

to a Fund; Alternate Calculation” in the accompanying product supplement. None of us, the Guarantor, the calculation agent, or BofAS accepts any responsibility for the calculation, maintenance or publication of any Underlying or any successor fund or successor index. None of us, the Guarantor, BofAS or any of our other affiliates makes any representation to you as to the future performance of the Underlyings. You should make your own investigation into the Underlyings.

|

|

The SPDR® S&P® Regional Banking ETF

|

|

●

|

float-adjusted market capitalization above US$500 million and float-adjusted liquidity ratio above 90%; or

|

|

●

|

float-adjusted market capitalization above US$400 million and float-adjusted liquidity ratio above 150%.

|

|

●

|

Market Capitalization: Float-adjusted market capitalization should be at least US$400 million for inclusion in the fund underlying index. Existing index components must have a float-adjusted market capitalization of US$300 million to remain in the fund underlying index at each rebalancing.

|

|

●

|

Liquidity: The liquidity measurement used is a liquidity ratio, defined as dollar value traded over the previous 12-months divided by the float-adjusted market capitalization as of the fund underlying index rebalancing reference date. Stocks having a float-adjusted market capitalization above US$500 million must have a liquidity ratio greater than 90% to be eligible for addition to the fund underlying index. Stocks having a float-adjusted market capitalization between US$400 and US$500 million must have a liquidity ratio greater than 150% to be eligible for addition to the fund underlying index. Existing index constituents must have a liquidity ratio greater than 50% to remain in the fund underlying index at the quarterly rebalancing. The length of time to evaluate liquidity is reduced to the available trading period for IPOs or spin-offs that do not have 12 months of trading history.

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

●

|

Takeover Restrictions: At the discretion of S&P®, constituents with shareholder ownership restrictions defined in company bylaws may be deemed ineligible for inclusion in the fund underlying index. Ownership restrictions preventing entities from replicating the index weight of a company may be excluded from the eligible universe or removed from the fund underlying index.

|

|

●

|

Turnover: S&P® believes turnover in index membership should be avoided when possible. At times, a company may appear to temporarily violate one or more of the addition criteria. However, the addition criteria are for addition to the fund underlying index, not for continued membership. As a result, an index constituent that appears to violate the criteria for addition to the fund underlying index will not be deleted unless ongoing conditions warrant a change in the composition of the fund underlying index.

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

|

|

The Russell 2000® Index

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

The Nasdaq-100 Index®

|

|

●

|

the security’s U.S. listing must be exclusively on the Nasdaq Global Select Market or the Nasdaq Global Market (unless the security was dually listed on another U.S. market prior to January 1, 2004 and has continuously maintained such listing);

|

|

●

|

the security must be of a non-financial company;

|

|

●

|

the security may not be issued by an issuer currently in bankruptcy proceedings;

|

|

●

|

the security must have a minimum three-month average daily trading volume of at least 200,000 shares;

|

|

●

|

if the issuer of the security is organized under the laws of a jurisdiction outside the U.S., then such security must have listed options on a recognized options market in the U.S. or be eligible for listed-options trading on a recognized options market in the U.S.;

|

|

●

|

the issuer of the security may not have entered into a definitive agreement or other arrangement which would likely result in the security no longer being eligible for inclusion in the NDX;

|

|

●

|

the issuer of the security may not have annual financial statements with an audit opinion that is currently withdrawn; and

|

|

●

|

the issuer of the security must have “seasoned” on NASDAQ, the New York Stock Exchange or NYSE Amex. Generally, a company is considered to be seasoned if it has been listed on a market for at least three full months (excluding the first month of initial listing).

|

|

●

|

the security’s U.S. listing must be exclusively on the Nasdaq Global Select Market or the Nasdaq Global Market;

|

|

●

|

the security must be of a non-financial company;

|

|

●

|

the security may not be issued by an issuer currently in bankruptcy proceedings;

|

|

●

|

the security must have a minimum three-month average daily trading volume of at least 200,000 shares;

|

|

●

|

if the issuer of the security is organized under the laws of a jurisdiction outside the U.S., then such security must have listed options on a recognized options market in the U.S. or be eligible for listed-options trading on a recognized options market in the U.S. (measured annually during the ranking review process);

|

|

●

|

the security must have an adjusted market capitalization equal to or exceeding 0.10% of the aggregate adjusted market capitalization of the NDX at each month-end. In the event a company does not meet this criterion for two consecutive month-ends, it will be removed from the NDX effective after the close of trading on the third Friday of the following month; and

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

●

|

the issuer of the security may not have annual financial statements with an audit opinion that is currently withdrawn.

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

Structuring the Securities

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the SPDR® S&P® Regional,Banking ETF, the Russell 2000® Index and the Nasdaq-100 Index® due September 29, 2025

|

|

|

|

|

|

|

|

U.S. Federal Income Tax Summary

|

|

●

|

There is no statutory, judicial, or administrative authority directly addressing the characterization of the Securities.

|

|

●

|

You agree with us (in the absence of an administrative determination, or judicial ruling to the contrary) to characterize and treat the Securities for all tax purposes as contingent income-bearing single financial contracts with respect to the Underlyings. In the opinion of Sidley Austin LLP, our tax counsel, the U.S. federal income tax characterization and treatment of the Securities described herein is a reasonable interpretation of current law.

|

|

●

|

Under this characterization and tax treatment of the Securities, a U.S. Holder (as defined beginning on page 38 of the accompanying prospectus) generally will recognize capital gain or loss upon maturity or upon a sale, exchange or redemption of the Securities prior to maturity. This capital gain or loss generally will be long-term capital gain or loss if you held the Securities for more than one year.

|

|

●

|

No assurance can be given that the Internal Revenue Service (“IRS”) or any court will agree with this characterization and tax treatment.

|

|

●

|

We intend to take the position that any Contingent Coupon Payments constitute taxable ordinary income to a U.S. Holder at the time received or accrued, in accordance with the U.S. Holder’s method of tax accounting.

|

|

●

|

We intend to treat any Contingent Coupon Payment made to Non-U.S. Holders (as defined beginning on page 39 of the accompanying prospectus) as generally subject to withholding at a 30% rate (or at a lower rate under an applicable income tax treaty) on the entire amount of any Contingent Coupon Payment made unless such payments are effectively connected with the conduct by the Non-U.S. Holder of a trade or business in the U.S. (in which case, to avoid withholding, the Non-U.S. Holder will be required to provide a Form W-8ECI). We (or the applicable paying agent) will not pay any additional amounts in respect of such withholding.

|

|

●

|

Under current IRS guidance, withholding on “dividend equivalent” payments (as discussed in the accompanying product supplement), if any, will not apply to Securities that are issued as of the date of this pricing supplement unless such Securities are “delta-one” instruments.

|

|

|