Terms of the Notes

The Contingent Income Auto-Callable Yield Notes Linked to the Least Performing of the Dow Jones Industrial Average®, the Nasdaq-100® Index and the Russell 2000® Index (the “Notes”) provide a monthly Contingent Coupon Payment of $8.333 on the applicable Contingent Payment Date if, on any monthly Observation Date, the Observation Value of each Underlying is greater than or equal to its Coupon Barrier. Beginning in June 2023, if the Observation Value of each Underlying is greater than or equal to 100% of its Starting Value on any of the Observation Dates occurring quarterly indicated by the second footnote appearing below the table beginning on page PS-4 of the Preliminary Pricing Supplement, the Notes will be automatically called, in whole but not in part, at an amount equal to 100% of the principal amount, together with the relevant Contingent Coupon Payment. No further amounts will be payable following an Automatic Call. If the Notes are not automatically called, at maturity you will receive the Redemption Amount, calculated as described under “Redemption Amount Determination”.

| Issuer: | BofA Finance LLC (“BofA Finance”) |

| Guarantor: | Bank of America Corporation (“BAC”) |

| Term: | Approximately 3 years, unless previously automatically called. |

| Underlyings: | The Dow Jones Industrial Average® (Bloomberg symbol: “INDU”), the Nasdaq-100® Index (Bloomberg symbol: “NDX”) and the Russell 2000® Index (Bloomberg symbol: “RTY”). |

| Pricing and Issue Dates*: | December 21, 2022 and December 27, 2022, respectively. |

| Observation Dates†*: | Monthly. Please see the Preliminary Pricing Supplement for further details. |

| Coupon Barrier: | For each Underlying, 70% of its Starting Value. |

| Threshold Value: | For each Underlying, 70% of its Starting Value. |

| Call Value: | For each Underlying, 100% of its Starting Value. |

| Contingent Coupon Payment*: | If, on any monthly Observation Date, the Observation Value of each Underlying is greater than or equal to its Coupon Barrier, we will pay a Contingent Coupon Payment of $8.333 per $1,000 in principal amount of Notes (equal to a rate of 0.8333% per month or 10.00% per annum) on the applicable Contingent Payment Date (including the Maturity Date). |

| Automatic Call: | Beginning in June 2023, all (but not less than all) of the Notes will be automatically called if the Observation Value of each Underlying is greater than or equal to its Call Value on any of the Observation Dates occurring quarterly indicated by the second footnote appearing below the table beginning on page PS-4 of the Preliminary Pricing Supplement. If the Notes are automatically called the Early Redemption Amount will be paid on the applicable Contingent Payment Date. |

| Early Redemption Amount: | For each $1,000 principal amount of Notes, $1,000 plus the applicable Contingent Coupon Payment. |

| Initial Estimated Value Range: | $910-$960 per Note. |

| Underwriting Discount*: | $28.50 (2.85% of the public offering price) per Note. |

| CUSIP: | 09709VC79. |

| Preliminary Pricing Supplement: | https://www.sec.gov/Archives/edgar/data/70858/000148105722004456/form424b2.htm |

|

* Subject to change prior to the Pricing Date. † Subject to adjustment. Please see the Preliminary Pricing Supplement for further details. | |

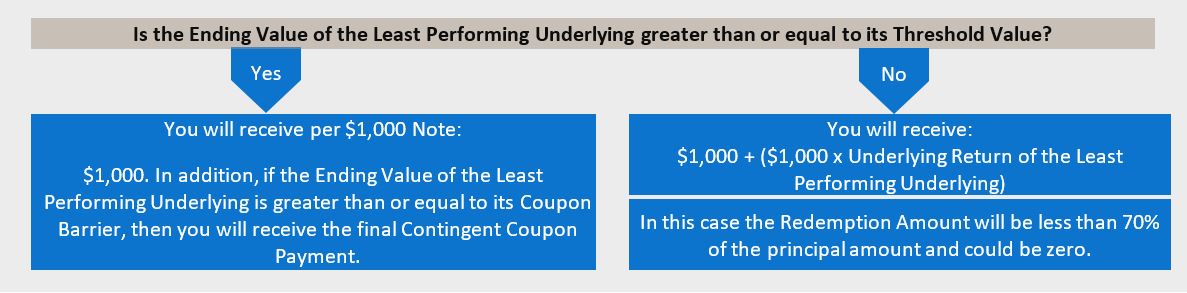

Redemption Amount Determination

(assuming the Notes have not been automatically called)

Hypothetical Returns at Maturity

| Underlying Return of the Least Performing Underlying |

Redemption Amount per Note |

Return on the Notes(1) |

| 60.00% | $1,008.333(2) | 0.8333% |

| 50.00% | $1,008.333 | 0.8333% |

| 40.00% | $1,008.333 | 0.8333% |

| 30.00% | $1,008.333 | 0.8333% |

| 20.00% | $1,008.333 | 0.8333% |

| 10.00% | $1,008.333 | 0.8333% |

| 5.00% | $1,008.333 | 0.8333% |

| 2.00% | $1,008.333 | 0.8333% |

| 0.00% | $1,008.333 | 0.8333% |

| -10.00% | $1,008.333 | 0.8333% |

| -20.00% | $1,008.333 | 0.8333% |

| -25.00% | $1,008.333 | 0.8333% |

| -27.00% | $1,008.333 | 0.8333% |

| -30.00%(3) | $1,008.333 | 0.8333% |

| -30.01% | $699.900 | -30.0100% |

| -40.00% | $600.000 | -40.0000% |

| -50.00% | $500.000 | -50.0000% |

| -100.00% | $0.000 | -100.0000% |

|

(1) The “Return on the Notes” is calculated based on the Redemption Amount and potential final Contingent Coupon Payment, not including any Contingent Coupon Payments paid prior to maturity. (2) This amount represents the sum of the principal amount and the final Contingent Coupon Payment. (3) This is the Underlying Return which corresponds to the Coupon Barrier and Threshold Value of the Least Performing Underlying. | ||

Risk Factors

| · | Your investment may result in a loss; there is no guaranteed return of principal. |

| · | Your return on the Notes is limited to the return represented by the Contingent Coupon Payments, if any, over the term of the Notes. |

| · | The Contingent Coupon Payment, Early Redemption Amount or Redemption Amount, as applicable, will not reflect the levels of the Underlyings other than on the Observation Dates. |

| · | The Notes are subject to a potential Automatic Call, which would limit your ability to receive the Contingent Coupon Payments over the full term of the Notes. |

| · | You may not receive any Contingent Coupon Payments and the Notes do not provide for any regular fixed coupon payments. |

| · | Because the Notes are linked to the least performing (and not the average performance) of the Underlyings, you may not receive any return on the Notes and may lose some or all of your principal amount even if the Observation Value or Ending Value of one Underlying is always greater than or equal to its Coupon Barrier or Threshold Value, as applicable. |

| · | Your return on the Notes may be less than the yield on a conventional debt security of comparable maturity. |

| · | Any payment on the Notes is subject to our credit risk and the credit risk of the Guarantor, and any actual or perceived changes in our or the Guarantor’s creditworthiness are expected to affect the value of the Notes. |

| · | The public offering price you pay for the Notes will exceed their initial estimated value. |

| · | We cannot assure you that a trading market for your Notes will ever develop or be maintained. |

| · | The Notes are subject to risks associated with small-size capitalization companies. |

| · | The Notes are subject to risks associated with foreign securities markets. |

You may revoke your offer to purchase the Notes at any time prior to the time at which we accept such offer on the date the Notes are priced. We reserve the right to change the terms of, or reject any offer to purchase, the Notes prior to their issuance. In the event of any changes to the terms of the Notes, we will notify you and you will be asked to accept such changes in connection with your purchase. You may also choose to reject such changes in which case we may reject your offer to purchase.

Please see the Preliminary Pricing Supplement for complete product disclosure, including related risks and tax disclosure.

This fact sheet is a summary of the terms of the Notes and factors that you should consider before deciding to invest in the Notes. BofA Finance has filed a registration statement (including preliminary pricing supplement, product supplement, prospectus supplement and prospectus) with the Securities and Exchange Commission, or SEC, for the offering to which this fact sheet relates. Before you invest, you should read this fact sheet together with the Preliminary Pricing Supplement dated December 2, 2022, Product Supplement EQUITY-1 dated January 3, 2020 and Prospectus Supplement and Prospectus dated December 31, 2019 to understand fully the terms of the Notes and other considerations that are important in making a decision about investing in the Notes. If the terms described in the applicable Preliminary Pricing Supplement are inconsistent with those described herein, the terms described in the applicable Preliminary Pricing Supplement will control. You may get these documents without cost by visiting EDGAR on the SEC Web site at sec.gov or by clicking on the hyperlinks to each of the respective documents incorporated by reference in the Preliminary Pricing Supplement. Alternatively, BofA Finance, any agent or any dealer participating in this offering will arrange to send you the Preliminary Pricing Supplement, Product Supplement EQUITY-1 and Prospectus Supplement and Prospectus if you so request by calling toll-free at 1-800-294-1322.