BofA Finance LLC

Fully and Unconditionally Guaranteed by Bank of America Corporation

Market Linked Securities

|

BofA Finance LLC

Fully and Unconditionally Guaranteed by Bank of America Corporation

Market Linked Securities

|

|

|

Issuer and Guarantor:

|

BofA Finance LLC (“BofA Finance” or “Issuer”) and Bank of America Corporation (“BAC” or “Guarantor”)

|

|

Underlyings:

|

S&P 500® Index, Russell 2000® Index and Nasdaq-100® Index

|

|

Pricing Date*:

|

March 29, 2023

|

|

Issue Date*:

|

April 3, 2023

|

|

Denominations:

|

$1,000 and any integral multiple of $1,000. References in the pricing supplement to a “Security” are to a Security with a principal amount of $1,000.

|

|

Contingent Coupon Payments:

|

On each Contingent Coupon Payment Date, you will receive a Contingent Coupon Payment at a per annum rate equal to the Contingent Coupon Rate if, and only if, the closing level of the Lowest Performing Underlying on the related Calculation Day is greater than or equal to its Coupon Barrier. Each Contingent Coupon Payment, if any, will be calculated per Security as follows: ($1,000 × Contingent Coupon Rate) / 4

|

|

Contingent Coupon Payment Dates:

|

Quarterly, on the third business day following each Calculation Day; provided that the Contingent Coupon Payment Date with respect to the Final Calculation Day will be the Maturity Date.

|

|

Contingent Coupon Rate:

|

At least 10.00% per annum, to be determined on the pricing date

|

|

Automatic Call:

|

If the closing level of the Lowest Performing Underlying on any of the Calculation Days from September 2023 to December 2025, inclusive, is greater than or equal to its Starting Value, the Securities will be automatically called, and on the related Call Settlement Date you will be entitled to receive a cash payment per Security equal to the principal amount per Security plus a final Contingent Coupon Payment.

|

|

Calculation Days*:

|

Quarterly, on the 24th day of each March, June, September and December, commencing June 2023 and ending December 2025, and March 24, 2026 (the “Final Calculation Day”).

|

|

Call Settlement Date:

|

Three business days after the applicable Calculation Day

|

|

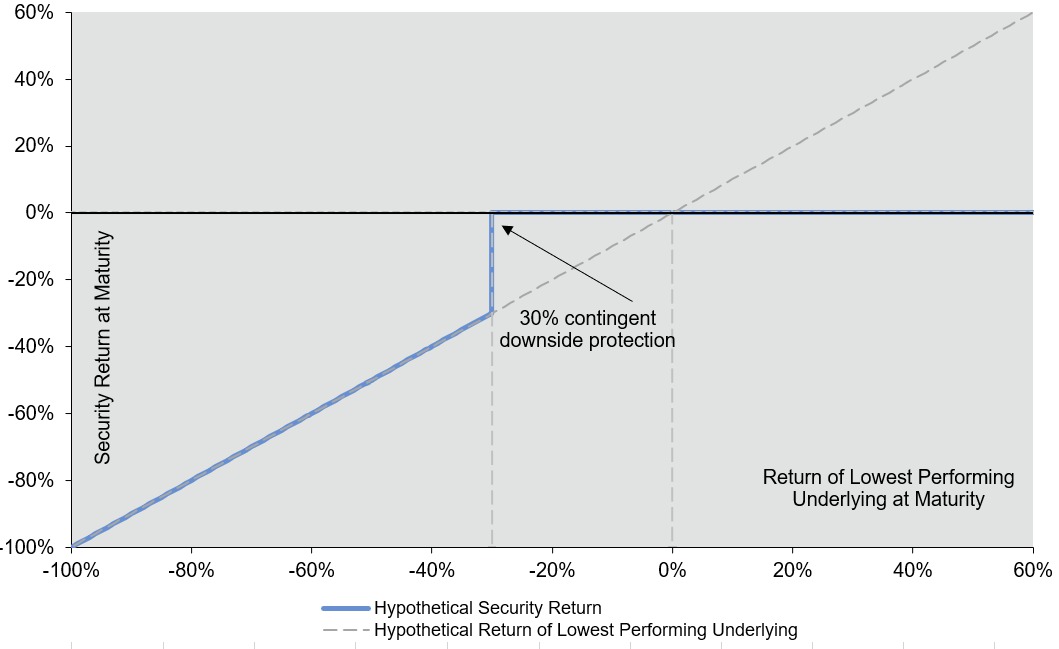

Maturity Payment Amount (per Security):

|

●

if the Ending Value of the Lowest Performing Underlying on the Final Calculation Day is greater than or equal to its

Threshold Value: $1,000; or ●

if the Ending Value of the Lowest Performing Underlying on the Final Calculation Day is less than its Threshold Value:

$1,000 × performance factor of the Lowest Performing Underlying on the Final Calculation Day

|

|

Maturity Date*:

|

March 27, 2026

|

|

Lowest Performing Underlying

|

For any Calculation Day, the Lowest Performing Underlying will be the Underlying with the lowest performance factor on that Calculation Day.

|

|

Performance Factor:

|

With respect to an Underlying on any Calculation Day, its closing level on such Calculation Day divided by its Starting Value (expressed as a percentage).

|

|

Starting Value:

|

For each Underlying, its closing level on the pricing date

|

|

Ending Value:

|

For each Underlying, its closing level on the Final Calculation Day

|

|

Coupon Barrier:

|

For each Underlying, 75% of its Starting Value

|

|

Threshold Value:

|

For each Underlying, 70% of its Starting Value

|

|

Calculation Agent:

|

BofA Securities, Inc. (“BofAS”), an affiliate of BofA Finance

|

|

Underwriting Discount**:

|

Up to 2.325%; dealers, including those using the trade name Wells Fargo Advisors (WFA), may receive a selling concession of 1.75% and WFA may receive a distribution expense fee of 0.075%.

|

|

CUSIP:

|

09709VMW3

|

|

Material Tax Consequences:

|

See the preliminary pricing supplement.

|

|

●

Your investment may result in a loss; there is no guaranteed return of principal.

●

Your return on the Securities is limited to the return represented by the Contingent Coupon Payments, if any, over the term of the Securities.

●

The Securities are subject to a potential automatic call, which would limit your ability to receive the Contingent Coupon Payments over the full term of the Securities.

●

You may not receive any Contingent Coupon Payments.

●

Because the Securities are linked to the lowest performing (and not the average performance) of the Underlyings, you may not receive any return on the Securities and may lose a significant portion or all of your principal amount even if the closing level of one Underlying is always greater than or equal to its Coupon Barrier or Threshold Value, as applicable.

●

Higher Contingent Coupon Rates are associated with greater risk.

●

Your return on the Securities may be less than the yield on a conventional debt security of comparable maturity.

●

The Contingent Coupon Payment, payment upon automatic call or Maturity Payment Amount, as applicable, will not reflect the levels of the Underlyings other than on the Calculation Days.

●

A Contingent Coupon Payment Date, a Call Settlement Date and the Maturity Date may be postponed if a Calculation Day is postponed.

●

We are a finance subsidiary and, as such, have no independent assets, operations or revenues.

●

Any payment on the Securities is subject to the credit risk of BofA Finance, as issuer, and BAC, as Guarantor, and actual or perceived changes in BofA Finance or the Guarantor’s creditworthiness are expected to affect the value of the Securities.

●

The public offering price you pay for the Securities will exceed their initial estimated value.

●

The initial estimated value does not represent a minimum or maximum price at which BofA Finance, BAC, BofAS or any of our other affiliates or WFS or its affiliates would be willing to purchase your Securities in any secondary market (if any exists) at any time.

|

●

BofA Finance cannot assure you that a trading market for your Securities will ever develop or be maintained.

●

The Securities are not designed to be short-term trading instruments, and if you attempt to sell the Securities prior to maturity, their market value, if any, will be affected by various factors that interrelate in complex ways, and their market value may be less than the principal amount. Trading and hedging activities by BofA Finance, the Guarantor and any of our other affiliates, including BofAS, and WFS and its affiliates, may create conflicts of interest with you and may affect your return on the Securities and their market value.

●

There may be potential conflicts of interest involving the calculation agent, which is an affiliate of ours.

●

Changes that affect the Indices may adversely affect the value of the Securities and any payments on the Securities.

●

We and our affiliates have no affiliation with any Index Sponsor and have not independently verified their public disclosure of information.

●

The Securities are subject to risks associated with foreign securities markets.

●

The Securities are subject to risks associated with small-size capitalization companies.

●

The U.S. federal income tax consequences of an investment in the Securities are uncertain, and may be adverse to a holder of the Securities.

|