|

Filed Pursuant to Rule 424(b)(2)

Registration Nos. 333-268718 and 333-268718-01

|

Pricing Supplement

Dated February 29, 2024

(To Prospectus dated December 30, 2022,

Series A Prospectus Supplement dated December 30, 2022 and

Product Supplement No. WF-1 dated March 8, 2023)

|

|

|

|

BofA Finance LLC

Medium-Term Notes, Series A

Fully and Unconditionally Guaranteed by Bank of America Corporation

|

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

$770,000 Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

|

■ Linked to the common stock of Tesla Inc. (the “Underlying Stock”)

■ Unlike ordinary debt securities, the Securities do not provide for fixed payments of interest, do not repay a fixed amount of principal on the Maturity Date and are subject to potential automatic call prior to the Maturity Date upon the terms described below. Whether the Securities pay a Contingent Coupon, whether the Securities are automatically called prior to the Maturity Date and, if they are not automatically called, whether you receive the principal amount of your Securities on the Maturity Date will depend, in each case, on the stock closing price of the Underlying Stock on the relevant Calculation Day

■ Contingent Coupon. The Securities will pay a Contingent Coupon on a quarterly basis until the earlier of the Maturity Date or automatic call if, and only if, the stock closing price of the Underlying Stock on the Calculation Day for that quarter is greater than or equal to the Coupon Barrier. However, if the stock closing price of the Underlying Stock on a Calculation Day is less than the Coupon Barrier, you will not receive any Contingent Coupon for the relevant quarter. If the stock closing price of the Underlying Stock is less than the Coupon Barrier on every Calculation Day, you will not receive any Contingent Coupons throughout the entire term of the Securities. The Coupon Barrier for the Underlying Stock is equal to 70% of the Starting Price. The Contingent Coupon Rate is 20.00% per annum

■ Automatic Call. If the stock closing price of the Underlying Stock on any of the quarterly Calculation Days from August 2024 to November 2027, inclusive, is greater than or equal to the Starting Price, the Securities will be automatically called for the principal amount plus a final Contingent Coupon Payment

■ Potential Loss of Principal. If the Securities are not automatically called prior to the Maturity Date, you will receive the principal amount on the Maturity Date if, and only if, the stock closing price of the Underlying Stock on the Final Calculation Day is greater than or equal to the Threshold Price. If the stock closing price of the Underlying Stock on the Final Calculation Day is less than the Threshold Price, you will lose more than 30%, and possibly all, of the principal amount of your Securities. The Threshold Price for the Underlying Stock is equal to 70% of the Starting Price

■ If the Securities are not automatically called prior to the Maturity Date, you will have full downside exposure to the Underlying Stock from the Starting Price if the stock closing price on the Final Calculation Day is less than the Threshold Price, but you will not participate in any appreciation of the Underlying Stock and will not receive any dividends on the Underlying Stock

■ All payments on the Securities are subject to the credit risk of BofA Finance LLC (“BofA Finance”), as issuer of the Securities, and Bank of America Corporation (“BAC” or the “Guarantor”), as guarantor of the Securities

■ Securities will not be listed on any securities exchange

|

The initial estimated value of the Securities as of the Pricing Date is $962.40 per Security, which is less than the public offering price listed below. The actual value of your Securities at any time will reflect many factors and cannot be predicted with accuracy. See “Selected Risk Considerations” beginning on page PS-9 of this pricing supplement and “Structuring the Securities” on page PS-19 of this pricing supplement for additional information.

The Securities have complex features and investing in the Securities involves risks not associated with an investment in conventional debt securities. Potential purchasers of the Securities should consider the information in “Selected Risk Considerations” beginning on page PS-9 herein and “Risk Factors” beginning on page PS-5 of the accompanying product supplement, page S-6 of the accompanying prospectus supplement, and page 7 of the accompanying prospectus.

None of the Securities and Exchange Commission (the “SEC”), any state securities commission, or any other regulatory body has approved or disapproved of these Securities or determined if this pricing supplement and the accompanying product supplement, prospectus supplement and prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

|

|

Public offering price

|

Underwriting Discount(1)(2)

|

Proceeds, before expenses, to BofA Finance

|

|

Per Security

|

$1,000.00

|

$23.25

|

$976.75

|

|

Total

|

$770,000.00

|

$17,902.50

|

$752,097.50

|

|

(1)

|

Wells Fargo Securities, LLC and BofA Securities, Inc. are the selling agents for the distribution of the Securities and are acting as principal. See “Terms of the Securities—Selling Agents” in this pricing supplement for further information.

|

|

(2)

|

In addition, in respect of certain Securities sold in this offering, BofA Securities, Inc. or its affiliates may pay a fee of up to $4.00 per Security to selected securities dealers in consideration for marketing and other services in connection with the distribution of the Securities to other securities dealers.

|

|

Wells Fargo Securities

|

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

|

|

|

|

Issuer:

|

BofA Finance LLC.

|

|

Guarantor:

|

BAC.

|

|

Underlying Stock:

|

The common stock of Tesla Inc. (Nasdaq Global Select Market symbol: “TSLA”) (the “Underlying Stock”).

|

|

Pricing Date:

|

February 29, 2024.

|

|

Issue Date:

|

March 5, 2024.

|

|

Maturity Date:

|

March 2, 2028, subject to postponement as described below in “—Market Disruption Events and Postponement Provisions”. The Securities are not subject to repayment at the option of any holder of the Securities prior to the Maturity Date.

|

|

Denominations:

|

$1,000 and any integral multiple of $1,000. References in this pricing supplement to a “Security” are to a Security with a principal amount of $1,000.

|

|

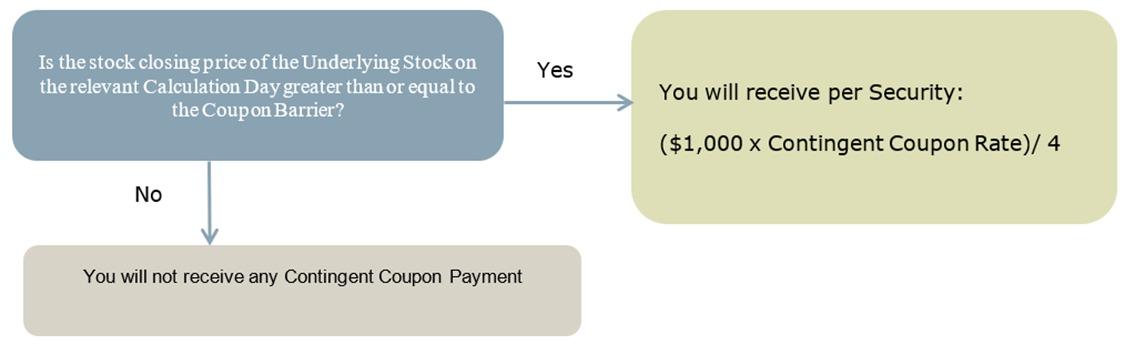

Contingent Coupon Payment:

|

On each Contingent Coupon Payment Date, you will receive a Contingent Coupon Payment at a per annum rate equal to the Contingent Coupon Rate if, and only if, the stock closing price of the Underlying Stock on the related Calculation Day is greater than or equal to the Coupon Barrier. Each “Contingent Coupon Payment,” if any, will be calculated per Security as follows: ($1,000 × Contingent Coupon Rate)/4. Any Contingent Coupon Payment will be rounded to the nearest cent, with one-half cent rounded upward.

If the stock closing price of the Underlying Stock on any Calculation Day is less than the Coupon Barrier, you will not receive any Contingent Coupon Payment on the related Contingent Coupon Payment Date. If the stock closing price of the Underlying Stock is less than the Coupon Barrier on all Calculation Days, you will not receive any Contingent Coupon Payments over the term of the Securities.

|

|

Contingent Coupon Payment Dates:

|

Quarterly, on the third business day following each Calculation Day (as each such Calculation Day may be postponed pursuant to “—Market Disruption Events and Postponement Provisions” below, if applicable); provided that the Contingent Coupon Payment Date with respect to the Final Calculation Day will be the Maturity Date.

|

|

Contingent Coupon Rate:

|

The “Contingent Coupon Rate” is 20.00% per annum (equal to 5.00% per quarter).

|

|

Automatic Call:

|

If the stock closing price of the Underlying Stock on any of the Calculation Days from August 2024 to November 2027, inclusive, is greater than or equal to the Starting Price, the Securities will be automatically called, and on the related Call Settlement Date you will be entitled to receive a cash payment per Security in U.S. dollars equal to the principal amount per Security plus a final Contingent Coupon Payment. The Securities will not be subject to automatic call until the second Calculation Day, which is approximately six months after the issue date.

If the Securities are automatically called, they will cease to be outstanding on the related Call Settlement Date and you will have no further rights under the Securities after such Call Settlement Date. You will not receive any notice from us if the Securities are automatically called.

|

|

Calculation Days:

|

Quarterly, on the 28th day of each February, May, August and November, commencing May 2024 and ending November 2027, and the Final Calculation Day, each subject to postponement as described below under “—Market Disruption Events and Postponement Provisions.” We refer to February 28, 2028 as the “Final Calculation Day.”

|

____________________

PS-2

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

|

Call Settlement Date:

|

Three business days after the applicable Calculation Day (as each such Calculation Day may be postponed pursuant to “—Market Disruption Events and Postponement Provisions” below, if applicable).

|

|

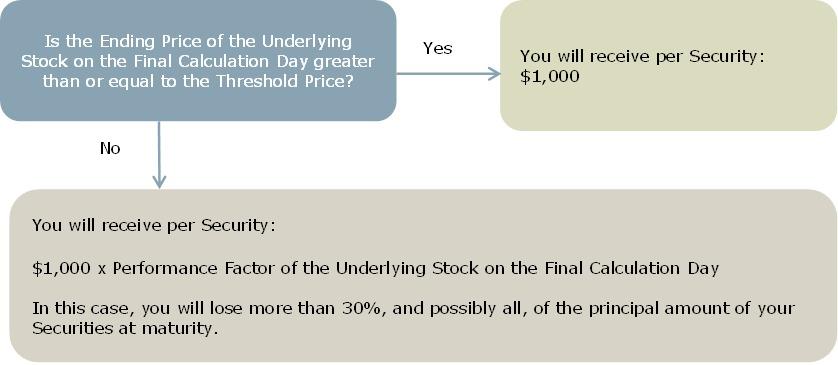

Maturity Payment Amount:

|

If the Securities are not automatically called prior to the Maturity Date, you will be entitled to receive on the Maturity Date a cash payment per Security in U.S. dollars equal to the Maturity Payment Amount (in addition to the final Contingent Coupon Payment, if any). The “Maturity Payment Amount” per Security will equal:

• if the Ending Price of the Underlying Stock on the Final Calculation Day is greater than or equal to the Threshold Price:

$1,000; or

• if the Ending Price of the Underlying Stock on the Final Calculation Day is less than the Threshold Price:

|

|

$1,000 × Performance Factor of the Underlying Stock on the Final Calculation Day

|

|

If the Securities are not automatically called prior to the Maturity Date and the Ending Price of the Underlying Stock on the Final Calculation Day is less than the Threshold Price, you will lose more than 30%, and possibly all, of the principal amount of your Securities on the Maturity Date.

Any return on the Securities will be limited to the sum of your Contingent Coupon Payments, if any. You will not participate in any appreciation of the Underlying Stock, but you will have full downside exposure to decreases in the stock closing price of the Underlying Stock on the Final Calculation Day if the Ending Price is less than the Threshold Price.

|

|

Performance Factor:

|

With respect to the Underlying Stock on any Calculation Day, the stock closing price on such Calculation Day divided by the Starting Price (expressed as a percentage).

|

|

Stock Closing Price:

|

Stock closing price and adjustment factor have the meanings set forth under “General Terms of the Securities—Certain Terms for Securities Linked to an Underlying Stock—Certain Definitions” in the accompanying product supplement.

|

|

Starting Price:

|

$201.88, which is the stock closing price on the Pricing Date.

|

|

Ending Price:

|

, which is the stock closing price on the Final Calculation Day.

|

|

Coupon Barrier:

|

$141.316, which is equal to 70.00% of the Starting Price.

|

|

Threshold Price:

|

$141.316, which is equal to 70.00% of the Starting Price.

|

____________________

.

PS-3

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

|

|

|

|

Market Disruption Events and Postponement Provisions:

|

Each Calculation Day is subject to postponement due to non-trading days and the occurrence of a market disruption event. In addition, the Maturity Date will be postponed if the Final Calculation Day is postponed and will be adjusted for non-business days. For more information regarding adjustments to the Calculation Days and the Maturity Date, see “General Terms of the Securities—Consequences of a Market Disruption Event; Postponement of a Calculation Day— Securities Linked to a Single Market Measure” and “—Payment Dates” in the accompanying product supplement. For purposes of the accompanying product supplement, each Contingent Coupon Payment Date, each Call Settlement Date and the Maturity Date is a “payment date.” In addition, for information regarding the circumstances that may result in a market disruption event, see “General Terms of the Securities—Certain Terms for Securities Linked to an Underlying Stock—Market Disruption Events” in the accompanying product supplement.

|

|

Calculation Agent:

|

BofA Securities, Inc. (“BofAS”), an affiliate of BofA Finance.

|

|

Selling Agents:

|

BofAS and Wells Fargo Securities, LLC (“WFS”).

Under our distribution agreement with BofAS, BofAS will purchase the Securities from us as principal at the public offering price indicated on the cover of this pricing supplement, less the indicated underwriting discount. BofAS will sell the Securities to WFS at the public offering price of the Securities less a concession of up to $23.25 per Security. WFS may provide dealers, which may include Wells Fargo Advisors (“WFA”) (the trade name of the retail brokerage business of WFS’s affiliates, Wells Fargo Clearing Services, LLC and Wells Fargo Advisors Financial Network, LLC), with a selling concession of up to $17.50 per Security. In addition to the concession allowed to WFA, WFS may pay up to $0.75 per Security to WFA as a distribution expense fee for each Security sold by WFA.

In addition, in respect of certain Securities sold in this offering, BofAS or its affiliates may pay a fee of up to $4.00 per Security to selected securities dealers in consideration for marketing and other services in connection with the distribution of the Securities to other securities dealers.

WFS has advised us that if it, WFA or any of their affiliates makes a secondary market in the Securities at any time up to the Issue Date or during the four-month period following the Issue Date, the secondary market price offered by it, WFA or any of their affiliates will be increased by an amount reflecting a portion of the costs associated with selling, structuring and hedging the Securities that are included in the public offering price of the Securities. Because this portion of the costs is not fully deducted upon issuance, WFS has advised us that any secondary market price it, WFA or any of their affiliates offers during this period will be higher than it otherwise would be outside of this period, as any secondary market price offered outside of this period will reflect the full deduction of the costs as described above. WFS has advised us that the amount of this increase in the secondary market price will decline steadily to zero over this four-month period. If you hold the Securities through an account at WFS, WFA or any of their affiliates, WFS has advised us that it expects that this increase will also be reflected in the value indicated for the Securities on your brokerage account statement. If you hold your Securities through an account at a broker-dealer other than WFS, WFA or any of their affiliates, the value of the Securities on your brokerage account statement may be different than if you held your Securities at WFS, WFA or any of their affiliates.

|

|

Material Tax

Consequences:

|

For a discussion of the material U.S. federal income and estate tax consequences of the ownership and disposition of the Securities, see “U.S. Federal Income Tax Summary.”

|

|

CUSIP:

|

09710PZF6

|

PS-4

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

|

Additional Information about BofA Finance, the Guarantor and the Securities

|

The terms and risks of the Securities are contained in this pricing supplement and in the following related product supplement, prospectus supplement and prospectus. Information included in this pricing supplement supersedes information in the product supplement, prospectus supplement and prospectus to the extent that it is different from that information. These documents can be accessed at the following links:

|

•

|

Product Supplement No. WF-1 dated March 8, 2023:

|

|

•

|

Series A MTN prospectus supplement dated December 30, 2022 and prospectus dated December 30, 2022:

|

These documents have been filed as part of a registration statement with the SEC, which may, without cost, be accessed on the SEC website at www.sec.gov or obtained from BofAS by calling 1-800-294-1322. Before you invest, you should read this pricing supplement and the accompanying product supplement, prospectus supplement and prospectus for information about us, BAC and this offering. Any prior or contemporaneous oral statements and any other written materials you may have received are superseded by this pricing supplement and the accompanying product supplement, prospectus supplement and prospectus. Certain terms used but not defined in this pricing supplement have the meanings set forth in the accompanying product supplement or prospectus supplement. Unless otherwise indicated or unless the context requires otherwise, all references in this document to “we,” “us,” “our,” or similar references are to BofA Finance, and not to BAC.

The Securities are our senior debt securities. Any payments on the Securities are fully and unconditionally guaranteed by BAC. The Securities and the related guarantee are not insured by the Federal Deposit Insurance Corporation or secured by collateral. The Securities will rank equally in right of payment with all of our other unsecured and unsubordinated obligations, except obligations that are subject to any priorities or preferences by law. The related guarantee will rank equally in right of payment with all of BAC’s other unsecured and unsubordinated obligations, except obligations that are subject to any priorities or preferences by law, and senior to its subordinated obligations. Any payments due on the Securities, including any repayment of the principal amount, will be subject to the credit risk of BofA Finance, as issuer, and BAC, as guarantor.

PS-5

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

The Securities are not appropriate for all investors. The Securities may be an appropriate investment for investors who:

▪ seek an investment with contingent coupon payments at a rate of 20.00% per annum until the earlier of the Maturity Date or automatic call, if, and only if, the stock closing price of the Underlying Stock on the applicable Calculation Day is greater than or equal to 70% of the Starting Price;

▪ understand that if the Ending Price of the Underlying Stock on the Final Calculation Day has declined by more than 30% from the Starting Price, they will be fully exposed to the decline in the Underlying Stock from the Starting Price and will lose more than 30%, and possibly all, of the principal amount of their Securities at maturity;

▪ are willing to accept the risk that they may receive few or no Contingent Coupon Payments over the term of the Securities;

▪ understand that the Securities may be automatically called prior to the Maturity Date and that the term of the Securities may be as short as approximately six months;

▪ understand and are willing to accept the full downside risks of the Underlying Stock;

▪ are willing to forgo participation in any appreciation of the Underlying Stock and dividends on the Underlying Stock; and

▪ are willing to hold the Securities until maturity.

The Securities may not be an appropriate investment for investors who:

▪ seek a liquid investment or are unable or unwilling to hold the Securities to maturity;

▪ require full payment of the principal amount of the Securities at maturity;

▪ seek a security with a fixed term;

▪ are unwilling to purchase Securities with an estimated value as of the Pricing Date that is lower than the public offering price set forth on the cover page;

▪ are unwilling to accept the risk that the stock closing price of the Underlying Stock on the Final Calculation Day may decline by more than 30% from the Starting Price;

▪ seek certainty of current income over the term of the Securities;

▪ seek exposure to the upside performance of the Underlying Stock;

▪ are unwilling to accept the risk of exposure to the Underlying Stock;

▪ are unwilling to accept the credit risk of BofA Finance, as issuer, and BAC, as guarantor, to obtain exposure to the Underlying Stock generally, or to obtain exposure to the Underlying Stock that the Securities provide specifically; or

▪ prefer the lower risk of conventional fixed income investments with comparable maturities issued by companies with comparable credit ratings.

The considerations identified above are not exhaustive. Whether or not the Securities are an appropriate investment for you will depend on your individual circumstances, and you should reach an investment decision only after you and your investment, legal, tax, accounting and other advisors have carefully considered the appropriateness of an investment in the Securities in light of your particular circumstances. You should also review carefully “Selected Risk Considerations” herein and “Risk Factors” in each of the accompanying product supplement, prospectus supplement and prospectus for risks related to an investment in the Securities. For more information about the Underlying Stock, please see the sections titled “The Common Stock of Tesla Inc.” below.

PS-6

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

|

|

|

Determining Payment On A Contingent Coupon Payment Date and at Maturity

|

If the Securities have not been previously automatically called, on each Contingent Coupon Payment Date, either you will receive a Contingent Coupon Payment or you will not receive a Contingent Coupon Payment, depending on the stock closing price of the Underlying Stock on the related Calculation Day, determined as follows:

If the Securities have not been automatically called prior to the Maturity Date, then at maturity you will receive (in addition to the final Contingent Coupon Payment, if otherwise payable) a cash payment per Security (the Maturity Payment Amount) based on the Ending Price of the Underlying Stock, calculated as follows:

PS-7

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

|

|

|

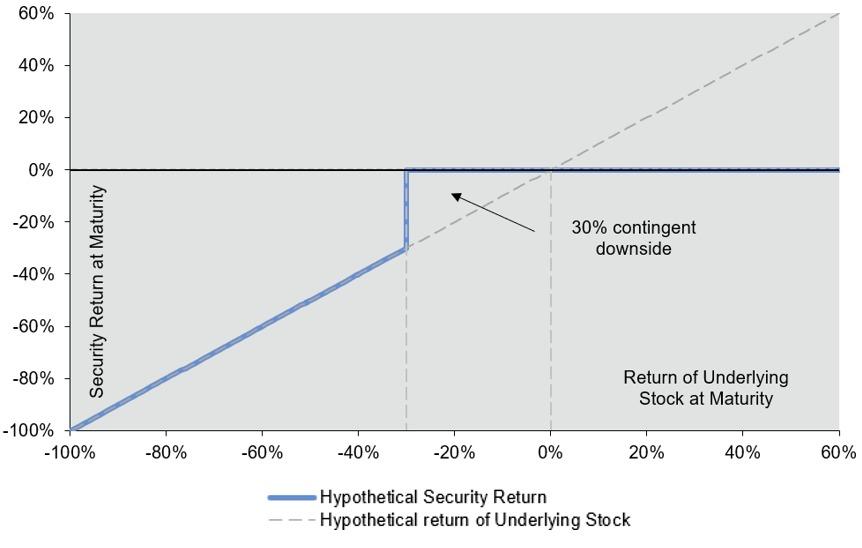

Hypothetical Payout Profile

|

The following profile illustrates the potential Maturity Payment Amount on the Securities (excluding the final Contingent Coupon Payment, if any) for a range of hypothetical performances of the Underlying Stock on the Final Calculation Day from the Starting Price to the Ending Price, assuming the Securities have not been automatically called prior to the Maturity Date. As this profile illustrates, in no event will you have a positive rate of return based solely on the Maturity Payment Amount received at maturity; any positive return will be based solely on the Contingent Coupon Payments, if any, received during the term of the Securities. This graph has been prepared for purposes of illustration only. Your actual return will depend on the actual Ending Price of the Underlying Stock on the Final Calculation Day and whether you hold your Securities to the Maturity Date.

PS-8

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

|

|

|

Selected Risk Considerations

|

The Securities have complex features and investing in the Securities will involve risks not associated with an investment in conventional debt securities. Your decision to purchase the Securities should be made only after carefully considering the risks of an investment in the Securities, including those discussed below, with your advisors in light of your particular circumstances. The Securities are not an appropriate investment for you if you are not knowledgeable about significant elements of the Securities or financial matters in general. You should carefully review the more detailed explanation of risks relating to the Securities in the “Risk Factors” sections beginning on page PS-5 of the accompanying product supplement, page S-6 of the accompanying prospectus supplement and page 7 of the accompanying prospectus.

Structure-related Risks

Your investment may result in a loss; there is no guaranteed return of principal. There is no fixed principal repayment amount on the Securities at maturity. If the Securities are not automatically called prior to maturity and the Ending Price of the Underlying Stock is less than the Threshold Price, at maturity you will lose 1% of the principal amount for each 1% that the Ending Price of the Underlying Stock is less than the Starting Price. In that case, you will lose a significant portion or all of your investment in the Securities.

Your return on the Securities is limited to the return represented by the Contingent Coupon Payments, if any, over the term of the Securities. Your return on the Securities is limited to the Contingent Coupon Payments paid over the term of the Securities, regardless of the extent to which the stock closing price of the Underlying Stock on any Calculation Day or the Ending Price of the Underlying Stock exceeds the Coupon Barrier or Starting Price, as applicable. Similarly, the amount payable at maturity or upon an automatic call will never exceed the sum of the principal amount and the applicable Contingent Coupon Payment, regardless of the extent to which the stock closing price of the Underlying Stock on any Calculation Day exceeds the Starting Price. In contrast, a direct investment in the Underlying Stock would allow you to receive the benefit of any appreciation in its price. Thus, any return on the Securities will not reflect the return you would realize if you actually owned those securities and received the dividends paid or distributions made on them.

The Securities are subject to a potential automatic call, which would limit your ability to receive the Contingent Coupon Payments over the full term of the Securities. The Securities are subject to a potential automatic call. Beginning in August 2024, the Securities will be automatically called if, on any Calculation Day prior to the Final Calculation Day, the stock closing price of the Underlying Stock is greater than or equal to the Starting Price. If the Securities are automatically called prior to the Maturity Date, you will be entitled to receive the principal amount and the Contingent Coupon Payment with respect to the applicable Calculation Day, and no further amounts will be payable with respect to the Securities. In this case, you will lose the opportunity to continue to receive Contingent Coupon Payments after the date of the automatic call. If the Securities are called prior to the Maturity Date, you may be unable to invest in other securities with a similar level of risk that could provide a return that is similar to the Securities.

You may not receive any Contingent Coupon Payments. The Securities do not provide for any regular fixed coupon payments. Investors in the Securities will not necessarily receive any Contingent Coupon Payments on the Securities. If the stock closing price of the Underlying Stock on a Calculation Day is less than the Coupon Barrier, you will not receive the Contingent Coupon Payment applicable to that Calculation Day. If the stock closing price of the Underlying Stock is less than the Coupon Barrier on all the Calculation Days during the term of the Securities, you will not receive any Contingent Coupon Payments during the term of the Securities, and will not receive a positive return on the Securities.

Higher Contingent Coupon Rates are associated with greater risk. The Securities offer Contingent Coupon Payments at a higher rate, if paid, than the fixed rate we would pay on conventional debt securities of the same maturity. These higher potential Contingent Coupon Payments are associated with greater levels of expected risk as of the Pricing Date as compared to conventional debt securities, including the risk that you may not receive a Contingent Coupon Payment on one or more, or any, Contingent Coupon Payment Dates and the risk that you may lose a substantial portion, and possibly all, of the principal amount per Security at maturity. The volatility of the Underlying Stock is an important factors affecting this risk. Volatility is a measurement of the size and frequency of daily fluctuations in the price of the Underlying Stock, typically observed over a specified period of time. Volatility can be measured in a variety of ways, including on a historical basis or on an expected basis as implied by option prices in the market. Greater expected volatility of the Underlying Stock as of the Pricing Date may result in a higher Contingent Coupon Rate, but it also represents a greater expected likelihood as of the Pricing Date that the stock closing price of the Underlying Stock will be less than the Coupon Barrier on one or more Calculation Days, such that you will not receive one or more, or any, Contingent Coupon Payments during the term of the Securities, and that the stock closing price of the Underlying Stock will be less than the Threshold Price on the Final Calculation Day such that you will lose a substantial portion, and possibly all, of the principal amount per Security at maturity. In general, the higher the Contingent Coupon Rate is relative to the fixed rate we would pay on conventional debt securities, the greater the expected risk that you will not receive one or more, or any, Contingent Coupon Payments during the term of the Securities and that you will lose a substantial portion, and possibly all, of the principal amount per Security at maturity.

Your return on the Securities may be less than the yield on a conventional debt security of comparable maturity. Any return that you receive on the Securities may be less than the return you would earn if you purchased a conventional debt security with the same Maturity Date. As a result, your investment in the Securities may not reflect the full opportunity cost to you when you consider factors, such as inflation, that affect the time value of money. In addition, if interest rates increase during the term of the Securities, the Contingent Coupon Payment (if any) may be less than the yield on a conventional debt security of comparable maturity.

PS-9

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

The Contingent Coupon Payment, payment upon automatic call or Maturity Payment Amount, as applicable, will not reflect the price of the Underlying Stock other than on the Calculation Days. The price of the Underlying Stock during the term of the Securities other than on the Calculation Days will not affect payments on the Securities. Notwithstanding the foregoing, investors should generally be aware of the performance of the Underlying Stock while holding the Securities, as the performance of the Underlying Stock may influence the market value of the Securities. The calculation agent will determine whether each Contingent Coupon Payment is payable and will calculate the payment upon an automatic call or the Maturity Payment Amount, as applicable, by comparing only the Starting Price, the Coupon Barrier or the Threshold Price, as applicable, to the stock closing price on the applicable Calculation Day or the Ending Price for the Underlying Stock. No other prices of the Underlying Stock will be taken into account. As a result, if the Securities are not automatically called prior to maturity, and the Ending Price of the Underlying Stock is less than the Threshold Price, you will receive less than the principal amount at maturity even if the price of the Underlying Stock was always above the Threshold Price prior to the Final Calculation Day.

A Contingent Coupon Payment Date, a Call Settlement Date and the Maturity Date may be postponed if a Calculation Day is postponed.

A Calculation Day (including the Final Calculation Day) with respect to the Underlying Stock will be postponed if the applicable originally scheduled Calculation Day is not a trading day with respect to the Underlying Stock or if the calculation agent determines that a market disruption event has occurred or is continuing with respect to the Underlying Stock on that Calculation Day. If such a postponement occurs with respect to an Calculation Day other than the Final Calculation Day, then the related Contingent Coupon Payment Date or Call Settlement Date, as applicable, will be postponed. If such a postponement occurs with respect to the Final Calculation Day, the Maturity Date will be the later of (i) the initial Maturity Date and (ii) three business days after the last Final Calculation Day as postponed.

Any payment on the Securities is subject to our credit risk and the credit risk of the Guarantor, and actual or perceived changes in our or the Guarantor’s creditworthiness are expected to affect the value of the Securities. The Securities are our senior unsecured debt securities. Any payment on the Securities will be fully and unconditionally guaranteed by the Guarantor. The Securities are not guaranteed by any entity other than the Guarantor. As a result, your receipt of the payment upon an automatic call or the Maturity Payment Amount at maturity, as applicable, will be dependent upon our ability and the ability of the Guarantor to repay our respective obligations under the Securities on the applicable Contingent Coupon Payment Date, Call Settlement Date or the Maturity Date, regardless of the stock closing price of the Underlying Stock as compared to the Starting Price. No assurance can be given as to what our financial condition or the financial condition of the Guarantor will be at any time after the Pricing Date of the Securities. If we and the Guarantor become unable to meet our respective financial obligations as they become due, you may not receive the amount(s) payable under the terms of the Securities.

In addition, our credit ratings and the credit ratings of the Guarantor are assessments by ratings agencies of our respective abilities to pay our obligations. Consequently, our or the Guarantor’s perceived creditworthiness and actual or anticipated decreases in our or the Guarantor’s credit ratings or increases in the spread between the yield on our respective securities and the yield on U.S. Treasury securities (the “credit spread”) prior to the Maturity Date of your Securities may adversely affect the market value of the Securities. However, because your return on the Securities depends upon factors in addition to our ability and the ability of the Guarantor to pay our respective obligations, such as the price of the Underlying Stock, an improvement in our or the Guarantor’s credit ratings will not reduce the other investment risks related to the Securities.

We are a finance subsidiary and, as such, have no independent assets, operations or revenues. We are a finance subsidiary of the Guarantor, have no operations other than those related to the issuance, administration and repayment of our debt securities that are guaranteed by the Guarantor, and are dependent upon the Guarantor and/or its other subsidiaries to meet our obligations under the Securities in the ordinary course. Therefore, our ability to make payments on the Securities may be limited.

Valuation- and Market-related Risks

The public offering price you are paying for the Securities exceeds their initial estimated value. The initial estimated value of the Securities that is provided on the cover page of this pricing supplement is an estimate only, determined as of the Pricing Date by reference to our and our affiliates’ pricing models. These pricing models consider certain assumptions and variables, including our credit spreads and those of the Guarantor, the Guarantor’s internal funding rate, mid-market terms on hedging transactions, expectations on interest rates, dividends and volatility, price-sensitivity analysis, and the expected term of the Securities. These pricing models rely in part on certain forecasts about future events, which may prove to be incorrect. If you attempt to sell the Securities prior to maturity, their market value may be lower than the price you paid for them and lower than their initial estimated value. This is due to, among other things, changes in the price of the Underlying Stock, changes in the Guarantor’s internal funding rate, and the inclusion in the public offering price of the underwriting discount and the hedging related charges, all as further described in "Structuring the Securities" below. These factors, together with various credit, market and economic factors over the term of the Securities, are expected to reduce the price at which you may be able to sell the Securities in any secondary market and will affect the value of the Securities in complex and unpredictable ways.

The initial estimated value does not represent a minimum or maximum price at which we, BAC, BofAS or any of our other affiliates or WFS or its affiliates would be willing to purchase your Securities in any secondary market (if any exists) at any time. The value of your Securities at any time after issuance will vary based on many factors that cannot be predicted with accuracy, including the performance of the Underlying Stock, our and BAC’s creditworthiness and changes in market conditions.

PS-10

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

We cannot assure you that a trading market for your Securities will ever develop or be maintained. We will not list the Securities on any securities exchange. We cannot predict how the Securities will trade in any secondary market or whether that market will be liquid or illiquid.

The Securities are not designed to be short-term trading instruments, and if you attempt to sell the Securities prior to maturity, their market value, if any, will be affected by various factors that interrelate in complex ways, and their market value may be less than the principal amount. The following factors are expected to affect the value of the Securities: price of the Underlying Stock at such time; volatility of the Underlying Stock; economic and other conditions generally; interest rates; dividend yields; our and the Guarantor’s financial condition and creditworthiness; and time to maturity.

Conflict-related Risks

Trading and hedging activities by us, the Guarantor and any of our other affiliates, including BofAS, and WFS and its affiliates, may create conflicts of interest with you and may affect your return on the Securities and their market value. We, the Guarantor or one or more of our other affiliates, including BofAS, and WFS and its affiliates, may buy or sell the Underlying Stock, or futures or options contracts on the Underlying Stock, or other listed or over-the-counter derivative instruments linked to the Underlying Stock. While we, the Guarantor or one or more of our other affiliates, including BofAS, and WFS and its affiliates, may from time to time own securities represented by the Underlying Stock, we, the Guarantor and our other affiliates, including BofAS, and WFS and its affiliates, do not control the Underlying Stock Issuer, and have not verified any disclosure made by any other company. We, the Guarantor or one or more of our other affiliates, including BofAS, or WFS and its affiliates, may execute such purchases or sales for our own or their own accounts, for business reasons, or in connection with hedging our obligations under the Securities. These transactions may present a conflict of interest between your interest in the Securities and the interests we, the Guarantor and our other affiliates, including BofAS, and WFS and its affiliates, may have in our or their proprietary accounts, in facilitating transactions, including block trades, for our or their other customers, and in accounts under our or their management. These transactions may adversely affect the price of the Underlying Stock in a manner that could be adverse to your investment in the Securities. On or before the Pricing Date, any purchases or sales by us, the Guarantor or our other affiliates, including BofAS or others on its behalf, and WFS and its affiliates (including for the purpose of hedging some or all of our anticipated exposure in connection with the Securities), may have affected the price of the Underlying Stock. Consequently, the price of the Underlying Stock may change subsequent to the Pricing Date, which may adversely affect the market value of the Securities.

We, the Guarantor or one or more of our other affiliates, including BofAS, and WFS and its affiliates, also may have engaged in hedging activities that could have affected the price of the Underlying Stock on the Pricing Date. In addition, these hedging activities, including the unwinding of a hedge, may decrease the market value of your Securities prior to maturity, and may affect the amounts to be paid on the Securities. We, the Guarantor or one or more of our other affiliates, including BofAS, and WFS and its affiliates, may purchase or otherwise acquire a long or short position in the Securities and may hold or resell the Securities. For example, BofAS may enter into these transactions in connection with any market making activities in which it engages. We cannot assure you that these activities will not adversely affect the price of the Underlying Stock, the market value of your Securities prior to maturity or the amounts payable on the Securities.

If WFS, BofAS or an affiliate of either selling agent participating as a dealer in the distribution of the Securities conducts hedging activities for us in connection with the Securities, such selling agent or participating dealer will expect to realize a projected profit from such hedging activities, and this projected profit will be in addition to any discount, concession or fee received in connection with the sale of the Securities to you. This additional projected profit may create a further incentive for the selling agents or participating dealers to sell the Securities to you.

There may be potential conflicts of interest involving the calculation agent, which is an affiliate of ours. We have the right to appoint and remove the calculation agent. One of our affiliates will be the calculation agent for the Securities and, as such, will make a variety of determinations relating to the Securities, including the amounts that will be paid on the Securities. Under some circumstances, these duties could result in a conflict of interest between its status as our affiliate and its responsibilities as calculation agent.

Underlying-related Risks

Any payments on the Securities will depend upon the performance of the Underlying Stock, and therefore the Securities are subject to the following risks, each as discussed in more detail in the accompanying product supplement.

|

●

|

The Securities may become linked to the common stock of a company other than an original Underlying Stock Issuer.

|

|

●

|

We cannot control actions by the Underlying Stock Issuer.

|

|

●

|

We and our affiliates have no affiliation with the Underlying Stock Issuer and have not independently verified any public disclosure of information.

|

|

●

|

You have limited anti-dilution protection.

|

Tax-related Risks

PS-11

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

The U.S. federal income tax consequences of the Securities are uncertain, and may be adverse to a holder of the Securities. See “U.S. Federal Income Tax Summary” below and “U.S. Federal Income Tax Summary” beginning on page PS-36 of the accompanying product supplement.

PS-12

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

If the Securities are automatically called:

If the Securities are automatically called prior to the Maturity Date, you will receive the principal amount of your Securities plus a final Contingent Coupon Payment on the applicable Call Settlement Date. In the event the Securities are automatically called, your total return on the Securities will equal any Contingent Coupon Payments received prior to the Call Settlement Date and the Contingent Coupon Payment received on the Call Settlement Date.

If the Securities are not automatically called:

If the Securities are not automatically called prior to the Maturity Date, the following table illustrates, for a range of hypothetical Performance Factors of the Underlying Stock on the Final Calculation Day, the hypothetical Maturity Payment Amount payable at maturity per Security (excluding the final Contingent Coupon Payment, if any). The Performance Factor of the Underlying Stock on the Final Calculation Day is the Ending Price expressed as a percentage of the Starting Price (i.e., the Ending Price divided by the Starting Price).

|

|

|

Hypothetical Performance Factor of Underlying Stock on Final Calculation Day

|

Hypothetical Maturity Payment Amount per Security

|

|

170.00%

|

$1,000.00

|

|

160.00%

|

$1,000.00

|

|

150.00%

|

$1,000.00

|

|

140.00%

|

$1,000.00

|

|

130.00%

|

$1,000.00

|

|

120.00%

|

$1,000.00

|

|

110.00%

|

$1,000.00

|

|

100.00%

|

$1,000.00

|

|

90.00%

|

$1,000.00

|

|

80.00%

|

$1,000.00

|

|

70.00%

|

$1,000.00

|

|

69.00%

|

$690.00

|

|

60.00%

|

$600.00

|

|

50.00%

|

$500.00

|

|

40.00%

|

$400.00

|

|

30.00%

|

$300.00

|

|

25.00%

|

$250.00

|

The above figures do not take into account Contingent Coupon Payments, if any, received during the term of the Securities. As evidenced above, in no event will you have a positive rate of return based solely on the Maturity Payment Amount received at maturity; any positive return will be based solely on the Contingent Coupon Payments, if any, received during the term of the Securities.

The above figures are for purposes of illustration only and may have been rounded for ease of analysis. If the Securities are not automatically called prior to the Maturity Date, the actual amount you will receive on the Maturity Date will depend on the actual Ending Price of the Underlying Stock on the Final Calculation Day.

PS-13

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

|

|

|

|

|

|

Hypothetical Contingent Coupon Payments

|

Set forth below are examples that illustrate how to determine whether a Contingent Coupon Payment will be paid and whether the Securities will be automatically called, if applicable, on a Contingent Coupon Payment Date prior to the Maturity Date. The examples do not reflect any specific Contingent Coupon Payment Date. The following examples assume that the Securities are subject to automatic call on the applicable Calculation Day. The Securities will not be subject to automatic call until the second Calculation Day, which is approximately six months after the issue date. The following examples reflect the Contingent Coupon Rate of 20.00% per annum and assume the hypothetical Starting Price, Coupon Barrier and stock closing price for the Underlying Stock indicated in the examples. The terms used for purposes of these hypothetical examples do not represent any actual Starting Price or Coupon Barrier. The hypothetical Starting Price of $100.00 for the Underlying Stock has been chosen for illustrative purposes only and does not represent the actual Starting Price for the Underlying Stock. The actual Starting Price and Coupon Barrier for the Underlying Stock are set forth under “Terms of the Securities” above. For historical data regarding the actual Closing Price of the Underlying Stock, see the historical information provided herein. These examples are for purposes of illustration only and the values used in the examples may have been rounded for ease of analysis.

Example 1. The price of the Underlying Stock on the relevant Calculation Day is greater than or equal to the Coupon Barrier and less than the Starting Price. As a result, investors receive a Contingent Coupon Payment on the applicable Contingent Coupon Payment Date and the Securities are not automatically called.

|

|

Common Stock of Tesla Inc.

|

|

Hypothetical Starting Price:

|

$100.00

|

|

Hypothetical stock closing price on relevant Calculation Day:

|

$90.00

|

|

Hypothetical Coupon Barrier:

|

$70.00

|

|

Performance Factor (stock closing price on Calculation Day divided by Starting Price):

|

90.00%

|

Since the hypothetical stock closing price of the Underlying Stock on the relevant Calculation Day is greater than or equal to the Coupon Barrier, but less than the Starting Price, you would receive a Contingent Coupon Payment on the applicable Contingent Coupon Payment Date and the Securities would not be automatically called. The Contingent Coupon Payment would be equal to $50.00 per Security, determined as follows: (i) $1,000 multiplied by 20.00% per annum divided by (ii) 4, rounded to the nearest cent.

Example 2. The price of the Underlying Stock on the relevant Calculation Day is less than the Coupon Barrier and the Starting Price. As a result, investors do not receive a Contingent Coupon Payment on the applicable Contingent Coupon Payment Date and the Securities are not automatically called.

|

|

Common Stock of Tesla Inc.

|

|

Hypothetical Starting Price:

|

$100.00

|

|

Hypothetical stock closing price on relevant Calculation Day:

|

$69.00

|

|

Hypothetical Coupon Barrier:

|

$70.00

|

|

Performance Factor (stock closing price on Calculation Day divided by Starting Price):

|

69.00%

|

Since the hypothetical stock closing price of the Underlying Stock on the relevant Calculation Day is less than the Coupon Barrier, you would not receive a Contingent Coupon Payment on the applicable Contingent Coupon Payment Date. In addition, because the hypothetical stock closing price of the Underlying Stock also is less than the Starting Price, the Securities would not be automatically called.

Example 3. The price of the Underlying Stock on the relevant Calculation Day is greater than or equal to the Starting Price. As a result, the Securities are automatically called on the applicable Contingent Coupon Payment Date for the principal amount plus a final Contingent Coupon Payment.

|

|

Common Stock of Tesla Inc.

|

|

Hypothetical Starting Price:

|

$100.00

|

|

Hypothetical stock closing price on relevant Calculation Day:

|

$115.00

|

|

Hypothetical Coupon Barrier:

|

$70.00

|

|

Performance Factor (stock closing price on Calculation Day divided by Starting Price):

|

115.00%

|

Since the hypothetical stock closing price of the Underlying Stock on the relevant Calculation Day is greater than or equal to the Starting Price, the Securities would be automatically called and you would receive the principal amount plus a final Contingent

PS-14

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

Coupon Payment on the applicable Contingent Coupon Payment Date, which is also referred to as the Call Settlement Date. On the Call Settlement Date, you would receive $1,050.00 per Security.

You will not receive any further payments after the Call Settlement Date.

PS-15

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

|

|

|

|

Hypothetical Payment at the Maturity Date

|

Set forth below are examples of calculations of the Maturity Payment Amount payable on the Maturity Date, assuming that the Securities have not been automatically called prior to the Maturity Date and assuming the hypothetical Starting Price, Coupon Barrier, Threshold Price and Ending Price for the Underlying Stock indicated in the examples. The terms used for purposes of these hypothetical examples do not represent any actual Starting Price, Coupon Barrier or Threshold Price. The hypothetical Starting Price of 100.00 for the Underlying Stock has been chosen for illustrative purposes only and does not represent the actual Starting Price for the Underlying Stock. The actual Starting Price, Coupon Barrier and Threshold Price for the Underlying Stock are set forth under “Terms of the Securities” above. For historical data regarding the actual closing price of the Underlying Stock, see the historical information provided herein. These examples are for purposes of illustration only and the values used in the examples may have been rounded for ease of analysis.

Example 1. The Ending Price of the Underlying Stock on the Final Calculation Day is greater than the Starting Price, the Maturity Payment Amount is equal to the principal amount of your Securities at maturity and you receive a final Contingent Coupon Payment:

|

|

Common Stock of Tesla Inc.

|

|

Hypothetical Starting Price:

|

$100.00

|

|

Hypothetical Ending Price:

|

$145.00

|

|

Hypothetical Coupon Barrier:

|

$70.00

|

|

Hypothetical Threshold Price:

|

$70.00

|

|

Performance Factor (Ending Price divided by Starting Price):

|

145.00%

|

Since the hypothetical Ending Price of the Underlying Stock on the Final Calculation Day is greater than the hypothetical Threshold Price, the Maturity Payment Amount would equal the principal amount. Although the hypothetical Ending Price of the Underlying Stock on the Final Calculation Day is significantly greater than the hypothetical Starting Price in this scenario, the Maturity Payment Amount will not exceed the principal amount.

In addition to any Contingent Coupon Payments received during the term of the Securities, on the Maturity Date you would receive $1,000 per Security. In addition, because the hypothetical Ending Price of the Underlying Stock on the Final Calculation Day is greater than the Coupon Barrier, you would receive a final Contingent Coupon Payment on the Maturity Date.

Example 2. The Ending Price of the Underlying Stock on the Final Calculation Day is less than the Starting Price but greater than the Threshold Price and the Coupon Barrier, the Maturity Payment Amount is equal to the principal amount of your Securities at maturity and you receive a final Contingent Coupon Payment:

|

|

Common Stock of Tesla Inc.

|

|

Hypothetical Starting Price:

|

$100.00

|

|

Hypothetical Ending Price:

|

$80.00

|

|

Hypothetical Coupon Barrier:

|

$70.00

|

|

Hypothetical Threshold Price:

|

$70.00

|

|

Performance Factor (Ending Price divided by Starting Price):

|

80.00%

|

Since the hypothetical Ending Price of the Underlying Stock is less than the hypothetical Starting Price, but not by more than 30%, you would be repaid the principal amount of your Securities at maturity.

In addition to any Contingent Coupon Payments received during the term of the Securities, on the Maturity Date you would receive $1,000 per Security. In addition, because the hypothetical Ending Price of the Underlying Stock on the Final Calculation Day is greater than the Coupon Barrier, you would receive a final Contingent Coupon Payment on the Maturity Date.

PS-16

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

Example 3. The Ending Price of the Underlying Stock on the Final Calculation Day is less than the Threshold Price and the Coupon Barrier, the Maturity Payment Amount is less than the principal amount of your Securities at maturity and you do not receive a final Contingent Coupon Payment:

|

|

Common Stock of Tesla Inc.

|

|

Hypothetical Starting Price:

|

$100.00

|

|

Hypothetical Ending Price:

|

$45.00

|

|

Hypothetical Coupon Barrier:

|

$70.00

|

|

Hypothetical Threshold Price:

|

$70.00

|

|

Performance Factor (Ending Price divided by Starting Price):

|

45.00%

|

Since the hypothetical Ending Price of the Underlying Stock on the Final Calculation Day is less than the hypothetical Starting Price by more than 30%, you would lose a portion of the principal amount of your Securities and receive the Maturity Payment Amount equal to $450.00 per Security, calculated as follows:

= $1,000 × Performance Factor of the Underlying Stock on the Final Calculation Day

= $1,000 × 45.00%

= $450.00

In addition to any Contingent Coupon Payments received during the term of the Securities, on the Maturity Date you would receive $450.00 per Security. Because the hypothetical Ending Price of the Underlying Stock on the Final Calculation Day is less than the Coupon Barrier, you would not receive a final Contingent Coupon Payment on the Maturity Date.

These examples illustrate that you will not participate in any appreciation of the Underlying Stock, but will be fully exposed to a decrease in the Underlying Stock if the Ending Price of the Underlying Stock on the Final Calculation Day is less than the Threshold Price.

To the extent that the Starting Price, Coupon Barrier, Threshold Price and Ending Price of the Underlying Stock differ from the values assumed above, the results indicated above would be different.

PS-17

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

|

|

|

All disclosures contained in this pricing supplement regarding the Underlying Stock and the Underlying Stock Issuer, have been derived from publicly available sources. Because the Underlying Stock are registered under the Securities Exchange Act of 1934, the Underlying Stock Issuer is required to periodically file certain financial and other information specified by the Securities and Exchange Commission (SEC). Information provided to or filed with the SEC by the Underlying Stock Issuer can be located through the SEC’s website at sec.gov by reference to the CIK number set forth below. This document relates only to the offering of the Securities and does not relate to any offering of Underlying Stock or any other securities of the Underlying Stock Issuer. None of us, the Guarantor, BofAS or any of our other affiliates has made any due diligence inquiry with respect to the Underlying Stock Issuer in connection with the offering of the Securities. None of us, the Guarantor, BofAS or any of our other affiliates has independently verified the accuracy or completeness of the publicly available documents or any other publicly available information regarding the Underlying Stock Issuer and hence makes no representation regarding the same. Furthermore, there can be no assurance that all events occurring prior to the date of this document, including events that would affect the accuracy or completeness of these publicly available documents that could affect the trading price of the Underlying Stock, have been or will be publicly disclosed. Subsequent disclosure of any events or the disclosure of or failure to disclose material future events concerning the Underlying Stock Issue could affect the price of the Underlying Stock and therefore could affect your return on the Securities. The selection of the Underlying Stock is not a recommendation to buy or sell the Underlying Stock.

None of us, the Guarantor, BofAS or any of our other affiliates makes any representation to you as to the future performance of the Underlying Stock. You should make your own investigation into the Underlying Stock.

The Common Stock of Tesla Inc.

Tesla Inc. designs, manufactures, and sells high-performance electric vehicles and electric vehicle powertrain components. The company owns its sales and service network and sells electric powertrain components to other automobile manufacturers. Tesla serves customers worldwide. This Underlying Stock trades on the Nasdaq Global Select Market under the symbol "TSLA." The company's CIK number is 0001318605 and its SEC file number is 001-34756.

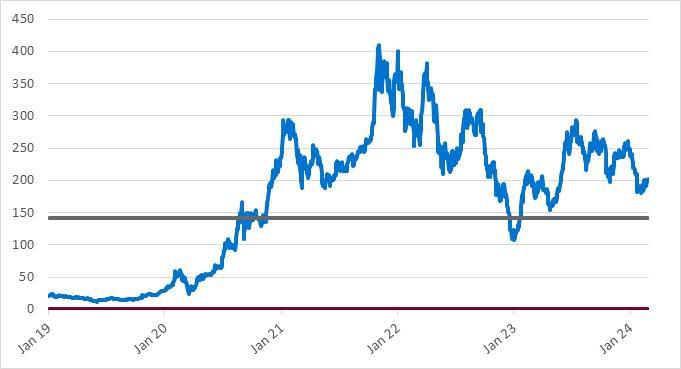

Historical Information

The following graph sets forth the daily historical performance of TSLA in the period from January 2, 2019 through the Pricing Date. We obtained this historical data from Bloomberg L.P. We have not independently verified the accuracy or completeness of the information obtained from Bloomberg L.P. The horizontal line in the graph represents TSLA’s Coupon Barrier and hypothetical Threshold Price of $141.316, which is 70.00% of TSLA’s Starting Price of $201.88.

This historical data on TSLA is not necessarily indicative of the future performance of TSLA or what the value of the Securities may be. Any historical upward or downward trend in the price of TSLA during any period set forth above is not an indication that the price of TSLA is more or less likely to increase or decrease at any time over the term of the Securities.

Before investing in the Securities, you should consult publicly available sources for the prices of TSLA.

PS-18

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

|

|

|

|

Structuring the Securities

|

The Securities are our debt securities, the return on which is linked to the performance of the Underlying Stock. The related guarantee is BAC’s obligation. Any payments on the Securities, including payment of the Maturity Payment Amount, depend on the credit risk of BofA Finance and BAC and on the performance of the Underlying Stock. As is the case for all of our and BAC’s respective debt securities, including our market-linked securities, the economic terms of the Securities reflect our and BAC’s actual or perceived creditworthiness at the time of pricing. In addition, because market-linked securities result in increased operational, funding and liability management costs to us and BAC, BAC typically borrows the funds under these types of securities at a rate, which we refer to in this pricing supplement as BAC’s internal funding rate, that is more favorable to BAC than the rate that it might pay for a conventional fixed or floating rate debt security. This generally relatively lower internal funding rate, which is reflected in the economic terms of the Securities, along with the fees and charges associated with market-linked securities, resulted in the initial estimated value of the Securities on the Pricing Date being less than their public offering price.

The initial estimated value of the Securities as of the Pricing Date is set forth on the cover page of this pricing supplement.

In order to meet our payment obligations on the Securities, at the time we issue the Securities, we may choose to enter into certain hedging arrangements (which may include call options, put options or other derivatives) with BofAS or one of our other affiliates. The terms of these hedging arrangements are determined based upon terms provided by BofAS and its affiliates, and take into account a number of factors, including our and BAC’s creditworthiness, interest rate movements, the volatility of the Underlying Stock, the tenor of the Securities and the hedging arrangements. The economic terms of the Securities and their initial estimated value depend in part on the terms of these hedging arrangements.

BofAS has advised us that the hedging arrangements will include hedging related charges, reflecting the costs associated with, and our affiliates’ profit earned from, these hedging arrangements. Since hedging entails risk and may be influenced by unpredictable market forces, actual profits or losses from these hedging transactions may be more or less than any expected amounts.

For further information, see “Selected Risk Considerations” beginning on page PS-9 above and “Use of Proceeds” on page PS-17 of the accompanying prospectus.

|

Validity of the Securities

|

In the opinion of McGuireWoods LLP, as counsel to BofA Finance, as issuer, and BAC, as guarantor, when the trustee has made the appropriate entries or notations on Schedule 1 to the master global note that represents the Securities (the “Master Note”) identifying the Securities offered hereby as supplemental obligations thereunder in accordance with the instructions of BofA Finance, and the Securities have been delivered against payment therefor as contemplated in this pricing supplement and the related prospectus, prospectus supplement and product supplement, all in accordance with the provisions of the indenture governing the Securities and the related guarantee, such Securities will be the legal, valid and binding obligations of BofA Finance, and the related guarantee will be the legal, valid and binding obligation of BAC, subject, in each case, to the effects of applicable bankruptcy, insolvency (including laws relating to preferences, fraudulent transfers and equitable subordination), reorganization, moratorium and other similar laws affecting creditors’ rights generally, and to general principles of equity. This opinion is given as of the date of this pricing supplement and is limited to the Delaware General Corporation Law and the Delaware Limited Liability Company Act (including the statutory provisions, all applicable provisions of the Delaware Constitution and reported judicial decisions interpreting either of the foregoing) and the laws of the State of New York as in effect on the date hereof. In addition, this opinion is subject to customary assumptions about the trustee’s authorization, execution and delivery of the indenture governing the Securities and due authentication of the Master Note, the validity, binding nature and enforceability of the indenture governing the Securities and the related guarantee with respect to the trustee, the legal capacity of individuals, the genuineness of signatures, the authenticity of all documents submitted to McGuireWoods LLP as originals, the conformity to original documents of all documents submitted to McGuireWoods LLP as copies thereof, the authenticity of the originals of such copies and certain factual matters, all as stated in the opinion letter of McGuireWoods LLP dated December 8, 2022, which has been filed as an exhibit to the Registration Statement (File Nos. 333-268718 and 333-268718-01) of BAC and BofA Finance, filed with the SEC on December 8, 2022

PS-19

|

Market Linked Securities—Auto-Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Common Stock of Tesla Inc. due March 2, 2028

|

|

|

|

|

|

|

U.S. Federal Income Tax Summary

|

You should consider the U.S. federal income tax consequences of an investment in the Securities, including the following:

|

•

|

There is no statutory, judicial, or administrative authority directly addressing the characterization of the Securities.

|

|

•

|

You agree with us (in the absence of an administrative determination, or judicial ruling to the contrary) to characterize and treat the Securities for all tax purposes as contingent income-bearing single financial contracts with respect to the Underlying Stock. In the opinion of Sidley Austin LLP, our tax counsel, the U.S. federal income tax characterization and treatment of the Securities described herein is a reasonable interpretation of current law.

|

|

•

|

Under this characterization and tax treatment of the Securities, a U.S. Holder (as defined on page 71 of the accompanying prospectus) generally will recognize capital gain or loss upon maturity or upon a sale, exchange or redemption of the Securities prior to maturity. This capital gain or loss generally will be long-term capital gain or loss if you hold the Securities for more than one year.

|

|

•

|

No assurance can be given that the Internal Revenue Service (“IRS”) or any court will agree with this characterization and tax treatment.

|

|

•

|

We intend to take the position that any Contingent Coupon Payments constitute taxable ordinary income to a U.S. Holder at the time received or accrued, in accordance with the U.S. Holder’s method of tax accounting.

|

|

•

|

We intend to treat any Contingent Coupon Payment made to Non-U.S. Holders (as defined on page 71 of the accompanying prospectus) as generally subject to withholding at a 30% rate (or at a lower rate under an applicable income tax treaty) on the entire amount of any Contingent Coupon Payment made unless such payments are effectively connected with the conduct by the Non-U.S. Holder of a trade or business in the U.S. (in which case, to avoid withholding, the Non-U.S. Holder will be required to provide a Form W-8ECI). We (or the applicable paying agent) will not pay any additional amounts in respect of such withholding.

|

|

•

|

Under current IRS guidance, withholding on “dividend equivalent” payments (as discussed in the accompanying product supplement), if any, will not apply to Securities that are issued as of the date of this pricing supplement unless such Securities are “delta-one” instruments.

|

You should consult your own tax advisor concerning the U.S. federal income tax consequences to you of acquiring, owning, and disposing of the Securities, as well as any tax consequences arising under the laws of any state, local, foreign, or other tax jurisdiction and the possible effects of changes in U.S. federal or other tax laws. You should review carefully the discussion under the section entitled “U.S. Federal Income Tax Summary” beginning on page PS-36 of the accompanying product supplement.

PS-20