| |

Filed Pursuant to Rule 424(b)(2)

Registration Nos. 333-268718 and 333-268718-01 |

| |

|

|

Dated June 28, 2024

(To Prospectus dated December 30, 2022,

Series A Prospectus Supplement dated December 30, 2022 and

Product Supplement No. WF-1 dated March 8, 2023)

|

|

|

|

|

|

BofA Finance LLC

Medium-Term Notes, Series A

Fully and Unconditionally Guaranteed by Bank of America Corporation |

|

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

$3,068,000 Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028 |

■ Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® (each referred to as an “Underlying”)

■ The Securities are redeemable debt securities that, unlike ordinary debt securities, do not provide for fixed payments of interest and do not repay a fixed amount of principal at maturity. Whether the Securities pay a Contingent Coupon and, if they are not redeemed prior to the Maturity Date, whether you are repaid the principal amount of your Securities at maturity will depend, in each case, on the closing level of the Lowest Performing Underlying on the relevant Calculation Day. The Lowest Performing Underlying on any Calculation Day is the Underlying that has the lowest closing level on that Calculation Day as a percentage of its Starting Value

■ Contingent Coupon. The Securities will pay a Contingent Coupon Payment on a quarterly basis until the earlier of the Maturity Date or early redemption if, and only if, the closing level of the Lowest Performing Underlying on the Calculation Day for that quarter is greater than or equal to its Coupon Barrier. However, if the closing level of the Lowest Performing Underlying on a Calculation Day is less than its Coupon Barrier, you will not receive any Contingent Coupon Payment for the relevant quarter. If the closing level of the Lowest Performing Underlying is less than its Coupon Barrier on every Calculation Day, you will not receive any Contingent Coupon Payments throughout the entire term of the Securities. The Coupon Barrier for each Underlying is equal to 75% of its Starting Value. The Contingent Coupon Rate is 8.15% per annum

■ Optional Redemption. We may, at our option, redeem the Securities on any Contingent Coupon Payment Date beginning approximately six months after issuance. If we elect to redeem the Securities prior to the Maturity Date, you will receive the principal amount plus any Contingent Coupon Payment otherwise due

■ Potential Loss of Principal. If we do not redeem the Securities prior to the Maturity Date, you will receive the principal amount on the Maturity Date if, and only if, the closing level of the Lowest Performing Underlying on the Final Calculation Day is greater than or equal to its Threshold Value. If the closing level of the Lowest Performing Underlying on the Final Calculation Day is less than its Threshold Value, you will lose more than 25%, and possibly all, of the principal amount of your Securities. The Threshold Value for each Underlying is equal to 75% of its Starting Value

■ If we do not redeem the Securities prior to the Maturity Date, you will have full downside exposure to the Lowest Performing Underlying from its Starting Value if its closing level on the Final Calculation Day is less than its Threshold Value, but you will not participate in any appreciation of any Underlying and will not receive any dividends on securities included in any Underlying

■ Your return on the Securities will depend solely on the performance of the Underlying that is the Lowest Performing Underlying on each Calculation Day. You will not benefit in any way from the performance of the better performing Underlyings. Therefore, you will be adversely affected if any Underlying performs poorly, even if the other Underlyings perform favorably

■ All payments on the Securities are subject to the credit risk of BofA Finance LLC (“BofA Finance”), as issuer of the Securities, and Bank of America Corporation (“BAC” or the “Guarantor”), as guarantor of the Securities

■ Securities will not be listed on any securities exchange |

The initial estimated value of the Securities as of the Pricing Date is $960.10 per Security, which is less than the public offering price listed below. The actual value of your Securities at any time will reflect many factors and cannot be predicted with accuracy. See “Selected Risk Considerations” beginning on page PS-9 of this pricing supplement and “Structuring the Securities” on page PS-27 of this pricing supplement for additional information.

The Securities have complex features and investing in the Securities involves risks not associated with an investment in conventional debt securities. Potential purchasers of the Securities should consider the information in “Selected Risk Considerations” beginning on page PS-9 herein and “Risk Factors” beginning on page PS-5 of the accompanying product supplement, page S-6 of the accompanying prospectus supplement, and page 7 of the accompanying prospectus.

None of the Securities and Exchange Commission (the “SEC”), any state securities commission, or any other regulatory body has approved or disapproved of these Securities or determined if this pricing supplement and the accompanying product supplement, prospectus supplement and prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

|

Public offering price |

Underwriting Discount(1)(2) |

Proceeds, before expenses, to BofA Finance |

Per Security |

$1,000.00 |

$23.25 |

$976.75 |

Total |

$3,068,000 |

$71,331.00 |

$2,996,669.00 |

(1) |

Wells Fargo Securities, LLC and BofA Securities, Inc. are the selling agents for the distribution of the Securities and are acting as principal. See “Terms of the Securities—Selling Agents” in this pricing supplement for further information. |

(2) |

In addition, in respect of certain Securities sold in this offering, BofA Securities, Inc. or its affiliates may pay a fee of up to $2.00 per Security to selected securities dealers in consideration for marketing and other services in connection with the distribution of the Securities to other securities dealers. |

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028

Issuer: |

BofA Finance LLC. |

Guarantor: |

BAC. |

Underlyings: |

The S&P 500® Index (Bloomberg symbol: “SPX”), the Russell 2000® Index (Bloomberg symbol: “RTY”) and the Dow Jones Industrial Average® (Bloomberg symbol: “INDU”), each a price return index. |

Pricing Date: |

June 28, 2024. |

Issue Date: |

July 3, 2024. |

Maturity Date: |

June 29, 2028, subject to postponement as described below in “—Market Disruption Events and Postponement Provisions”. The Securities are not subject to repayment at the option of any holder of the Securities prior to the Maturity Date. |

Denominations: |

$1,000 and any integral multiple of $1,000. References in this pricing supplement to a “Security” are to a Security with a principal amount of $1,000. |

Contingent Coupon Payment: |

On each Contingent Coupon Payment Date, unless the Securities have been previously redeemed, you will receive a Contingent Coupon Payment at a per annum rate equal to the Contingent Coupon Rate if, and only if, the closing level of the Lowest Performing Underlying on the related Calculation Day is greater than or equal to its Coupon Barrier. Each “Contingent Coupon Payment,” if any, will be calculated per Security as follows: ($1,000 × Contingent Coupon Rate)/4. Any Contingent Coupon Payment will be rounded to the nearest cent, with one-half cent rounded upward.

If the closing level of the Lowest Performing Underlying on any Calculation Day is less than its Coupon Barrier, you will not receive any Contingent Coupon Payment on the related Contingent Coupon Payment Date. If the closing level of the Lowest Performing Underlying is less than its Coupon Barrier on all Calculation Days, you will not receive any Contingent Coupon Payments over the term of the Securities.

|

Contingent Coupon Payment Dates: |

Quarterly, on the third business day following each Calculation Day (as each such Calculation Day may be postponed pursuant to “—Market Disruption Events and Postponement Provisions” below, if applicable); provided that the Contingent Coupon Payment Date with respect to the Final Calculation Day will be the Maturity Date. |

Contingent Coupon Rate: |

The “Contingent Coupon Rate” is 8.15% per annum (equal to 2.0375% per quarter). |

Calculation Days: |

Quarterly, on the 24th of each March, June, September and December, commencing September 2024 and ending March 2028, and the Final Calculation Day, each subject to postponement as described below under “—Market Disruption Events and Postponement Provisions.” We refer to June 26, 2028 as the “Final Calculation Day.” |

Optional Redemption: |

We may, at our option, redeem the Securities, in whole but not in part, on any Optional Redemption Date. If we elect to redeem the Securities prior to the Maturity Date, you will be entitled to receive on the applicable Optional Redemption Date a cash payment per Security in U.S. dollars equal to the principal amount plus any Contingent Coupon Payment otherwise due.

If we elect to redeem the Securities on an Optional Redemption Date, we will give you notice at least five business days but not more than 60 calendar days before the Optional Redemption Date. Any redemption of the Securities will be at our option and will not automatically occur based on the performance of any Underlying.

If the Securities are redeemed, they will cease to be outstanding on the applicable Optional Redemption Date and you will have no further rights under the Securities after that date. |

Optional Redemption Dates: |

Quarterly, beginning approximately six months after the issue date, on the Contingent Coupon Payment Dates following each Calculation Day scheduled to occur from December 2024 to March 2028, inclusive. |

PS-2

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028

Maturity Payment Amount: |

If we do not redeem the Securities prior to the Maturity Date, you will be entitled to receive on the Maturity Date a cash payment per Security in U.S. dollars equal to the Maturity Payment Amount (in addition to the final Contingent Coupon Payment, if any). The “Maturity Payment Amount” per Security will equal:

• if the Ending Value of the Lowest Performing Underlying on the Final Calculation Day is greater than or equal to its Threshold Value:

$1,000; or

• if the Ending Value of the Lowest Performing Underlying on the Final Calculation Day is less than its Threshold Value: |

$1,000 × Performance Factor of the Lowest Performing Underlying on the Final Calculation Day |

If we do not redeem the Securities prior to the Maturity Date and the Ending Value of the Lowest Performing Underlying on the Final Calculation Day is less than its Threshold Value, you will lose more than 25%, and possibly all, of the principal amount of your Securities on the Maturity Date.

Any return on the Securities will be limited to the sum of your Contingent Coupon Payments, if any. You will not participate in any appreciation of any Underlying, but you will have full downside exposure to decreases in the value of the Lowest Performing Underlying on the Final Calculation Day if the Ending Value of that Underlying is less than its Threshold Value. |

Lowest Performing Underlying: |

For any Calculation Day, the “Lowest Performing Underlying” will be the Underlying with the lowest Performance Factor on that Calculation Day. |

Performance Factor: |

With respect to an Underlying on any Calculation Day, its closing level on such Calculation Day divided by its Starting Value (expressed as a percentage). |

Closing Level: |

With respect to each Underlying, closing level has the meaning set forth under “General Terms of the Securities—Certain Terms for Securities Linked to an Index—Certain Definitions” in the accompanying product supplement. |

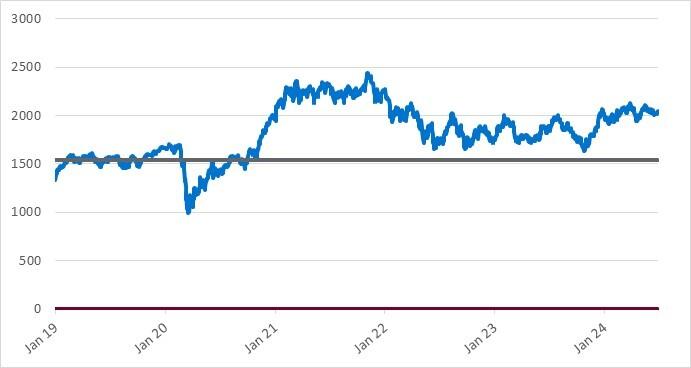

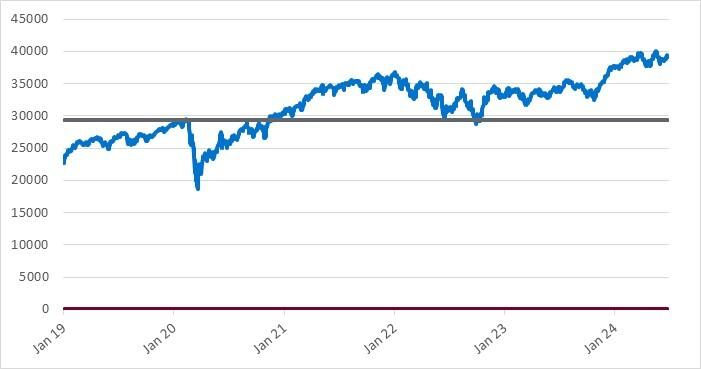

Starting Value: |

With respect to the S&P 500® Index: 5,460.48, its closing level on the Pricing Date.

With respect to the Russell 2000® Index: 2,047.691, its closing level on the Pricing Date.

With respect to the Dow Jones Industrial Average®: 39,118.86, its closing level on the Pricing Date. |

Ending Value: |

With respect to each Underlying, its closing level on the Final Calculation Day. |

Coupon Barrier: |

With respect to the S&P 500® Index: 4,095.36, which is equal to 75% of its Starting Value.

With respect to the Russell 2000® Index: 1,535.76825, which is equal to 75% of its Starting Value.

With respect to the Dow Jones Industrial Average®: 29,339.145, which is equal to 75% of its Starting Value. |

Threshold Value: |

With respect to the S&P 500® Index: 4,095.36, which is equal to 75% of its Starting Value.

With respect to the Russell 2000® Index: 1,535.76825, which is equal to 75% of its Starting Value.

With respect to the Dow Jones Industrial Average®: 29,339.145, which is equal to 75% of its Starting Value. |

Market Disruption Events and Postponement Provisions: |

Each Calculation Day is subject to postponement due to non-trading days and the occurrence of a Market Disruption Event. In addition, the Maturity Date will be postponed if the Final Calculation Day is postponed and will be adjusted for non-business days. For more information regarding adjustments to the Calculation Days and the Maturity Date, see “General Terms of the Securities—Consequences of a Market Disruption Event; Postponement of a Calculation Day—Securities Linked to Multiple Market Measures” and “—Payment Dates” in the accompanying product supplement. For purposes of the accompanying product supplement, each Contingent Coupon Payment Date, each Optional Redemption Date and the Maturity Date is a “payment date.” In addition, for information regarding the circumstances that may result in a Market Disruption Event, see “General Terms of the Securities—Certain Terms for Securities Linked to an Index—Market Disruption Events” in the accompanying product supplement. |

Calculation Agent: |

BofA Securities, Inc. (“BofAS”), an affiliate of BofA Finance. |

PS-3

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028

Selling Agents: |

BofAS and Wells Fargo Securities, LLC (“WFS”).

Under our distribution agreement with BofAS, BofAS will purchase the Securities from us as principal at the public offering price indicated on the cover of this pricing supplement, less the indicated underwriting discount. BofAS will sell the Securities to WFS at the public offering price of the Securities less a concession of up to $23.25 per Security. WFS will provide dealers, which may include Wells Fargo Advisors (“WFA”) (the trade name of the retail brokerage business of WFS’s affiliates, Wells Fargo Clearing Services, LLC and Wells Fargo Advisors Financial Network, LLC), with a selling concession of up to $17.50 per Security. In addition to the concession allowed to WFA, WFS may pay up to $0.75 per Security to WFA as a distribution expense fee for each Security sold by WFA.

In addition, in respect of certain Securities sold in this offering, BofAS or its affiliates may pay a fee of up to $2.00 per Security to selected securities dealers in consideration for marketing and other services in connection with the distribution of the Securities to other securities dealers.

WFS has advised us that if it, WFA or any of their affiliates makes a secondary market in the Securities at any time up to the Issue Date or during the four-month period following the Issue Date, the secondary market price offered by it, WFA or any of their affiliates will be increased by an amount reflecting a portion of the costs associated with selling, structuring and hedging the Securities that are included in the public offering price of the Securities. Because this portion of the costs is not fully deducted upon issuance, WFS has advised us that any secondary market price it, WFA or any of their affiliates offers during this period will be higher than it otherwise would be outside of this period, as any secondary market price offered outside of this period will reflect the full deduction of the costs as described above. WFS has advised us that the amount of this increase in the secondary market price will decline steadily to zero over this four-month period. If you hold the Securities through an account at WFS, WFA or any of their affiliates, WFS has advised us that it expects that this increase will also be reflected in the value indicated for the Securities on your brokerage account statement. If you hold your Securities through an account at a broker-dealer other than WFS, WFA or any of their affiliates, the value of the Securities on your brokerage account statement may be different than if you held your Securities at WFS, WFA or any of their affiliates.

|

Material Tax

Consequences: |

For a discussion of the material U.S. federal income and estate tax consequences of the ownership and disposition of the Securities, see “U.S. Federal Income Tax Summary.” |

CUSIP: |

09711DHX3 |

|

|

|

|

|

|

|

|

|

|

PS-4

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028

Additional Information about BofA Finance, the Guarantor and the Securities |

The terms and risks of the Securities are contained in this pricing supplement and in the following related product supplement, prospectus supplement and prospectus. Information included in this pricing supplement supersedes information in the product supplement, prospectus supplement and prospectus to the extent that it is different from that information. These documents can be accessed at the following links:

• |

Product Supplement No. WF-1 dated March 8, 2023: |

These documents have been filed as part of a registration statement with the SEC, which may, without cost, be accessed on the SEC website at www.sec.gov or obtained from BofAS by calling 1-800-294-1322. Before you invest, you should read this pricing supplement and the accompanying product supplement, prospectus supplement and prospectus for information about us, BAC and this offering. Any prior or contemporaneous oral statements and any other written materials you may have received are superseded by this pricing supplement and the accompanying product supplement, prospectus supplement and prospectus. Certain terms used but not defined in this pricing supplement have the meanings set forth in the accompanying product supplement or prospectus supplement. Unless otherwise indicated or unless the context requires otherwise, all references in this document to “we,” “us,” “our,” or similar references are to BofA Finance, and not to BAC.

The Securities are our senior debt securities. Any payments on the Securities are fully and unconditionally guaranteed by BAC. The Securities and the related guarantee are not insured by the Federal Deposit Insurance Corporation or secured by collateral. The Securities will rank equally in right of payment with all of our other unsecured and unsubordinated obligations, except obligations that are subject to any priorities or preferences by law. The related guarantee will rank equally in right of payment with all of BAC’s other unsecured and unsubordinated obligations, except obligations that are subject to any priorities or preferences by law, and senior to its subordinated obligations. Any payments due on the Securities, including any repayment of the principal amount, will be subject to the credit risk of BofA Finance, as issuer, and BAC, as guarantor.

PS-5

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028

The Securities are not appropriate for all investors. The Securities may be an appropriate investment for investors who:

■ seek an investment with Contingent Coupon Payments at a rate of 8.15% per annum until the earlier of the Maturity Date or optional redemption, if, and only if, the closing level of the Lowest Performing Underlying on the applicable Calculation Day is greater than or equal to 75% of its Starting Value;

■ understand that if the Ending Value of the Lowest Performing Underlying on the Final Calculation Day has declined by more than 25% from its Starting Value, they will be fully exposed to the decline in the Lowest Performing Underlying from its Starting Value and will lose more than 25%, and possibly all, of the principal amount of their Securities at maturity;

■ are willing to accept the risk that they may receive few or no Contingent Coupon Payments over the term of the Securities;

■ understand that we may redeem the Securities prior to the Maturity Date at our option beginning approximately six months after issuance, that the term of the Securities may be as short as approximately six months, and that it is more likely that we will redeem the Securities when it would otherwise be advantageous for you to continue to hold the Securities;

■ understand that the return on the Securities will depend solely on the performance of the Underlying that is the Lowest Performing Underlying on each Calculation Day (including the Final Calculation Day) and that they will not benefit in any way from the performance of the better performing Underlyings;

■ understand that the Securities are riskier than alternative investments linked to only one of the Underlyings or linked to a basket composed of each Underlying;

■ understand and are willing to accept the full downside risks of each Underlying;

■ are willing to forgo participation in any appreciation of any Underlying and dividends on securities included in the Underlyings; and

■ are willing to hold the Securities until maturity.

The Securities may not be an appropriate investment for investors who:

■ seek a liquid investment or are unable or unwilling to hold the Securities to maturity;

■ require full payment of the principal amount of the Securities at maturity;

■ seek a security with a fixed term;

■ are unwilling to purchase Securities with an estimated value as of the Pricing Date that is lower than the public offering price set forth on the cover page;

■ are unwilling to accept the risk that the closing level of the Lowest Performing Underlying on the Final Calculation Day may decline by more than 25% from its Starting Value;

■ seek certainty of current income over the term of the Securities;

■ seek exposure to the upside performance of any or each Underlying;

■ seek exposure to a basket composed of each Underlying or a similar investment in which the overall return is based on a blend of the performances of the Underlyings, rather than solely on the Lowest Performing Underlying;

■ are unwilling to accept the risk of exposure to the Underlyings;

■ are unwilling to accept the credit risk of BofA Finance, as issuer, and BAC, as guarantor, to obtain exposure to the Underlyings generally, or to obtain exposure to the Underlyings that the Securities provide specifically; or

■ prefer the lower risk of conventional fixed income investments with comparable maturities issued by companies with comparable credit ratings.

The considerations identified above are not exhaustive. Whether or not the Securities are an appropriate investment for you will depend on your individual circumstances, and you should reach an investment decision only after you and your investment, legal, tax, accounting and other advisors have carefully considered the appropriateness of an investment in the Securities in light of your particular circumstances. You should also review carefully “Selected Risk Considerations” herein and “Risk Factors” in each of the accompanying product supplement, prospectus supplement and prospectus for risks related to an investment in the Securities. For more information about the Underlyings, please see the sections titled “The S&P 500® Index,” “The Russell 2000® Index” and “The Dow Jones Industrial Average®” below.

PS-6

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028

|

Determining Payment On A Contingent Coupon Payment Date and at Maturity |

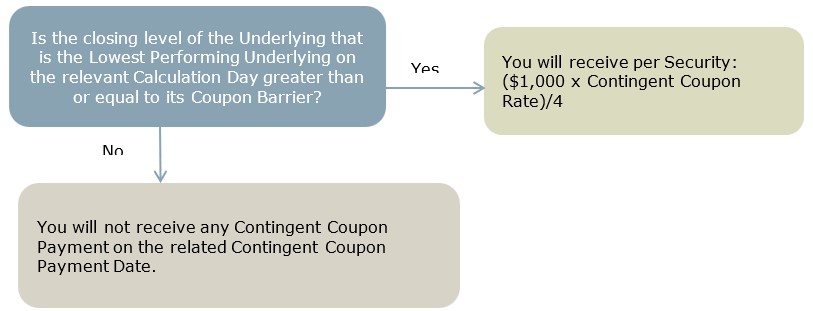

Unless we have previously redeemed the Securities at our option, on each Contingent Coupon Payment Date, either you will receive a Contingent Coupon Payment or you will not receive a Contingent Coupon Payment, depending on the closing level of the Lowest Performing Underlying on the related Calculation Day.

Step 1: Determine which Underlying is the Lowest Performing Underlying on the relevant Calculation Day. The Lowest Performing Underlying on any Calculation Day is the Underlying with the lowest Performance Factor on that Calculation Day. The Performance Factor of an Underlying on a Calculation Day is its closing level on that Calculation Day as a percentage of its Starting Value (i.e., its closing level on that Calculation Day divided by its Starting Value).

Step 2: Determine whether a Contingent Coupon Payment is paid on the applicable Contingent Coupon Payment Date based on the closing level of the Lowest Performing Underlying on the relevant Calculation Day, as follows:

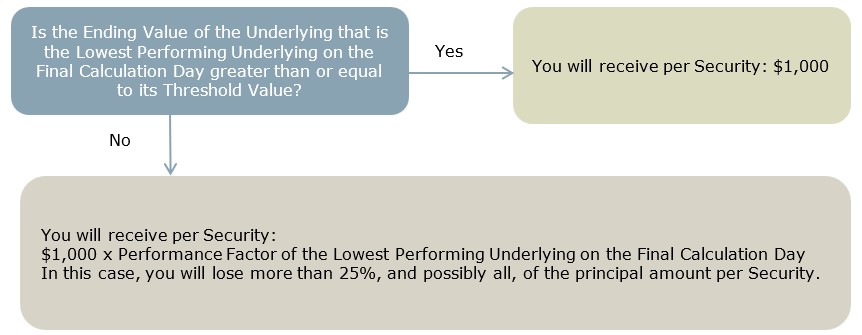

If we have not previously redeemed the Securities prior to the Maturity Date at our option, then at maturity you will receive (in addition to the final Contingent Coupon Payment, if otherwise payable) a cash payment per Security (the Maturity Payment Amount) calculated as follows:

Step 1: Determine which Underlying is the Lowest Performing Underlying on the Final Calculation Day. The Lowest Performing Underlying on the Final Calculation Day is the Underlying with the lowest Performance Factor on the Final Calculation Day. The Performance Factor of an Underlying on the Final Calculation Day is its Ending Value as a percentage of its Starting Value (i.e., its Ending Value divided by its Starting Value).

Step 2: Calculate the Maturity Payment Amount based on the Ending Value of the Lowest Performing Underlying, as follows:

PS-7

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028

|

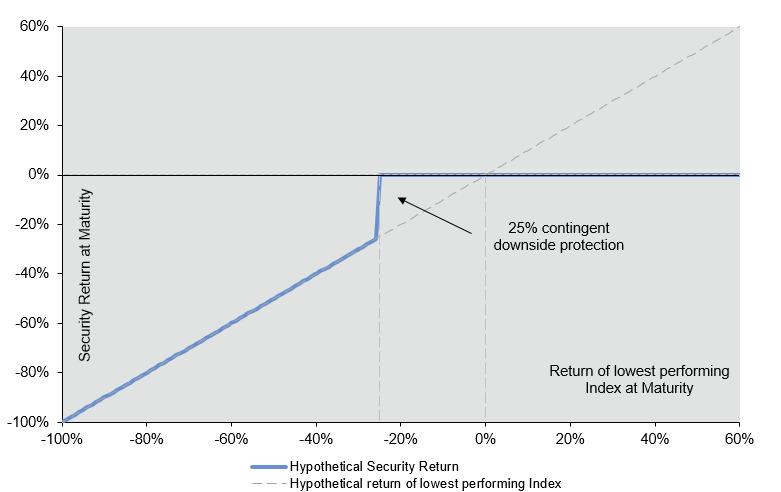

Hypothetical Payout Profile |

The following profile illustrates the potential Maturity Payment Amount on the Securities (excluding the final Contingent Coupon Payment, if any) for a range of hypothetical performances of the Lowest Performing Underlying on the Final Calculation Day from its Starting Value to its Ending Value, assuming the Securities have not been redeemed prior to the Maturity Date. As this profile illustrates, in no event will you have a positive rate of return based solely on the Maturity Payment Amount received at maturity; any positive return will be based solely on the Contingent Coupon Payments, if any, received during the term of the Securities. This graph has been prepared for purposes of illustration only. Your actual return will depend on the actual Ending Value of the Lowest Performing Underlying on the Final Calculation Day and whether you hold your Securities to the Maturity Date. The performance of the better performing Underlyings is not relevant to your return on the Securities.

PS-8

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028

|

Selected Risk Considerations |

The Securities have complex features and investing in the Securities will involve risks not associated with an investment in conventional debt securities. Your decision to purchase the Securities should be made only after carefully considering the risks of an investment in the Securities, including those discussed below, with your advisors in light of your particular circumstances. The Securities are not an appropriate investment for you if you are not knowledgeable about significant elements of the Securities or financial matters in general. You should carefully review the more detailed explanation of risks relating to the Securities in the “Risk Factors” sections beginning on page PS-5 of the accompanying product supplement, page S-6 of the accompanying prospectus supplement and page 7 of the accompanying prospectus.

Structure-related Risks

Your investment may result in a loss; there is no guaranteed return of principal. There is no fixed principal repayment amount on the Securities at maturity. If we do not redeem the Securities prior to maturity and the Ending Value of any Underlying is less than its Threshold Value, at maturity you will lose 1% of the principal amount for each 1% that the Ending Value of the Lowest Performing Underlying is less than its Starting Value. In that case, you will lose a significant portion or all of your investment in the Securities.

Your return on the Securities is limited to the return represented by the Contingent Coupon Payments, if any, over the term of the Securities. Your return on the Securities is limited to the Contingent Coupon Payments paid over the term of the Securities, regardless of the extent to which the closing level of any Underlying on any Calculation Day or the Ending Value of any Underlying exceeds its Coupon Barrier or Starting Value, as applicable. Similarly, the amount payable at maturity or upon early redemption will never exceed the sum of the principal amount and the applicable Contingent Coupon Payment, regardless of the extent to which the closing level of any Underlying on any Calculation Day exceeds its Starting Value. In contrast, a direct investment in the securities included in one or more of the Underlyings would allow you to receive the benefit of any appreciation in their values. Thus, any return on the Securities will not reflect the return you would realize if you actually owned those securities and received the dividends paid or distributions made on them.

The Securities are subject to a potential early redemption, which would limit your ability to receive the Contingent Coupon Payments over the full term of the Securities. On each Optional Redemption Date we may, at our option, redeem your Securities in whole, but not in part. If the Securities are redeemed prior to the Maturity Date, you will be entitled to receive the Stated Principal Amount plus any Contingent Coupon Payment otherwise due, and no further amounts will be payable on the Securities. In this case, you will lose the opportunity to continue to receive Contingent Coupon Payments after the date of the early redemption. If the Securities are redeemed prior to the Maturity Date, you may be unable to invest in other securities with a similar level of risk that could provide a return that is similar to the Securities. Even if we do not exercise our option to redeem your Securities, our ability to do so may adversely affect the market value of your Securities. It is our sole option whether to redeem your Securities prior to maturity on any Optional Redemption Date and we may or may not exercise this option for any reason. Because of this, the term of your Securities could be as short as approximately six months.

It is more likely that we will redeem the Securities in our sole discretion prior to maturity to the extent that the expected Contingent Coupon Payments payable on the Securities are greater than the coupon that would be payable on other instruments issued by us of comparable maturity, terms and credit rating trading in the market. The greater likelihood of us redeeming the Securities in that environment increases the risk that you will not be able to reinvest the proceeds from the redeemed Securities in another investment that provides a similar yield with a similar level of risk. We are less likely to redeem the Securities prior to maturity when the expected Contingent Coupon Payments payable on the Securities are less than the coupon that would be payable on other comparable instruments issued by us, which includes when the level of any of the Underlyings is less than its Coupon Barrier. Therefore, the Securities are more likely to remain outstanding when the expected Contingent Coupon Payments payable on the Securities are less than what would be payable on other comparable instruments and when your risk of not receiving a coupon is relatively higher.

You may not receive any Contingent Coupon Payments. The Securities do not provide for any regular fixed coupon payments. Investors in the Securities will not necessarily receive any Contingent Coupon Payments on the Securities. If the closing level of the Lowest Performing Underlying on a Calculation Day is less than its Coupon Barrier, you will not receive the Contingent Coupon Payment applicable to that Calculation Day. If the closing level of the Lowest Performing Underlying is less than its Coupon Barrier on all the Calculation Days during the term of the Securities, you will not receive any Contingent Coupon Payments during the term of the Securities, and you will not receive a positive return on the Securities.

Because the Securities are linked to the lowest performing (and not the average performance) of the Underlyings, you may not receive any return on the Securities and may lose a significant portion or all of your principal amount even if the closing level of one Underlying is always greater than or equal to its Coupon Barrier or Threshold Value, as applicable. Your Securities are linked to the lowest performing of the Underlyings, and a change in the level of one Underlying may not correlate with changes in the level of the other Underlying(s). The Securities are not linked to a basket composed of the Underlyings, where the depreciation in the level of one Underlying could be offset to some extent by the appreciation in the level of the other Underlying(s). In the case of the Securities, the individual performance of each Underlying would not be combined, and the depreciation in the level of one Underlying would not be offset by any appreciation in the level of the other Underlying(s). Even if the closing level of an Underlying is at or above its Coupon Barrier on a Calculation Day, you will not receive the Contingent Coupon Payment with respect to that Calculation Day if the closing level of another Underlying is below its Coupon Barrier on that day. In addition, even if the Ending

PS-9

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028

Value of an Underlying is at or above its Threshold Value, you will lose a portion of your principal if the Ending Value of the Lowest Performing Underlying is below its Threshold Value.

Higher Contingent Coupon Rates are associated with greater risk. The Securities offer Contingent Coupon Payments at a higher rate, if paid, than the fixed rate we would pay on conventional debt securities of the same maturity. These higher potential Contingent Coupon Payments are associated with greater levels of expected risk as of the Pricing Date as compared to conventional debt securities, including the risk that you may not receive a Contingent Coupon Payment on one or more, or any, Contingent Coupon Payment Dates and the risk that you may lose a substantial portion, and possibly all, of the principal amount per Security at maturity. The volatility of the Underlyings and the correlation among the Underlyings are important factors affecting this risk. Volatility is a measurement of the size and frequency of daily fluctuations in the level of an Underlying, typically observed over a specified period of time. Volatility can be measured in a variety of ways, including on a historical basis or on an expected basis as implied by option prices in the market. Correlation is a measurement of the extent to which the levels of the Underlyings tend to fluctuate at the same time, in the same direction and in similar magnitudes. Greater expected volatility of the Underlyings or lower expected correlation among the Underlyings as of the Pricing Date may result in a higher Contingent Coupon Rate, but it also represents a greater expected likelihood as of the Pricing Date that the closing level of at least one Underlying will be less than its Coupon Barrier on one or more Calculation Days, such that you will not receive one or more, or any, Contingent Coupon Payments during the term of the Securities, and that the closing level of at least one Underlying will be less than its Threshold Value on the Final Calculation Day such that you will lose a substantial portion, and possibly all, of the principal amount per Security at maturity. In general, the higher the Contingent Coupon Rate is relative to the fixed rate we would pay on conventional debt securities, the greater the expected risk that you will not receive one or more, or any, Contingent Coupon Payments during the term of the Securities and that you will lose a substantial portion, and possibly all, of the principal amount per Security at maturity.

Your return on the Securities may be less than the yield on a conventional debt security of comparable maturity. Any return that you receive on the Securities may be less than the return you would earn if you purchased a conventional debt security with the same Maturity Date. As a result, your investment in the Securities may not reflect the full opportunity cost to you when you consider factors, such as inflation, that affect the time value of money. In addition, if interest rates increase during the term of the Securities, the Contingent Coupon Payment (if any) may be less than the yield on a conventional debt security of comparable maturity.

A Contingent Coupon Payment Date, an Optional Redemption Date and the Maturity Date may be postponed if a Calculation Day is postponed.

A Calculation Day (including the Final Calculation Day) with respect to an Underlying will be postponed if the applicable originally scheduled Calculation Day is not a trading day with respect to any Underlying or if the calculation agent determines that a Market Disruption Event has occurred or is continuing with respect to that Underlying on that Calculation Day. If such a postponement occurs with respect to a Calculation Day other than the Final Calculation Day, then the related Contingent Coupon Payment Date, will be postponed. If such a postponement occurs with respect to the Final Calculation Day, the Maturity Date will be the later of (i) the initial Maturity Date and (ii) three business days after the last Final Calculation Day as postponed.

Any payment on the Securities is subject to our credit risk and the credit risk of the Guarantor, and actual or perceived changes in our or the Guarantor’s creditworthiness are expected to affect the value of the Securities. The Securities are our senior unsecured debt securities. Any payment on the Securities will be fully and unconditionally guaranteed by the Guarantor. The Securities are not guaranteed by any entity other than the Guarantor. As a result, your receipt of any Contingent Coupon Payments or the payment upon an early redemption or the Maturity Payment Amount at maturity, as applicable, will be dependent upon our ability and the ability of the Guarantor to repay our respective obligations under the Securities on the applicable payment date, regardless of the closing level of the Lowest Performing Underlying as compared to its Starting Value. No assurance can be given as to what our financial condition or the financial condition of the Guarantor will be at any time after the Pricing Date of the Securities. If we and the Guarantor become unable to meet our respective financial obligations as they become due, you may not receive the amount(s) payable under the terms of the Securities.

In addition, our credit ratings and the credit ratings of the Guarantor are assessments by ratings agencies of our respective abilities to pay our obligations. Consequently, our or the Guarantor’s perceived creditworthiness and actual or anticipated decreases in our or the Guarantor’s credit ratings or increases in the spread between the yield on our respective securities and the yield on U.S. Treasury securities (the “credit spread”) prior to the Maturity Date of your Securities may adversely affect the market value of the Securities. However, because your return on the Securities depends upon factors in addition to our ability and the ability of the Guarantor to pay our respective obligations, such as the levels of the Underlyings, an improvement in our or the Guarantor’s credit ratings will not reduce the other investment risks related to the Securities.

We are a finance subsidiary and, as such, have no independent assets, operations or revenues. We are a finance subsidiary of the Guarantor, have no operations other than those related to the issuance, administration and repayment of our debt securities that are guaranteed by the Guarantor, and are dependent upon the Guarantor and/or its other subsidiaries to meet our obligations under the Securities in the ordinary course. Therefore, our ability to make payments on the Securities may be limited.

Valuation- and Market-related Risks

The public offering price you are paying for the Securities exceeds their initial estimated value. The initial estimated value of the Securities that is provided on the cover page of this pricing supplement is an estimate only, determined as of the Pricing Date by

PS-10

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028

reference to our and our affiliates’ pricing models. These pricing models consider certain assumptions and variables, including our credit spreads and those of the Guarantor, the Guarantor’s internal funding rate, mid-market terms on hedging transactions, expectations on interest rates, dividends and volatility, price-sensitivity analysis, and the expected term of the Securities. These pricing models rely in part on certain forecasts about future events, which may prove to be incorrect. If you attempt to sell the Securities prior to maturity, their market value may be lower than the price you paid for them and lower than their initial estimated value. This is due to, among other things, changes in the levels of the Underlyings, changes in the Guarantor’s internal funding rate, and the inclusion in the public offering price of the underwriting discount and the hedging related charges, all as further described in "Structuring the Securities" below. These factors, together with various credit, market and economic factors over the term of the Securities, are expected to reduce the price at which you may be able to sell the Securities in any secondary market and will affect the value of the Securities in complex and unpredictable ways.

The initial estimated value does not represent a minimum or maximum price at which we, BAC, BofAS or any of our other affiliates or WFS or its affiliates would be willing to purchase your Securities in any secondary market (if any exists) at any time. The value of your Securities at any time after issuance will vary based on many factors that cannot be predicted with accuracy, including the performance of the Underlyings, our and BAC’s creditworthiness and changes in market conditions.

We cannot assure you that a trading market for your Securities will ever develop or be maintained. We will not list the Securities on any securities exchange. We cannot predict how the Securities will trade in any secondary market or whether that market will be liquid or illiquid.

The Securities are not designed to be short-term trading instruments, and if you attempt to sell the Securities prior to maturity, their market value, if any, will be affected by various factors that interrelate in complex ways, and their market value may be less than the principal amount. The following factors are expected to affect the value of the Securities: value of the Underlyings at such time; volatility of the Underlyings; economic and other conditions generally; interest rates; dividend yields; exchange rate movements and volatility; our and the Guarantor’s financial condition and creditworthiness; and time to maturity.

Conflict-related Risks

Trading and hedging activities by us, the Guarantor and any of our other affiliates, including BofAS, and WFS and its affiliates, may create conflicts of interest with you and may affect your return on the Securities and their market value. We, the Guarantor or one or more of our other affiliates, including BofAS, and WFS and its affiliates, may buy or sell the securities held by or included in the Underlyings, or futures or options contracts on the Underlyings or those securities, or other listed or over-the-counter derivative instruments linked to the Underlyings or those securities. While we, the Guarantor or one or more of our other affiliates, including BofAS, and WFS and its affiliates, may from time to time own securities represented by the Underlyings, except to the extent that BAC’s or Wells Fargo & Company’s (the parent company of WFS) common stock may be included in the Underlyings, as applicable, we, the Guarantor and our other affiliates, including BofAS, and WFS and its affiliates, do not control any company included in the Underlyings, and have not verified any disclosure made by any other company. We, the Guarantor or one or more of our other affiliates, including BofAS, or WFS and its affiliates, may execute such purchases or sales for our own or their own accounts, for business reasons, or in connection with hedging our obligations under the Securities. These transactions may present a conflict of interest between your interest in the Securities and the interests we, the Guarantor and our other affiliates, including BofAS, and WFS and its affiliates, may have in our or their proprietary accounts, in facilitating transactions, including block trades, for our or their other customers, and in accounts under our or their management. These transactions may adversely affect the levels of the Underlyings in a manner that could be adverse to your investment in the Securities. On or before the Pricing Date, any purchases or sales by us, the Guarantor or our other affiliates, including BofAS or others on its behalf, and WFS and its affiliates (including for the purpose of hedging some or all of our anticipated exposure in connection with the Securities), may have affected the levels of the Underlyings. Consequently, the levels of the Underlyings may change subsequent to the Pricing Date, which may adversely affect the market value of the Securities.

We, the Guarantor or one or more of our other affiliates, including BofAS, and WFS and its affiliates, also may have engaged in hedging activities that could have affected the levels of the Underlyings on the Pricing Date. In addition, these hedging activities, including the unwinding of a hedge, may decrease the market value of your Securities prior to maturity, and may affect the amounts to be paid on the Securities. We, the Guarantor or one or more of our other affiliates, including BofAS, and WFS and its affiliates, may purchase or otherwise acquire a long or short position in the Securities and may hold or resell the Securities. For example, BofAS may enter into these transactions in connection with any market making activities in which it engages. We cannot assure you that these activities will not adversely affect the levels of the Underlyings, the market value of your Securities prior to maturity or the amounts payable on the Securities.

If WFS, BofAS or an affiliate of either selling agent participating as a dealer in the distribution of the Securities conducts hedging activities for us in connection with the Securities, such selling agent or participating dealer will expect to realize a projected profit from such hedging activities, and this projected profit will be in addition to any discount, concession or fee received in connection with the sale of the Securities to you. This additional projected profit may create a further incentive for the selling agents or participating dealers to sell the Securities to you.

There may be potential conflicts of interest involving the calculation agent, which is an affiliate of ours. We have the right to appoint and remove the calculation agent. One of our affiliates will be the calculation agent for the Securities and, as such, will make a variety of determinations relating to the Securities, including the amounts that will be paid on the Securities. Under some

PS-11

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028

circumstances, these duties could result in a conflict of interest between its status as our affiliate and its responsibilities as calculation agent.

Underlying-related Risks

Any payments on the Securities will depend upon the performance of the Underlyings, and therefore the Securities are subject to the following risks, each as discussed in more detail in the accompanying product supplement.

● |

Changes that affect the Underlyings may adversely affect the value of the Securities and any payments on the Securities. |

● |

We and our affiliates have no affiliation with any index sponsor and have not independently verified their public disclosure of information. |

The Securities are subject to risks associated with small-size capitalization companies. The stocks comprising the RTY are issued by companies with small-sized market capitalization. The stock prices of small-size companies may be more volatile than stock prices of large capitalization companies. Small-size capitalization companies may be less able to withstand adverse economic, market, trade and competitive conditions relative to larger companies. Small-size capitalization companies may also be more susceptible to adverse developments related to their products or services.

Tax-related Risks

The U.S. federal income tax consequences of the Securities are uncertain, and may be adverse to a holder of the Securities. See “U.S. Federal Income Tax Summary” below and “U.S. Federal Income Tax Summary” beginning on page PS-36 of the accompanying product supplement.

PS-12

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028

If we redeem the Securities prior to the Maturity Date:

If we redeem the Securities prior to the Maturity Date, you will receive the principal amount of your Securities plus, if otherwise due, any Contingent Coupon Payment on the applicable Optional Redemption Date. In the event we redeem the Securities prior to the Maturity Date, your total return on the Securities will equal any Contingent Coupon Payments received prior to the Optional Redemption Date and any Contingent Coupon Payment received on the Optional Redemption Date.

If we do not redeem the Securities prior to the Maturity Date:

If we do not redeem the Securities prior to the Maturity Date, the following table illustrates, for a range of hypothetical Performance Factors of the Lowest Performing Underlying on the Final Calculation Day, the hypothetical Maturity Payment Amount payable at maturity per Security (excluding the final Contingent Coupon Payment, if any). The Performance Factor of the Lowest Performing Underlying on the Final Calculation Day is its Ending Value expressed as a percentage of its Starting Value (i.e., its Ending Value divided by its Starting Value).

|

Hypothetical Performance Factor of Lowest Performing Underlying on Final Calculation Day |

Hypothetical Maturity Payment Amount per Security |

175.00% |

$1,000.00 |

160.00% |

$1,000.00 |

150.00% |

$1,000.00 |

140.00% |

$1,000.00 |

130.00% |

$1,000.00 |

120.00% |

$1,000.00 |

110.00% |

$1,000.00 |

100.00% |

$1,000.00 |

90.00% |

$1,000.00 |

80.00% |

$1,000.00 |

75.00% |

$1,000.00 |

74.00% |

$740.00 |

70.00% |

$700.00 |

60.00% |

$600.00 |

50.00% |

$500.00 |

40.00% |

$400.00 |

30.00% |

$300.00 |

25.00% |

$250.00 |

The above figures do not take into account Contingent Coupon Payments, if any, received during the term of the Securities. As evidenced above, in no event will you have a positive rate of return based solely on the Maturity Payment Amount received at maturity; any positive return will be based solely on the Contingent Coupon Payments, if any, received during the term of the Securities.

The above figures are for purposes of illustration only and may have been rounded for ease of analysis. If the Securities are not redeemed at our option prior to the Maturity Date, the actual amount you will receive on the Maturity Date will depend on the actual Ending Value of the Lowest Performing Underlying on the Final Calculation Day. The performance of the better performing Underlyings is not relevant to your return on the Securities.

PS-13

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028

|

Hypothetical Contingent Coupon Payments |

Set forth below are examples that illustrate how to determine whether a Contingent Coupon Payment will be paid on a Contingent Coupon Payment Date, assuming we have not redeemed the Securities prior to such date. The examples do not reflect any specific Contingent Coupon Payment Date. The following examples reflect the Contingent Coupon Rate of 8.15% per annum and assume the hypothetical Starting Value, Coupon Barrier and closing level for each Underlying indicated in the examples. The terms used for purposes of these hypothetical examples do not represent any actual Starting Value or Coupon Barrier. The hypothetical Starting Value of 100.00 for each Underlying has been chosen for illustrative purposes only and does not represent the actual Starting Value for any Underlying. The actual Starting Value and Coupon Barrier for each Underlying are set forth under “Terms of the Securities” above. For historical data regarding the actual closing levels of the Underlyings, see the historical information provided herein. These examples are for purposes of illustration only and the values used in the examples may have been rounded for ease of analysis. If we were to redeem the Securities on the relevant Contingent Coupon Payment Date in either of the examples below, you would receive the principal amount on the Contingent Coupon Payment Date in addition to a final Contingent Coupon Payment, if otherwise payable.

Example 1. The closing level of the Lowest Performing Underlying on the relevant Calculation Day is greater than or equal to its Coupon Barrier. As a result, investors receive a Contingent Coupon Payment on the applicable Contingent Coupon Payment Date.

|

S&P 500® Index |

Russell 2000® Index |

Dow Jones Industrial Average® |

Hypothetical Starting Value: |

100.00 |

100.00 |

100.00 |

Hypothetical closing level on relevant Calculation Day: |

90.00 |

95.00 |

80.00 |

Hypothetical Coupon Barrier: |

75.00 |

75.00 |

75.00 |

Performance Factor on Calculation Day (closing level on Calculation Day divided by Starting Value): |

90.00% |

95.00% |

80.00% |

Step 1: Determine which Underlying is the Lowest Performing Underlying on the relevant Calculation Day.

In this example, the Dow Jones Industrial Average® has the lowest Performance Factor and is, therefore, the Lowest Performing Underlying on the relevant Calculation Day.

Step 2: Determine whether a Contingent Coupon Payment will be paid on the applicable Contingent Coupon Payment Date.

Since the hypothetical closing level of the Lowest Performing Underlying on the relevant Calculation Day is greater than or equal to its Coupon Barrier, you would receive a Contingent Coupon Payment on the applicable Contingent Coupon Payment Date. The Contingent Coupon Payment would be equal to $20.375 per Security, determined as follows: (i) $1,000 multiplied by 8.15% per annum divided by (ii) 4, rounded to the nearest cent.

Example 2. The closing level of the Lowest Performing Underlying on the relevant Calculation Day is less than its Coupon Barrier. As a result, investors do not receive a Contingent Coupon Payment on the applicable Contingent Coupon Payment Date.

|

S&P 500® Index |

Russell 2000® Index |

Dow Jones Industrial Average® |

Hypothetical Starting Value: |

100.00 |

100.00 |

100.00 |

Hypothetical closing level on relevant Calculation Day: |

69.00 |

125.00 |

105.00 |

Hypothetical Coupon Barrier: |

75.00 |

75.00 |

75.00 |

Performance Factor on Calculation Day (closing level on Calculation Day divided by Starting Value): |

69.00% |

125.00% |

105.00% |

Step 1: Determine which Underlying is the Lowest Performing Underlying on the relevant Calculation Day.

In this example, the S&P 500® Index has the lowest Performance Factor and is, therefore, the Lowest Performing Underlying on the relevant Calculation Day.

Step 2: Determine whether a Contingent Coupon Payment will be paid on the applicable Contingent Coupon Payment Date.

Since the hypothetical closing level of the Lowest Performing Underlying on the relevant Calculation Day is less than its Coupon Barrier, you would not receive a Contingent Coupon Payment on the applicable Contingent Coupon Payment Date. This is the case even though the closing levels of the better performing Underlyings were greater than their respective Coupon Barriers on the relevant Calculation Day.

As this example illustrates, whether you receive a Contingent Coupon Payment on a Contingent Coupon Payment Date will depend solely on the closing level of the Lowest Performing Underlying on the relevant Calculation Day. This will be the case even if the better performing indices perform favorably. The performance of the better performing Underlyings is not relevant to your return on the Securities.

PS-14

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028

|

Hypothetical Payment at the Maturity Date |

Set forth below are examples of calculations of the Maturity Payment Amount payable on the Maturity Date, assuming that we have not redeemed the Securities prior to the Maturity Date and assuming the hypothetical Starting Value, Coupon Barrier, Threshold Value and Ending Value for each Underlying indicated in the examples. The terms used for purposes of these hypothetical examples do not represent any actual Starting Value, Coupon Barrier or Threshold Value. The hypothetical Starting Value of 100.00 for each Underlying has been chosen for illustrative purposes only and does not represent the actual Starting Value for any Underlying. The actual Starting Value, Coupon Barrier and Threshold Value for each Underlying are set forth under “Terms of the Securities” above. For historical data regarding the actual closing levels of the Underlyings, see the historical information provided herein. These examples are for purposes of illustration only and the values used in the examples may have been rounded for ease of analysis.

Example 1. The Ending Value of the Lowest Performing Underlying on the Final Calculation Day is greater than its Starting Value, the Maturity Payment Amount is equal to the principal amount of your Securities at maturity and you receive a final Contingent Coupon Payment:

|

S&P 500® Index |

Russell 2000® Index |

Dow Jones Industrial Average® |

Hypothetical Starting Value: |

100.00 |

100.00 |

100.00 |

Hypothetical Ending Value: |

145.00 |

135.00 |

125.00 |

Hypothetical Coupon Barrier: |

75.00 |

75.00 |

75.00 |

Hypothetical Threshold Value: |

75.00 |

75.00 |

75.00 |

Performance Factor (Ending Value divided by Starting Value): |

145.00% |

135.00% |

125.00% |

Step 1: Determine which Underlying is the Lowest Performing Underlying on the Final Calculation Day.

In this example, the Dow Jones Industrial Average® has the lowest Performance Factor and is, therefore, the Lowest Performing Underlying on the Final Calculation Day.

Step 2: Determine the Maturity Payment Amount based on the Ending Value of the Lowest Performing Underlying on the Final Calculation Day.

Since the hypothetical Ending Value of the Lowest Performing Underlying on the Final Calculation Day is greater than or equal to its hypothetical Threshold Value, the Maturity Payment Amount would equal the principal amount. Although the hypothetical Ending Value of the Lowest Performing Underlying on the Final Calculation Day is significantly greater than its hypothetical Starting Value in this scenario, the Maturity Payment Amount will not exceed the principal amount.

In addition to any Contingent Coupon Payments received during the term of the Securities, on the Maturity Date you would receive $1,000.00 per Security. In addition, because the hypothetical Ending Value of the Lowest Performing Underlying on the Final Calculation Day is greater than its hypothetical Coupon Barrier, you would receive a final Contingent Coupon Payment on the Maturity Date.

Example 2. The Ending Value of the Lowest Performing Underlying on the Final Calculation Day is less than its Starting Value but greater than its Threshold Value and its Coupon Barrier, the Maturity Payment Amount is equal to the principal amount of your Securities at maturity and you receive a final Contingent Coupon Payment:

|

S&P 500® Index |

Russell 2000® Index |

Dow Jones Industrial Average® |

Hypothetical Starting Value: |

100.00 |

100.00 |

100.00 |

Hypothetical Ending Value: |

80.00 |

115.00 |

110.00 |

Hypothetical Coupon Barrier: |

75.00 |

75.00 |

75.00 |

Hypothetical Threshold Value: |

75.00 |

75.00 |

75.00 |

Performance Factor (Ending Value divided by Starting Value): |

80.00% |

115.00% |

110.00% |

Step 1: Determine which Underlying is the Lowest Performing Underlying on the Final Calculation Day.

In this example, the S&P 500® Index has the lowest Performance Factor and is, therefore, the Lowest Performing Underlying on the Final Calculation Day.

Step 2: Determine the Maturity Payment Amount based on the Ending Value of the Lowest Performing Underlying on the Final Calculation Day.

PS-15

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028

Since the hypothetical Ending Value of the Lowest Performing Underlying is less than its hypothetical Starting Value, but not by more than 25%, you would be repaid the principal amount of your Securities at maturity.

In addition to any Contingent Coupon Payments received during the term of the Securities, on the Maturity Date you would receive $1,000.00 per Security. In addition, because the hypothetical Ending Value of the Lowest Performing Underlying on the Final Calculation Day is greater than its Coupon Barrier, you would receive a final Contingent Coupon Payment on the Maturity Date.

Example 3. The Ending Value of the Lowest Performing Underlying on the Final Calculation Day is less than its Threshold Value and its Coupon Barrier, the Maturity Payment Amount is less than the principal amount of your Securities at maturity and you do not receive a final Contingent Coupon Payment:

|

S&P 500® Index |

Russell 2000® Index |

Dow Jones Industrial Average® |

Hypothetical Starting Value: |

100.00 |

100.00 |

100.00 |

Hypothetical Ending Value: |

120.00 |

45.00 |

90.00 |

Hypothetical Coupon Barrier: |

75.00 |

75.00 |

75.00 |

Hypothetical Threshold Value: |

75.00 |

75.00 |

75.00 |

Performance Factor (Ending Value divided by Starting Value): |

120.00% |

45.00% |

90.00% |

Step 1: Determine which Underlying is the Lowest Performing Underlying on the Final Calculation Day.

In this example, the Russell 2000® Index has the lowest Performance Factor and is, therefore, the Lowest Performing Underlying on the Final Calculation Day.

Step 2: Determine the Maturity Payment Amount based on the Ending Value of the Lowest Performing Underlying on the Final Calculation Day.

Since the hypothetical Ending Value of the Lowest Performing Underlying on the Final Calculation Day is less than its hypothetical Threshold Value, you would lose a portion of the principal amount of your Securities and receive the Maturity Payment Amount equal to $450.00 per Security, calculated as follows:

= $1,000 × Performance Factor of the Lowest Performing Underlying on the Final Calculation Day

= $1,000 × 45.00%

= $450.00

In addition to any Contingent Coupon Payments received during the term of the Securities, on the Maturity Date you would receive $450.00 per Security. Because the hypothetical Ending Value of the Lowest Performing Underlying on the Final Calculation Day is less than its Coupon Barrier, you would not receive a final Contingent Coupon Payment on the Maturity Date.

These examples illustrate that you will not participate in any appreciation of any Underlying, but will be fully exposed to a decrease in the Lowest Performing Underlying if the Ending Value of the Lowest Performing Underlying on the Final Calculation Day is less than its Threshold Value, even if the Ending Values of the other Underlyings have appreciated or have not declined below their respective Threshold Values.

To the extent that the Starting Value, Coupon Barrier, Threshold Value and Ending Value of the Lowest Performing Underlying differ from the values assumed above, the results indicated above would be different.

PS-16

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028

All disclosures contained in this pricing supplement regarding the Underlyings, including, without limitation, their make-up, method of calculation, and changes in their components, have been derived from publicly available sources. The information reflects the policies of, and is subject to change by, each of S&P Dow Jones Indices LLC (“SPDJI”), the sponsor of each of the SPX and the INDU, and FTSE Russell, the sponsor of the RTY. We refer to SPDJI and FTSE Russell as the “Underlying Sponsors”. The Underlying Sponsors, which license the copyright and all other rights to the respective Underlyings, have no obligation to continue to publish, and may discontinue publication of, the Underlyings. The consequences of any Underlying Sponsor discontinuing publication of the applicable Underlying are discussed in “General Terms of the Securities — Discontinuance of an Index” in the accompanying product supplement. None of us, the Guarantor, the calculation agent, or BofAS accepts any responsibility for the calculation, maintenance or publication of any Underlying or any successor index. None of us, the Guarantor, BofAS or any of our other affiliates makes any representation to you as to the future performance of the Underlyings. You should make your own investigation into the Underlyings.

|

The S&P 500® Index |

The SPX includes a representative sample of 500 companies in leading industries of the U.S. economy. The SPX is intended to provide an indication of the pattern of common stock price movement. The calculation of the level of the SPX is based on the relative value of the aggregate market value of the common stocks of 500 companies as of a particular time compared to the aggregate average market value of the common stocks of 500 similar companies during the base period of the years 1941 through 1943.

The SPX includes companies from eleven main groups: Communication Services; Consumer Discretionary; Consumer Staples; Energy; Financials; Health Care; Industrials; Information Technology; Real Estate; Materials; and Utilities. SPDJI may from time to time, in its sole discretion, add companies to, or delete companies from, the SPX to achieve the objectives stated above.

Company additions to the SPX must have an unadjusted company market capitalization of $18.0 billion or more (an increase from the previous requirement of an unadjusted company market capitalization of $15.8 billion or more).

SPDJI calculates the SPX by reference to the prices of the constituent stocks of the SPX without taking account of the value of dividends paid on those stocks. As a result, the return on the Securities will not reflect the return you would realize if you actually owned the SPX constituent stocks and received the dividends paid on those stocks.

Computation of the SPX

While SPDJI currently employs the following methodology to calculate the SPX, no assurance can be given that SPDJI will not modify or change this methodology in a manner that may affect payments on the Securities.

Historically, the market value of any component stock of the SPX was calculated as the product of the market price per share and the number of then outstanding shares of such component stock. In March 2005, SPDJI began shifting the SPX halfway from a market capitalization weighted formula to a float-adjusted formula, before moving the SPX to full float adjustment on September 16, 2005. SPDJI’s criteria for selecting stocks for the SPX did not change with the shift to float adjustment. However, the adjustment affects each company’s weight in the SPX.

Under float adjustment, the share counts used in calculating the SPX reflect only those shares that are available to investors, not all of a company’s outstanding shares. Float adjustment excludes shares that are closely held by control groups, other publicly traded companies or government agencies.

In September 2012, all shareholdings representing more than 5% of a stock’s outstanding shares, other than holdings by “block owners,” were removed from the float for purposes of calculating the SPX. Generally, these “control holders” will include officers and directors, private equity, venture capital and special equity firms, other publicly traded companies that hold shares for control, strategic partners, holders of restricted shares, ESOPs, employee and family trusts, foundations associated with the company, holders of unlisted share classes of stock, government entities at all levels (other than government retirement/pension funds) and any individual person who controls a 5% or greater stake in a company as reported in regulatory filings. However, holdings by block owners, such as depositary banks, pension funds, mutual funds and ETF providers, 401(k) plans of the company, government retirement/pension funds, investment funds of insurance companies, asset managers and investment funds, independent foundations and savings and investment plans, will ordinarily be considered part of the float.

Treasury stock, stock options, restricted shares, equity participation units, warrants, preferred stock, convertible stock, and rights are not part of the float. Shares held in a trust to allow investors in countries outside the country of domicile, such as depositary shares and Canadian exchangeable shares are normally part of the float unless those shares form a control block. If a company has multiple classes of stock outstanding, shares in an unlisted or non-traded class are treated as a control block.

For each stock, an investable weight factor (“IWF”) is calculated by dividing the available float shares by the total shares outstanding. Available float shares are defined as the total shares outstanding less shares held by control holders. This calculation is subject to a 5% minimum threshold for control blocks. For example, if a company’s officers and directors hold 3% of the company’s shares, and no other control group holds 5% of the company’s shares, SPDJI would assign that company an IWF of 1.00, as no control group meets the 5% threshold. However, if a company’s officers and directors hold 3% of the company’s shares and another control group holds 20% of the company’s shares, SPDJI would assign an IWF of 0.77, reflecting the fact that 23% of the company’s outstanding shares are considered to be held for control. As of July 31, 2017, companies with multiple share class lines are no longer eligible for inclusion in the SPX. Constituents of the SPX prior to July 31, 2017 with multiple share class lines will be grandfathered in and continue to be included in the

PS-17

Market Linked Securities—Callable with Contingent Coupon and Contingent Downside

Principal at Risk Securities Linked to the Lowest Performing of the S&P 500® Index, the Russell 2000® Index and the Dow Jones Industrial Average® due June 29, 2028

SPX. If a constituent company of the SPX reorganizes into a multiple share class line structure, that company will remain in the SPX at the discretion of the S&P Index Committee in order to minimize turnover.

The SPX is calculated using a base-weighted aggregate methodology. The level of the SPX reflects the total market value of all component stocks relative to the base period of the years 1941 through 1943. An indexed number is used to represent the results of this calculation in order to make the level easier to work with and track over time. The actual total market value of the component stocks during the base period of the years 1941 through 1943 has been set to an indexed level of 10. This is often indicated by the notation 1941- 43 = 10. In practice, the daily calculation of the SPX is computed by dividing the total market value of the component stocks by the “index divisor.” By itself, the index divisor is an arbitrary number. However, in the context of the calculation of the SPX, it serves as a link to the original base period level of the SPX. The index divisor keeps the SPX comparable over time and is the manipulation point for all adjustments to the SPX, which is index maintenance.

Index Maintenance

Index maintenance includes monitoring and completing the adjustments for company additions and deletions, share changes, stock splits, stock dividends, and stock price adjustments due to company restructuring or spinoffs. Some corporate actions, such as stock splits and stock dividends, require changes in the common shares outstanding and the stock prices of the companies in the SPX, and do not require index divisor adjustments.

To prevent the level of the SPX from changing due to corporate actions, corporate actions which affect the total market value of the SPX require an index divisor adjustment. By adjusting the index divisor for the change in market value, the level of the SPX remains constant and does not reflect the corporate actions of individual companies in the SPX. Index divisor adjustments are made after the close of trading and after the calculation of the SPX closing level.